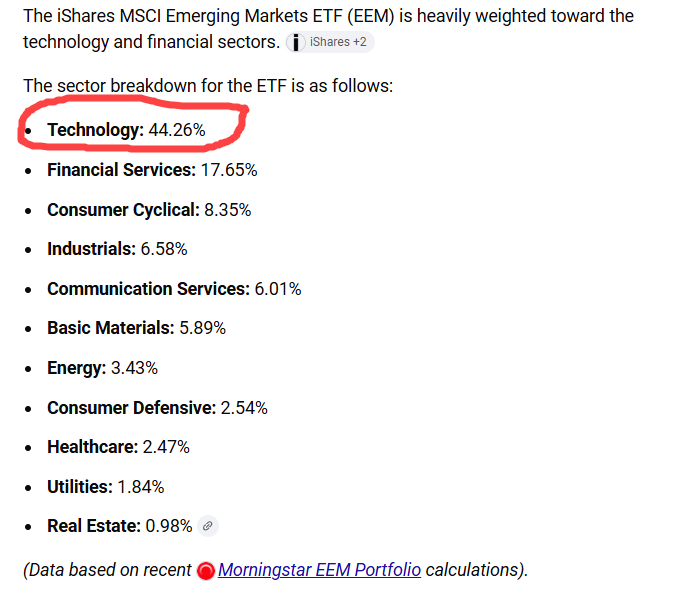

1. Emerging Markets Now Tech Stock ETF—44% Weighting

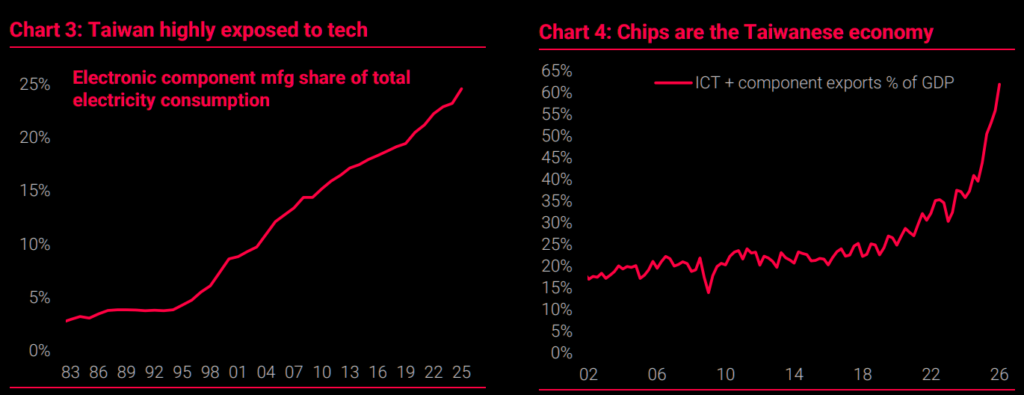

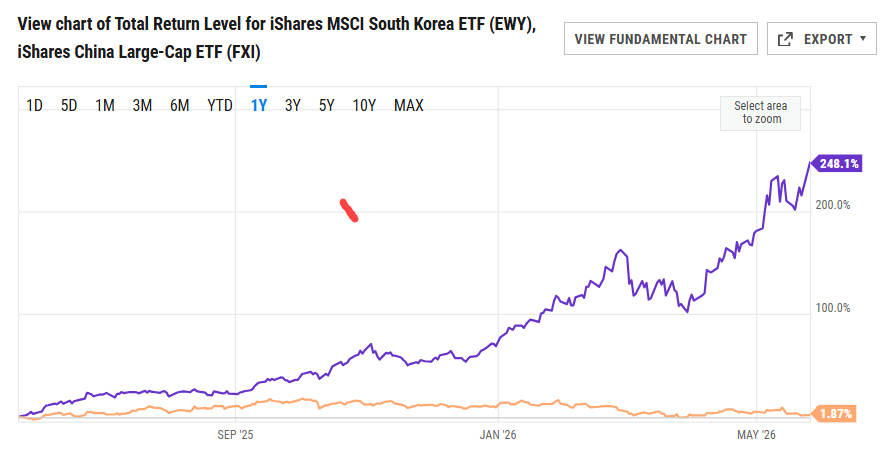

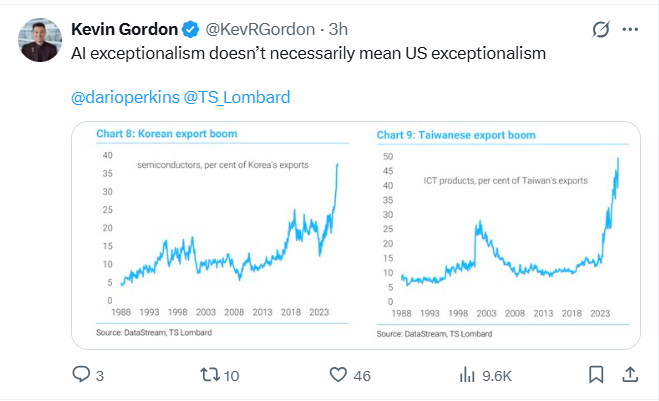

2. Korean and Taiwanese AI Export Boom

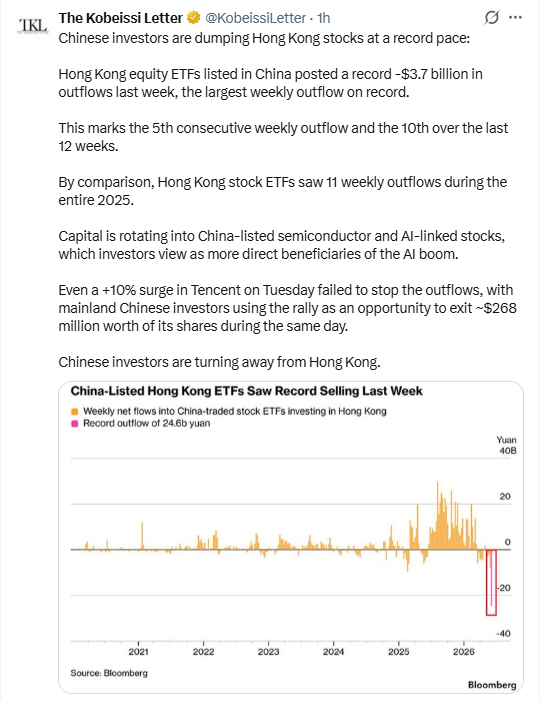

