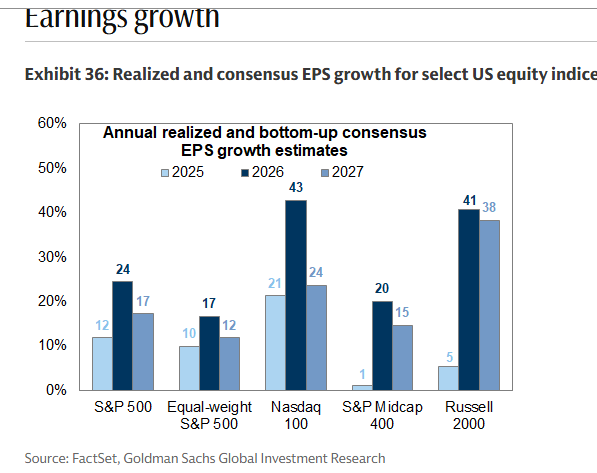

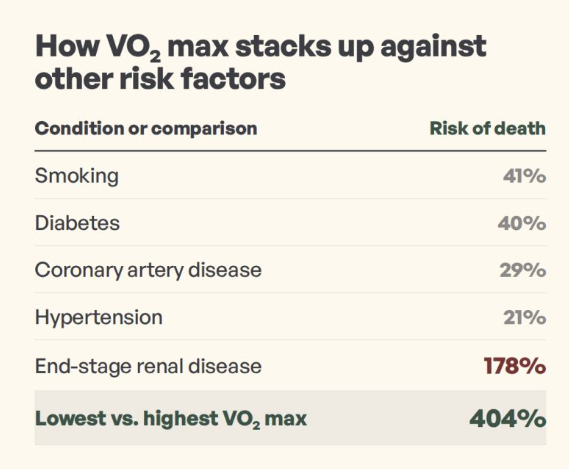

1. Goldman Earnings Growth 2026—43% QQQ and 41% Small Cap

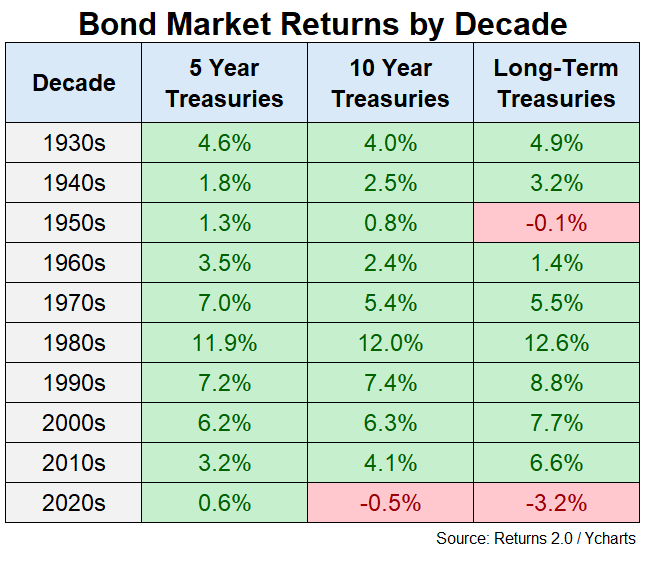

2. The Bond Bear Market-2010’s 3.2% Return…2020’s 0.6% Return

The bond bear market. The 2020s (so far) are the worst decade ever for bond investors:

