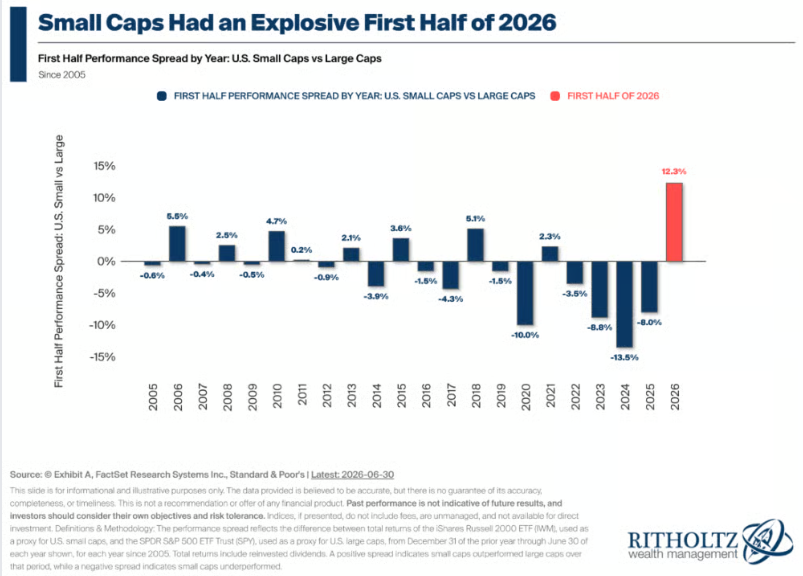

1. Small Cap Underperformed Large Cap 4 Years in a Row Prior to 2026

The Irrelevant Investor

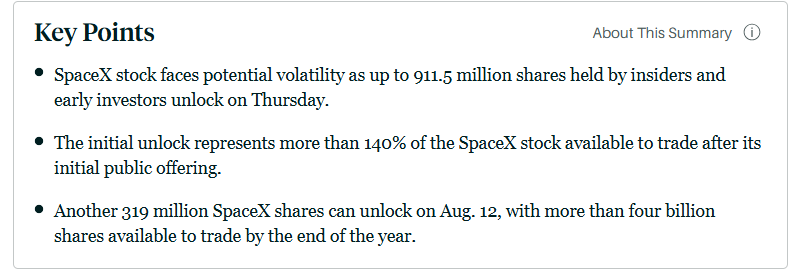

2. SPCX Unlock-Barrons

Barron’s

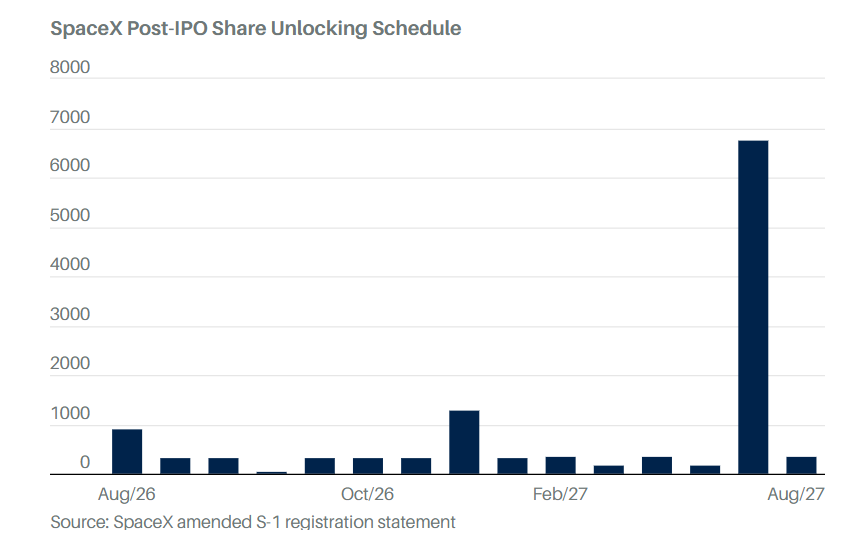

3. Leverage ETFs -Understand What You are Buying

Advisor Perspectives

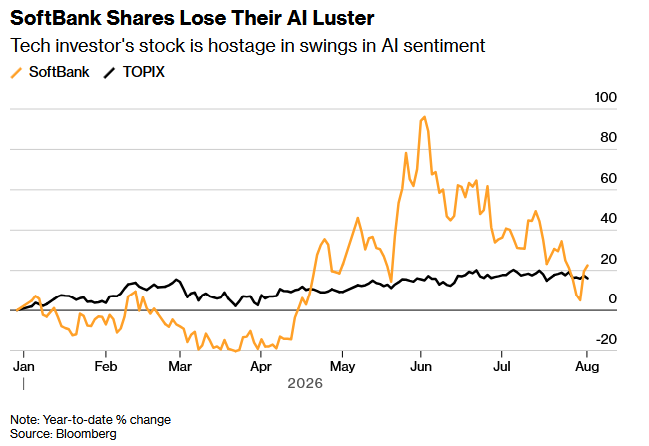

4. Softbank Gives Up Half Its 2026 Gains

Bloomberg-In June, SoftBank briefly became the most valuable company on the Tokyo Stock Exchange, buoyed by enthusiasm around Arm, OpenAI and AI infrastructure investment plans. It’s since given up more than half of its gains this year.

Bloomberg

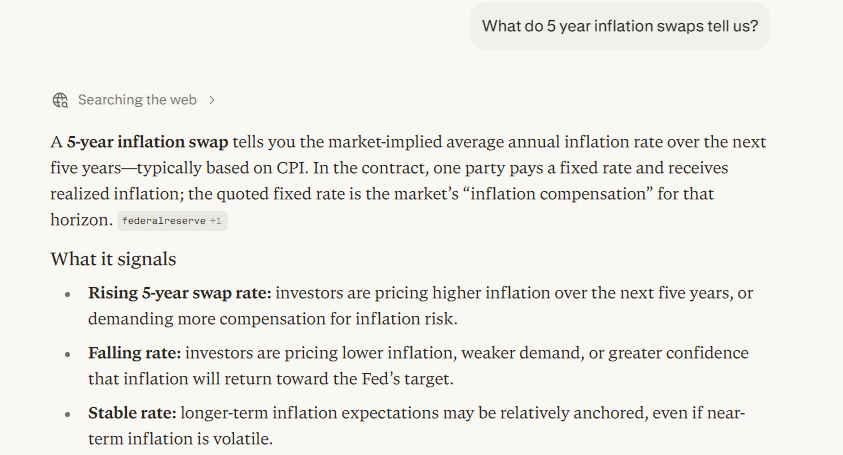

5. Five Year Inflation Swaps Not Predicting Inflation

Perplexity

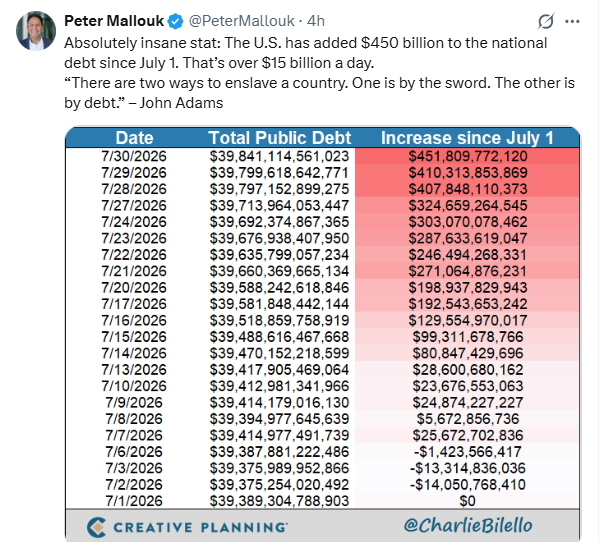

6. The U.S. Added $450Billion to National Debt Since July 1

7. ”AI is Going to Cause Mass Unemployment”??? Jobless Claims Lowest Since 1969

Layoffs fall to the lowest level since the U.S. put men on the moon. Here’s what that says about the economy.

