1. FANG+ ETF Closes Below 50Day Moving Average….-11% from Highs

2. NVIDIA Closes Below 50-Day…-18% from Highs

3. AI Stock …SMCI -40% from Highs…

4. Tesla -20% from July Run Up

50day never made it thru 200day to upside on chart.

5. EV Inventory 125 Days

6. Chipotle Closes Below 200-Day

Not sure if CMG, UPS, MCD telling us consumers slowing down spending.

7. Shares Of Major French-Fry Supplier Crash As Restaurant Traffic Slowdown Worsens

ZEROHEDGE BY TYLER DURDEN

One of the world’s largest producers and processors of frozen french fries, waffle fries, and other frozen potato products reported fourth-quarter profit and sales that missed estimates. The company also issued a below-consensus full-year adjusted EBITDA outlook due to sliding global restaurant traffic. This is an ominous sign, as elevated inflation and high interest rates are squeezing consumers. Lamb Weston reported adjusted earnings per share of 78 cents for the fourth quarter ending May 26, which was well below analysts’ expectations tracked by Bloomberg of $1.25. Revenue also missed, coming in at $1.61, versus the average estimated $1.7 billion. Here’s a snapshot of fourth-quarter earnings (courtesy of Bloomberg):

Momentum activities like public speaking, board sports and leadership all share an attribute with riding a bicycle: It gets easier when you get good at it.

The first error we often make is believing that someone (even us) will never be good at riding a bike, because riding a bike is so difficult. When we’re not good at it, it’s obvious to everyone.

The second error is coming to the conclusion that people who are good at it are talented, born with the ability to do it. They’re not, they have simply earned a skill that translates into momentum.

There’s a difference between, “This person is a terrible public speaker,” and “this person will never be good at public speaking.”

And there’s a difference between, “They are a great leader,” and “they were born to lead.”

The thing about momentum activities is that we notice them only twice: when people are terrible at them, and when they’re good at it. That includes the person you see in the mirror.

Three Lower Highs in a Row for 2 year treasury yields…trend is down pulled back to early Feb 2024 levels.

3. Q2 2024 First Year Over Year Increase in IPOs Since 2021

From Zachary Goldberg Jefferies –Wall Street Horizon noted, the second quarter of 2024 marked the first year-on-year increase in new global #IPOs since Q3 2021 and the single most active quarter since Q3 2022.

4. UPS Stock Breaks Below 2023 Lows

5. AT&T Chart…Can T Break Out of 10-Year Range?

6. De-Globalization Will Not Be Easy

Bernstein Advisors Trade Deficit is at record levels.

8. The US housing-market logjam keeps getting worse

Business Insider

Existing home sales fell in June to nearly to their slowest pace since 2010.

The decline comes as home prices notched a record high in the same month.

Buyers are likely waiting for interest-rate cuts that would loosen financial conditions.

The pace of existing home sales fell close to a record low in June as record-high prices and persistently high mortgage rates turned buyers away. Data from the National Association of Realtors shows that sales slumped 5.4% from May to June, hitting an annualized rate of 3.89 million. That marks the one of the slowest paces since 2010. Adding to the reluctance of buyers was a second straight monthly record for home prices. The median existing-home price surging 4.1% year-to-year to $426,900. The two dynamics are combining to worsen a long-standing logjam in the housing market. While the issue was once a lack of inventory, home sales have stayed stagnant even as more units have come available. It’s likely buyers are waiting for interest rates to start declining.

9. American Mortgage Holders Loan to Value at Super Strong Levels

10. Most Followed Accounts On Instagram…Ronaldo and Messi

Aside from Instagram’s own account, Cristiano Ronaldo has the most followers on Instagram with over 600 million. Another soccer star Leo Messi currently ranks third for most Instagram followers, just over 100 million behind rival Ronaldo. With the exception of YouTube’s MrBeast and T-Series (over 260 million subscribers), each of Instagram’s top 20 accounts has more followers than all other social media accounts. 17 of the top 20 Instagram accounts are focused on a single person.