A Wealth of Common Sense

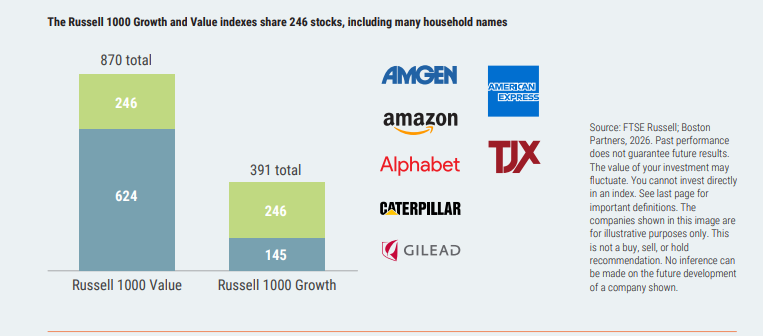

3. The Russell 1000 Growth and Russell 1000 Value Share 246 Names

Savvy Investor

4. Healthcare Services ETF XHS-Breaks Higher After Going Sideways for 3 Years

StockCharts

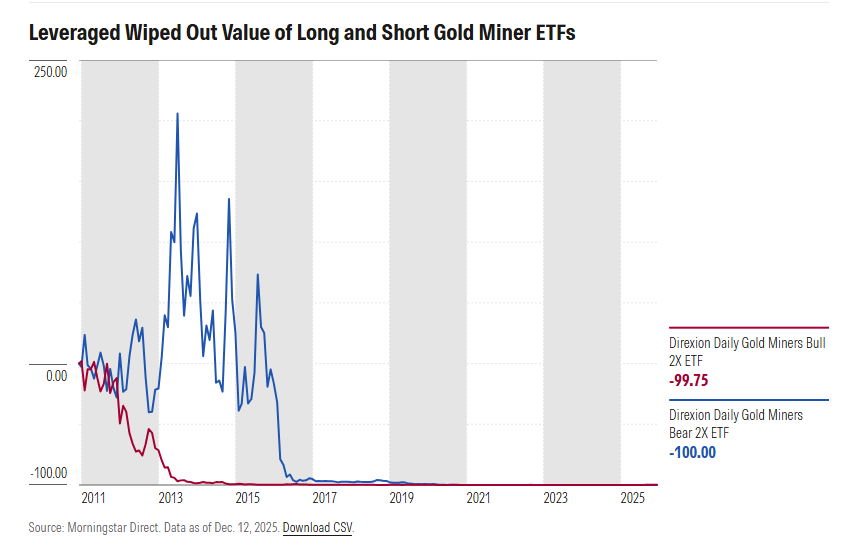

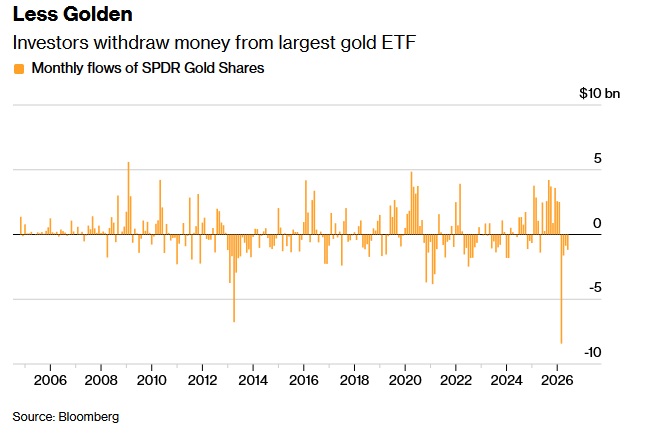

5. Leveraged Bull and Leveraged Bear Gold Miners Wiped Out—Leveraged ETFs Not Buy and Hold

Morningstar

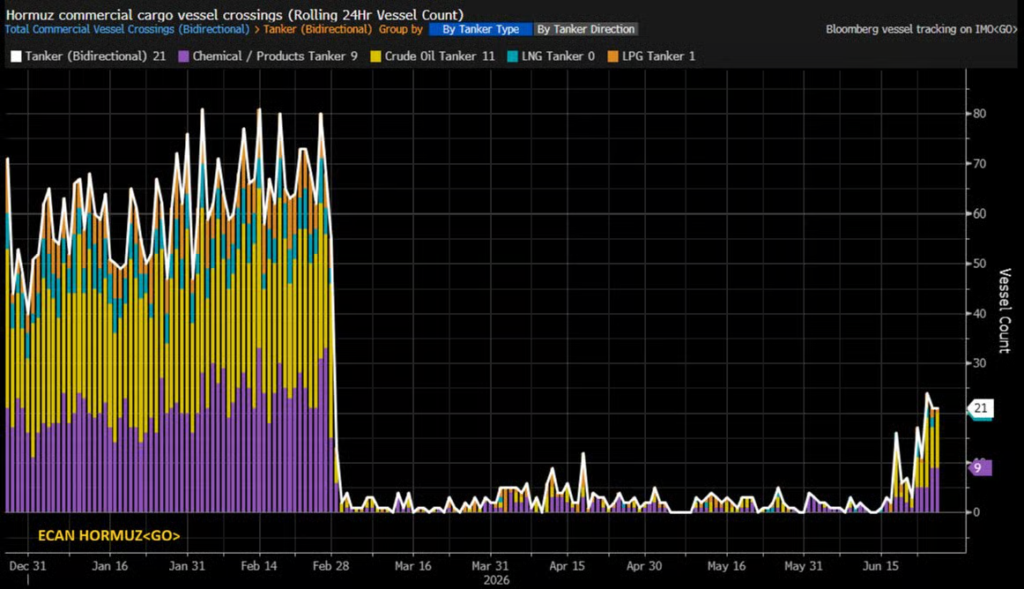

6. Hormuz Traffic Increasing but Well Below Pre-Collapse Levels

Hormuz traffic. “Tanker traffic through Hormuz is recovering, but remains well below pre-collapse levels … Activity has clearly moved off the lows seen from late-February through early June, but the rebound is still modest versus the 50-80 tanker-crossing range seen earlier in the year.”

7. Record $17 Billion Estimated Stolen in Crypto Scams and Fraud in 2025 as Impersonation Tactics and AI Enablement Surge

January 13, 2026 | Chainalysis Team TL;DR

We estimate $17 billion was stolen in crypto scams and fraud in 2025 — as impersonation scams show massive 1400% year-over-year (YoY) growth. AI-enabled scams were 4.5 times more profitable than traditional scams.

Major scam operations became increasingly industrialized, with sophisticated infrastructure, including phishing-as-a-service tools, AI-generated deepfakes, and professional money laundering networks.

Strong connections to East and Southeast Asian crime networks were identified, particularly through forced labor compounds in Cambodia, Myanmar, and other regions, where trafficking victims are forced to operate scams.

Law enforcement made record-breaking seizures, including a 61,000 bitcoin recovery in the UK and a $15 billion seizure linked to the Prince Group criminal organization, showing improved capability to combat crypto fraud.

4. This Chart Shows SMH Semiconductors vs. Mag 7 Stocks MAGS

StockCharts

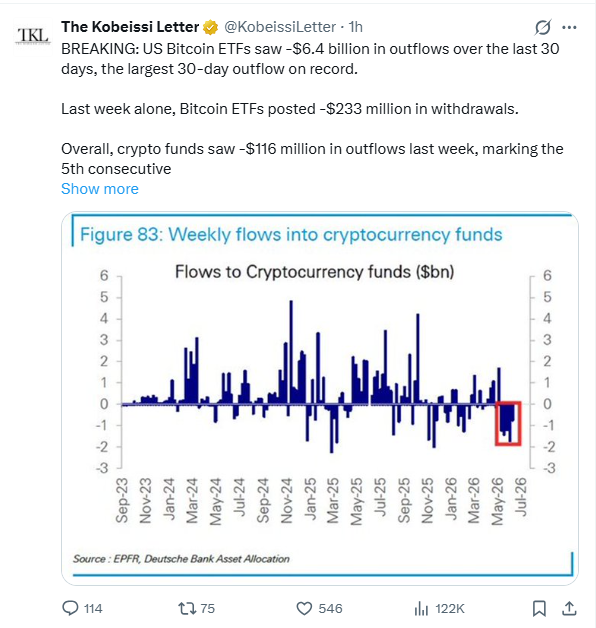

5. History of Bitcoin -50% Drawdowns

Bespoke The chart below shows Bitcoin in the year after each of the prior periods when prices first fell 50%+ from an all-time high. One of the things you always hear about Bitcoin after it sees a large decline like the current one is that “prices always come back”. That’s an accurate statement, but after prices experienced a 50% haircut in the three prior periods, the road back to new highs wasn’t necessarily short or smooth.

As shown in the chart, one year after each of the prior three periods, Bitcoin was lower a year later than it was when the drawdown first reached 50%. Not only that, but in two of the three periods, it barely even experienced a bounce. The one exception was after the June 2021 drawdown when prices quickly rebounded to new highs, but almost as quickly returned back to new lows. Perhaps the best thing Bitcoin has working in its favor is that you don’t hear much about $500,000 or even million-dollar price targets anymore.

