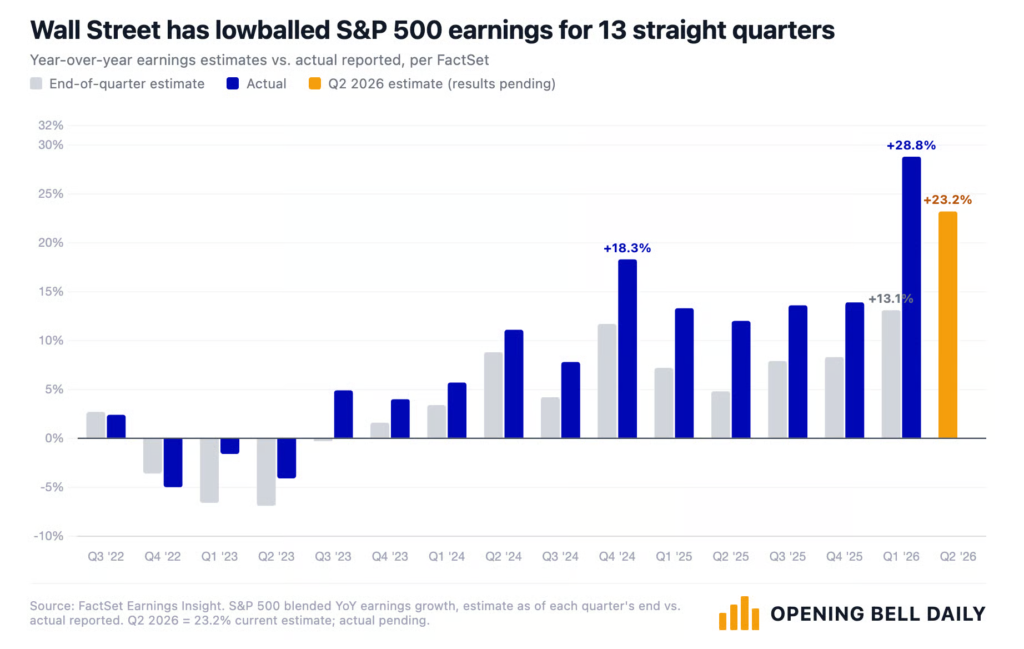

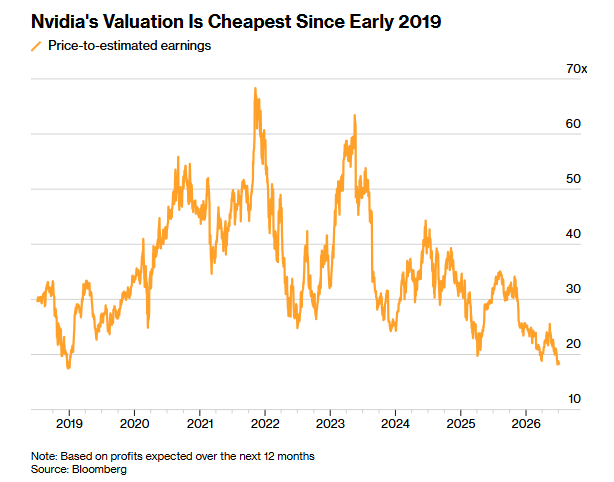

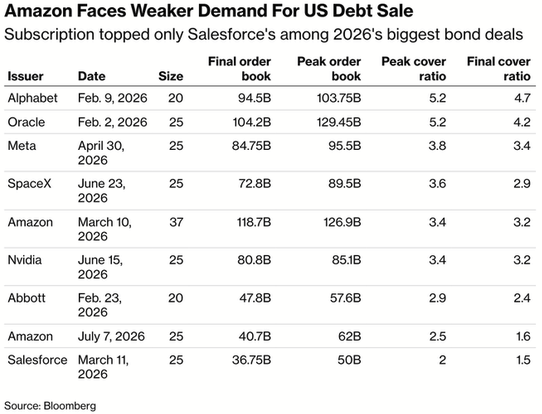

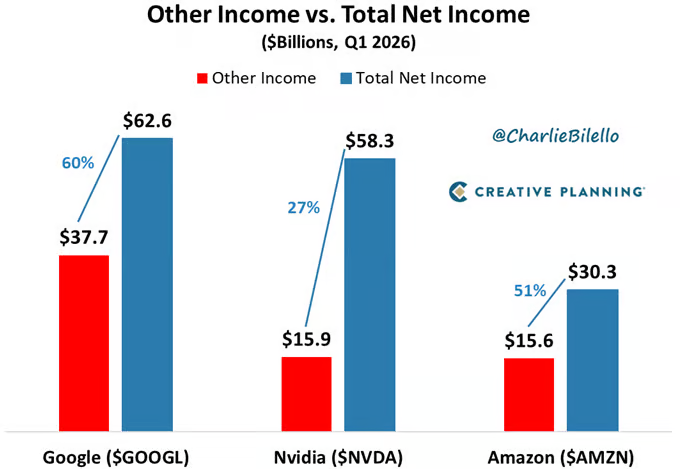

1. Year Over Year S&P Earnings Growth Skewed by “Other Income”

@Charlie Bilello In the first quarter, just 3 companies (Google, Nvidia, and Amazon) saw massive gains in the “other income” category from their private investments in companies like SpaceX and Anthropic. The total of $69 billion in “other income” was roughly 10% of the S&P 500’s overall net income for the quarter. Absent this boost, S&P 500 YoY earnings growth would have been 15% in Q1, well below the reported figure (+28%).