Rising sales and a labor shortage are deterring job cuts. Jobless claims haven’t been this low since 1969. Marketwatch By Jeffry Bartash

Businesses aren’t hiring lots of people, but they are extremely reluctant to shrink their workforces with sales rising and the economy still expanding.

The last time layoffs in the U.S. were as low as they are now, NASA was landing astronauts on the moon, young Americans were rocking out at Woodstock and President Richard Nixon was moving into the White House.

“Layoffs remain historically low and have, if anything, declined further this year,” said chief U.S. economist Stephen Stanley of Santander Capital Markets.

Ethan Allen’s CEO on Effective Leadership StrategiesSee All Videos

The ultralow level of jobless claims is another sign of a gradually strengthening labor market and possibly even a growing shortage of labor.

Businesses aren’t hiring lots of people, but they are extremely reluctant to shrink their workforces with sales rising and the economy still expanding.

New jobless claims in the last three weeks totaled 199,000, 198,000 and 189,000 after adjusting for seasonal swings in employment. By contrast, new claims averaged 223,000 in the same three-week period a year earlier.

“These are levels indicative of a sturdy labor market,” economists Robert Kavcic and Shelly Kaushik of BMO Capital Markets wrote.

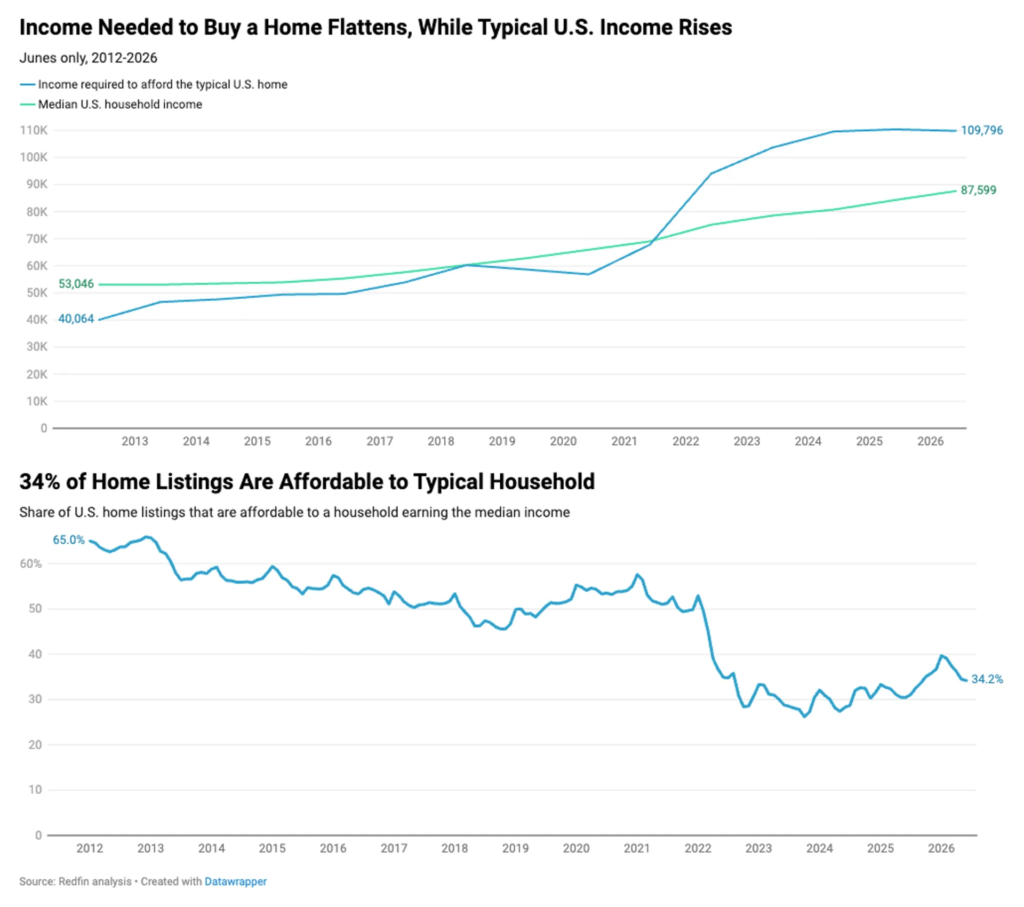

8. 34% of American Homes are Affordable for Typical Household

Home affordability. “Americans need to earn $109,796 to afford the typical U.S. home for sale, down 0.5% from an all-time high of $110,382 a year ago … Just over one-third (34.2%) of U.S. home listings were affordable to someone earning the median income in June, up from 30.5% a year earlier.”