Bespoke

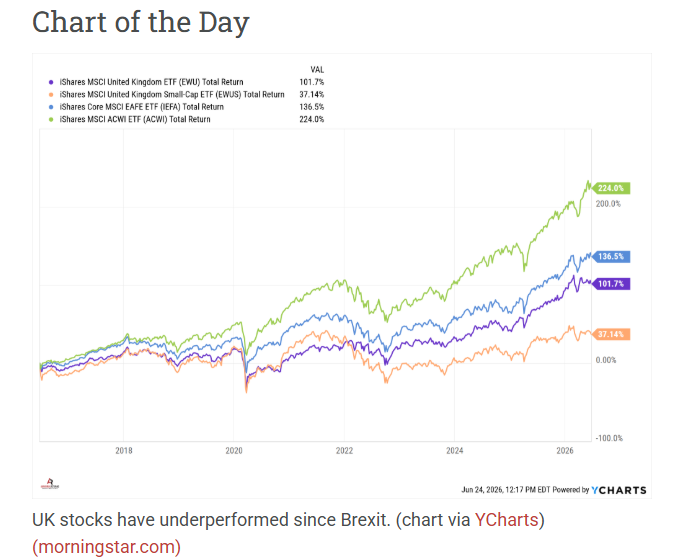

6. United Kingdom Market Underperformance

Abnormal Returns

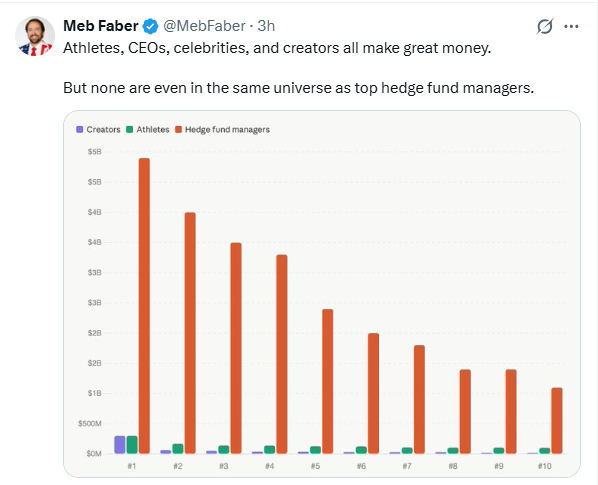

7. Hedge Fund Managers Earnings Dwarf Pro Athletes

Meb Faber

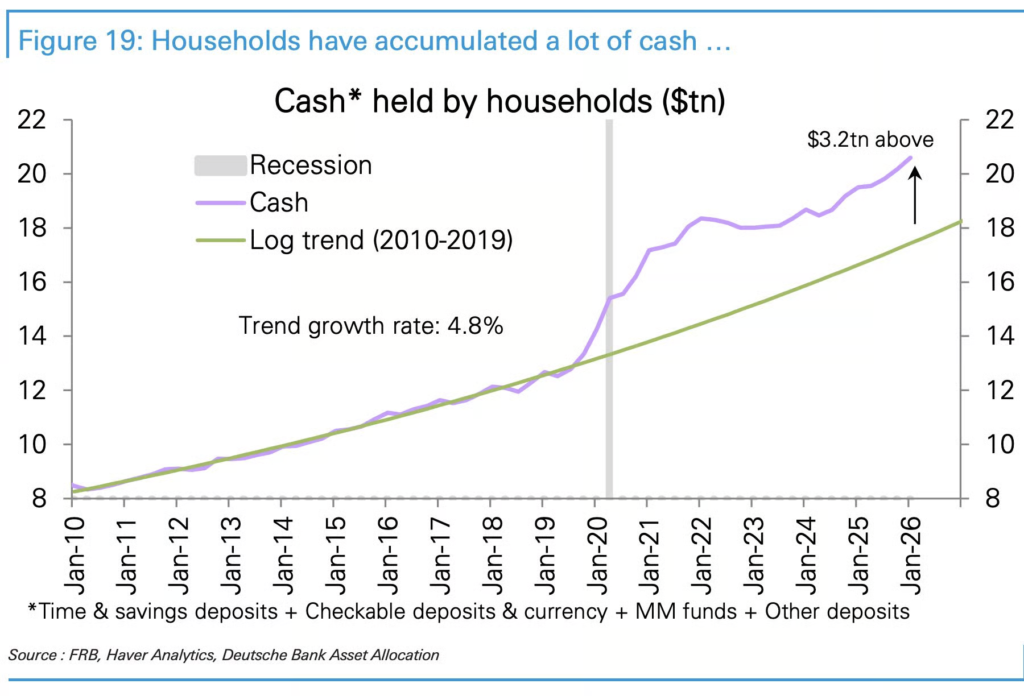

8. Households Sitting on $3.2 Trillion in Cash Plus $8 Trillion Money Markets

Household cash. “U.S. households are sitting on $3.2 trillion of cash”.

10. 10 Meaning Questions for Your Midlife and Retirement

Reflections to make a difference in the direction and quality of your life.-Psychology Today Elaine Dundon

Key points

Retirement can often present a crisis of meaning.

It is up to us to determine how we will embrace midlife and beyond.

Our choices are shaped by our inner perception of ourselves.

We are the ship that travels our life’s journey, our odyssey. Along the way, we encounter many adventures; some enjoyable, some challenging, some upsetting.

The phase of retirement and our corresponding older years represent a time where we are faced with new challenges. It is up to us to determine how we will embrace this new phase: growing, evolving, and actualizing our potential; or instead, stagnating, complaining, and even ending up further adrift or shipwrecked.

Socrates, an ancient Greek philosopher, taught us the importance of asking questions to raise our awareness of our thinking patterns, to uncover our biases, assumptions, and blocks, and importantly, to see the direction and consequences of our current thinking.

10 “Meaning Questions”

Here are 10 “Meaning Questions,” derived from my research in MEANINGology, designed to stimulate your deeper understanding of yourself as you prepare for, hopefully, a happy and very fulfilling future:

Our choices are shaped by our inner perception of ourselves. Do you believe you are now too old to change the direction or the circumstances in your life?

In what ways do you feel discontent with your life, question your past decisions, or feel that you failed to manifest the life you thought you would have by now?

Who will you be without the identity you have adopted from your previous jobs, titles, and trophies; social status; or material possessions?

What do you need to do to live more authentically—to stop living by other people’s expectations and instead live a life truly your own?

Do you dread the future or do you see a vibrant future, full of hope and possibility?

Do you prefer the safety of staying the same and within the current borders of your current life or do you want to embrace the challenges of change and growth?

What dreams have you lost along the way? What have you always wanted to learn and experience?

How do you plan to build new social friendships so that you will feel alive and connected and to combat potential loneliness in the future?

How will you contribute to humanity and help to make the world a better place in this next phase of your life?

What is limiting you from moving forward?

Retirement can present a crisis of meaning when we leave the safety of our jobs and find ourselves without the structure of work and without a sense of identity and belonging.