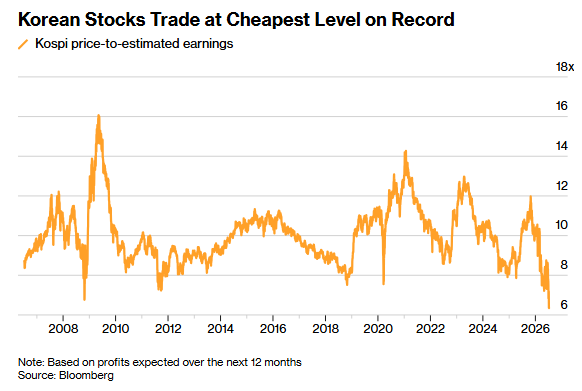

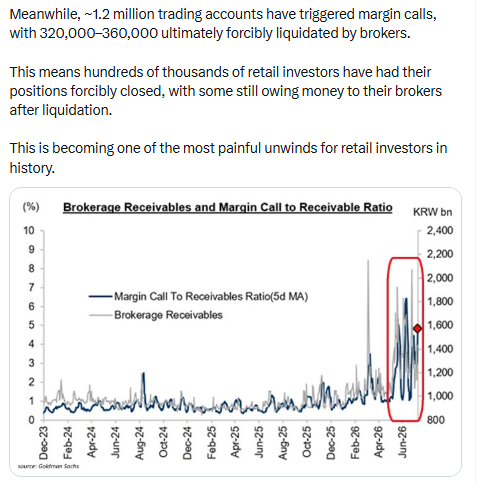

2. Leverage Play in S.Korea Blowing Up…350k Accounts Liquidated by Brokers Due to Margin Calls

Global Markets Investor

