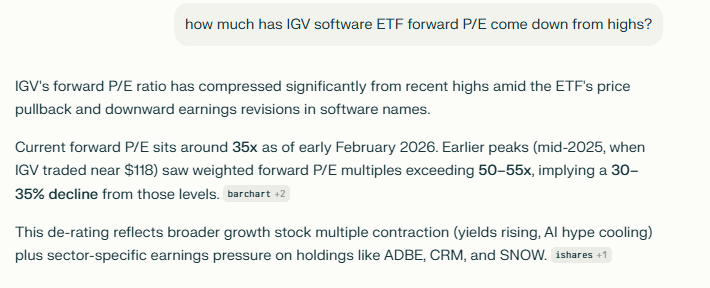

3. Software Forward PE Drop ….Forward P/E of Software ETF 55x to 35x

Perplexity

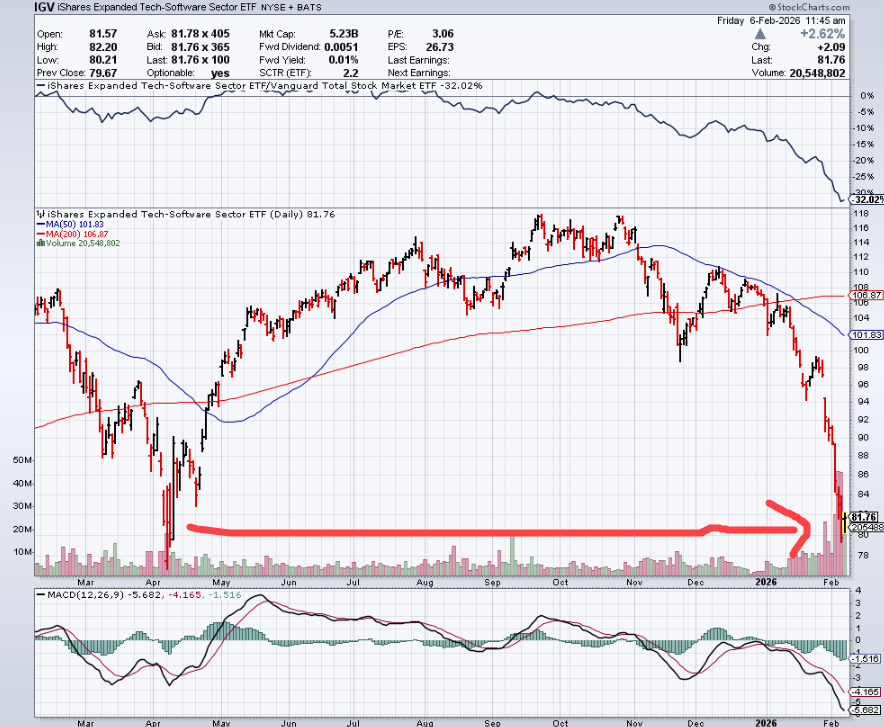

4. IGV Software ETF Right on Liberation Day Lows

StockCharts

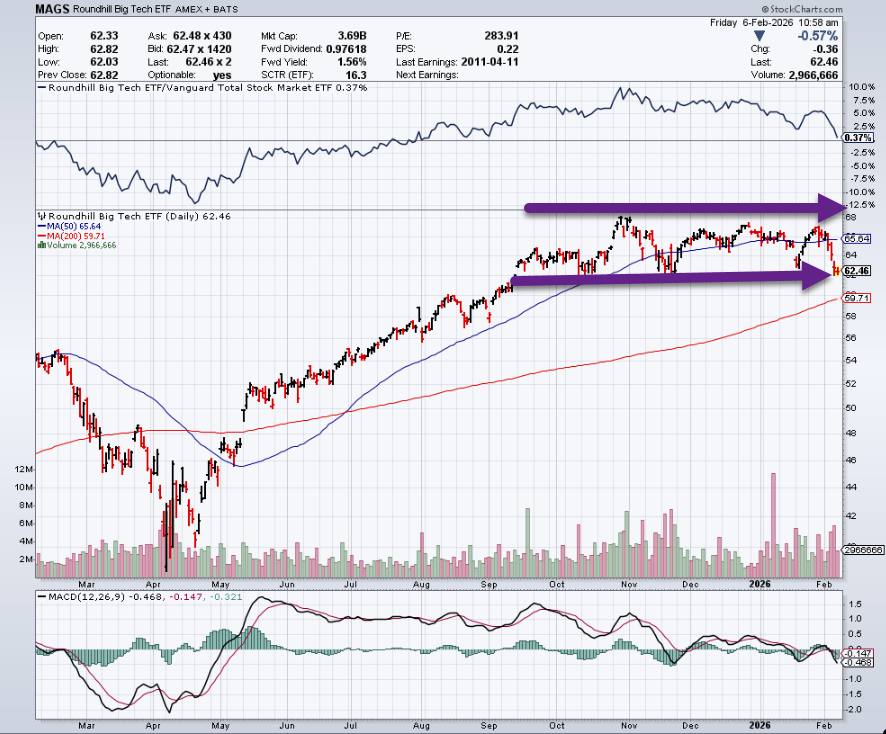

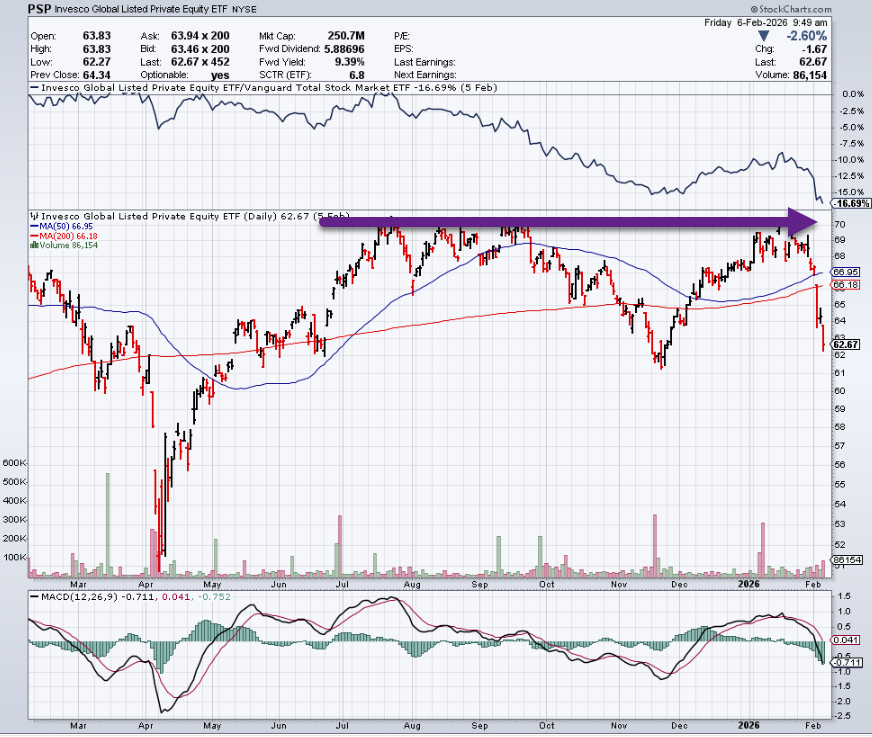

5. Private Equity ETF PSP Failed 4x at New Highs

StockCharts

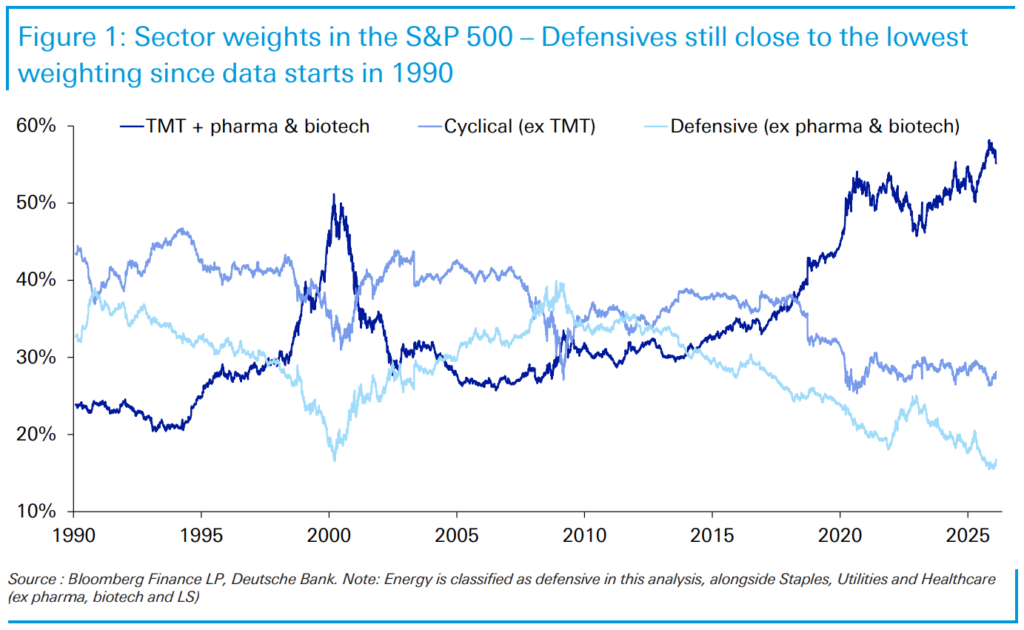

6. Defensives Still Close to Lowest Weighting in S&P 500 Since 1990

After a fascinating week in markets, today’s CoTD —updated from last week’s pack (link here)—shows that US defensive stocks remain close to the “cheapest” levels we’ve seen since our dataset begins in 1990. In other words, even with the recent rotation out of tech, the broader picture still shows limited impact when you zoom out.

For more colour on positioning and flows behind the recent equity move, see Parag Thatte’s latest weekly report (link here). Two themes stand out:

Tech bounced on Friday from the bottom of its 10-year relative channel versus the S&P 500. Notably, it was sitting at the top of that channel back in October when the rotation began.

The rotation away from tech began around the time Q3 earnings revealed a broadening of earnings growth—from a narrow set of sectors (mainly tech) to most sectors.

This second point is particularly interesting: improving earnings elsewhere may have helped create the conditions for the tech sell-off just as much as anything happening within tech itself. And while tech still shows the strongest earnings growth, today’s chart suggests that as other sectors improve, relative valuations become compelling enough for investors to reallocate.