Remember, just because you may have been able to save money for your retirement does not mean you will live a meaningful life during your later years. Life with money but without meaning suggests you are simply surviving, not thriving. As I shared in our book, Prisoners of Our Thoughts1, the world-renowned psychiatrist and existential philosopher Viktor Frankl so wisely concluded, “Even more people today have the means to live but no meaning to live for.”

Now is the time to start reflecting and asking these existential questions that will truly make a difference both in the direction and the quality of your life in midlife and beyond. Outside forces may control the external circumstances but you control your internal world. Importantly, your choices create your own unique journey or odyssey in life. It is up to you. You are the captain of your life voyage! Every day is a new day to be enjoyed, not simply endured.

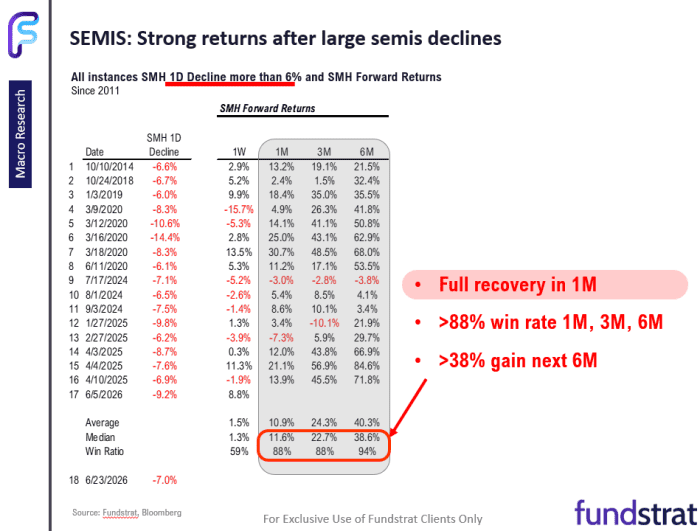

Marketwatch By Steve Goldstein Microchip stocks tumbled on Tuesday, but a look at similar one-day downturns in the semiconductor sector shows the declines are often fleeting.

Tom Lee, the usually bullish head of research at Fundstrat, found 17 other examples of semiconductor stocks falling at least 6% in a single session since 2011, after the VanEck Semiconductor ETF

fell 7% on Monday. That exchange-traded fund is still up 73% this year, driven by the price hikes that producers of memory chips and other semiconductors have been able to pass along to companies building out artificial-intelligence applications.In the previous 17 episodes, Lee said, the median one-month gain for the stocks was 12%, with wins 88% of the time. The median three-month gain was 23%, also with an 88% win rate, and the median six-month gain was 39%, with a 94% win rate.

Marketwatch

9. Oil Gives Back All of the Iran Rally

StockCharts

10. 10-Year Treasury Yield Following Oil Down….Below 4.5%

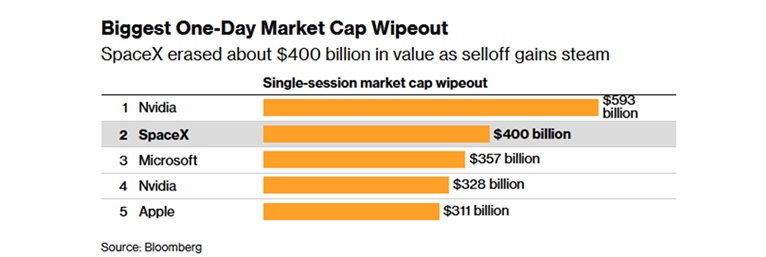

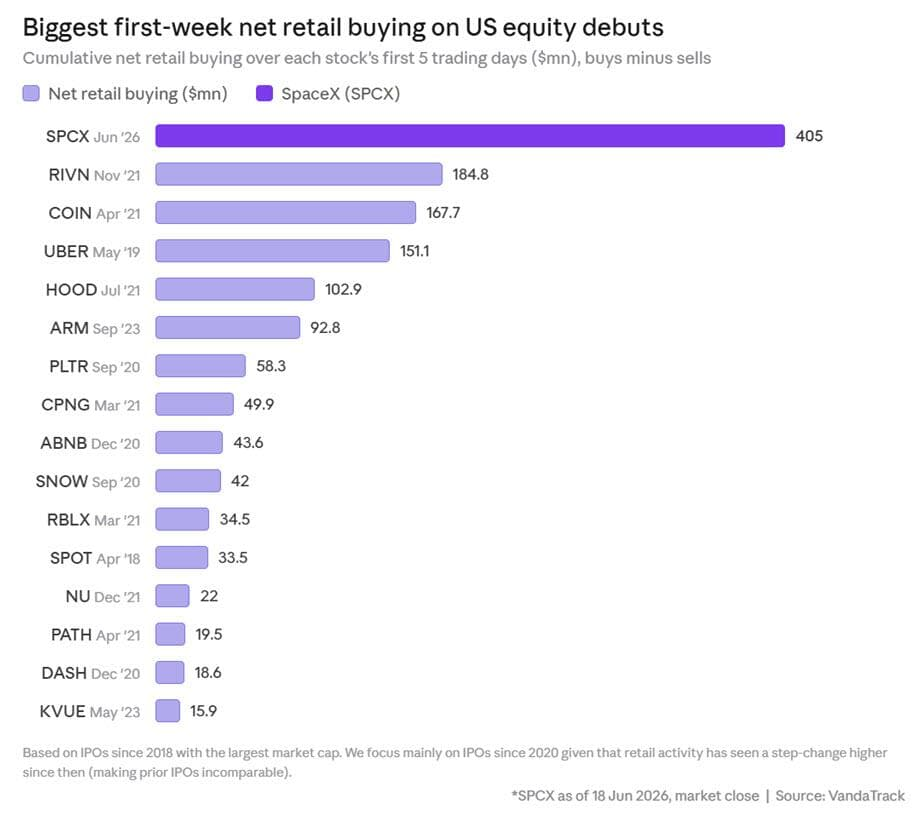

2. Record Amount of Retail Investor Buying in SPCX Last Week

Zerohedge-Vanda Track was even more effusive, and in a retrospective published earlier on Monday wrote that “SpaceX’s first week of trading was one for the record books. Retail investors bought a net $405mn of SPCX during its first 5 trading sessions, comfortably the strongest retail IPO debut in recent history. Retail buying was extreme during the first few sessions before moderating later in the week. The flow profile increasingly resembles a retail investor that is building long-term positions rather than chasing a short-term meme stock.”