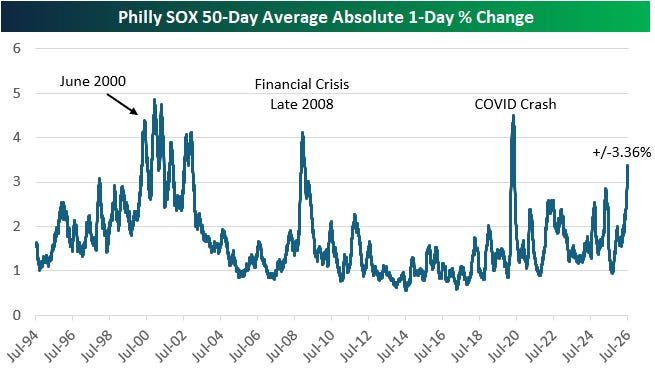

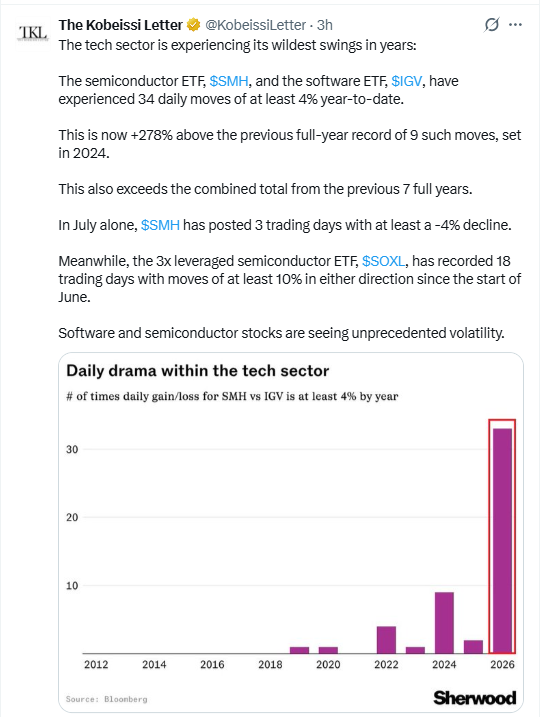

3. Tech Sector Volatility at Records While VIX Sitting at 16

The Kobeissi Letter

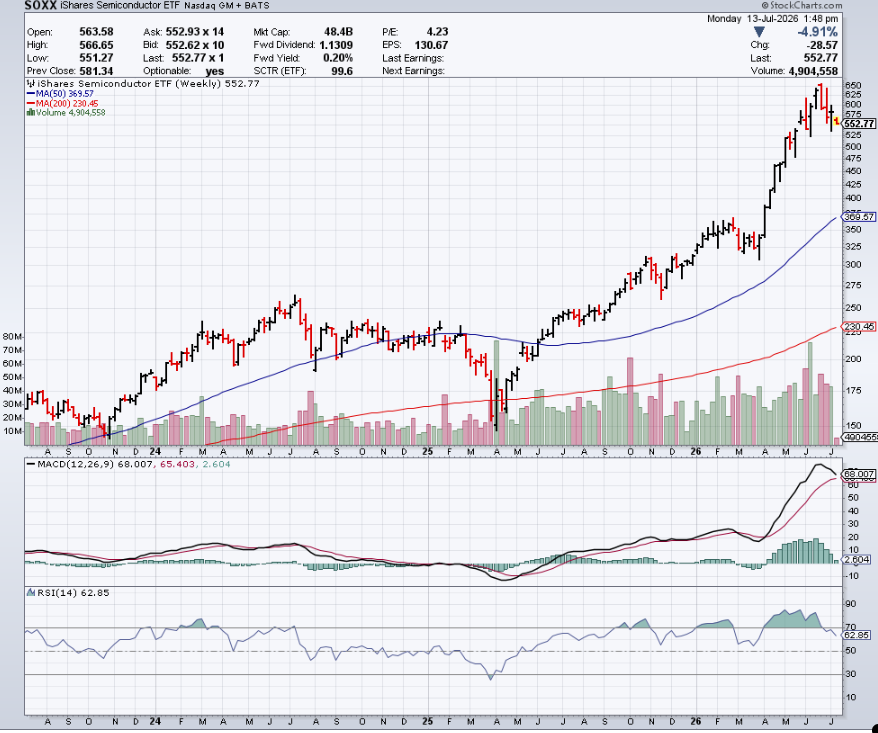