Deutsche Bank

7. Murder Rate Per 100,000 People

Semafor

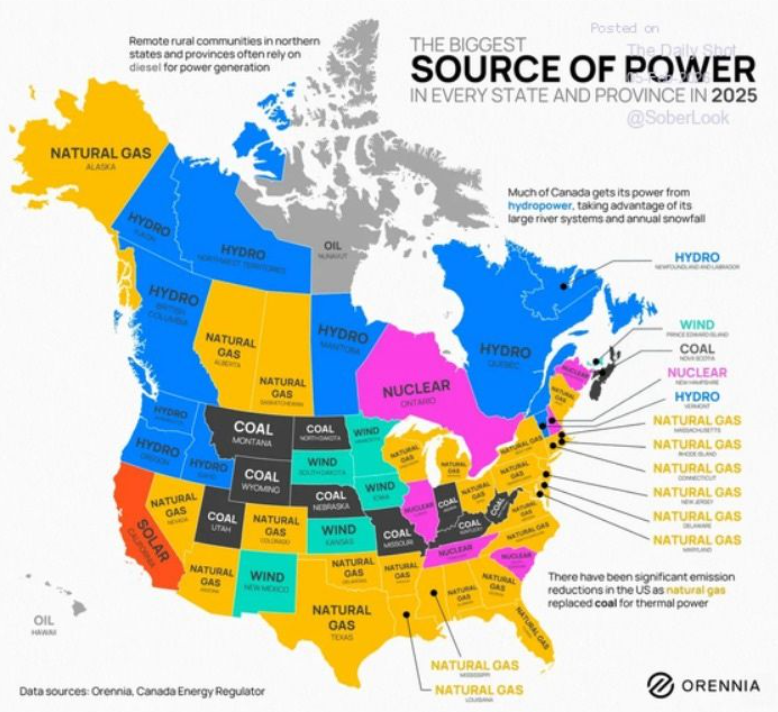

8. Source of Power by State 2025

Orennia

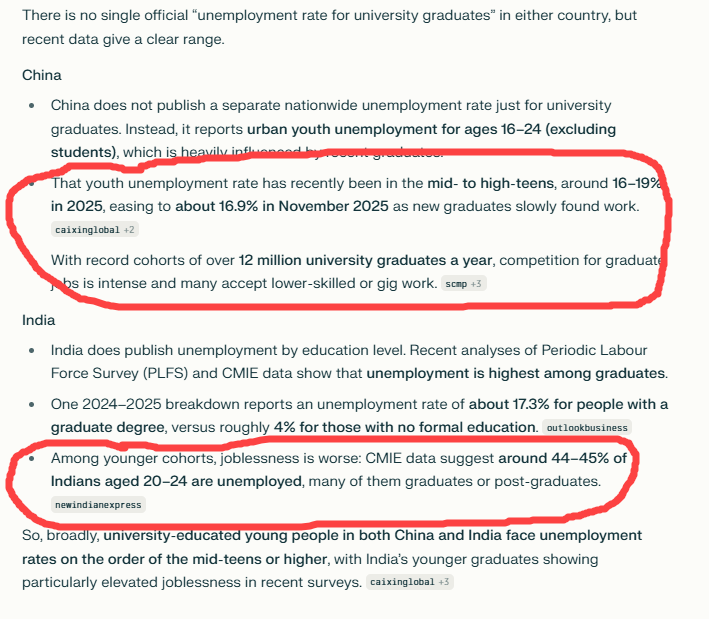

9. Unemployment Rate for College Grads in U.S. 2.5%-2.8%….Vs. China/India

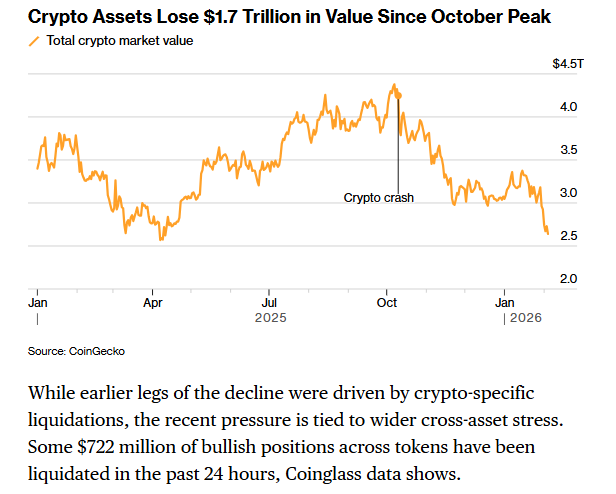

1. Crypto Assets Lose $1.7 Trillion in Value Since October

Bloomberg

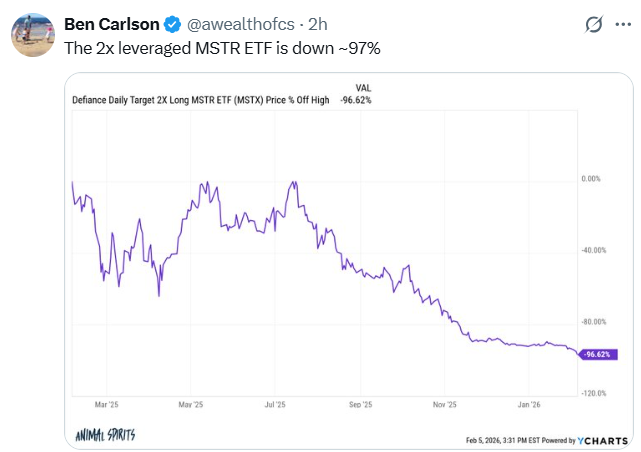

2. 2 X Leverage an Already Leveraged MSTR -97%

Ben Carlson

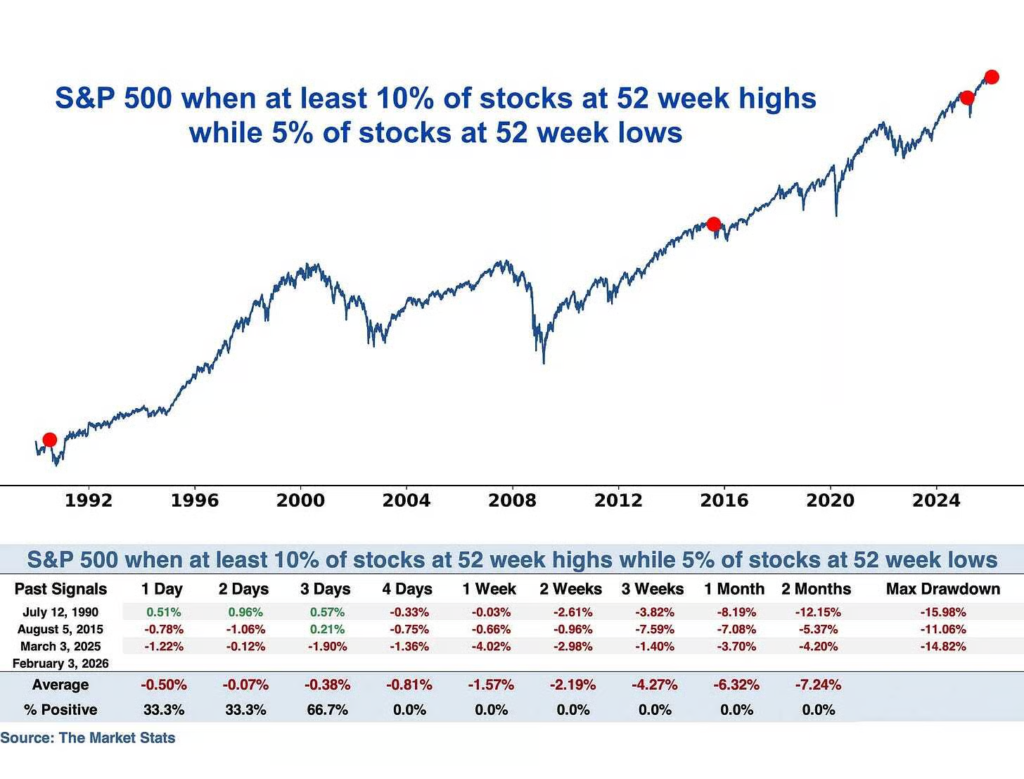

3. For Short-Term Traders

Highs vs. lows. “This is a very split market. 16% of S&P 500 stocks are at 52 week highs while 5% are at 52 week lows. This only happened 3 other times: July 1990, August 2015, March 2025. Each were followed by at least a -10% $SPX correction in the next 2 months”.

Rituals — repeated, meaningful routines — give the brain structure when life feels uncertain.

Their predictability can calm stress, reduce mental load, and improve social interactions.

You can design small, personal rituals to actively program your brain for resilience, clarity, and connection.

A few years ago, during a particularly chaotic period at work, I started making my morning coffee the exact same way every day: same mug, same timing, same two minutes of silence while it brewed.

It wasn’t intentional; I was just too overwhelmed to think about it. But something interesting happened: Those two minutes became the calmest part of my day. Even when everything else felt out of control, I had this one predictable moment that somehow made the rest manageable.

I had just experienced the power of rituals completely by accident, and it wasn’t until I left tech to study neuroscience that I understood why that simple coffee routine had been so effective.

Rituals are some of the most powerful technologies invented by humankind.

Most people think of rituals as elaborate religious ceremonies or ancient traditions. But your life is actually filled with them.

Waiting for everyone to be served before eating, giving presents for birthdays and holidays, saying “hello” and exchanging scripted pleasantries, clapping at the end of a performance — all of these are rituals woven throughout our days.

Since the dawn of time, humans have used rituals to acknowledge one another, signal belonging, mark beginnings and endings, and more.

In fact, I believe rituals are some of the most powerful technologies invented by humankind. Think of them as repetitive, patterned, often culturally transmitted “software” that serves psychological functions that go far beyond mere habit or tradition.