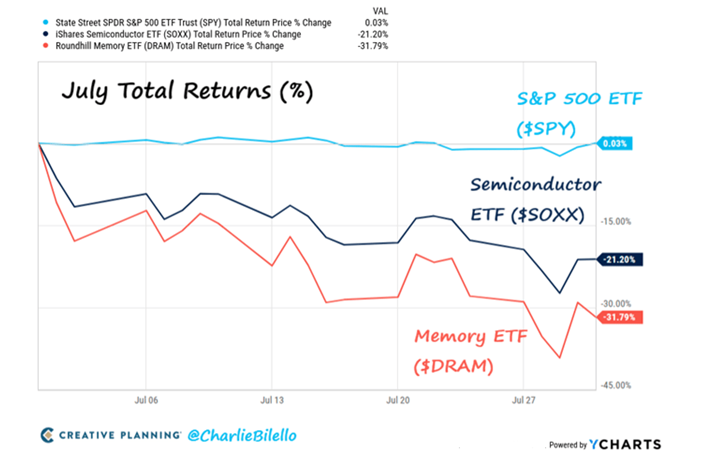

1. July Returns…Semiconductors and DRAM Stocks Correction

@Charlie Bilello

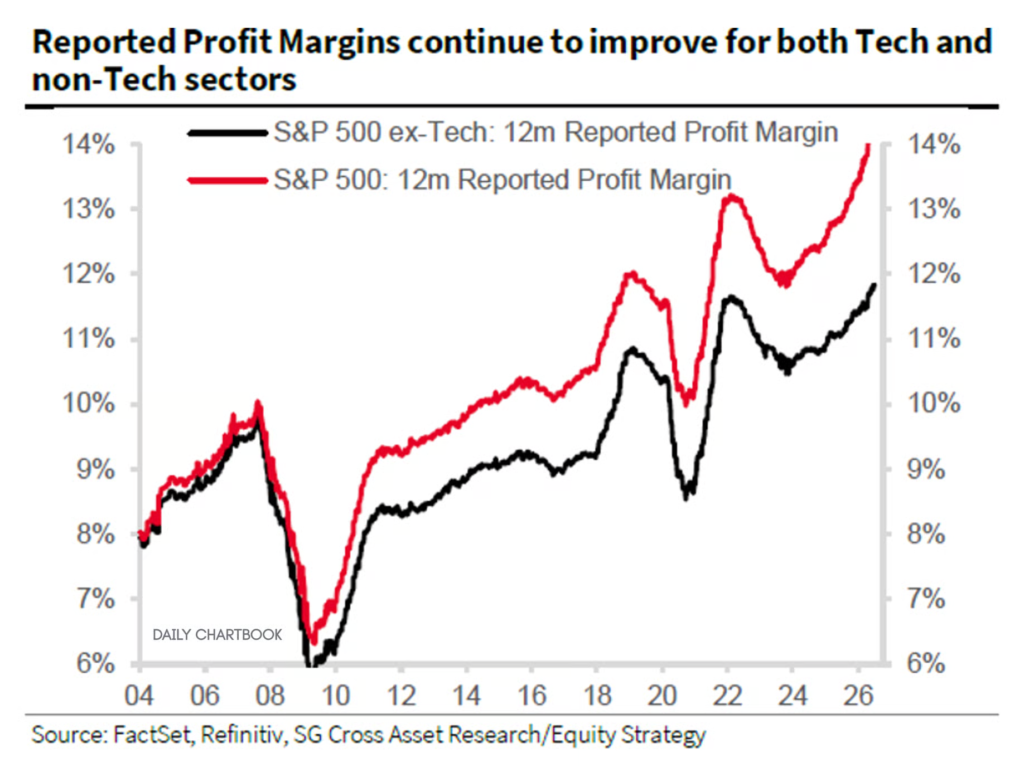

2. Profit Margins Better in 10 of 11 Sectors

Profit margins. Higher margins are not just a Tech story: 10 out of 11 sectors are experiencing margin expansion.

Manish Kabra – SocGen

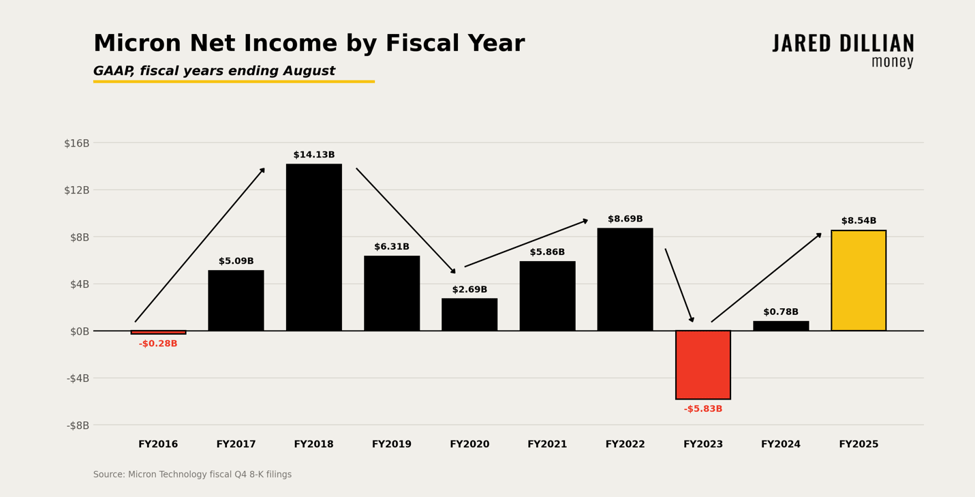

3. History of Micron MU Drawdowns

Jared Dillian Money It’s important to remember that semiconductors are the canonical cyclical sector in the market—and that memory is the most cyclical corner of semiconductors. Take Micron, for example. It earned $8.7 billion in fiscal-year 2022. It lost $5.8 billion in fiscal-year 2023. Just looking at the last decade, it has been like riding the Zipper:

How has that affected the stock? Peak-to-trough drawdowns of 50–90% are routine, not exceptional:

Dot-com bust (-90%+)

2008 (-90%)

2015 (-60%)

2018–19 (-60%)

2022 (-50%)

Jared Dillian Money

4. I Have Mentioned Rolling Mini-Bubbles….Summary by WSJ James Mackintosh

WSJ

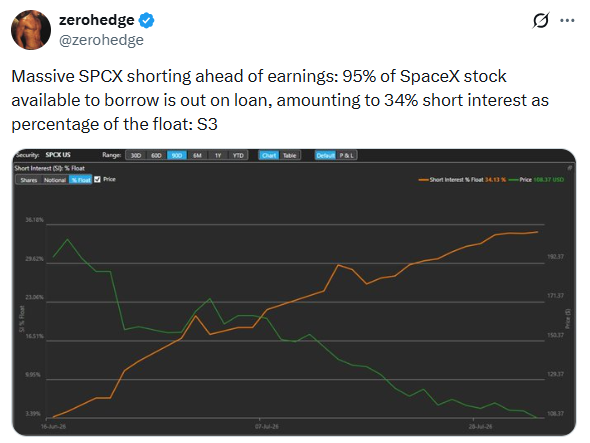

5. Massive Short Interest in SPCX….But Window Opening for Insider and Early Investor Selling

zerohedge

6. MAG 7 Closing in on New Highs….$72 Print Needed

StockCharts

7. Fed Rate Hike In September Chances Fall Below 50%

Polymarket

8. Who Controls the World’s Money?

@stockregion

9. 300 Legislators Have Served More Than 30 Years in Congress

Barrons By Brian Hamilton To date, more than 300 legislators have served for more than 30 years in Congress. Some 70% of the current members were career politicians before they made it to Washington. No Founder would have even thought to consider laws around term limits because they couldn’t have fathomed hanging out well beyond their welcome, all the while depending on the government dole for their salary.

The natural question is, why would legislators want to stick around for so long?

It turns out that, since 2004, the top 100 wealth gainers in Congress have averaged a 114% increase in net worth while in office, according to a recent Ballotpedia study. During the same period, the median U.S. household saw its inflation-adjusted net worth decline by nearly 1%. That means that for every $1 of wealth the average American lost, Congress’s top 100 gained $121. Wow. Today, at least 30% of senators are estimated to be worth more than $10 million, despite their taxpayer-funded base salary being just $174,000.

How is this possible?

One obvious explanation is that these politicians are privy to information that average Americans aren’t, yet they are still permitted to own and trade individual stocks. The 2012 Stock Act, which requires members of Congress to report stock trades worth more than $1,000 within a 45-day window, does nothing to curb legislators’ trading.

You would hope that they would want to act in the interest of the country without the appearance of personal gain. However, an investigation conducted by a consortium of news organizations that analyzed nearly 9,000 financial-disclosure reports identified 78 members of Congress who violated the Stock Act.

A preventive neurologist said hearing loss is associated with a higher risk of dementia.

A preventive neurologist said vision and hearing loss are risk factors for cognitive decline.

Some researchers theorize that sensory loss reduces brain activity and stimulation.

Wearing sunglasses or earplugs at concerts can go a long way in curbing vision and hearing loss.

How do hearing aids impact dementia risk?

What tests catch early vision loss?

How does isolation affect cognition?

Provide feedback

What feels off in this AI-generated summary?

If you’re trying to reduce your personal risk of developing dementia or Alzheimer’s, the answer might be right in front of your eyes — or within earshot.

Dr. Kellyann Niotis, a preventive neurologist and assistant professor of neurology at Weill Cornell Medicine, said vision and hearing loss are two risk factors for cognitive decline.

“They’re two big ones that people don’t often think about as related to their brain,” Niotis said at a June salon dinner with Julianne Moore to promote Brain Health Matters, a public health campaign from Lilly to encourage brain health awareness. “So if you are not up to date on your annual screenings, please, please, please do that.”

Niotis, who focuses on diseases like Alzheimer’s, told Business Insider that she hopes more people will take risk factors like sensory loss more seriously as they age. A 2024 Lancet study found that nearly half of all dementia cases worldwide could potentially be prevented by mitigating risk factors, including vision and hearing loss.

Niotis shared why our eyes and ears are so linked to brain health — and what to watch out for.

Why sensory loss may be connected to cognitive decline

Niotis said researchers are still trying to figure out exactly why hearing and vision loss are tied to neurodegenerative diseases like dementia. As of now, there are some hypotheses.