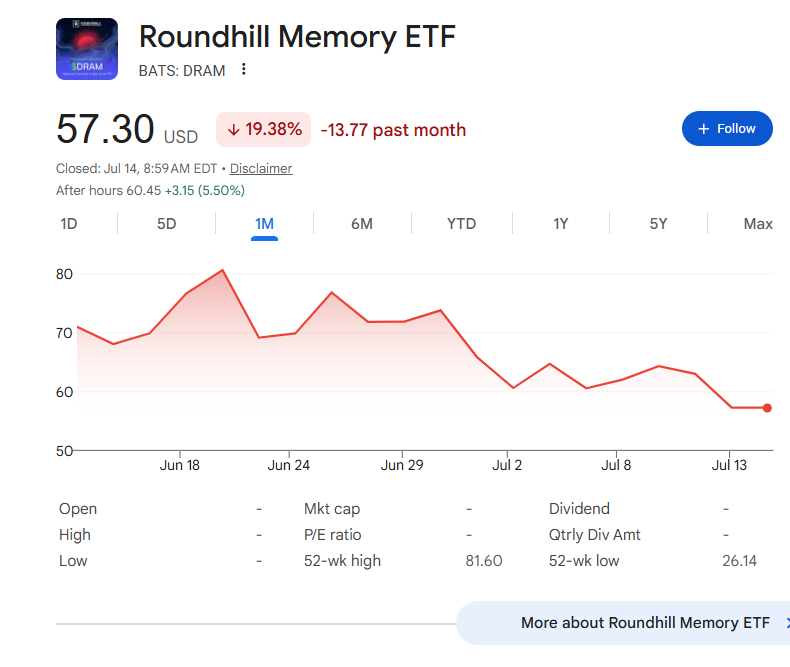

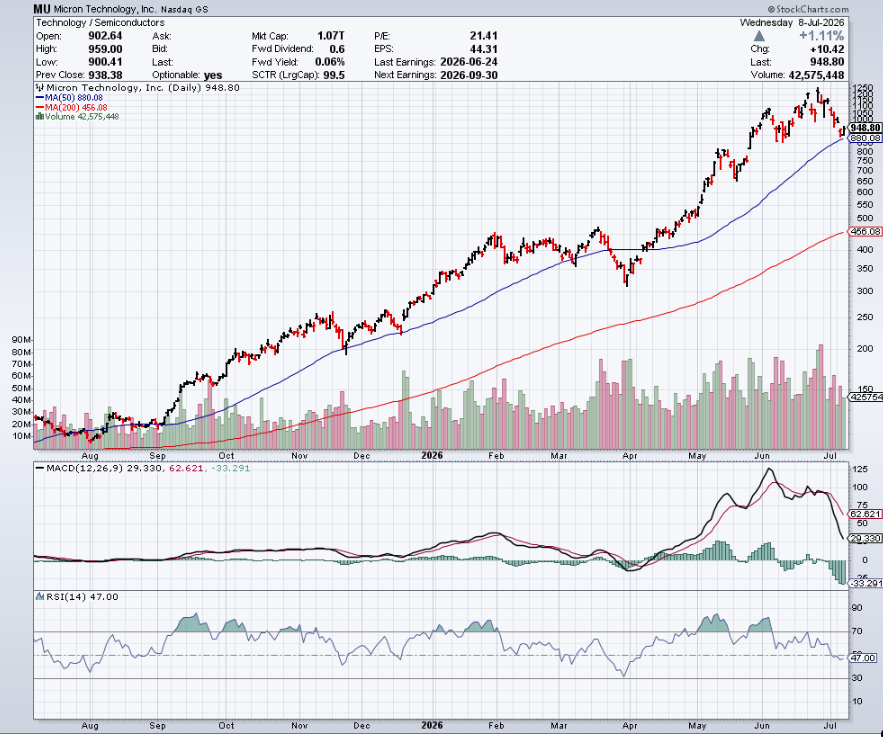

4. Semis and DRAM Record Volatility….Overall VIX Trending Down

StockCharts

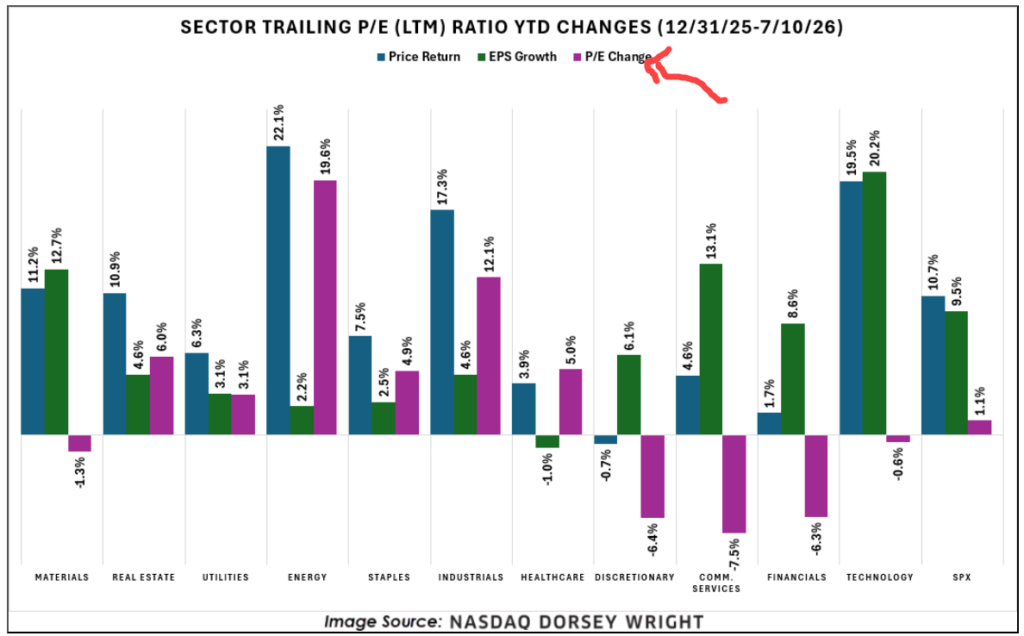

