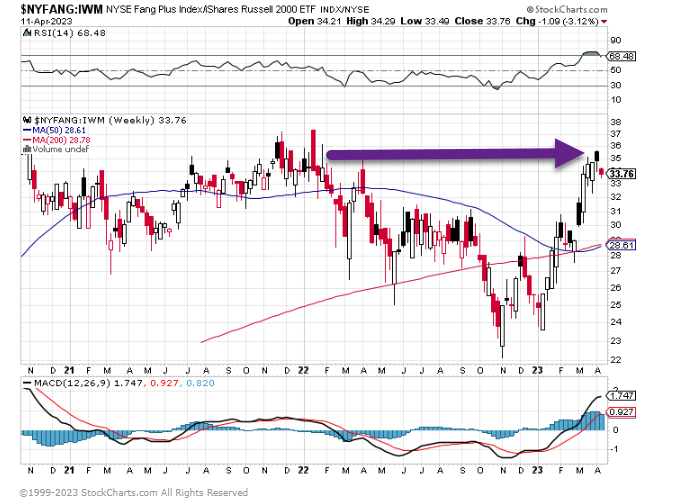

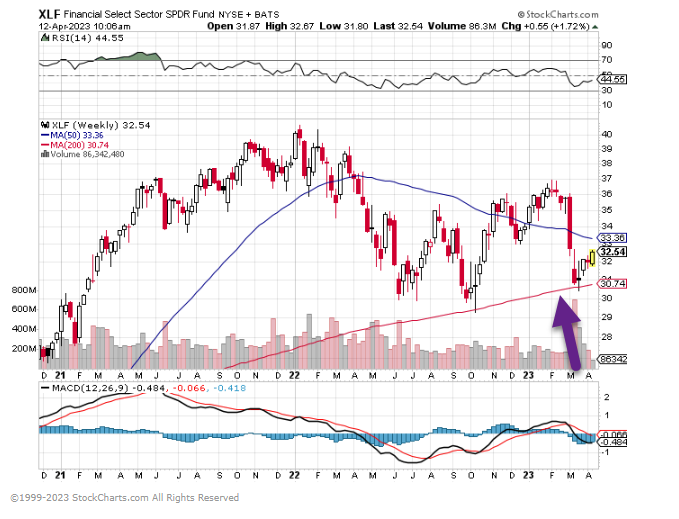

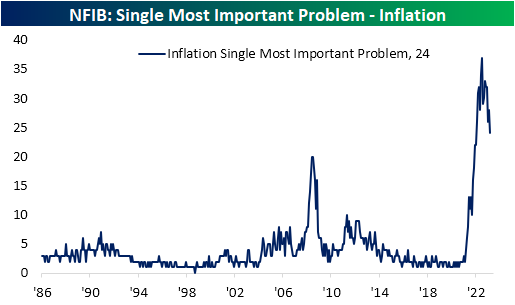

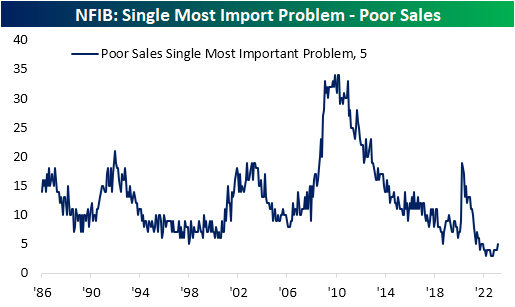

1. Huge Options Trading Around Regional Banks as they Report Earnings this Week.

Dave Lutz at Jones Trading Regional bank share prices have stabilised since SVB’s collapse sparked a massive mid-March slide, but traders are buying record amounts of options tied to midsized lenders that had some of the highest volatility, according to Bloomberg data. Several banks that were badly hit in the recent volatility — including Citizens Financial, Charles Schwab and KeyBank — have seen options interest hit record levels, while many more are at multiyear highs. Pricing of the contracts suggests investors expect stock swings for some banks to be up to three times normal levels, according to FT