The psychology and neuroscience of rituals

When people face stress, danger, or major life changes, rituals provide a sense of stability through structured actions. Having something concrete to do when everything appears uncertain reduces anxiety and feelings of helplessness.

This sense of agency extends to rituals’ broader social function: Shared routines make cooperation easier in times of stress. When a team huddles before a game, the action signals membership and commitment to the group.

Rituals also help us make sense of life’s most challenging moments. They mark transitions — such as birth, puberty, marriage, and death — and help us navigate events that feel overwhelming. They also support us as we forge a new identity through rites of passage. That’s why graduation ceremonies don’t just celebrate achievement; they help transform a person’s identity from “student” to “graduate.”

Lastly, rituals transmit culture across generations. Children learn gratitude from family dinner traditions, not from lectures about being thankful. Repeatedly doing something together works better than just talking about it.

Rituals are like a software upgrade for your nervous system. They affect your brain and body in three specific ways:

Calm. Rituals help quiet the brain’s threat-detection system, especially the amygdala. When that system calms down, we feel more grounded. This is one reason repeating familiar sequences of actions helps during chaotic transitions.

Clarity. Predictable steps activate parts of the prefrontal cortex involved in planning, which reduces mental load as your brain doesn’t have to constantly decide what comes next. This makes challenging tasks feel more manageable, especially under stress.

Connection. When people move or speak in sync, the brain releases bonding chemicals, such as oxytocin and endogenous opioids. These make social interactions feel warmer and more trusting. That’s why shared rituals create a sense of “us.”

Most rituals are inherited from the culture around us — we simply adopt what we see others doing. But here’s the part I find most exciting: You don’t have to copy-paste rituals from others. You can consciously design rituals that serve your specific needs.

How to design your own rituals

Creating personal rituals that serve your specific needs only takes a bit of observation, experimentation, and reflection.

Start with observation. Notice the moments in your day when you feel scattered, stressed, or disconnected. These transition points are perfect opportunities for designing a new ritual.