ZeroHedge

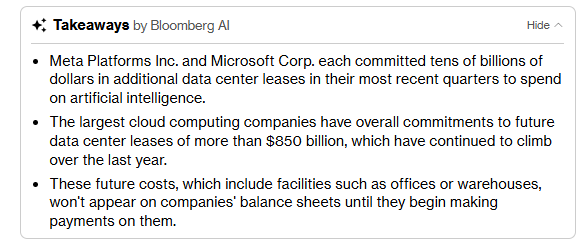

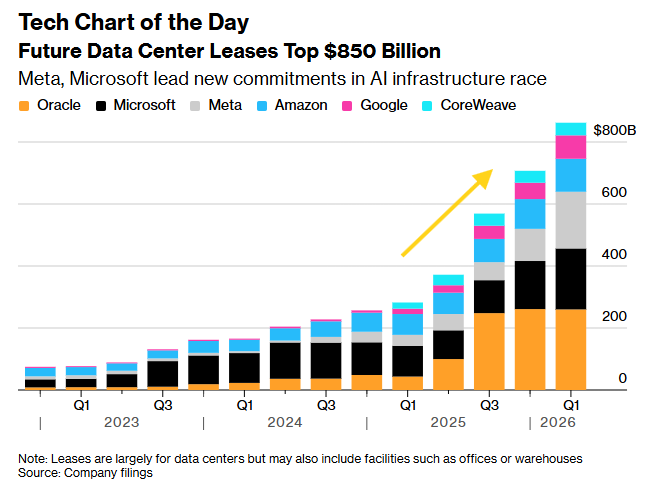

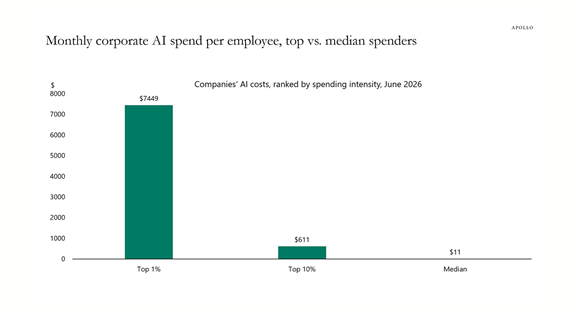

3. AI Corporate Spend Concentrated at Top

The Daily Spark

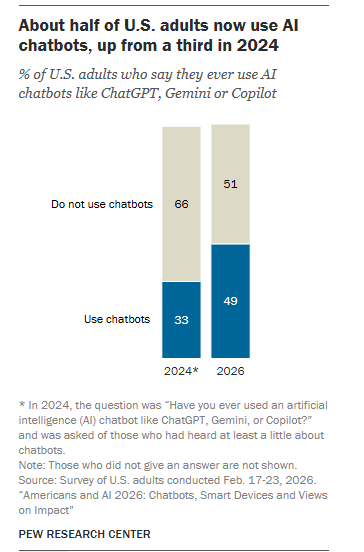

4. But Number of Adults at Home Using AI Chat Box Increasing

Pew Research Center

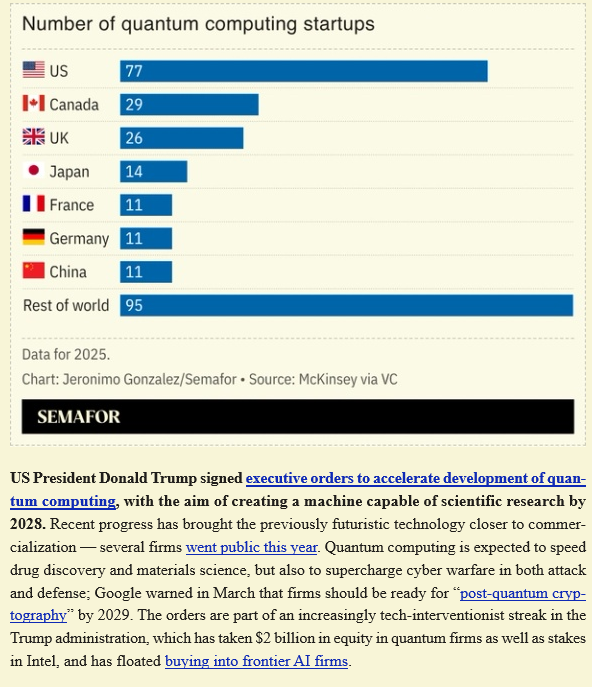

5. U.S. Leading in Quantum Computing

Semafor

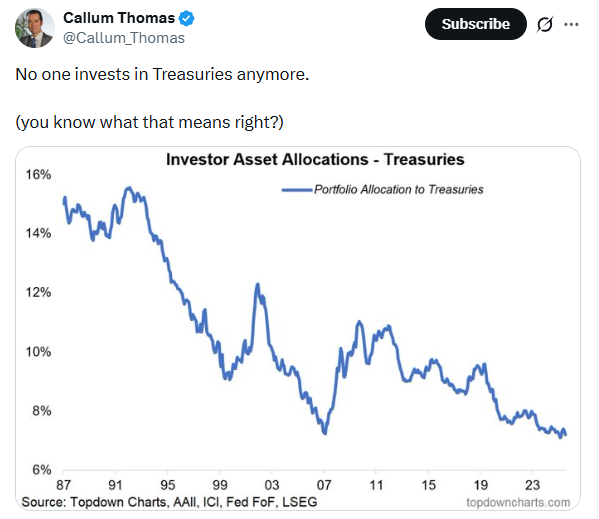

6. No One Invests in Treasuries Anymore

Callum Thomas

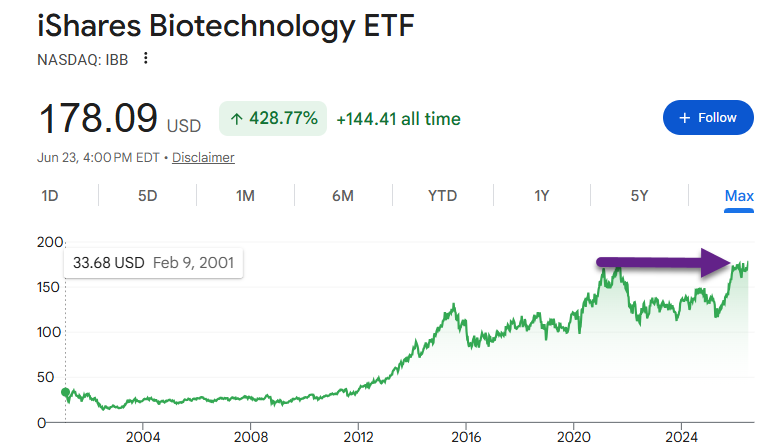

7. IBB Biotech ETF Breaking Out to New Highs

Google Finance

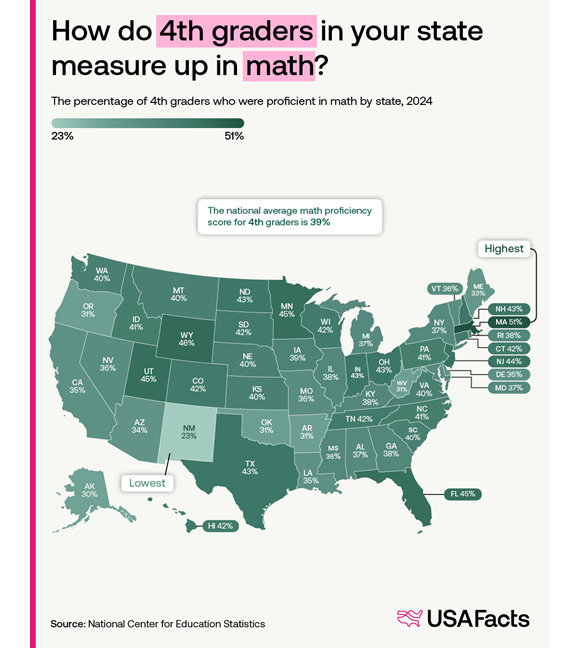

8. How Many 4th Graders in Your State are Proficient in Math

USAFacts

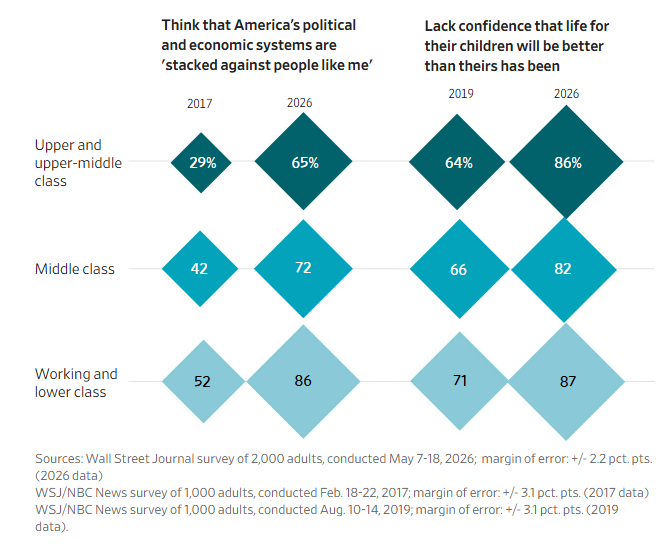

9. WSJ Poll

WSJ

10. Discipline = 3 Core Habits

Discipline essentially comes down to mastering three core habits: setting clear priorities, showing up consistently even when unmotivated, and delaying gratification. Together, these practices shift discipline from a fleeting feeling into a sustainable, everyday system.