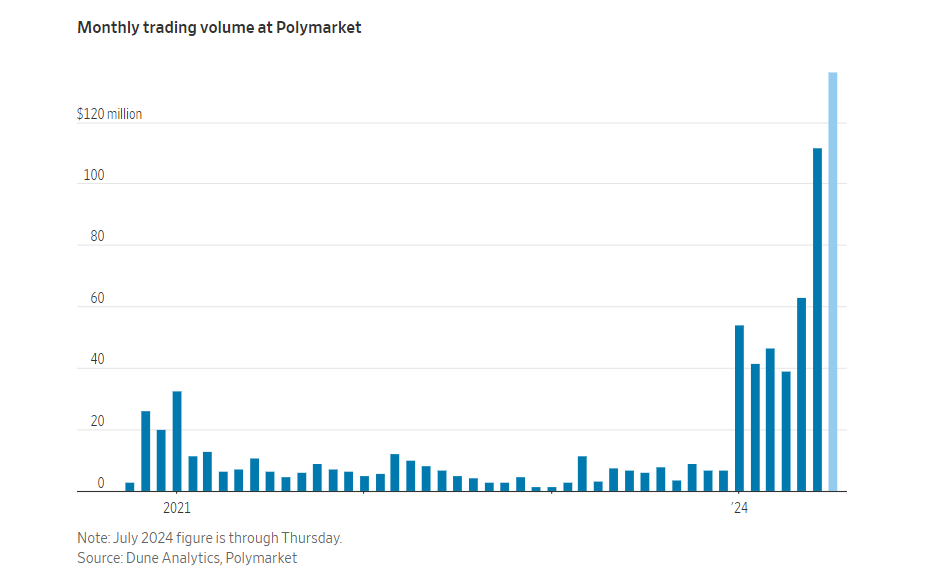

1. Trading on Polymarket Hits $112m…Bets on Politics, Sports, Pop Culture

WSJ Alexander Osipovich Welcome to the world of Polymarket, a four-year-old startup that offers bets on politics, sports, pop culture and pretty much anything else. Trading volumes on Polymarket hit a record $112 million in June and have already exceeded that level so far this month. Activity rose sharply after the June 27 presidential debate, in which President Biden’s disastrous performance unleashed speculation that he would drop out of the race.

Mega-Cap Tech drove 2023-2024 rally…small cap tech still below 2021 highs.

4. Manhattan Real Estate Manager SL Green +205% from Lows

Yahoo Finance Description-SL Green Realty Corp., Manhattan’s largest office landlord, is a fully integrated real estate investment trust, or REIT, that is focused primarily on acquiring, managing and maximizing value of Manhattan commercial properties. As of September 30, 2023, SL Green held interests in 59 buildings totaling 32.5 million square feet. This included ownership interests in 28.8 million square feet of Manhattan buildings and 2.8 million square feet securing debt and preferred equity investments.

50- week about to go thru 200week to upside.