3. Chinese Investors Dumping Hong Kong Stocks—Buying Chinese AI and Chips

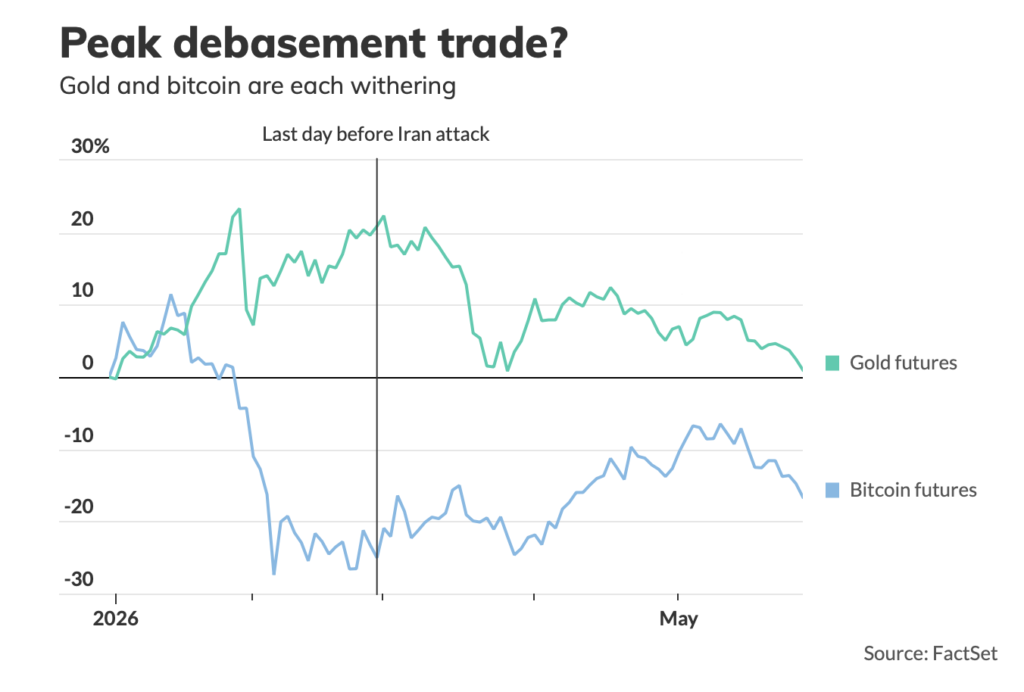

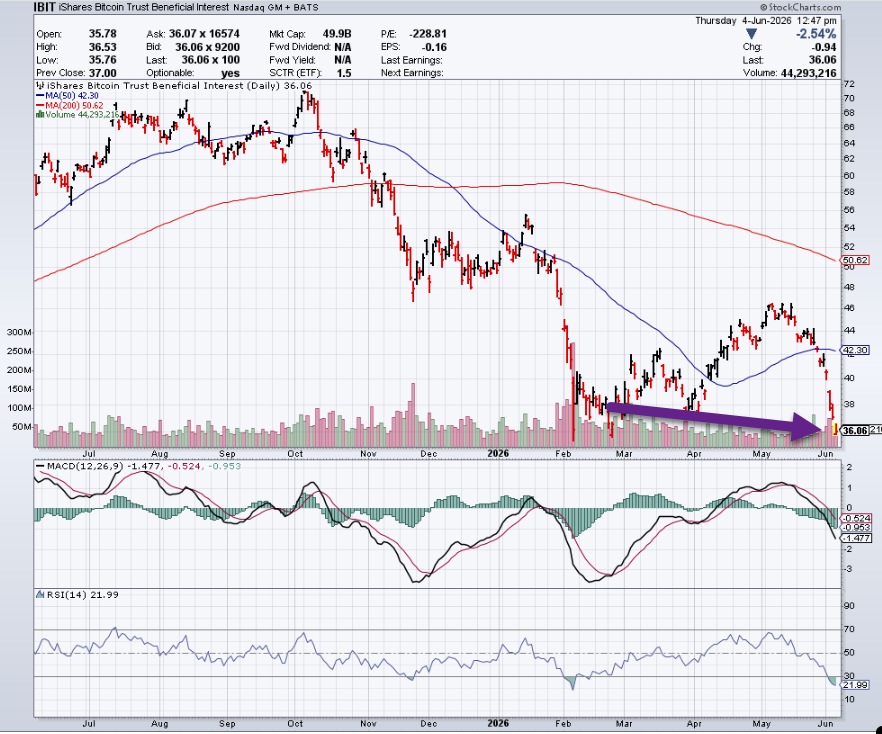

4. Bitcoin ETFS Longest Streak in a Row of Net Outflows

On Tuesday, bitcoin ETFs registered their 12th day in a row — and longest streak ever — of net outflows, according to SoSoValue. Net assets across bitcoin ETFs fell to $85 billion from $107.8 billion on May 14.

Bitcoin is down 12% week-to-date after some fear-based unloading on Monday — following Strategy’s minor sale of 32 coins — triggered a cascade of long liquidations that accelerated the downward pressure.

IBIT ETF New YTD Low.

