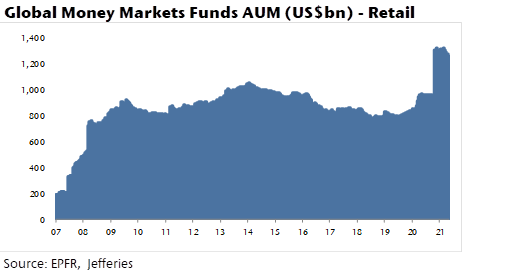

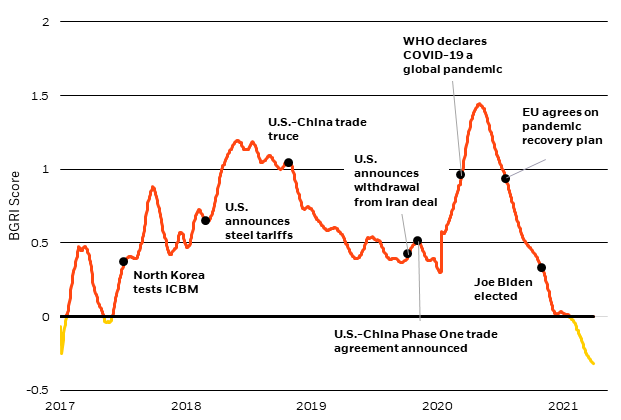

1. Market’s Attention to Geopolitical Risk Drops to Negative….Lowest in 5 Years.

Chart of the week-BlackRock Geopolitical Risk Indicator – global

Chart of the week-BlackRock Geopolitical Risk Indicator – global

Eddie Spence and Nishant Kumar

https://finance.yahoo.com/news/gold-set-tear-even-higher-230000863.html

Dollar Index 50 day closed below 200 day….breaking support

©1999-2021 StockCharts.com All Rights Reserved

Consensus is higher but yield on 30 year only rallied back to 2019 levels

©1999-2021 StockCharts.com All Rights Reserved

4.ARK Innovation Fund Update

ARKK had -37% correction…

©1999-2021 StockCharts.com All Rights Reserved

However….Longer-Term chart ARKK was below $50 pre-covid.

©1999-2021 StockCharts.com All Rights Reserved

Spinoffs historical alpha generating strategy about to break out to another new high

Will this gap close?

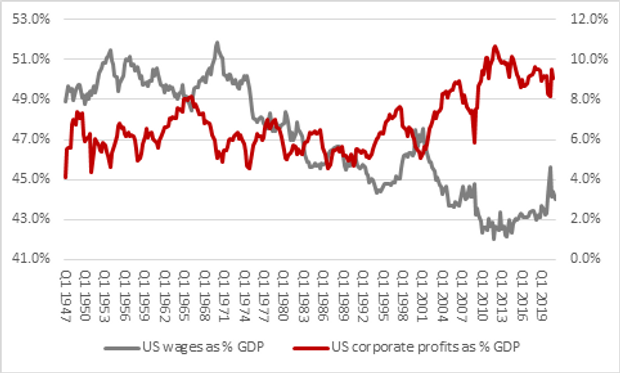

CHART VIA AJ BELL. SOURCE: ST. LOUIS FEDERAL RESERVE DATABASE, U.S. BUREAU FOR LABOR STATISTICS

Between stories of fast-food restaurants struggling to find burger flippers and news that Amazon will hire 75,000 workers at an average pay of more than $17 an hour — well above U.S. minimum wage — rising pay is on the mind.

“Workers and their families may well be thinking ‘about time, too,’” said Russ Mould, an analyst at AJ Bell, who provided our chart of the day. “Since 1947, Americans’ pay has fallen by 5 percentage points as a portion of GDP. American corporate profits have increased by almost exactly the same amount.”

Retail gasoline prices are at about $3.04 a gallon on average nationwide, the most expensive since 2014 – And after a year of lockdowns to curb the coronavirus pandemic, tens of millions of American road-trippers are expected to be stung by those prices: More than 34 million Americans are expected to take to the highways between May 27 and May 31, AAA expects, an increase of 53% from last year but still down 10% from 2019.

From Dave Lutz at Jones Trading

Advisor Perspectives Blog –Furthermore, given the extremely high correlation between stocks and bonds, a level of extreme not seen since the “Dot.com” peak

The Fed will continue to supply liquidity, which will help the market ignore the reality of the majority of return barometers. However, as we saw in March of 2020, that does not preclude hair-raising volatility and significant declines. But, to Yardeni’s point, in the short-term Fed liquidity does support prices on the margin regardless of the environment.