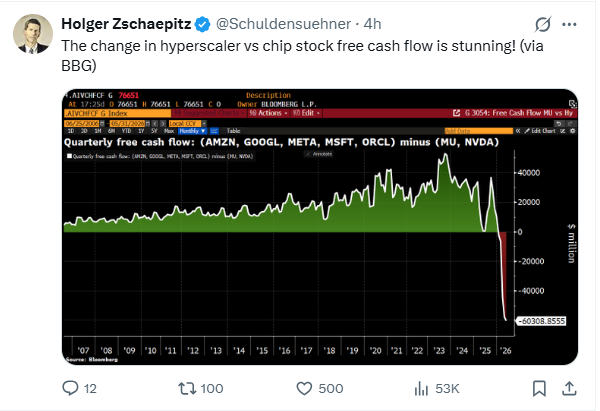

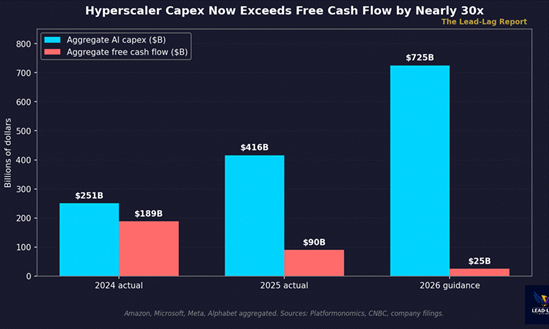

1. Hyperscalers Cash Flow vs. Capex-Lead Lag Report

The four largest hyperscalers spent $416 billion on capex in 2025 and have guided to roughly $725 billion in 2026, while Amazon’s trailing-twelve-month free cash flow collapsed 95%, from $38.2 billion to $1.2 billion.

Aggregate capex now runs about 3.9 times annual depreciation across the hyperscalers. Oracle sits at 8x. These ratios mean the eventual depreciation cliff is being engineered into earnings, not yet absorbed.

AI-tied corporate bond issuance hit $121 billion in 2025, a 332% surge versus the 2020-2024 baseline. AI debt is now 14% of the JP Morgan US investment-grade index — a larger weight than US banks.

Microsoft’s annualized AI revenue is roughly $37 billion against $97 billion of LTM capex — about 38% coverage. MIT’s Project NANDA finds 95% of organizations report zero return on generative AI. The demand side is not keeping pace with the supply side