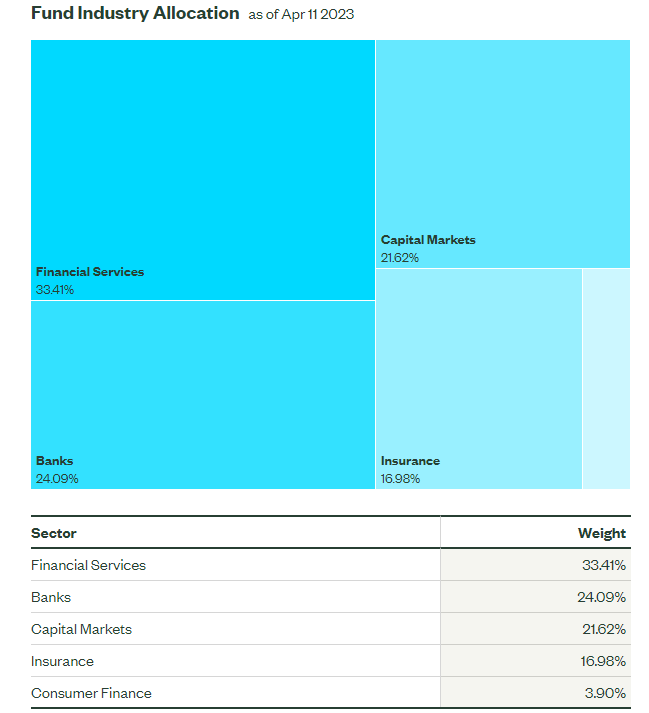

2. Artificial Intelligence Adoption Rates Across Sectors

https://www.capitalgroup.com/advisor/insights.html

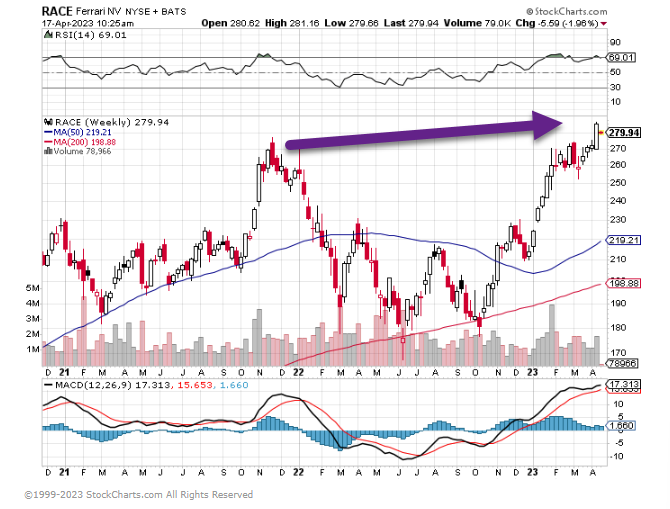

3. No Recession for Ferrari’s…RACE Stock Makes New Highs

RACE vs. Walmart….This chart compares Ferrari to Walmart….Right at Previous Highs