StockCharts

5. COIN Coinbase Stock at Support Going Back to 2024

StockCharts

6. LLY Breaks Out to New Highs

StockCharts

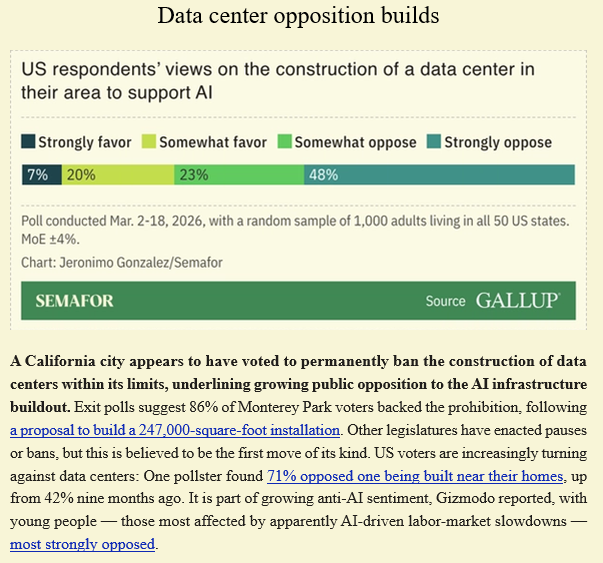

7. Data Center Build Out 70% Of Americans Oppose

Semafor

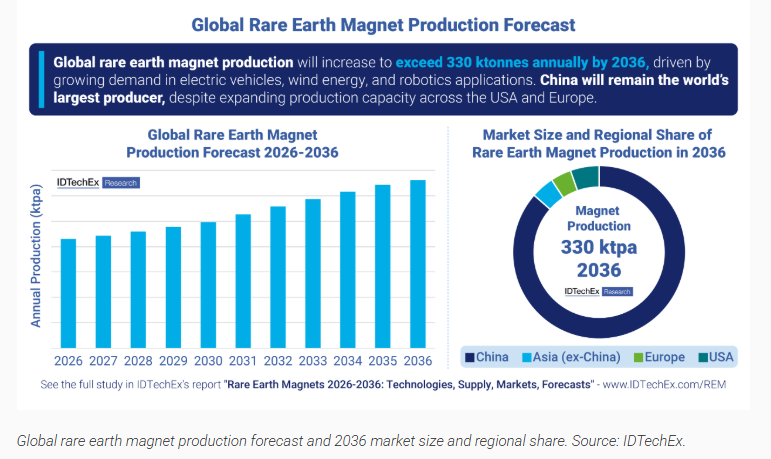

8. The World Will Need 3x the Amount of Magnets in 10 Years….China 80% of Production

IDTechEx

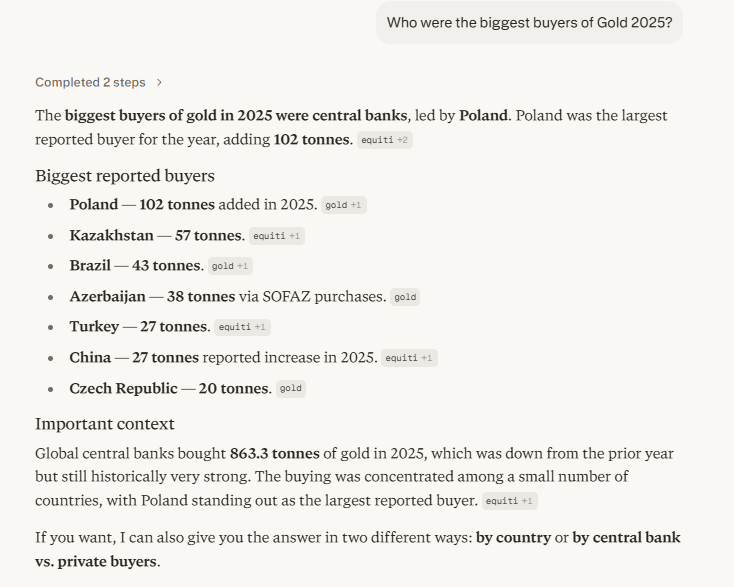

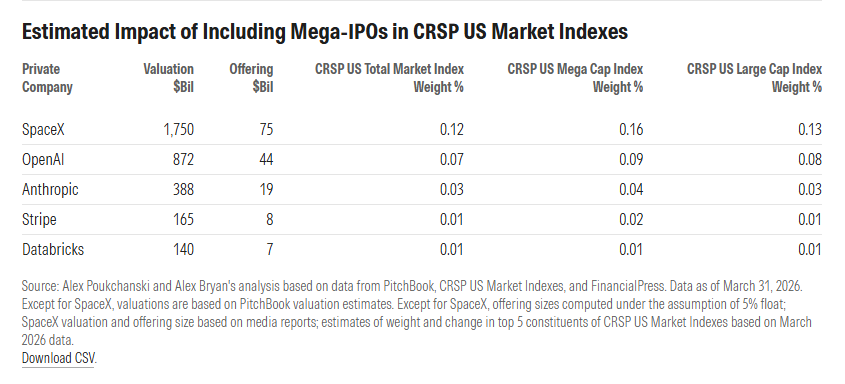

9. Mega-IPOs Will Be Small Weight in Indexes

How Will Mega-IPOs Change the Face of the US Stock Market?