One is related to brain stimulation. A big part of brain health preservation is challenging your brain, be it through puzzles, learning a new language, or playing an instrument, Niotis said.

Sensory loss can make it harder to activate certain parts of the brain. “There’s a thought that as someone loses their sight, they aren’t being provided with that sensory stimulation that that region of the brain needs,” Niotis said.Another theory is more straightforward: losing your sight or hearing has downstream effects on other brain-healthy habits. “If you can’t see well, are you less socially engaged? Are you more socially isolated? Are you less willing to engage in activities, like exercise, that otherwise are keeping your brain active?” Niotis said.

Watch out for halos or other people complaining about your hearing

When it comes to sensory loss, there are a few red flags to watch out for.

For vision loss, conditions like cataracts are common in older adults and reduce visual sharpness. Even so, “if that’s significantly impacting your ability to see, it could be putting your brain at risk,” Niotis said, whether the loss of vision weakens signals in the brain or changes how you socialize.

You should consider getting an eye examination if you experience signs of glaucoma (a group of eye diseases that damage the optic nerve), changes in how you perceive colors, seeing a lot of halos (such as when you’re driving), and words “jumping” around the page, she said. These are not, on their own, direct symptoms of dementia or cognitive decline, and do not necessarily influence dementia risk. However, untreated, they could become risk factors down the line, Niotis said.

Hearing loss is a little more subtle: “It’s often recognized by people around you,” Niotis said, so if you’re suddenly fielding complaints from friends and family, it might be a sign to get your hearing checked — and not delay it. “Most people I find are not able to appreciate that loss the same way they are able to appreciate vision loss,” she said, making it easier to dismiss.

Thankfully, there are some ways to preserve your hearing and vision.

One of the biggest preventablecauses of hearing loss “is completely in our control,” Niotis said. “It’s exposure to loud noises.” She said taking precautions such as wearing earplugs at concerts or proper hearing protection when working loud machinery is very important.

When it comes to vision loss, Niotis said wearing sunglasses and reducing direct sun exposure to the eyes can protect the eyes from ultraviolet radiation, which contributes to cataracts and some other UV-related eye damage.

And while there’s no research that links permanent vision loss to screen time, Niotis said it can still be a good idea to take screen breaks. “If you’re someone who’s staring at a phone or screen all of the time, you’re training your eyes to do one particular task, which is to converge and look in front of you,” she said, potentially leading to temporary eye strain or eventual nearsightedness.

For that, she recommends taking a break and going for a walk — an already brain-healthy habit.

This article is not a substitute for professional medical advice, diagnosis, or treatment. Always consult your qualified physician or healthcare provider.

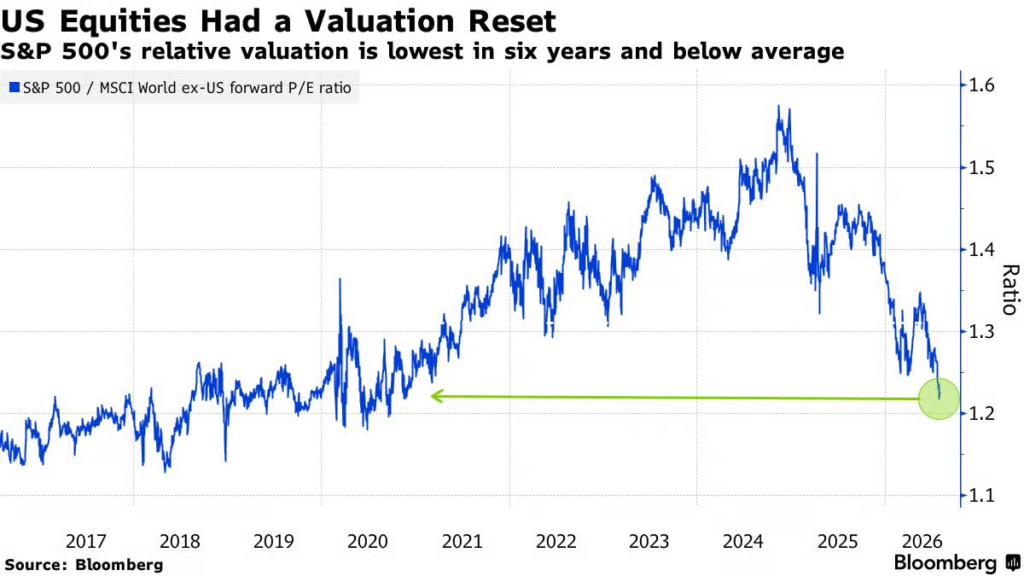

1. S&P Premium to International Equities at 6-Year Low

SPX relative valuation. “US stock valuations have dropped drastically against the rest of the world, with their premium dwindling to only about 22%. That’s the lowest in more than six years and well-below the 10-year average of 31%.”

Michael Msika – Bloomberg

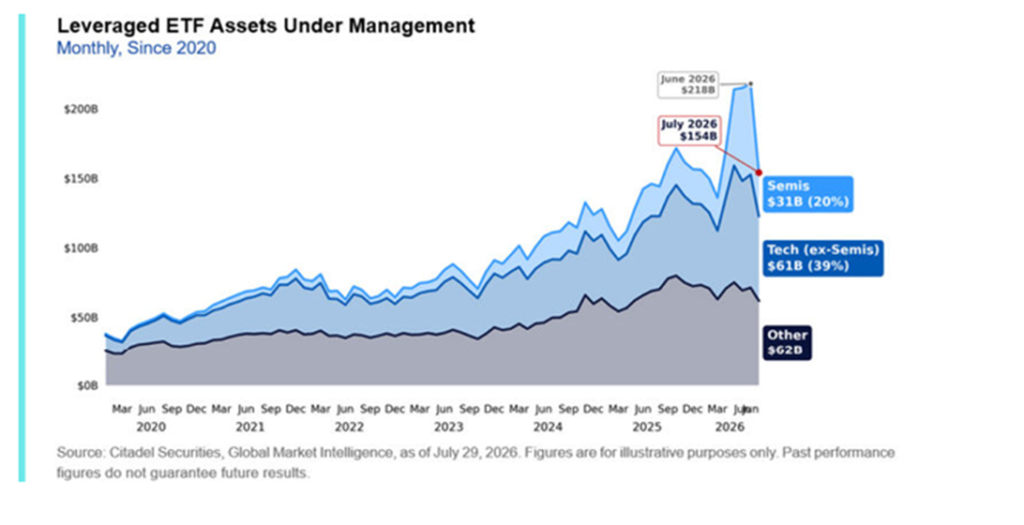

2. Leveraged ETF Assets Declined by $60B from Peak..Momentum Unwind

Citadel Scotty notesLeveraged ETF assets have declined more than $60 billion from their June peak – The largest reductions have occurred across the market’s most crowded themes, with Technology leveraged ETF assets down approximately 40% and Semiconductor assets down nearly 55% over the past month.