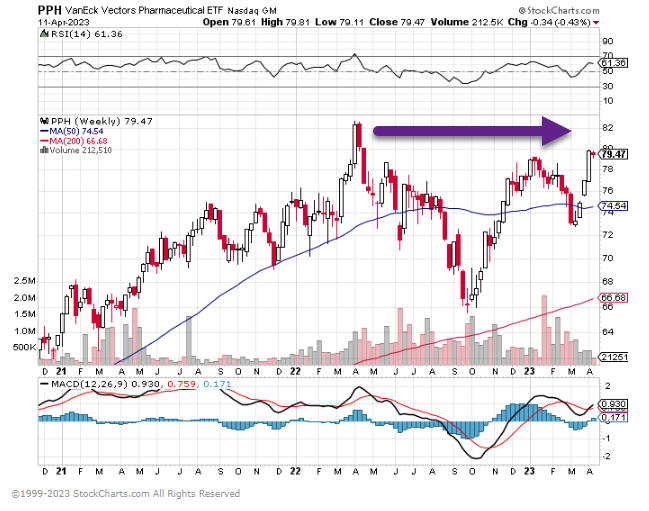

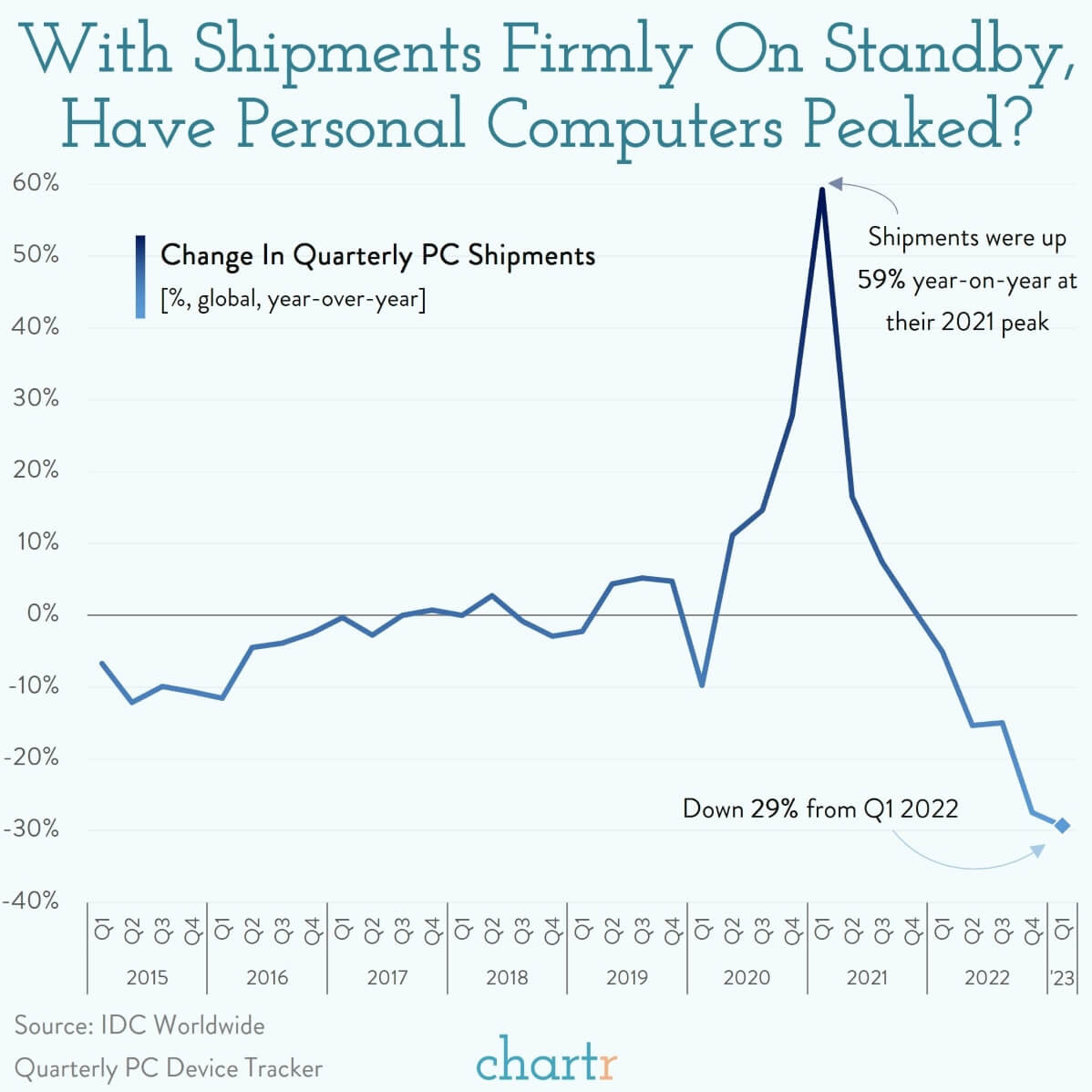

4. Update AI and Robot ETFs.

BOTZ rally off lows still below 200 week moving average

ROBO closes above 200 week moving average

5. MSTR Following Bitcoin…Doubles Off the Bottom

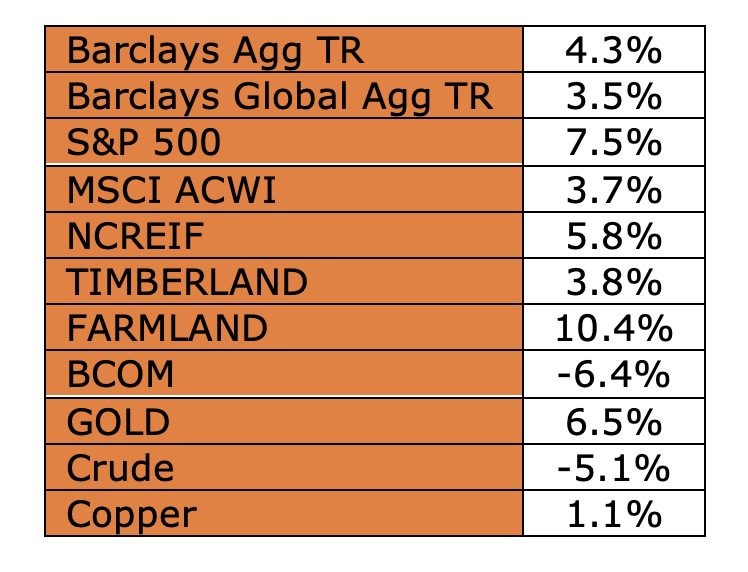

6. 2008-2020 Commodities -73%

Ratio of GSCI to S&P 500 Index, 1998-February 2021

Total Return, 2008 to 2020: Commodities have trailed stock and bond returns since 2008

CAIA Association https://caia.org/blog/2021/04/23/worried-about-inflation-get-real