5. S&P Sector Changes in P/E Ratio….5 Sectors P/E Ratios Lower in 2026

NASDAQ DORSEY WRIGHT

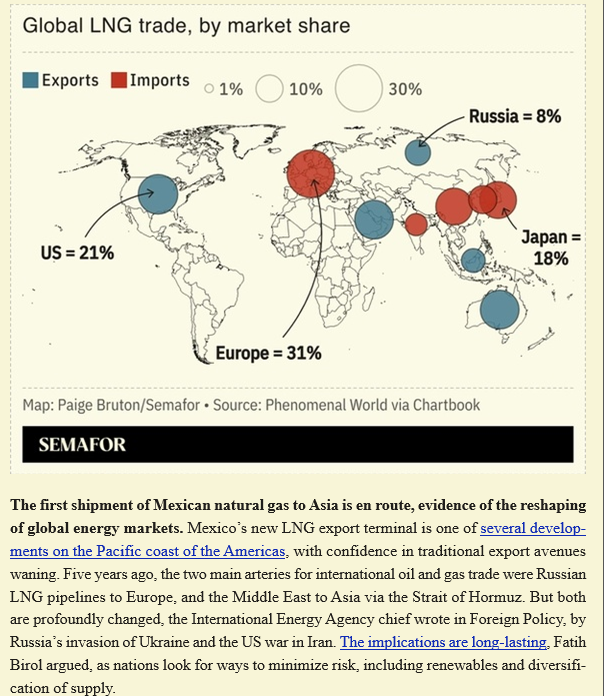

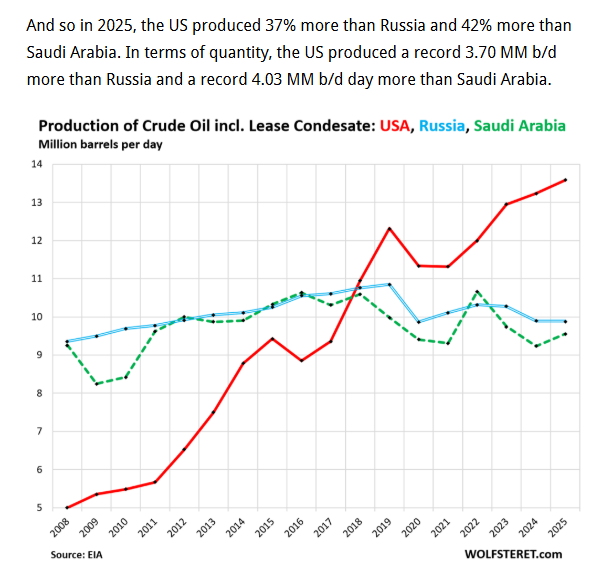

6. USA Oil– Out Producing Russia and Saudis

Wolf Street.