Next, experiment. Pick one specific moment in your day and try a simple ritual. Maybe it’s making your morning coffee the same way each day, arranging your desk before work, or taking three deep breaths before important meetings. The key is choosing something small enough to stick with yet meaningful enough to feel intentional.

Finally, reflect and adjust. After a week or two, ask yourself: Does this ritual actually help? Does it feel natural or forced? Pretend to be a scientist and answer these questions from a place of curiosity. Tweak as needed.

The most effective personal rituals are simple enough to remember, specific enough to feel meaningful, and flexible enough to adapt to different circumstances. Start small with one daily ritual, then gradually expand your toolkit.

These repeated patterns of action will help you actively program your brain for resilience, clarity, and connection. Use them before exams, competitions, or challenging conversations. Keep experimenting and adapting them as you and your circumstances change.

Your brain is already wired to respond to rituals — you just need to give it the right patterns to follow.

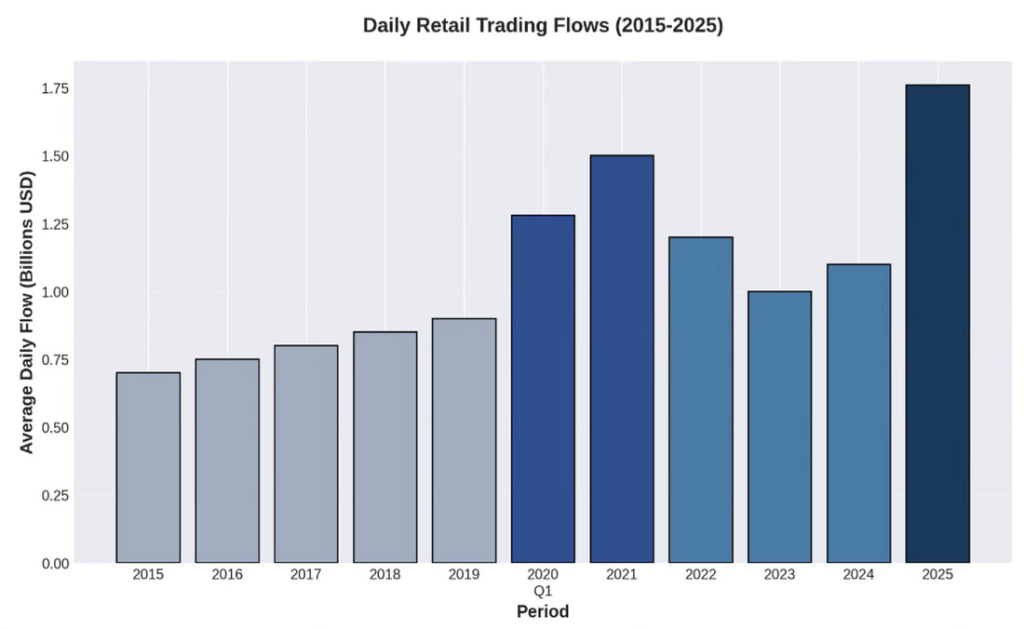

1. Retail Investor Flow Jumped 60% from 2024 to 2025

Retail Flows Hit Record Highs

Here’s the part that should make Wall Street nervous: retail isn’t just maintaining presence, it’s accelerating. JPMorgan data shows that retail flows in 2025 jumped 60% from 2024 levels and are running 17% higher than the 2021 meme stock peak.

Retail investors are now over 20% of the total U.S. trading volume. Retail has now become a bigger force in the market than institutional long only and hedge funds.