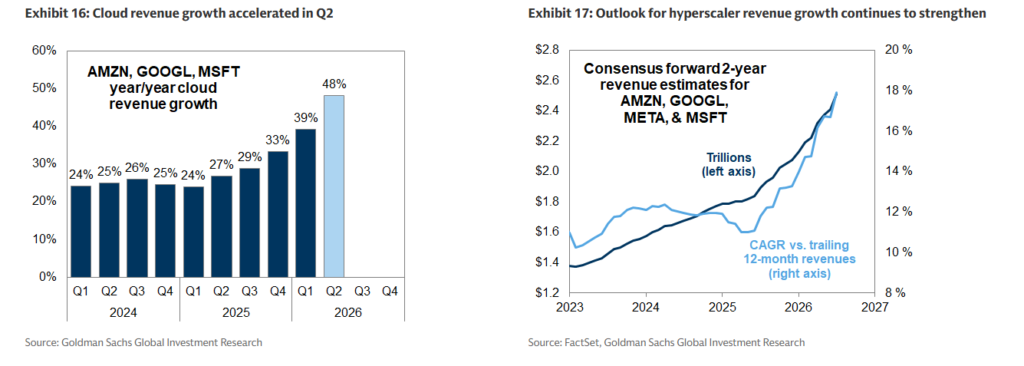

3. Cloud Revenue Growth and Hyperscaler Revenue Growth

Dan Stratemeier Jefferies

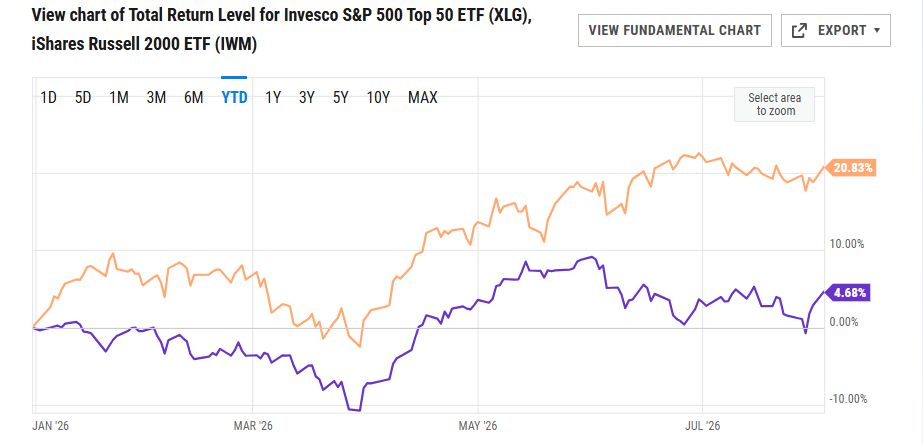

4. XLG is Mega Cap Stock ETF …2026 Small Cap IWM +21% vs. XLG +5%

YCharts

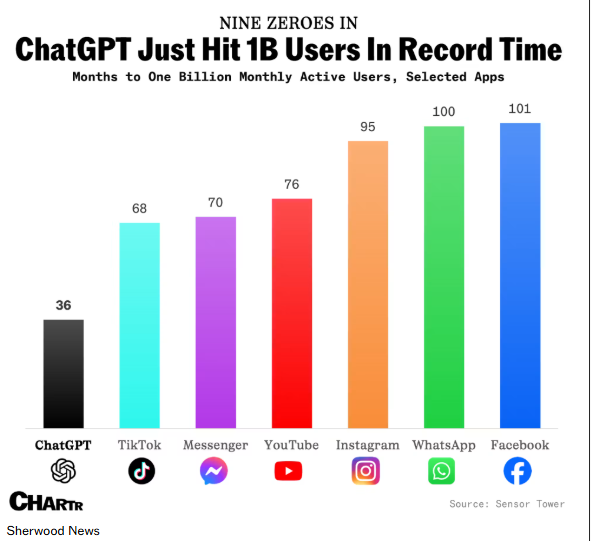

5. ChatGPT Hits 1B Users

Sherwood News

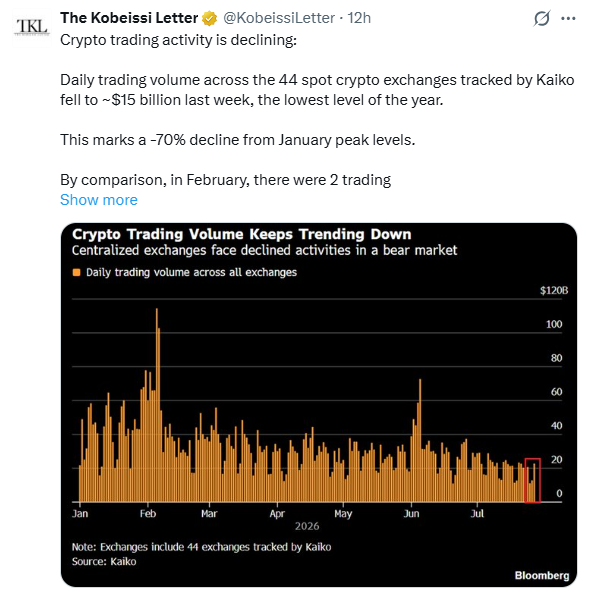

6. Crypto Volume Not Rebounding

The Kobeissi Letter

7. BMY Bristol Myers New Highs…Long-Term Chart 50 month thru 200 month to Upside. BMY Still Negative 5-Year Return

StockCharts

8. Violence as a Service

Semafor

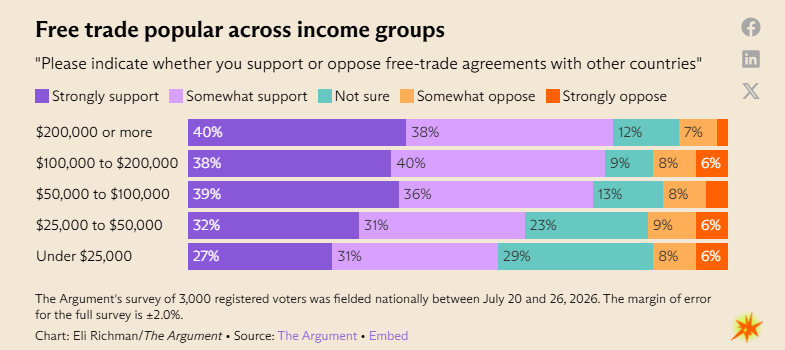

9. Free Trade Popular Across Income Groups

The Argument

10. 5 Habit-Building Hacks From Top Coaches That Actually Work

There are few things in life that hold us back more than wanting desperately to make positive changes in our lives but simply, frustratingly, not making those changes, day after day, week after week, month after month. In my heart of hearts, for example, I know that practicing breathwork regularly brings me clarity, a fresh flow of creative ideas for my work and lower stress levels. So, developing a daily or even weekly practice would surely bring untold benefits. But despite putting it in my planner—in caps with three exclamation points—it’s just. Not. Happening.

If you’re in a similar boat—whether it’s drinking eight glasses of water a day, prospecting one new client a week, finishing that course on public speaking or getting to bed on time for a solid night’s sleep—there’s good news. The psychology of human habits is becoming less of a mystery, and coaches, who regularly deal in the currency of cultivating consistent behaviors, are using these insights with clients daily to learn how to hack our stubborn brains.

Here, we’ve compiled some fresh tips from career, creativity and life coaches to bring you some of the latest thinking on how to hack your habit-building efforts—so you can crack the code and drive the growth you know is waiting for you on the other side.

1. Start Small…Tiny…Tinier

Many habits fail to take hold because they are simply too big or too daunting, which is bound to overwhelm your resolve. James Clear, the author of Atomic Habits: An Easy & Proven Way to Build Good Habits & Break Bad Ones and a former performance coach, suggests picking a habit that’s so easy that you can do it with hardly any willpower.

If your goal is to write in a gratitude journal every day for 20 minutes, for example, start off with just two minutes, then try to increase that amount by a small percentage every day. If your habit is more complex, say crafting one new course each month, then break it down into smaller pieces, tackling just one small section a day. This approach, Clear says, takes patience. But it should feel easy, especially in the beginning, which is key to getting started and maintaining momentum.

2. Do the Thing that Can’t be Undone

If the challenge is primarily getting started, try a simple, brave act of commitment. If you’ve been wanting to learn how to tap dance, for instance, sign up for the class and pay the registration in full.