Substack

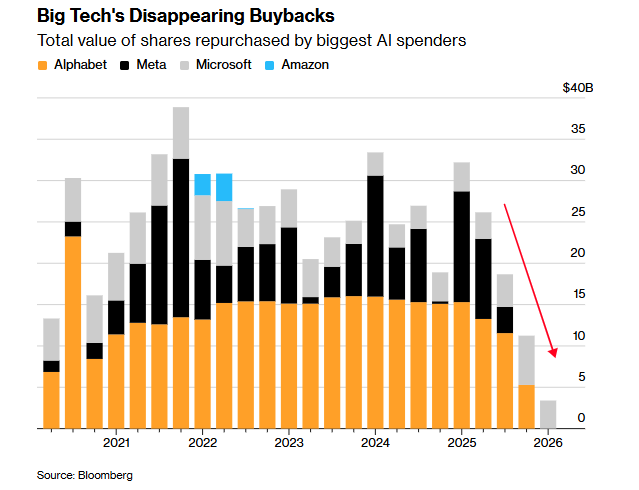

2. Mag 7 Buybacks Disappear

Bloomberg

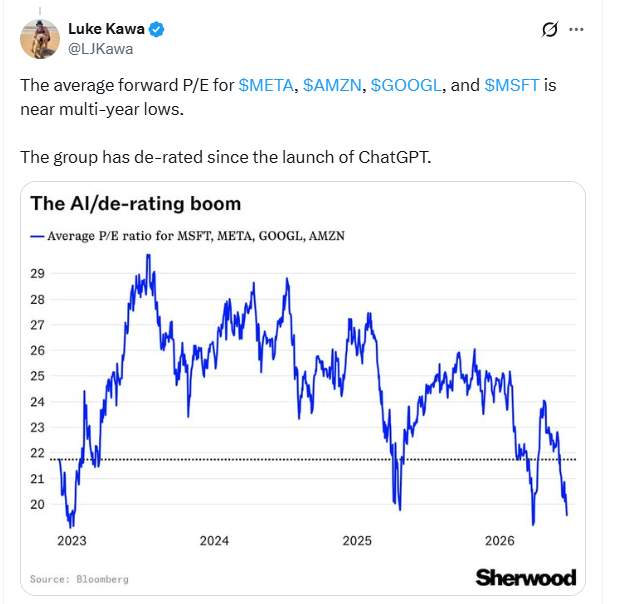

3. Average P/E Ratios Plummeting for Some of Mag 7

Luke Kawa

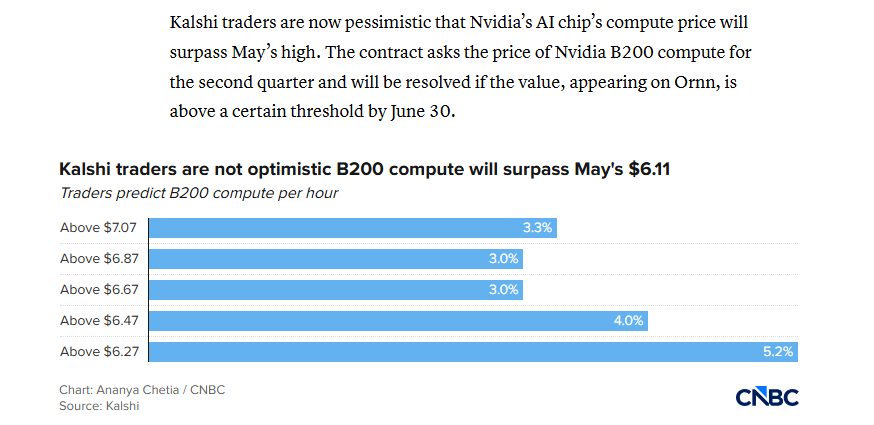

4. Kalshi Traders Betting Against NVDA Chip Prices-CNBC

CNBC

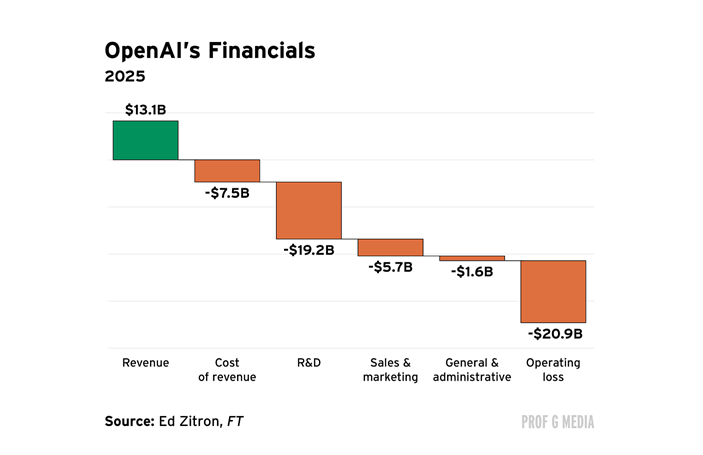

5. Open AI’s Financials $21B Operating Losses-Ed Elson

Prof G Media

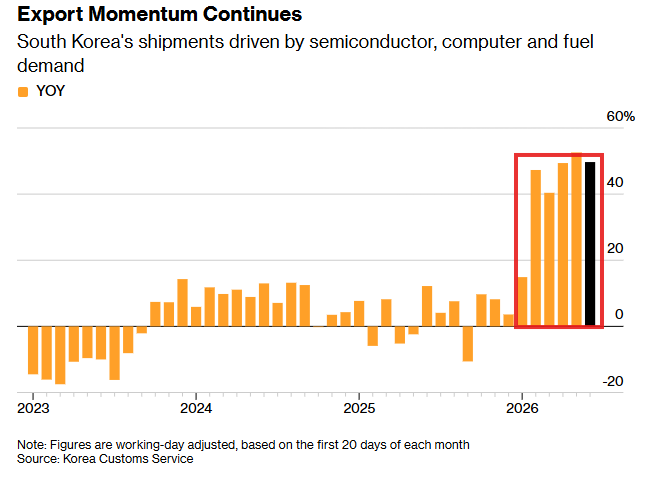

6. Semi Shipments from S.Korea Momentum Continues

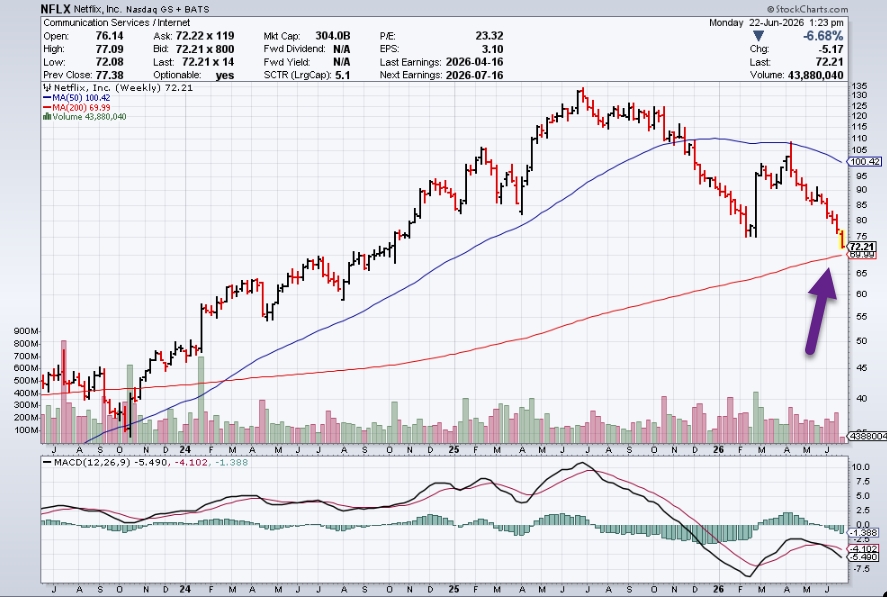

7. NFLX Closing in on -50% from Highs….Right at 200 Week Moving Average

StockCharts

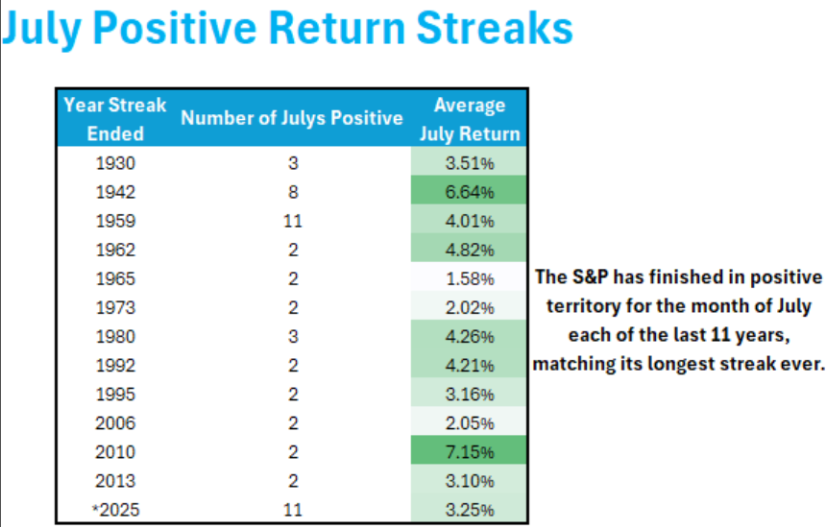

8. July Positive S&P Returns for 11 Years in a Row

NASDAQ DORSEY WRIGHT

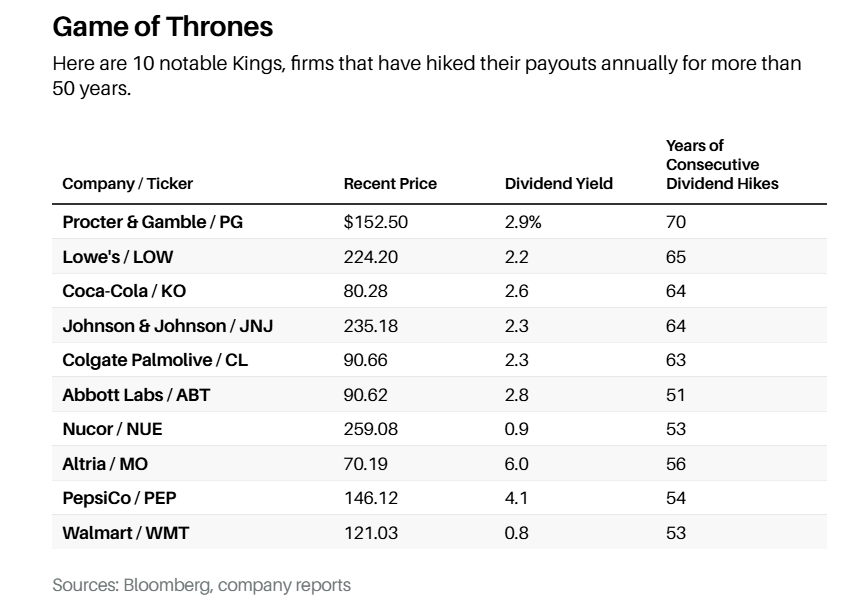

9. Dividend Kings-Companies Raising Dividends 50 Years in a Row

Barrons By Andrew Bary What the Kings lack are technology companies—not surprising since most big tech firms are less than 50 years old.That has contributed to an underperformance for the group since 2014, with the Kings returning 8.7% annually against nearly 14% for the S&P 500 index through the end of 2025. The big gap has opened up in the past few years during the tech-led bull run.

‘These are defensive stocks,” says Brian Bollinger, president of Simply Safe Dividends. ‘They’re 30% less volatile on average than the S&P 500.” The group has produced average annual dividend increases of 5% over the past 10 years.

Barron’s

10. SpaceX turns to bond market to raise capital, reports $100.8 billion cash

SpaceX employees cross the road as they go to work at the SpaceX facility in Hawthorne on the day of their company’s IPO, in Hawthorne, California, U.S. June 12, 2026. REUTERS/Mike Blake Purchase Licensing Rights, opens new tab

June 22 (Reuters) – Elon Musk’s SpaceX (SPCX.O), opens new tab turned to the bond market for the first time, capitalizing on a post-IPO momentum that has vaulted its cash reserves past $100 billion as the rockets-to-AI group ramps up spending.

Monday’s notes offering comes mere days after SpaceX’s IPO, signaling the company’s push to reshape its balance sheet by replacing short-term bridge financing with longer-dated debt, which can help it fund an ambitious and costly expansion into AI and next-generation rockets.