So. Much. Crypto-Cullen Roche

I am about to write a post entirely about crypto. But before I do that I want to make it clear that this space gets WAY too much attention. I mean, we’re talking about an asset class that is incredibly small relative to the scope of the global financial asset portfolio. At just 1% of global financial assets the entire crypto space is about the size of Amazon. Amazingly though, the crypto space dominates the airwaves. It’s virtually all anyone can talk about these days. So, here I am to pile on.

Of course, the reason it’s getting so much attention is because of the sharp increase in prices. Crypto is the get rich quick narrative of the year. Or, more recently, the get poor quickly narrative. I was looking at the long-term charts of this space and it’s just incredible. Here’s the recent rise and fall:

And here’s the max drawdown chart. This is an asset class that has only existed for 10 years and has already experienced three drawn out 80% declines. Amazing stuff and kudos to the people who actually held on through all of this.

I don’t really know where I am going with all of this. I guess I am trying to add some broader perspective around narratives that some times make crypto seem much more important to our economy than it really is. Which, I guess is consistent with how the financial media tends to focus on these things. The highest flyers get the most attention, whether it’s a silly ad talking about how “Joe Schmo made $1MM betting on XYZ Penny stock” or whatever.

https://www.pragcap.com/three-things-i-think-i-think-crypto-crypto-crypto/

Jeremy Taylor

Thu, May 27, 2021, 8:02 AM·3 min read

Rolls-Royce is notoriously coy about the price of its truly bespoke limousines, yet since this new, outrageously decadent Boat Tail was inspired by the $13 million Rolls-Royce Sweptail from 2017, but with increased complexity, it may easily be the most expensive new car to date. (That title currently resides with Bugatti’s La Voiture Noire, which sold for a reported $18.7 million after taxes.) The stunning cabriolet is named after the tapered rear end—a style which dates back to the 1920s, when cars like the Auburn 851 Speedster and Bentley Speed Six Boat-Tail were the talk of the town.

In the very early days of boat-tail design, engineers would simply fix the hull of a boat onto the rolling chassis of a car, creating a streamlined automobile with a nautical theme. It’s a design which disappeared gracefully into the history books, until now.

The new Rolls-Royce Boat Tail measures an ocean-going 19 feet in length and is based on the aluminum spaceframe platform shared by the Phantom, Cullinan and new Ghost models, and it shares the same 6.75-liter V-12 engine. Otherwise, this remarkable car is decked out like no other Rolls-Royce on the planet.

The example showcased is one of three different Boat Tail versions that have been recently hand-built as customer commissions, this one for a mystery man and his wife living Stateside—both believed to be in the music industry. And I was recently granted a sneak preview before the car is ceremoniously handed over.

The most eye-catching feature of this vehicle is the enormous, hand-painted Azur blue bonnet, graduating down to a lighter shade. Up front, a painted Rolls-Royce pantheon grille replaces the traditional stainless-steel finish for the first time in the modern era.

At the rear, twin side-opening compartments are hinged in the middle and open like butterfly wings to reveal an Aladdin’s cave of goodies. On the nearside, a dual champagne cooler was specifically designed to fit bottles of the owner’s favorite Armand de Brignac vintage. On the other side is a set of crockery by Christofle of Paris matched to salt and pepper grinders, all engraved with the car’s name. Caviar is kept cool in a proper onboard fridge—with various other food compartments—rather than a chiller.

The crowning glory, however, is a parasol that slots into the rear of the Boat Tail to provide extra shade. With a stainless-steel shaft and aluminum coupling, the high tensile fabric is stretched over carbon-fiber stays. And just to be sure, it was tested in a wind tunnel.

Rolls worked with Swiss-based House of Bovet to create reversible “his and hers” watches for the couple who own the car. The centerpiece of the minimalist dashboard is a slot to insert one of the timepieces, serving double duty as the Boat Tail clock.

One side of the man’s watch is said to show the celestial pattern above his birthplace. A titanium drawer beneath the “clock” slot is designed to carry another wrist watch, particularly important in this Rolls, as Alex Innes, the head of the marque’s Coachbuild Design department, explained.

“One of the great characteristics of piloting a Rolls-Royce is the light steering and thin steering wheel,” notes Innes. “This particular client likes to remove his wristwatch when driving and hated the idea that it would be stowed of sight.”

The Boat Tail is a four-seat convertible with an emergency tonneau, just in case the heavens open. The car is also provided with a detachable carbon-fiber roof that turns the Rolls into a breathtaking coupe. A lightweight aluminum hoist for the latter is, naturally, included in the package.

https://www.yahoo.com/lifestyle/rolls-royce-boat-tail-may-120200931.html

Momentum Re-Balance (MTUM ETF) –This is sector rotation strategy.

Nice look at the massive sector changes coming in the $MTUM rebalance this month, big move into value stocks. Financials is the new Tech via

Jefferies