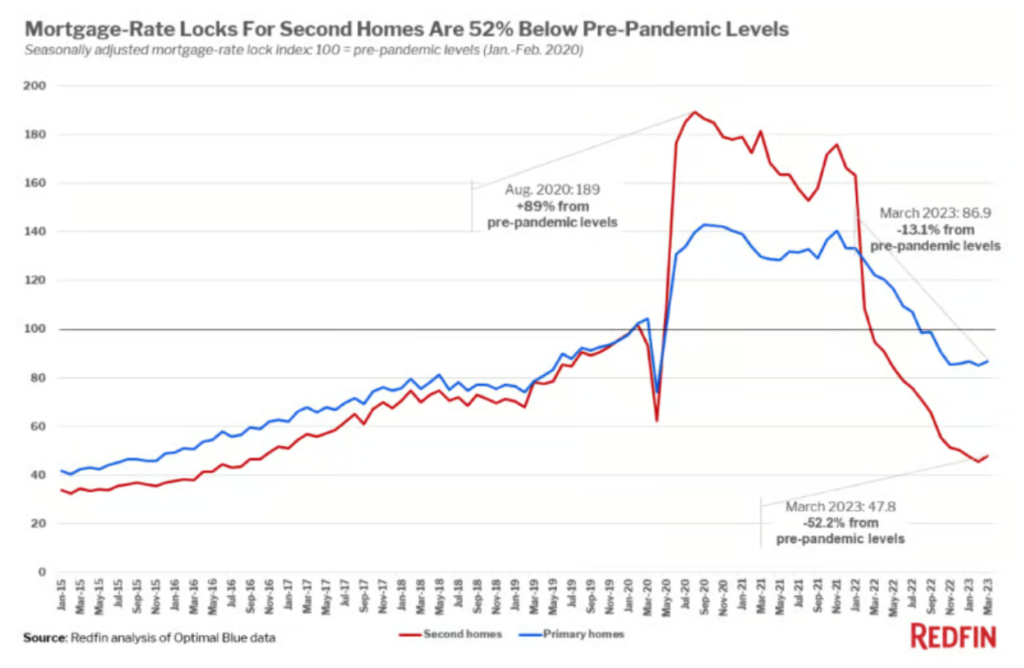

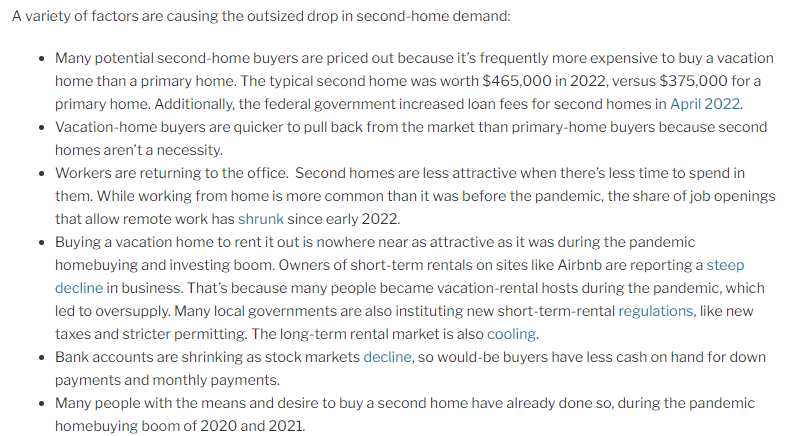

7. Vacation Home Demand Slowing Down…-52% from Pre-Pandemic

Vacation Home Slowdown REDFIN BLOG

Demand for vacation homes has plummeted, now 52% below pre-pandemic levels (Redfin).

What’s driving this? Higher interest rates, the lack of affordability, a decline in remote working, and the cooling rental market are all contributing…

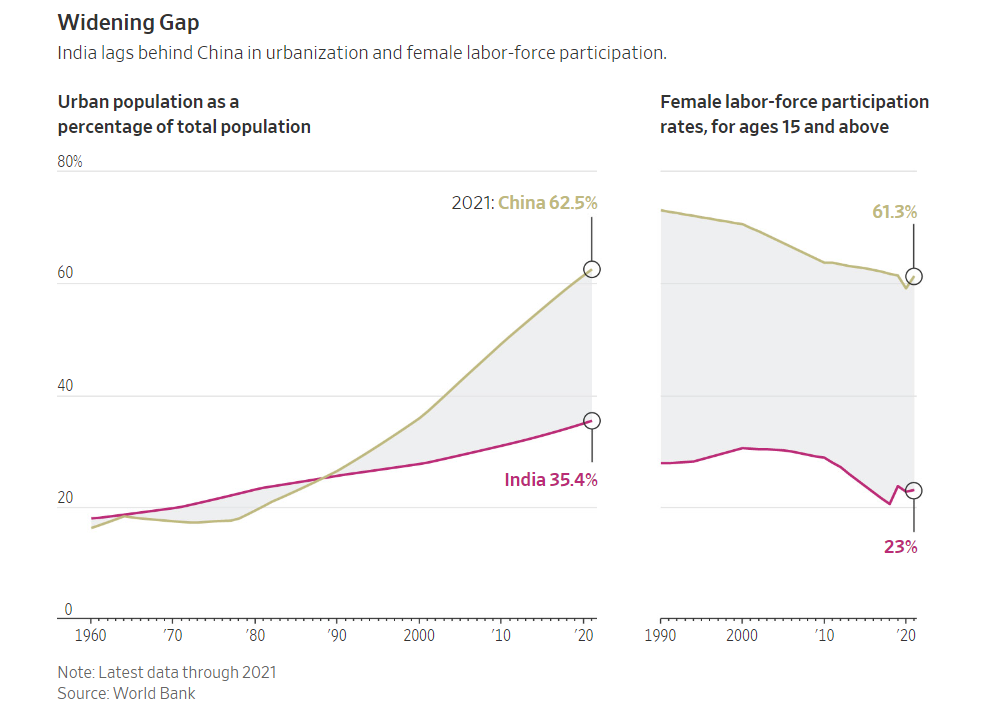

8. Population of India Passed China…Female Labor-Force Participation and Urbanization Far Behind

https://www.wsj.com/articles/india-china-population-economy-9dd7bf27?mod=itp_wsj&ru=yahoo

9. Even More Young Americans Are Unfit to Serve, a New Study Finds. Here’s Why.

U.S. Marines with Charlie Company, 1st Recruit Training Battalion, stand in formation before the motivational run at Marine Corps Recruit Depot San Diego, Sept. 15, 2022. (Grace J. Kindred/U.S. Marine Corps)

Military.com | By Thomas Novelly

A new study from the Pentagon shows that 77% of young Americans would not qualify for military service without a waiver due to being overweight, using drugs or having mental and physical health problems.

A slide detailing the findings from the Pentagon’s 2020 Qualified Military Available Study shared with Military.com shows a 6% increase from the latest 2017 Department of Defense research that showed 71% of Americans would be ineligible for service.

“When considering youth disqualified for one reason alone, the most prevalent disqualification rates are overweight (11%), drug and alcohol abuse (8%), and medical/physical health (7%),” the study, which examined Americans between the ages of 17 and 24, read. The study was conducted by the Pentagon’s office of personnel and readiness.