5. CRWD -30% Correction but Still in Green for 2024

CRWD close to next support

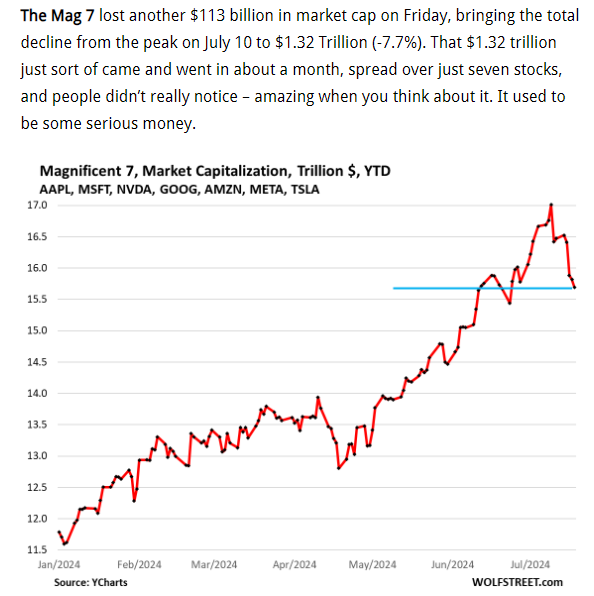

6. Mag 7 Lost $1.32 Trillion from Highs…A Blip on Long-Term Chart

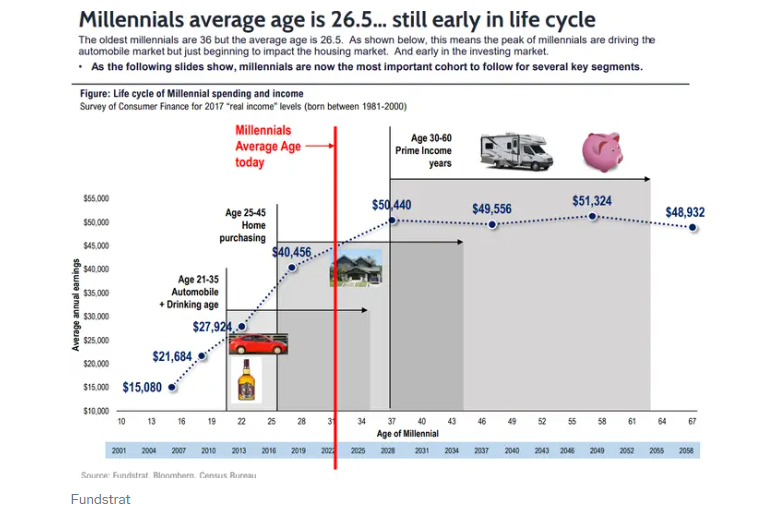

Business Insider Tom Lee Fundstrat Lee put the chart above together several years ago, but his thesis remains the same. The average age of millennials is now around 31 years old, and the global cohort of 2.5 billion people is starting to enter its prime age years of 30-50 years old. “This would be the third time that stocks entered a cycle where annual returns compound at high teens. You had the roaring 20’s, and then you had the 50’s through the late 60’s, and this is a third cycle,” Lee told CNBC last month. “They all coincided with a surge in the number of people aged 30-50, so in other words the number of prime age adults, and this time it’s powered by millennials and Gen Z.”

10. Why you are probably sitting down for too long -BBC

Annabel Bourne Sitting down for prolonged periods can have a profound effect on our health In the office, on transport, at home…Sitting down is ingrained in most peoples’ days. But, due in part to vascular dysfunction, staying sedentary for too long can increase the risk of serious health conditions like cardiovascular disease and type 2 diabetes. In 1953, epidemiologist Jeremy Morris found that London bus drivers were more than twice as likely as bus conductors to develop coronary heart disease. Demographically (in age, sex and income range) the two groups of workers were the same, so why was there such a significant difference? Morris’ answer: bus conductors were required to be on their feet and regularly climb the steps of London’s iconic double-decker buses as they sold tickets to passengers, whereas the drivers remained seated for long stretches of time. His landmark study laid the groundwork for research on the links between physical activity and coronary health. Whilst London bus conductors may now be a thing of the past, Morris’ results are more relevant than ever. Since the Covid-19 pandemic, there has been a huge shift towards working from home, which is likely to increase our collective sitting time.

Why does sedentary behaviour increase risk of cardiovascular disease? The primary hypothesis is increased vascular dysfunction, particularly in the legs. The vascular system is responsible for keeping blood and lymph fluid – which forms part of the immune system – moving through the blood vessels. David Dunstan, a physiologist at Deakin University’s Institute for Physical Activity and Nutrition, in Melbourne, Australia, has extensively researched the effects of prolonged sitting and possible interventions. “What characterises sitting is a reduction in muscular activity,” says Dunstan. “If I’m on a chair, the chair is taking all the responsibility there.” The combined effect of reduced muscular activity, lower metabolic demand and gravitational forces decreases peripheral blood flow to the leg muscles, which can lead to blood pooling in the calves. The biomechanics of sitting, with the legs usually bent, can also reduce blood flow. Researchers suggest that 120-180 minutes of prolonged sitting is the threshold of too long spent seated Reduced muscular activity of the leg muscles reduces their metabolic demand. Metabolic demand is the primary determinant of blood flow, so blood flow in the legs is also reduced. The biomechanics of sitting, with the legs usually bent can cause to blood pool in the calves – one study of 21 young healthy volunteers saw their calves increase in circumference by nearly 1cm (0.4in) over the course of two hours. This can also reduce blood flow.