Daily Chartbook

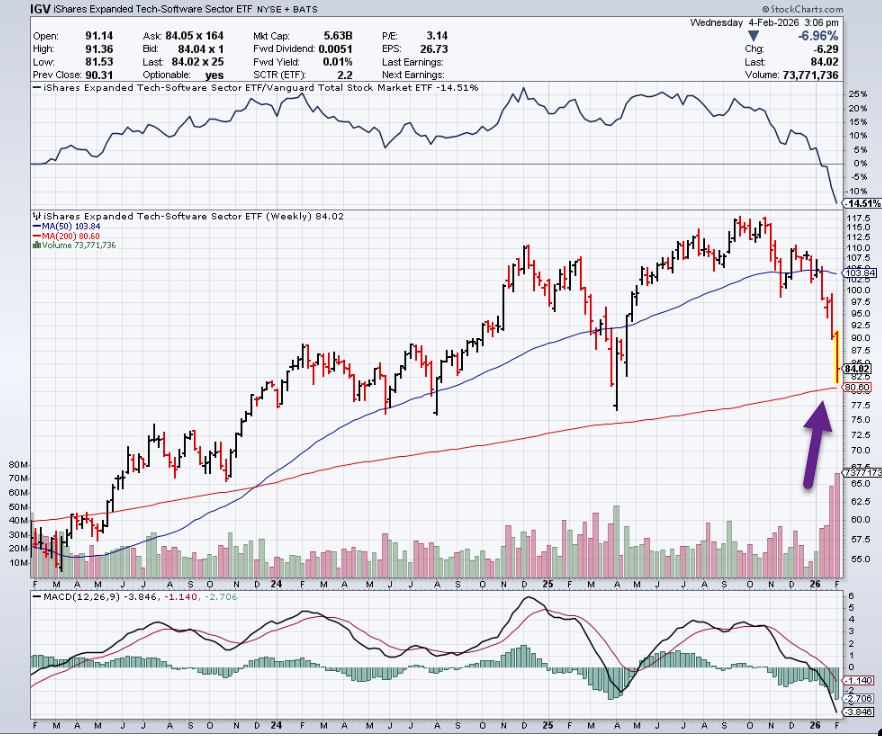

2. IGV Software ETF -30% from Highs ….Right on 200-Week Moving Average

StockCharts

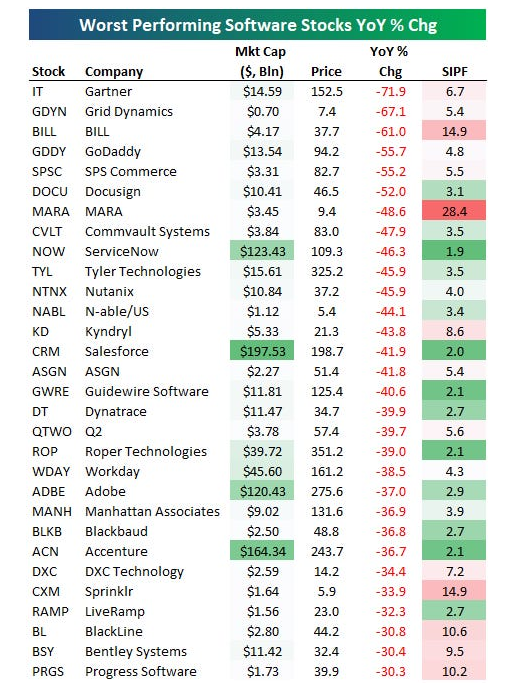

3. Worst Performing Software Stocks-Bespoke

Bespoke’s

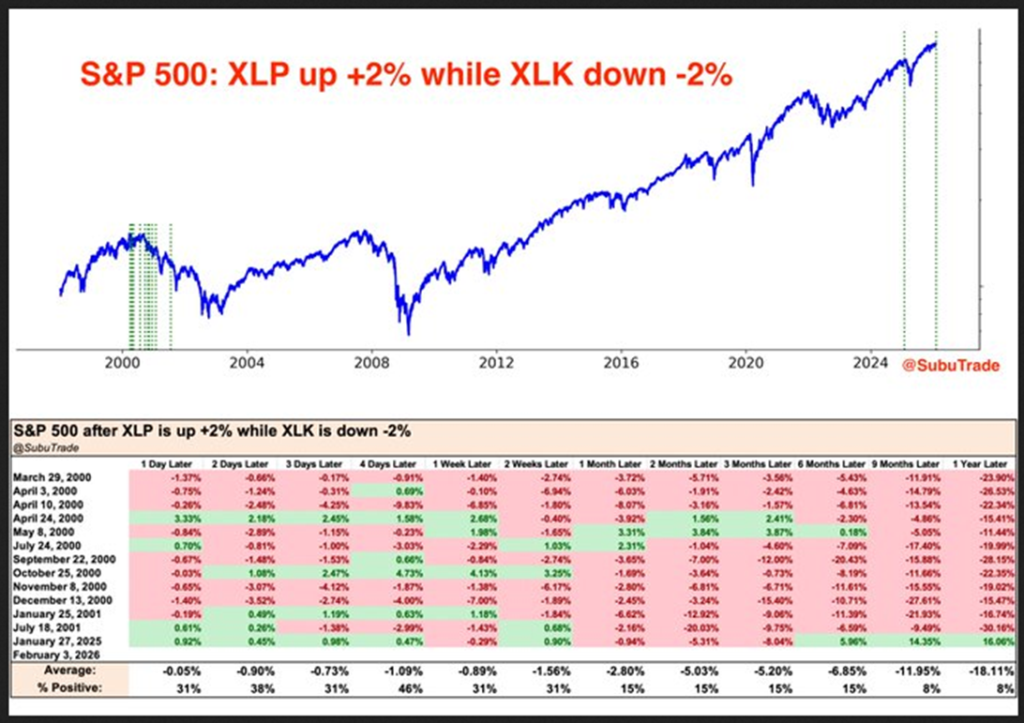

4. History of Consumer Staple Rally vs. Tech

“Due to the AI disruption fear in Service Businesses, Legal tools, Consulting and Advertising -we are seeing rotation into Consumer Staples and Cyclicals that are less threatened by AI” Noted JonesTrading’s Mike O’Rourke. Yesterday the Defensive sector XLP was up +2%, while tech sector XLK was down -2% – “This only happened in 2000-2001 dot-com bust & January 2025 (before Trump tariffs crash)” noted Twits.

5. $227 Million Out of Bitcoin ETFS….IBIT Breaks Below April 2025 Levels

WSJ-$227 Million in Net Withdraws from Bitcoin ETFs Ending Jan 28Th

1. January Close Gives Us Good Probability for 2026

Ryan Detrick

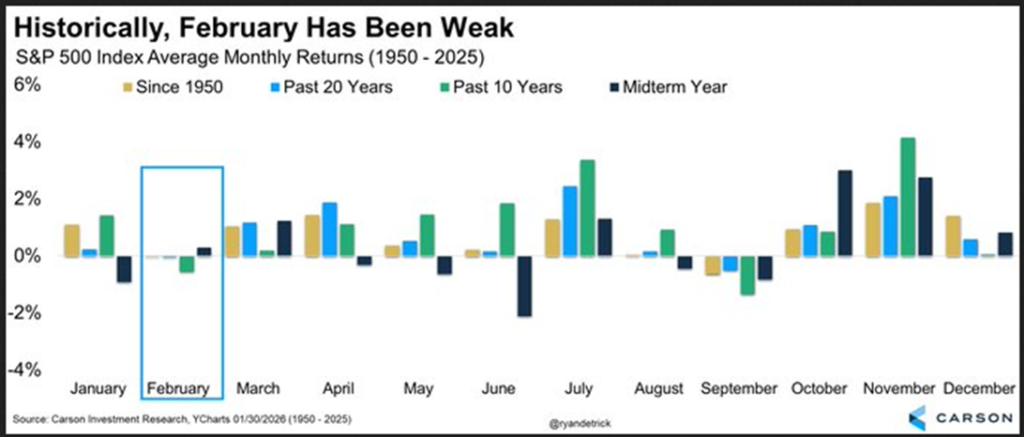

2. Historically February Has Been Weak Month

Dave Lutz at Jones Trading February is one of two months (September being the other) that is negative on average since 1950, the past 10 years, and the past 20 years.