Our brains are well equipped to avoid things it deems as uncomfortable or challenging, so removing the negotiation from the table flips a “psychological switch from ‘maybe’ to ‘I’m doing this,’” she adds.

3. Create a Double-Reward Loop

Neuroscientists understand that habitual behaviors are typically formed when they are rewarded immediately. One way to activate this is by “temptation bundling,” or pairing a “should do” task with a “want to do” task.

Grace Adele Boyle, a coach to executives and creatives, has found that when you double up on rewards, you also double your chances of sticking with it.

“Reserve something deeply enjoyable—an addictive audiobook, favorite show or a specific podcast—that you only engage with while doing your habit,” she says. “I take it one step further and include a second reward immediately after habit completion. I call this a ‘double-reward loop,’ and it keeps your brain engaged during the habit and creates anticipation for next time through immediate reinforcement.”

For her, this looks like saving certain media only for workouts, then enjoying a crave-worthy chocolate protein shake immediately afterward.

4. Use the ‘Most Days’ Theory

You’ve been pushing hard with a habit or an intention, and you just aren’t seeing results. Instead, you are stuck in a shame spiral. If this scenario sounds familiar, try the “most days” theory, coined by Bree Groff, a workplace culture coach, speaker and author, in a viral Substack post. She writes: “It’s the theory that we derive enormous benefit from the habits we practice most days.”

Groff advocates for a gentler approach to change: practice the desired behavior most days—if not every day—because consistent, flexible effort is more sustainable than perfection.

If you’re trying to adopt a daily yoga practice, for example, and you find yourself rolling out your mat five days out of seven, well, that’s a win.

5. Make the New Habit Your Entire Personality

A growing body of research suggests that seeing a habit as something that aligns with your identity (“I am someone who…”) is far more powerful than seeing a habit as something you do.

He suggests a 60-second “identity rehearsal” each morning to choose a word that aligns with the person you’re striving to become, thus setting the tone for the habits you want to cultivate.

Boyle agrees, adding that while willpower can fade, personal values don’t. She suggests asking yourself questions like, “Why does this habit matter to me? What does it make possible? What value does it honor? Who does it help me become?” To set yourself up for maximum success, make your answers to these questions “personal, emotional and visible,” she says.

Image courtesy of Roman Samborsky/Shutterstock

This article was first published in the March 2026 issue of SUCCESS® digital edition. Get your FREE copy here.

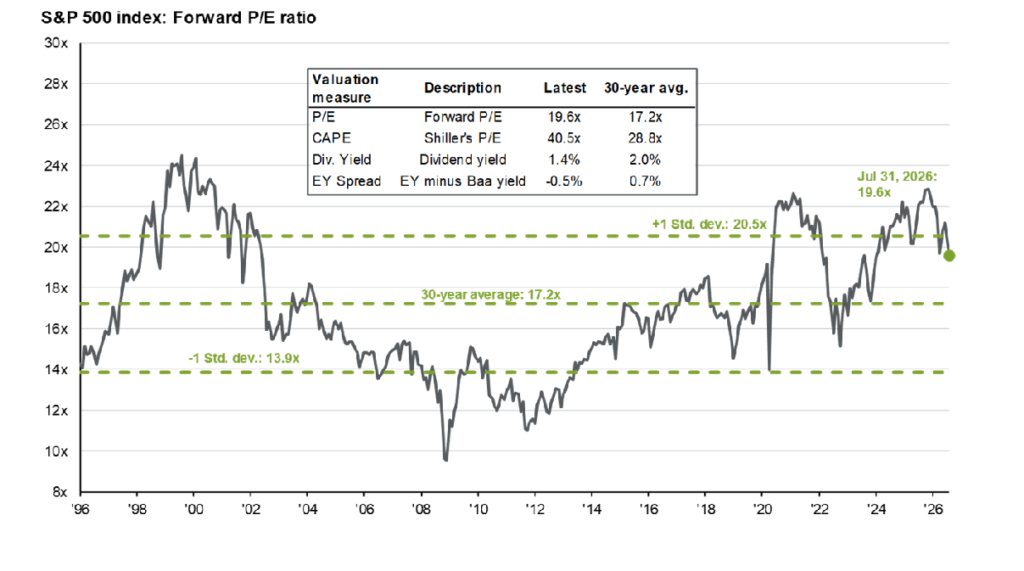

2. JP Morgan S&P 500 Valuation Updated Chart…Stocks Not Cheap But Grew Cheaper in 2026 with Growing Earnings

JPMorgan

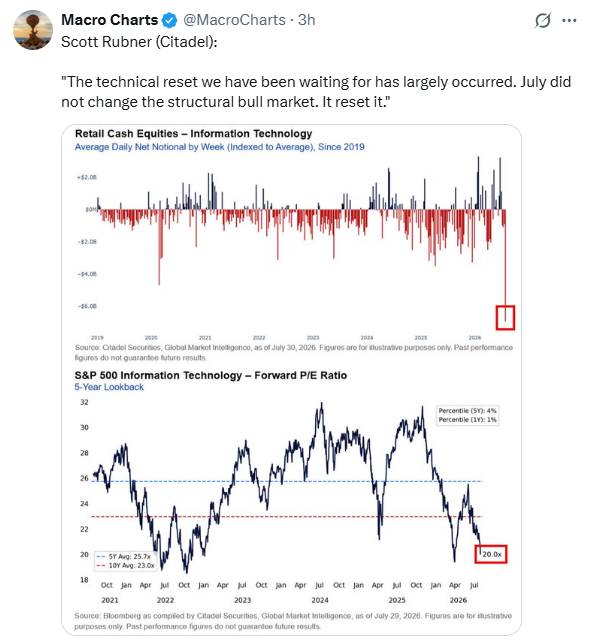

3. Technology Reset on Sell Off

Macro Charts

4. Amazon Breaks Out to New Highs

StockCharts

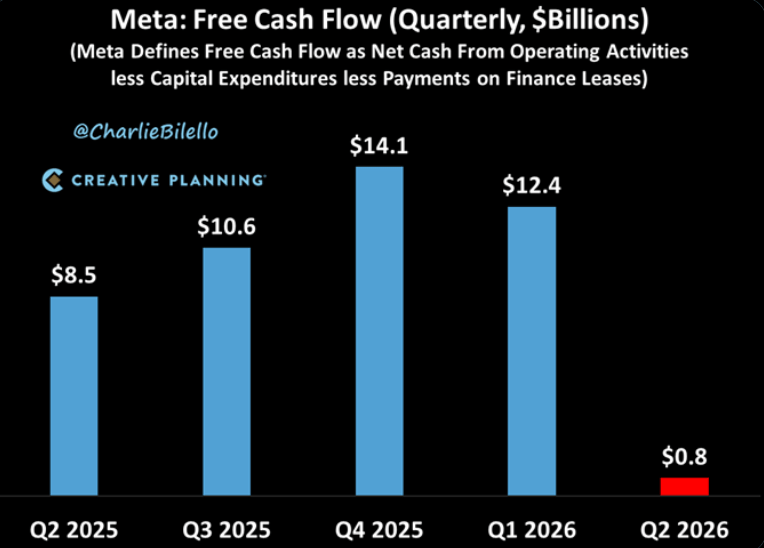

5. META Legal Bills are 5-6% of Expenses

In the most recent quarter (Q2 2026), Meta’s legal charges were about $2.4 billion, which was roughly 5–6% of total costs and expenses, not 13%.abcnews+2

What the numbers show

Q2 2026 total costs and expenses: $42.03 billion.abcnews+2

Q2 2026 legal charges: $2.40 billion (recorded in general and administrative expenses).abcnews+2

So legal expenses were about 5–6% of Meta’s total costs in that quarter.