Reduced blood flow, however, reduces shear stress, and the endothelium produces vasoconstrictors like endothelin-1 which cause the blood vessels to narrow. In a vicious cycle, vasoconstriction further reduces blood flow, and blood pressure rises to keep the blood moving. High blood pressure, or hypertension, is one of the predominant risk factors for cardiovascular disease. “That’s [vascular dysfunction] one of the potential mechanisms,” says Dunstan. “But the truth is that we haven’t been able to pinpoint the exact mechanisms, and there’s likely to be multiple. Whilst the underlying mechanisms are hypothetical, recent studies support the theory. A study with 16 young, healthy men found that sitting for three-hour periods increased blood pooling in the legs, peripheral vascular resistance, diastolic blood pressure and leg circumference. Another study finds that blood pressure increases with time spent sitting uninterrupted. Researchers generally agree that 120-180 minutes of uninterrupted sitting is probably the threshold at which you have probably spent too long in a seated position, but vascular dysfunction generally increases with time spent sitting.

Dunstan, who specialises in researching type 2 diabetes, also notes that sedentary behaviour increases post-meal, or post-prandial, rises in blood glucose and insulin. Impaired insulin sensitivity and impaired vascular function, both contribute to a higher risk of cardiovascular disease and type 2 diabetes. People are becoming more sedentary because it’s what society has encouraged. As things get more efficient, we don’t have to move around so much – Benjamin Gardner Given all these well-known potential consequences, why is it that we sit for so long – and can we break the habit? “I think people are becoming more sedentary because it’s what society has encouraged,” says

Benjamin Gardner, a social psychologist specialising in habitual behaviour at the University of Surrey, who has been researching why people sit for so long. “It’s not that anyone’s deliberately pushing it. It’s just as things get more efficient, we don’t have to move around so much.” In 2018, Gardner and colleagues found that encouraging standing in meetings presented unique social obstacles. “We encouraged people to try this [standing up] in three different meetings, and we interviewed them after each one to find out how they got on, and the findings were fascinating,” says Gardner. “In a formal meeting, it was felt it was not appropriate to be standing.”

Some researchers believe we need more social factors to make it easier for people to break up the time they spend sitting (Credit: Getty Images) Other interventions include height-adjustable workstations, sit/stand chairs, treadmill workstations, and fidgeting the legs which enhances blood flow. (Learn more aboutwhy fidgeting is good for you.) Just getting up every-so-often and going for a light walk or climbing some stairs has also been shown to be beneficial. Wearable technology may also help nudge us into action. In a promising new study, wearable devices called accelerometers provided 24-hour data on individual behaviour patterns including sitting, standing, sleeping and exercising.

As Dunstan pointed out, this potentially allows for tailored optimal sitting and standing times, with devices then sending automatic reminders whenever we sit for too long. However, the use of technology is not without its drawbacks, as some may become frustrated by or desensitised to its prompts. Above all, Gardner and colleagues encourage moving between sitting and standing positions more frequently. The premise of breaking up sedentary time by just standing up is simple, but has significant health benefits, particularly for low-activity individuals. For wheelchair users or others with mobility constraints, specific, adapted exercises can be beneficial. For many, sedentary behaviour can seem like an unavoidable consequence of modern life and work. But even small changes to your routine – be it stretching more, fidgeting or standing up to make a cup of tea – can help break your sitting habit. — For essential climate news and hopeful developments to your inbox, sign up to the Future Earth newsletter, while The Essential List delivers a handpicked selection of features and insights twice a week. For more science, technology and health stories from the BBC, follow us on Facebook and X.

Barrons-The catchphrase “Drill baby drill” is in the 2024 Republican party platform. But it’s a relic that rings hollow. While Trump promoted fossil fuels in his first term and was hostile to renewables—pulling the U.S. out of the Paris Agreement on climate—the energy sector declined 30% in total return on his watch, hit by Covid and depressed oil prices. Under Biden, the sector has returned a total 148%, despite Biden’s promotion of a “Green New Deal” and getting the U.S. back in the Paris agreement. Paul R. La Monica