Wolf Street

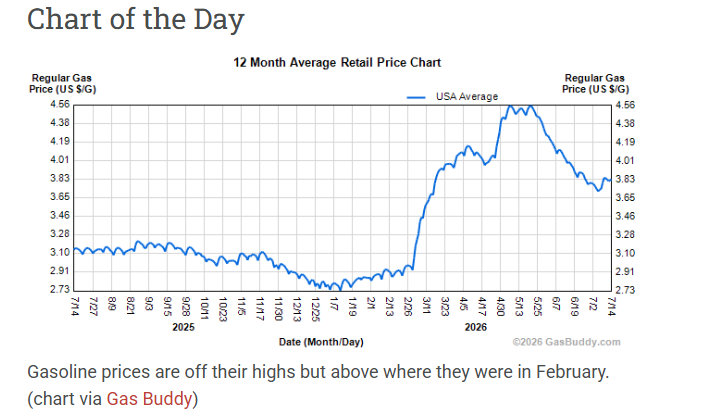

7. Retail Gas Prices—Now We Need the Next Drop to 2025 Levels

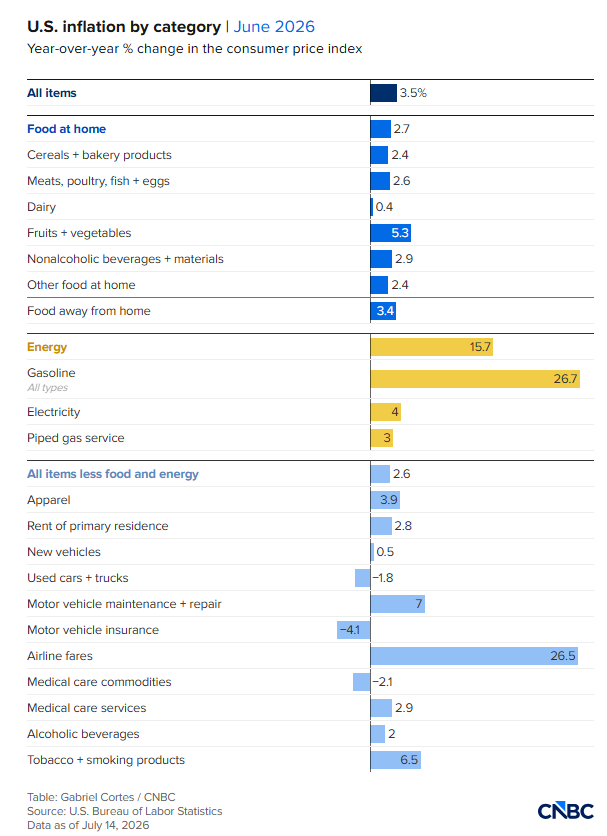

8. CPI Breakdown-CNBC

CNBC

9. 10-Year Small Down Tick Post CPI

CNBC

10. 3 Top Tier Emotionally Intelligent Tendencies

Psychology Today EI is the “it” factor and doing 3 things means you have it. Erin Leonard Ph.D.

Key points

- Emotional intelligence is the “it” factor.

- There are three high level EI tendencies that signify you have it.

- Although you may not enact these tendencies every time, you try very hard to make them your norm.

- Respond instead of react, set boundaries in place of being passive aggressive, and embrace accountability.