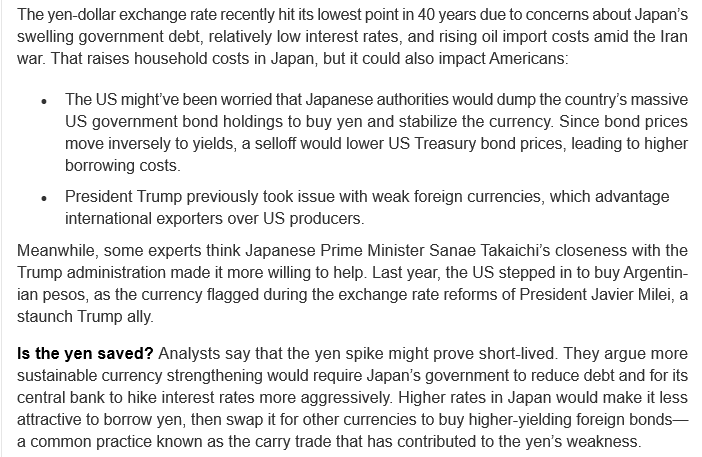

This Chart Shows U.S. Dollar Drop vs. Yen in Last Few Weeks

StockCharts

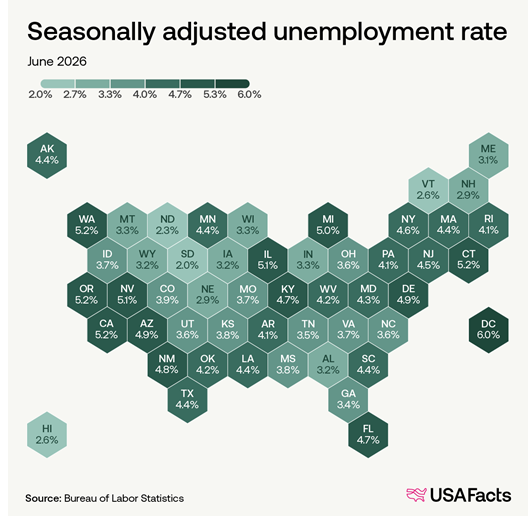

7. USA Unemployment by State…Some States 2-3%

USAFacts

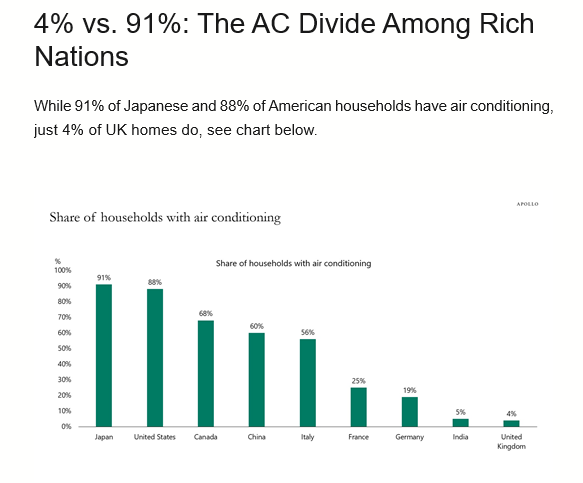

8. The Air Conditioning Divide

Apollo

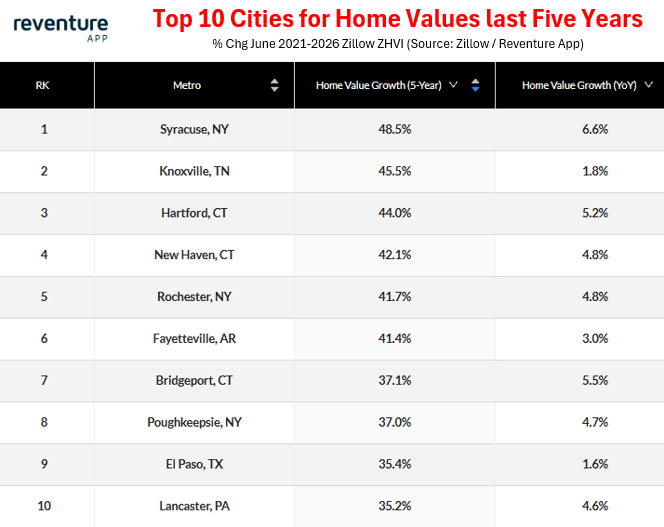

9. Top 10 Cities with Growing Home Values

Nick Gerli

10. Perseverance in Life

Psychology Today Personal Perspective: Moving forward in the face of crushing obstacles Greg O’Brien

Key points

Perseverance often means steady faithfulness, not dramatic acts of courage.

Forward motion—no matter how slow—is vital when facing crushing obstacles.

Studies show perseverance and optimism can help reduce anxiety, depression, and panic.

“If you can’t fly then run, if you can’t run then walk, if you can’t walk then crawl, but whatever you do, you have to keep moving forward.” — Martin Luther King, 1960

I’ve been crawling a lot of late.

I’m not alone in this. Life, at times, offers all of us a haversack of trials—crushing burdens in the moment and beyond.

And we think of giving up.

I’m not saying my challenges are any tougher than others, but just sayin’: in my case, fighting off advancing and bruising Alzheimer’s, cancer, black hole depression, and the death of a son in 2022. No parent should ever have to bury a child.

Some days, the urge just to give up is overwhelming, as the body feels frozen in the moment and the demons are snapping. But I’m trying not to take the bait, and think often of others struggling.

I’m encouraged by Albert Einstein, who said: “You never fail until you stop trying.”

As an aging jock, 76 now, I don’t want to stop trying. So, I’m fighting forward, but can’t say it’s easy in any way.

We all find discernment in many ways. I was raised Irish Catholic, both mother and father with deep Irish roots (47 of 48 branches of our family tree from Erie). I’m now a bit more evangelical, though I haven’t forgotten my roots.

I’m not preaching, just trying to connect; we all come from different places.

I so respect that…

I recently saw the blockbuster summer movie The Odyssey—Director Chris Nolan’s account of the ancient epic about the hero Odysseus trying to return home to his wife and son after serving in the Trojan War and the interminable string of hurdles in his path. Bloodied but unbowed, as William Henley writes in his epic poem “Invictus,” Odysseus never gave up, and through remarkable perseverance, he finally makes it home.

Doug Scalise, my pastor on Outer Cape Cod, emphasized the drive of Odysseus in his Sunday sermon to underscore the faith needed to persevere in life. “There’s something deeply admirable about refusing to quit,” Scalise said. “Sometimes we imagine perseverance as dramatic acts of courage. Occasionally it is. More often it looks like quiet faithfulness over a lifetime.”

Added Scalise, “Have you ever had a week where every day brings another problem, another disappointment, another phone call telling you something you didn’t want to hear?” In a reference to the New Testament Book of Hebrews, he says: “Faith in everything requires perseverance.”

As a wholly imperfect person, I’m trying to find my way out of a valley of depression without wavering. Scalise once reinforced to me that one can’t helicopter out of such a serpentine valley; you have to walk it out.

We often find perseverance in different ways, though forward motion is forward motion.

Experts say perseverance is the confluence of passion and lasting stamina and is more critical in life than talent or intelligence.

The American Psychological Association notes: “People who don’t give up on their goals (or who get better over time at not giving up on their goals) and who have a positive outlook appear to have less anxiety and depression and fewer panic attacks, according to a study of thousands of Americans over the course of 18 years.”

The study, published by the American Psychological Association in the Journal of Abnormal Psychology, says: “Perseverance cultivates a sense of purposefulness that can create resilience against, or decrease, current levels of major depressive disorder, generalized anxiety disorder and panic disorder.”