Its shares slid 9% in morning trading, falling for the third consecutive trading session.

SpaceX listed on the Nasdaq on June 12 after raising $85.7 billion from its initial public offering, making it one of the world’s most valuable companies.

Musk holds 82% of SpaceX’s voting power after the IPO.

“With Musk maintaining supermajority voting control through a dual-class structure, issuing bonds keeps economic ownership intact for existing shareholders without new share issuance,” said Adam Sarhan, chief executive of 50 Park Investments.

“This debt choice over additional equity clearly prioritizes avoiding further shareholder dilution.”

SpaceX has increased spending on AI infrastructure and the development of its next-generation Starship rocket, investments that have weighed on profitability despite strong growth at its Starlink satellite internet business.

Revenue rose 33% to $18.67 billion last year, though it reported a net loss after heavy spending and the integration of Musk’s artificial intelligence venture, xAI.

The company did not disclose the size or pricing terms of the proposed notes offering. The proceeds will be used for general corporate purposes as well as to repay borrowings under its bridge loan facility and cover related fees and expenses, it said.

SpaceX held $15.9 billion in cash and cash equivalents at the end of March, according to its IPO filing.

Separately, SpaceX signed a deal with Reflection AI to provide additional computing capacity to the startup at Musk’s Colossus 2 data center, Reflection AI said in a post on LinkedIn.

The agreement is worth up to $6.3 billion, CNBC reported earlier on Monday.

Credit rating agencies assigned the company investment-grade ratings last week, signaling confidence in SpaceX’s financial stability as it moves forward with its costly AI plans.

Moody’s issued a “Baa1” and Fitch a “BBB+” rating, indicating that SpaceX’s debt is considered investment-grade and carries moderate credit risk, with sufficient capacity to meet its financial commitments.

Reporting by Harshita Mary Varghese in Bengaluru; Editing by Pooja Desai