10. Peter Lynch Quotes: 25 More Highly Valuable Insights

From Abnormal Returns Blog www.abnormalreturns.com ”The bearish argument always sounds more intelligent.” (p. 23) “It’s self-defeating to try to invest in good markets and get out of bad ones.” (p. 48) “Obviously you don’t have to be able to predict the stock market to make money in stocks, or else I wouldn’t have made any money.” (p. 84) “If professionals can’t predict economies and professional forecasters can’t predict markets, then what chance does the amateur investor have?” (p. 87) “No wonder why people make money in the real estate market and lose money in the stock market. They spend months choosing their houses, and minutes choosing their stocks. In fact, they spend more time shopping for a good microwave oven than shopping for a good investment.” (p. 80) ”The simpler it is, the better I like it.” (p. 130). “Why take chances on a fickle purchase when there’s so much steady business around?” (p. 142) “When management owns stock, then rewarding the shareholders becomes a first priority, whereas when management simply collects a paycheck, then increasing salaries becomes a first priority.” (p. 143) “Insider selling usually means nothing and it’s silly to react to it. There are many reasons that officers might sell. But there’s only one reason that insiders buy.” (p. 144) “Wait for the earnings. You can get tenbaggers in companies that have already proven themselves. When in doubt, tune in later.” (p. 159) “Value always wins out – or at least in enough cases that it’s worthwhile to believe it.” (p. 161) “Once you’re able to tell the story of a stock to your family, your friends, or the dog, and so that even a child could understand it, then you have a proper grasp of the situation.” (p. 175) “La Quinta was a great story, and not one of those would-be, could-be, might-be, soon-to-be tales. If they aren’t already doing it, then don’t invest in it.” (p. 179) “It’s never too late not to invest in an unproven enterprise.” (p. 182) “All else being equal, a 20-percent grower selling at 20 times earnings is a much better buy than a 10-percent grower selling at 10 times earnings.” (p. 218) “All of this research I’ve been talking about takes a couple of hours, at most, for each stock.” (p. 227) “What’s wrong with high expectations? If you expect to make 30 percent year after year, you’re most likely to get frustrated at stocks for defying you.” (p. 237) “Going into cash would be getting out of the market. My idea is to stay in the market forever, and to rotate stocks depending on the fundamental situation.” (p. 242) “Sell the winners and hold on to the losers is as sensible as pulling out the flowers and watering the weeds.” (p. 243) “Most money I make is in the third or fourth year that I’ve owned something.” (p. 266) “In most cases it’s better to buy the original good company at a high price than it is to jump on the ‘next one’ at a bargain price.” (p. 268) “It takes years, not months, to produce big results.” (p. 285) “Just because the price goes up doesn’t mean you’re right.” (p. 286) “Buying a company with mediocre prospects just because the stock is cheap is a losing technique.” (p. 286) “You don’t have to kiss all the girls. I’ve missed my share of tenbaggers and it hasn’t kept me from beating the market.” (p. 286)