The effects of SpaceX and other big private companies going public won’t be sweeping or come all at once. Dan LefkovitzThe Alexes estimate initial weights for the mega-IPOs in CRSP market indexes based on their float-adjusted market capitalization. The impact is smallest in the total market index but greater for both the CRSP US Large Cap Index and the CRSP US Mega Cap Index. At a $75 billion float-adjusted market capitalization, SpaceX would receive a 12-basis-point (0.12%) weight in the total market index, falling well outside the top 100 constituents. (As weights adjust and constituents are reshuffled, indexes will experience some turnover, which is quantified in the paper.)

Estimated Impact of Including Mega-IPOs in CRSP US Market Indexes

Source: Alex Poukchanski and Alex Bryan’s analysis based on data from PitchBook, CRSP US Market Indexes, and FinancialPress. Data as of March 31, 2026. Except for SpaceX, valuations are based on PitchBook valuation estimates. Except for SpaceX, offering sizes computed under the assumption of 5% float; SpaceX valuation and offering size based on media reports; estimates of weight and change in top 5 constituents of CRSP US Market Indexes based on March 2026 data.

Morningstar

10. Habits of High Performers

Cognitive Performance Habits (40-52) success.com

Your brain is not built for constant output. It operates in cycles. These habits are about working with your neurology rather than against it.

40. Time-block your deep work in two-hour windows. Research on ultradian rhythms—the brain’s natural 90- to 120-minute focus cycles—suggests that peak cognitive performance happens in distinct windows, followed by dips. Two-hour blocks align with this cycle. Schedule your hardest work in your biological peak hours.

41. Do your most important task before noon. For most people (non-night-owls), prefrontal cortex activity is highest in the first half of the day. Use it on creative, strategic or complex work. Use the afternoon for communication, admin and meetings.

42. Shut off notifications during focus time—completely. Not silenced. Off. A notification doesn’t need to be read to break focus; the awareness that one arrived is enough to fragment attention. Studies consistently support the foundational finding that it takes an average of 23 minutes to return to deep focus after an interruption.

43. Write down your top three priorities before you start each day. Not a full to-do list. Three things. This practice forces prioritization under constraint and sets an intention that survives the reactive pull of the morning.

44. Do a weekly review every Friday afternoon. Block 30 minutes. Review what you completed, what didn’t get done and why, and what your top priorities are for next week. This practice prevents the feeling of being perpetually behind and connects daily work to longer-term goals.

45. Read intentionally for 20 minutes a day. Not scrolling. Not trade newsletters. Books. Long-form reading builds sustained attention, strengthens vocabulary and exposes you to ideas at a depth that short-form content cannot replicate.

46. Avoid multitasking during deep work—completely. Your brain does not actually multitask. It switches between tasks rapidly, and each switch carries a cognitive cost. What feels like efficiency is usually just faster degradation of output quality.

47. Create a “shutdown ritual” to end your workday. Close your tabs, write tomorrow’s top three goals and say a specific phrase that signals the day is done. This ritual—as small as it is—trains your brain to disengage from work mode and makes the transition to personal time more successful.

48. Keep a decision journal. Log important decisions with your reasoning at the time. Review it quarterly. High-performers who track decisions improve their judgment not because they think harder in the moment but because they learn from patterns they would otherwise forget.

49. Batch your email and Slack into two or three windows per day. Constant inbox monitoring is the cognitive equivalent of allowing interruptions every 10 minutes. Set windows—morning, midday, late afternoon—and let the rest wait.

50. Learn something new outside your domain once a week. Cross-domain learning is consistently linked to creative thinking—research shows that knowledge breadth, especially in mid-career, is one of the strongest predictors of creative output. Read something in a field adjacent to yours. Take a course. Attend a talk.

51. Reduce daily decision volume wherever possible. Steve Jobs’ black turtleneck was famously a decision-reduction strategy. You don’t need to go that far. But standardizing low-stakes decisions—meals, clothes, default responses—preserves cognitive resources for decisions that actually matter.

52. Protect your thinking time like it’s revenue-generating. Because it is. Block 30 to 60 minutes of unstructured thinking time on your calendar at least twice a week. No deliverables. No agenda. Just space to process, connect and generate. Most high-performers consider this their most productive time once they build the habit.