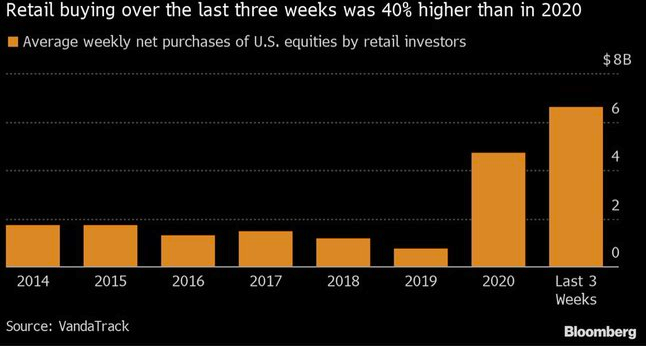

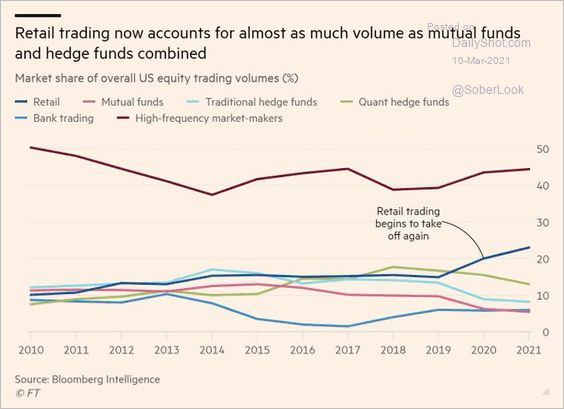

1. Retail Trading Now Accounts for Almost as Much Volume as Mutual Funds and Hedge Funds Combined.

The average Robinhood user is 31 years old and has a median $240 account balance. Just 2% are ‘pattern day traders.’ A MagnifyMoney survey polled young investors on where they get their investing information. 41% of the more than 1,500 people polled said they watch YouTube and 24% said they take the cues from people on TikTok. 22% of the polled investors traded stock at least once a week.

Continue readingFollow up from yesterday…Small cap value 50 day about to cross thru 200 day to upside.