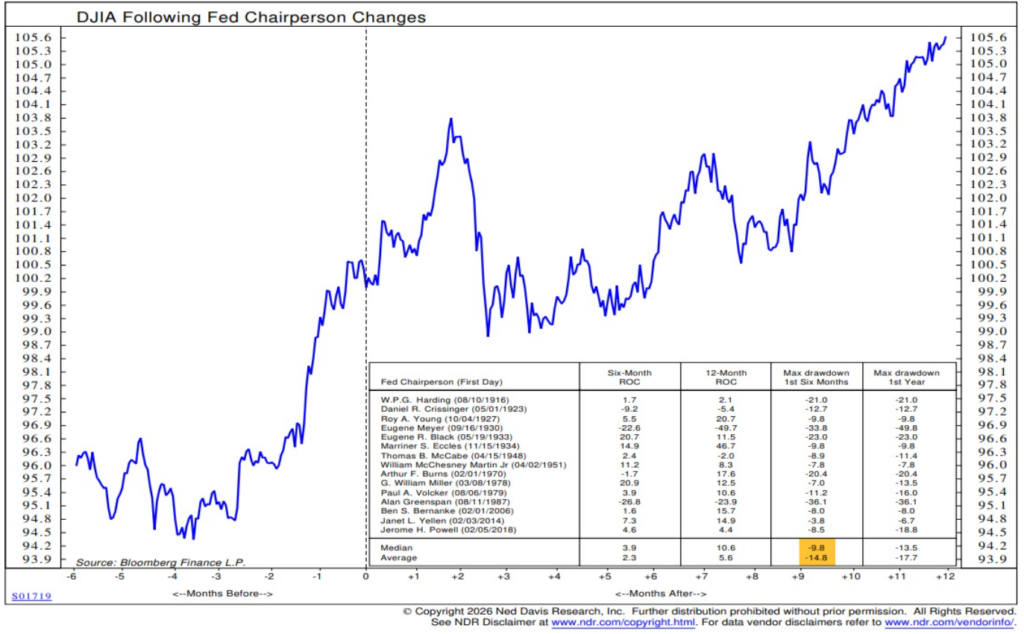

3. Change in Fed Chair Has Historic Short-Term Volatility

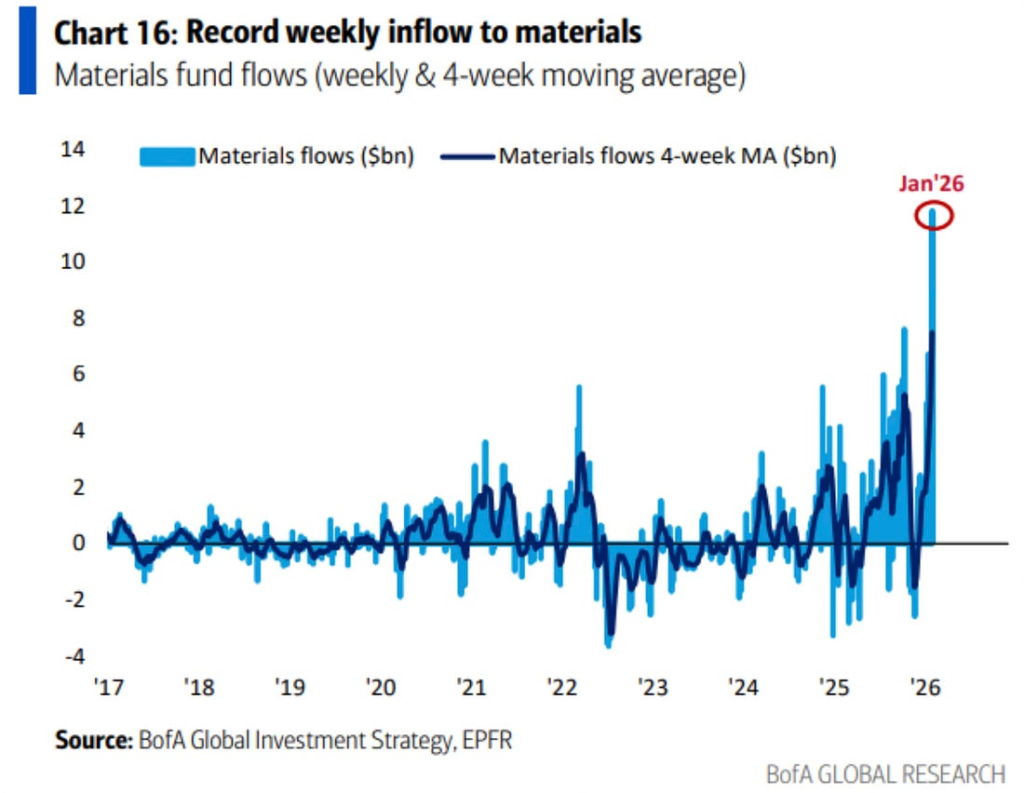

4. Material Stocks Massive Inflows to Start 2026-10x Past Years

Mike Zaccardi

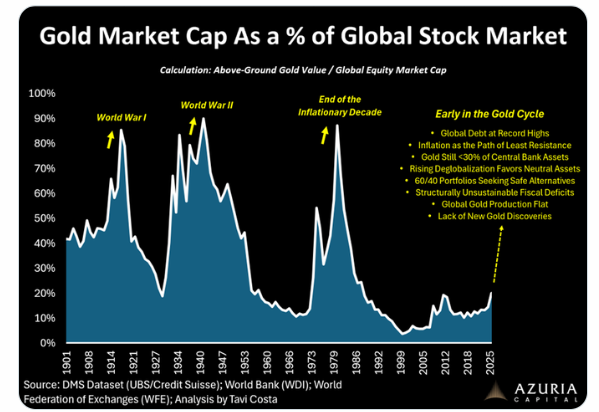

5. Gold Market Cap vs. Global Stock Market Still Low

Tavi Costa

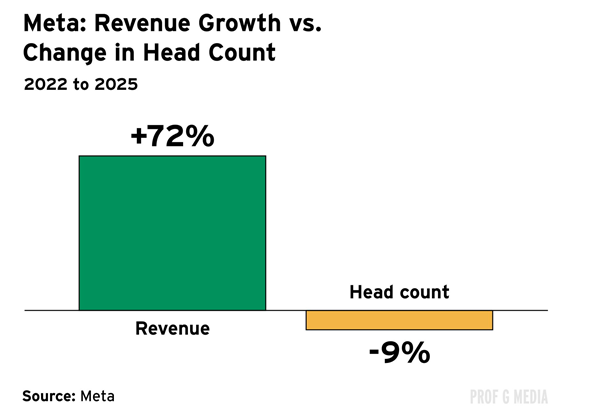

6. AI Productivity Boost Just Kicking in for Companies??? Prof G Market Letter

PROF G MEDIA

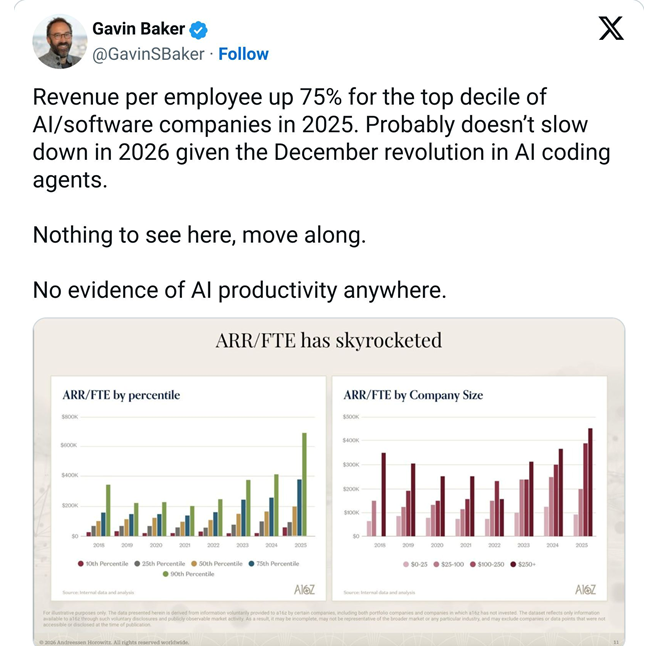

7. Revenue Per Employee on the Upswing

Gavin Baker

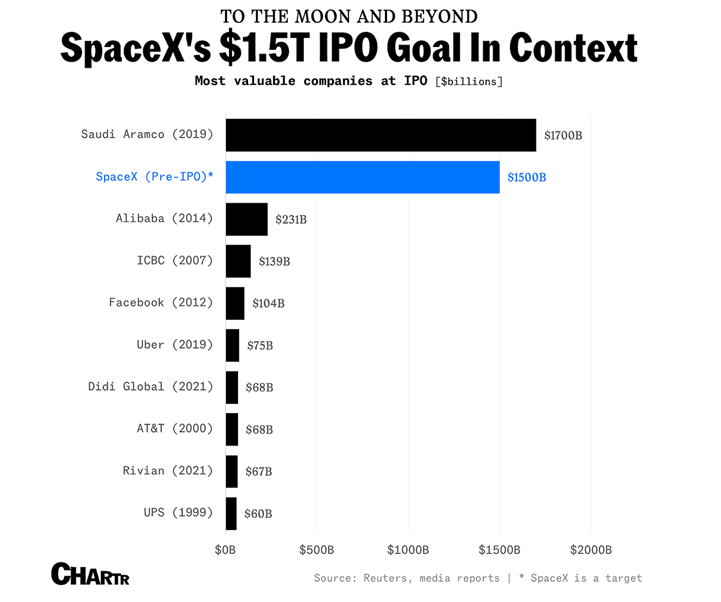

8. Space X IPO $1.5T

chartr

9. Greenland 1.5m Metric Tons of Rare Earths

Visual Capitalist

10. Ray Kroc -He Opened McDonalds at 52 Years Old

Brain Food Shane Parish

Ray Kroc turned McDonald’s from a single roadside restaurant into a system built to scale.

At 52, after decades of selling paper cups and milkshake machines, he opened “the first McDonald’s” in 1955 and helped grow it to nearly 8,000 restaurants worldwide.

Here’s the story of McDonald’s

Some Tiny Lessons from this episode:

“I was an overnight success all right. But thirty years is a long, long night.”

Do a few things. Do them perfectly.

Trust isn’t built in grand gestures. It’s built when you could take the last slice and don’t.

What you refuse to do matters more than what you do.

Dreams are only wasted if they’re not linked to action.