Read Next: The Army is Having No Issue Retaining Soldiers, Amid a Crisis Recruiting New Ones

Mental health accounted for 4% of disqualifications, while aptitude, conduct or being a dependent accounted for 1% each. Most youth, 44%, were disqualified for multiple reasons.

The updated figures paint a picture of what is currently plaguing military recruiters in many of the service branches, with a shrinking pool of potential service members available to them.

Maj. Charlie Dietz, a Department of Defense spokesman, confirmed that the study shared with Military.com was accurate and said all the services are being challenged by the current recruiting environment.

“There are many factors that we are navigating through, such as the fact that youth are more disconnected and disinterested compared to previous generations,” Dietz said. “The declining veteran population and shrinking military footprint has contributed to a market that is unfamiliar with military service resulting in an overreliance of military stereotypes.”

Lawmakers have been raising the alarm over the recruiting environment throughout the year. Sen. Thom Tillis, R-N.C., the ranking member of the Senate Armed Services Committee personnel panel, said during an April 27 hearing that he was worried the widespread ineligibility of many Americans will contribute to readiness problems.

“To put it bluntly, I am worried we are now in the early days of a long-term threat to the all-volunteer force. [There is] a small and declining number of Americans who are eligible and interested in military service,” Tillis said. He added that “every single metric tracking the military recruiting environment is going in the wrong direction.”

The Council for a Strong America, a nonprofit organization made up of retired military officers, law enforcement and business leaders that advocates for better nutrition and healthy lifestyles among kids, issued a press release expressing alarm at the findings.

The group called on lawmakers in Washington to take action so that younger generations would qualify for military service.

“The retired admirals and generals of Mission: Readiness recognize that the underlying causes of obesity cannot be solved by the efforts of the military alone,” the Council for a Strong America said in a statement. “With an increase in youth being ineligible for military service, it is more important than ever for policymakers, including state and local school boards, to promote healthy eating, increased access to fresh and nutritious foods, and physical activity for children from an early age.”

Dietz told Military.com that the Army and most of the service’s reserve components are in jeopardy of missing their FY2022 recruiting goals.

— Thomas Novelly can be reached at thomas.novelly@military.com. Follow him on Twitter @TomNovelly.

10. What SuperAgers show us about longevity, cognitive health as we age

These ‘Betty Whites’ are showing us that with a healthy lifestyle, social connections and resilience, we can lower our risks of cognitive decline

By Richard Sima

April 13, 2023 at 6:00 a.m. EDT

Aging often comes with cognitive decline, but “SuperAgers” are showing us what is possible in our golden years.

“These are like the Betty Whites of the world,” Emily Rogalski said. She is a cognitive neuroscientist at Northwestern University’s Feinberg School of Medicine and associate director of the Mesulam Center for Cognitive Neurology and Alzheimer’s Disease.

She was part of the research team that coined the term “SuperAgers” 15 years ago. It describes people older than 80 whose memory is as good as those 20 to 30 years younger, if not better.

What researchers are learning from SuperAgers and about dementia prevention could allow us to discover new protective factors in lifestyle, genetics and resilience for common changes that arise with aging.

“It’s invigorating to know that there are good trajectories of aging,” Rogalski said. “It’s possible to live long and live well.”

What a good aging trajectory may look like

There are three major trajectories of aging’s effects on our cognition, Rogalski said.

In the pathologic trajectory, cognition deteriorates faster than expected for the age, as in the case of dementia.

The reality is that the biggest risk factor for dementia is aging, said Mitchell Clionsky. Clionsky is a neuropsychiatrist who, with his wife, physician Emily Clionsky, wrote “Dementia Prevention: Using Your Head to Save Your Brain.”

A 2023 report from the Alzheimer’s Association estimates that 1 in 3 Americans older than 85 have Alzheimer’s disease, the most common form of dementia. More hopefully, research has uncovered many of the different risk factors that can be mitigated with lifestyle changes. A 2020 report from Lancet estimates that about 40 percent of dementias may be preventable.