1. $190 Trillion in Treasuries Traded 2023..10-Year Treasury Approaching 4%

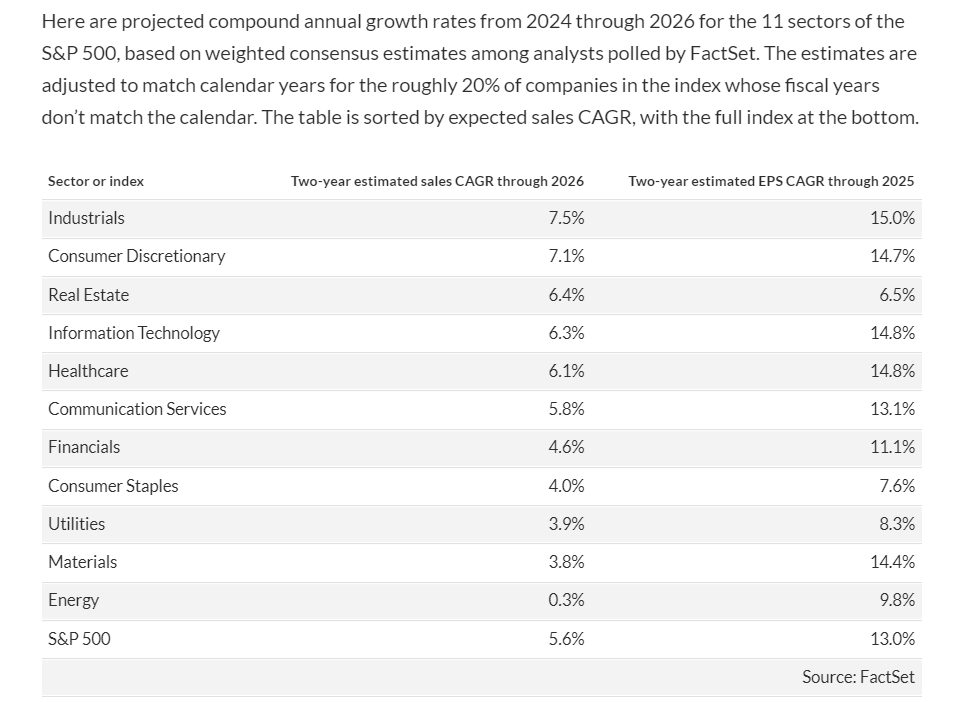

2. Earnings Upgrades Moving to Non-Tech Sectors

DC Lite Blog EPS sentiment. “Earnings-per-share upgrades have fallen sharply for the Nasdaq 100, while upgrades for the S&P 500 and Russell 2000 are on the rise.”

3. 12-Month Forward Earnings Estimates for AI is Falling

Market Ear Blog

4. Equity Inflows Slow in August

Marketwatch Barbara Kollmeyer August, he adds, is typically the “worst month of the year for equity flows. There are no predicted inflows in August as the capital has already been deployed for [the third quarter]. Buyers are out of ammo and I am on the look out for outflows,” Rubner says, providing this chart:

5. We Showed Chart Earlier in Week Showing Luxury Brands Earnings Growth Over 20-Years

8. Record Number of Americans Have $500k in Stocks and $500k in Home Equity

Torsten Slok, Ph.D.Chief Economist, Partner-Apollo Global Management The University of Michigan Survey of Consumer Sentiment shows that a record-high 30% of the population have stocks worth more than $500,000, and 37% own a home worth more than $500,000, see charts below. It is remarkable that these wealth gains for the household sector have taken place while the Fed was raising interest rates. The bottom line is that the tailwind to consumer spending for homeowners and equity owners is significant, in particular when combined with record-high cash flows from fixed income.

There are gentler ways to start the day than with an ice-cold shower, yet the potential health benefits – warding off illness, improving mood and helping with weight loss – could just be enough to make you consider braving the chill. Prof Mike Tipton, a physiologist at the University of Portsmouth, has spent four decades studying how temperature affects our health. It’s a promising area of new research and, coupled with anecdotal accounts, might persuade you to turn the dial down to cold. “For the people who say, I feel alive, awake, it sets me up for the day, I’m not going to knock it in any way. But there’s work to be done to figure out the mechanism,” he says. Read on to find out why.

1. Boosts your immune system One of the most rigorous studies into cold showers involved 3,000 volunteers in the Netherlands turning the water to as cold as possible for the final 30, 60 or 90 seconds of their shower. A control group showered as normal. After three months, results showed that those who included a cold water blast in their shower had taken 29 per cent fewer sick days – regardless of how long the water was cold for. “My particular hypothesis is that the sudden change in skin temperature is driving a lot of the beneficial changes,” says Prof Tipton. “That sudden fall produces the cold shock response – a gasp, hyperventilation and increasing workload in the heart. “Because it’s part of a fight or flight response, you’re activating the stress hormones, serotonin goes up and beta endorphins increase,” which contributes to boosting the immune system to ward off illness, he says. Longer exposure to cold water is, of course, fatal, accounting for 60 per cent of deaths in cold water, Prof Tipton says. “This is a very double edged sword. A minute in cold water may prime your immune system, five minutes may actually impair it. It’s the dose of cold that’s critical.”

2. Enhances mental health Exposure to cold water may drastically improve mental health in patients, even when drugs have failed to do so, research suggests. One study by Prof Tipton and colleagues found that weekly cold-water swimming helped to ease a 24-year-old woman’s depression. She had previously spent seven years battling the condition, during which medication failed to reduce her “She said that she was the happiest she could remember being. A year later, she was drug-free and open water swimming. She’d overcome a big challenge in her mind,” he says. It’s not clear if a cold shower could have the same effect. “It may be the distraction of the cold water [that eased her depression]. When exposed to cold water, most people say all they can think about is the temperature and it takes their mind off everything else,” he says. However, improvements in her mental health could also be down to the exercise involved in cold water swimming, overcoming the challenge of the cold, or the social inclusion of swimming with others, he noted. “Is it the cold, or is it any one of these other things? We won’t know until there are studies that isolate cold exposure,” Prof Tipton adds.