Lead author of the study, Nur Hani Zainal, M.S., from Pennsylvania State University, notes: “Looking on the bright side of unfortunate events has the same effect because people feel that life is meaningful, understandable and manageable…Our findings suggest that people can improve their mental health by raising or maintaining high levels of tenacity, resilience and optimism.”

No one said it would be easy…Something to be said for baby steps.

As Rev. King once observed, “You don’t have to see the whole staircase, just take the first step.”

Had Odysseus not persevered, had he given up, symbolically he’d still be in the Trojan Horse.

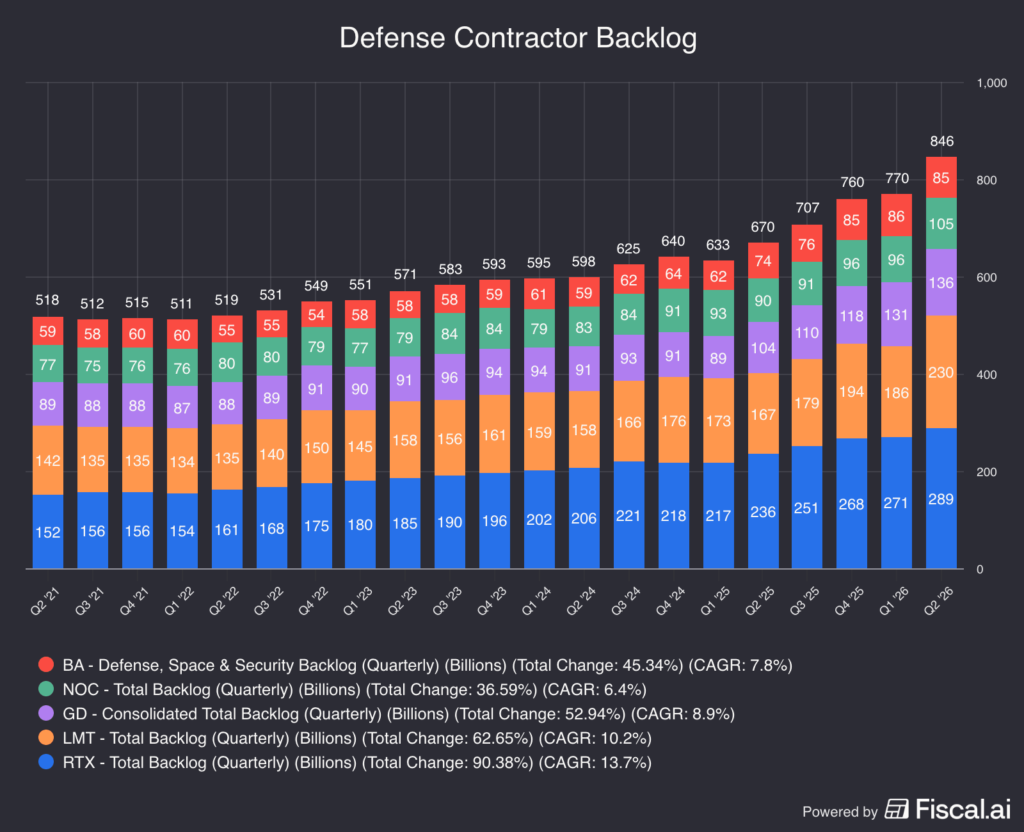

With all the ongoing global conflicts (and the munition replenishment required for those conflicts), the “Big Five” prime defense contractors all reported record orders in the 2nd quarter.

Combined, the five companies (including only Boeing’s defense division) now have a backlog of $846 billion. That’s up $176 billion, or 26%, compared to the 2nd quarter of last year.

Thinking about tackling a long list of renovation projects before putting your home on the market? It’s a common instinct, but bigger isn’t always better when it comes to preparing your home to sell. While some updates can make your home more appealing, others can cost thousands of dollars without adding enough value to justify the expense.

Whether you’re selling a home in Chicago, IL, or preparing to list a house in West Palm Beach, FL, knowing which improvements to skip can help you focus your time and budget on updates that leave the best impression on buyers.

1. Skip major remodels before listing

A full kitchen or bathroom remodel might seem like a smart investment, but these projects are often expensive and time consuming. Unless the space has significant damage or functional issues, there’s a good chance buyers would rather personalize these rooms themselves.

Instead of gutting an entire room, consider making smaller improvements that freshen the space. Small updates like replacing outdated cabinet hardware, updating light fixtures, or repairing worn caulking can help a room feel well maintained without the price tag of a full renovation.

2. Luxury upgrades aren’t always worth the investment

Installing high-end appliances, custom built-ins, or premium finishes may sound like a great way to attract buyers, but luxury features don’t always deliver the return sellers expect.

Every buyer has different tastes, and features that feel like must haves to one person may not appeal to another. Rather than investing heavily in upgrades that could go unnoticed, focus on presenting a clean, functional home that allows buyers to imagine making it their own.

3. Think twice before replacing flooring

Worn or damaged flooring can certainly affect a buyer’s first impression, but replacing perfectly functional floors simply because they’re not your style may not be necessary.

Professional carpet cleaning, refinishing hardwood floors, or making minor repairs can often refresh a room at a fraction of the cost of installing brand new flooring. If the existing flooring is in good condition, many buyers will appreciate having the opportunity to choose their own finishes after moving in.

4. Avoid overdoing the landscaping

Curb appeal plays an important role in attracting buyers, but that doesn’t mean you need to completely redesign your yard before listing.

Large landscaping projects, mature tree installations, or elaborate outdoor features can quickly become expensive and may not increase your home’s value enough to offset the cost. Instead, focus on simple maintenance like mowing the lawn, trimming shrubs, pulling weeds, adding fresh mulch, and planting a few seasonal flowers to create a welcoming first impression.

5. Be careful with DIY projects

Taking on home improvement projects yourself can save money, but only if they’re done well. Uneven tile, sloppy paint lines, poorly installed fixtures, or unfinished projects can leave buyers wondering what other maintenance may have been overlooked.

If you’re not confident completing a project correctly, it may be better to leave it to a professional or skip it altogether. Buyers generally respond better to a home that feels properly maintained than one filled with noticeable DIY mistakes.

6. Focus your budget on simple improvements that make an impact

When preparing to sell, the goal isn’t to create a brand new home. It’s to help buyers see a property that has been cared for and is ready for its next owner.

“Cleaning, decluttering, and applying a fresh coat of paint are appealing to buyers and make the home look more spacious,” says Tommy Decebal Adamescu, Board Certified Master Home Inspector at HomeSpector, Inc. “Servicing the mechanical systems and maintaining the landscape can also have a good impact without overspending.”

Simple improvements like deep cleaning, decluttering, touching up paint where needed, and making sure heating, cooling, and plumbing systems are functioning properly can go a long way toward creating buyer confidence without stretching your budget.

7. Preparing your home without overspending

It’s easy to assume that selling a home requires expensive renovations, but that’s rarely the case. Instead of investing in projects with uncertain returns, focus on improvements that help your home look clean, well maintained, and move in ready. By prioritizing practical updates over costly remodels, you can make a strong first impression while keeping more money in your pocket.

If you are represented by an agent, this is not a solicitation of your business. This article is for informational purposes only, and is not a substitute for professional advice from a medical provider, licensed attorney, financial advisor, or tax professional. Consumers should independently verify any agency or service mentioned will meet their needs. Learn more about our Editorial Guidelines here.

Kierra Todd is a content marketing strategist at Redfin, where she crafts engaging stories about shopping for homes and open houses. Originally from Alexandria, VA, she enjoys returning home for special occasions and holidays to spend time with family. Her dream home blends warm, traditional charm with modern design and plenty of space to host friends and loved ones.