In the normal or average trajectory, research shows, memory and cognitive abilities can begin to decline around your 30s or 40s. By the time most people are 80, on certain memory tests, they can remember about half as much as when they were 50, Rogalski said. Despite being less sharp, older people following this trajectory are still able to function — and thrive — in everyday life.

There is, however, a lot of individual variability.

This variability led to the discovery of the third trajectory: SuperAgers, who even past their 80s appeared to be at least as mentally acute in memory as those in their 50s and 60s.

It is not known what percent of the general population qualifies as SuperAgers, but they appear to be rare, Rogalski said. Even when researchers tried to screen only participants who believed they had good memory, less than 10 percent met the definition.

Over time, researchers followed those enrolled, examining their health, imaging their brains, recording their life histories and asking them to donate their brains to be studied after they die.

“The word I would use to describe this group is resilient,” Rogalski said. Many SuperAgers endured hardship, including extreme poverty, losing family at an early age or surviving Holocaust concentration camps, she said.

SuperAgers tend to have strong positive social relationships, which require a degree of adaptability when there are fewer peers of their age.

One SuperAger lives with his daughter and grandchildren, who do not know much about Frank Sinatra or Franklin Delano Roosevelt, Rogalski said. Instead, the SuperAger asks his grandchildren about their interests: Taylor Swift and Chance the Rapper.

“He laughs at this and finds joy in trying to keep up with what his grandkids are interested in instead of seeing that as too far of a reach or a burden,” Rogalski said. “And I think that that’s a really lovely outlook.”

What makes the brain of a SuperAger special

With age, the brain normally shrinks, especially in the cortex, which is the more evolutionarily recent part of the brain.

Not so with SuperAgers, whose brains appear more youthful in areas implicated in memory and executive abilities.

In the anterior cingulate cortex, a frontal brain region important for many cognitive functions, including attention and memory, SuperAgers had a thicker cortical layer compared with cognitively normal 80-plus-year-olds and even 50-year-olds. SuperAgers also had larger, healthier neurons in the entorhinal cortex, another brain area critical for memory, compared with both their older and 20-to-30-years-younger counterparts.

Intriguingly, SuperAgers also have an abundance of a special type of brain cell known as von Economo neurons, which are believed to be important for social affiliative behaviors. Studies suggest that von Economo neurons were four to five times denser in the anterior cingulate cortex of SuperAgers than in normal 80-year-olds, and even in individuals decades younger.

At the same time, SuperAger brains appear to have added protection against suspected biological hallmarks of Alzheimer’s, with less amyloid beta plaques, a cellular waste product, and neurofibrillary tangles.

Preventing dementia and preserving cognition

Becoming a SuperAger is probably partly because of the genetic lottery, but there are many lifestyle factors we can modify to lengthen our cognitive health span as we age.

“Stop being a dementia worrier, start being a prevention warrior,” Mitchell Clionsky said. “The active approach to this is what’s going to make the difference.”

And it is never too late to address the risk factors we can change, Emily Clionsky said. The average age of her patients who saw benefits was the mid-70s. “My oldest patient was over 100,” she said.

There is no one thing that will ensure healthy cognitive aging, but all these factors are interactive, researchers said. If we start chipping away at the dementia risks and pile on protective factors, we can reap positive effects. Here are some that may help:

· Eat like a centenarianby incorporating fiber-rich foods and nuts into your diet.

· Exercise your body. Most people know the importance of getting up and moving, yet don’t always follow through. “I tell them to examine their ‘but,’” Mitchell Clionsky said. Figure out what is getting in the way of exercising and ask “How do we break it down into something you will do,” he said.

· Exercise your brain. The brain loves a challenge, so do activities that engage your noggin.

· Stay connected. Social isolation and loneliness are risk factors for dementia, while social contact is protective.

· Foster resilience. When something bad occurs, try to embrace the challenge. “What in this can be a learning moment? What in this can be a turning point?” Rogalski said.

SuperAgers cannot only help us age better but also reimagine what is possible in older age.

“I think there’s the possibility to set new expectations in aging and to revalue rather than devalue older adults,” Rogalski said.

Do you have a question about human behavior or neuroscience? Email BrainMatters@washpost.com and we may answer it in a future column.

https://www.washingtonpost.com/wellness/2023/04/13/superagers-brain-cognition-dementia-longevity/