Emotional intelligence is the “it” factor. EI people are secure enough to handle their own flaws and continually evolve as a result. They look in the mirror instead of outsourcing all blame, and they are not fixated on the ego-win in the moment, but rather on the deeper, meaningful, and long-term priorities. Although this description portrays them as saint-like, they are certainly not. They make mistakes like everyone else and occasionally lose their temper, but overall, they routinely do 3 things that set them apart from everyone else.

1) They respond… not react.

When confronted, they quickly reflect on what the person is saying instead of immediately lashing out defensively. Their ability to think about the other person’s perspective, while looking at themselves to evaluate the merit of the confrontation, allows them to respond rather than react. They are equipped with a greater understanding of the issue; they can decide fairly whether they are at fault or not and reply with a grounded, balanced, and wise rebuttal that is not disrespectful or destructive to the relationship.

Alternatively, someone who reacts refuses to think about their part in the issue and immediately lashes out and redirects the blame onto the person who is confronting them. They deflect any accountability and use their fervor to shut down the person who is bringing up a problem. Following the confrontation, typically a person with low emotional intelligence plays the victim and acts as though they have been bullied, or they become passive-aggressive towards the person who “dares” to bring up an issue with them. Either way, the problem is not remedied, and now there is a chasm in the relationship.

2) They are not passive-aggressive… they set a boundary.

It is not fun to have your kindness taken advantage of or exploited. It is understandable to be angry in these situations, yet an emotionally intelligent person uses this as critical data. If a person repeatedly manipulates you for their own gain and does not care how it impacts you, they may be the type to react, not respond, when you tell them how you feel, which means it may be painful and useless. Instead, the emotionally intelligent person now sees this person realistically and, despite their disappointment, recognizes the importance of setting a boundary so they are not exploited again in the future. They know that this does not require them to be cold or rude. It simply means that they will be busy the next time this person needs help with something, or instead of going out to dinner with the friend who always forgets her debit card, they will propose going on a walk instead. Basically, they think creatively about how to casually implement a boundary that protects them from being used in the future.

A person who is angry because they perceive a friend took advantage of them or the friend doesn’t give them their way, may seek to covertly make this friend pay, passive-aggressively. Unfortunately, this person typically attempts to sabotage the friend’s success by doing something sneaky or they talk nasty about them to key mutual acquaintances. This is the, “you hurt me, and I’ll hurt you worse” mentality. Yet, they are nice to your face. This passive aggressive approach signals a sizable deficit in emotional intelligence.

3) They apologize when they are wrong… not when they get caught.

Typically, an emotionally intelligent individual is self-aware. They care about how their actions and words impact others, especially the people with whom they are close. So, they are cognizant of how they interact. They wish to understand the people that they care about, so they are careful to listen attentively and honor the person’s feelings rather than making it about them and what they want and feel.

This self-awareness and motivation to be a good person in their friendships and relationships also allows them to catch their mistakes. Maybe they had a selfish moment or were too tired and stressed to authentically listen and offer empathy. Whatever it may be, they search their soul because, although the moment is over, it nags at them. They do not feel quite right about how they handled it. Because they are secure enough to handle their own flaws, they apologize to the person that they impacted. Their accountability fosters trust and closeness with the people in their lives and sustains strong attachments with people who share these relational qualities.

A person with deficits in emotional intelligence usually defends against truly knowing their own character flaws. They may not be strong enough to handle them. So, they resist looking at themselves and instead feel more secure critiquing others. The last thing they want to do is show any “weakness” in a relationship, so they refuse to look at the possibility that they did something hurtful or selfish…. Until they get caught. When their back is against the wall, and they have no choice but to apologize because they risk losing the person, they will. However, it may come with excuses, justifications, and minimizations, which may signify insincerity. Often, insincere apologies are a sign that the person will repeat the same mistake.

Emotional intelligence is a gift when you use it wisely. Responding instead of reacting, setting healthy boundaries in place of being passive-aggressive, and embracing accountability in a relationship rather than evading it are top-tier emotional intelligence tendencies. You can find more on this important topic in my book, How to Outsmart a Narcissist: Use Emotional Intelligence to Regain Control at Home, at Work, and in Life.