3. Improves skin and hair health Lukewarm water is the ideal for face washing, as it effectively removes dirt, oil and impurities without causing excessive dryness or irritation, explains Dr Anastasia Therianou, a consultant dermatologist on Harley Street and at Imperial College Healthcare NHS Trust. However, cold water constricts blood vessels in the skin, which can reduce redness and inflammation – so can improve the appearance of skin, she says. When it comes to hair, a cold shower can help lock in moisture. “Cold water closes the hair cuticles, so the hydration is ‘trapped’ inside the hair,” Dr Therianou says. “This is beneficial for people with thin hair that tends to break easily. However, cold water cannot fully remove the excessive oils from the scalp so it’s advisable to wash your hair in warm water and then condition and rinse using cold water – if you can bear it.”

4. Supports weight loss A review of more than 100 studies suggested cold water immersion, such as swimming or a cold bath, can activate and expand brown adipose tissue – a “good” fat that burns calories – and also reduce “bad” white fat, and therefore aid weight loss. “The brown fat cells develop from white fat cells and, as their energy source, they like free fatty acids which they get from the white fat cells,” explains James Mercer, a professor emeritus at The Arctic University of Norway who co-authored the review. “By reducing the content of free fatty acids in the white fat cells, theoretically, one loses weight.” However, scientists have not yet investigated whether a cold shower would also trigger this process. “My gut feeling is no, since the development of brown fat in cold water swimmers seems to require a very strong cold stimulus which I do not think you would get from a short cold shower,” says Prof Mercer. “A cold shower doesn’t provide the same stimulus as being immersed in cold water, as only about a third of the body is exposed to the cold,” says Prof Tipton. “As a result, the cold shock response is roughly about a third of the size it would be in an immersion. That doesn’t mean it’s not big enough to have a positive effect – but nobody’s done the study.”

5. Relieves muscle soreness and accelerates recovery Athletes frequently turn to ice baths to aid their recovery, the idea being that the cold reduces blood flow, swelling and inflammation of the muscles. Cold showers could have a similar effect, as the cold water is an analgesic (painkiller) and may be enough to decrease swelling, says Prof Tipton. However, he notes that while there is “some evidence” cold water can help muscle aches, the evidence “is not convincing across the board”. For example, some studies suggest that cold water actually lowers protein generation, which is vital for building and repairing muscle.

6. Aids in pain relief and reduces migraines There’s anecdotal evidence of cold baths and cold water swimming easing very severe migraines, Prof Tipton notes. These accounts suggest short-term exposure to the cold may ease pain, he says. Cold receptors are located about 0.18mm below the skin surface and, when skin temperature drops quickly, these fire off an enormous amount of information to the central nervous system and the subsequent gasping changes blood flow in the brain, he explains. A reduction in pain could be down to a combination of those two things or other factors,” he says.

7. Enhances mood and promotes emotional wellbeing There’s anecdotal evidence from cold water swimmers that it dramatically improves their mood and wellbeing, says Prof Tipton. “I work with the Bluetits [an outdoor swimming group in Pembrokeshire] and I am overwhelmed by the accounts of people who say it has changed their life. People are in tears about it. “The vast majority of people who report benefits, say it’s to their mental wellbeing, although the mechanism behind this effect is unclear. The cold water is clearly activating people and waking them up, which will be down to the cold shock response and the release of stress hormones.” Health risks to consider before having a cold shower

Before stepping into a cold shower, it’s important to consider if you’re in good enough health to do so, says Prof Tipton. “We’re a tropical animal that wants to be naked in 28C. Taking that animal and showering it with 10 or 12C water is a really stressful thing to do,” he says. The cold triggers cold water shock, which is a gasp of breath, followed by rapid breathing and high blood pressure. While this can be beneficial for some over a short time, it will become detrimental to everyone with time, so people should stay in a cold shower for no more than one minute. It is especially dangerous for people with cardiovascular disease, aneurysms or heart problems and they therefore shouldn’t try it, Prof Tipton says. Other complications of cold water that could affect anyone include hypothermia and non-freezing cold injury, he warns, is damage to the small nerves and blood vessels of the hands and feets that can last for life. Recommended Cold water therapy: What is it, types and where to start