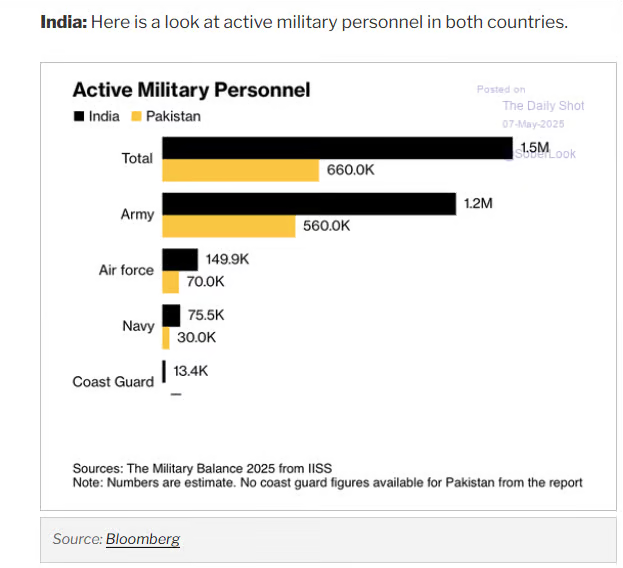

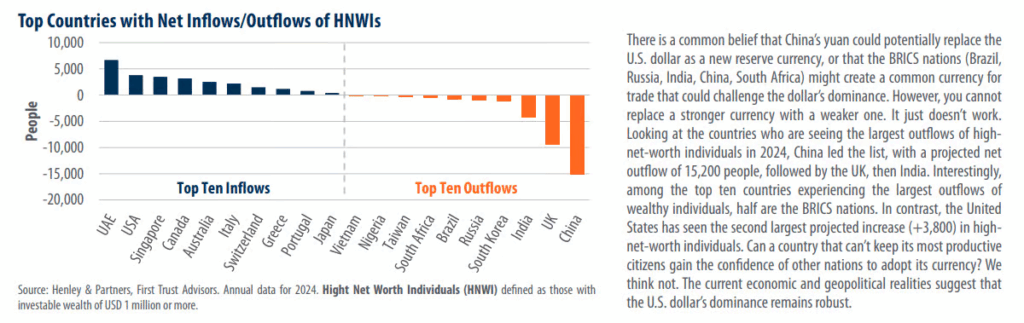

1. The Countries “Projected” to Take Over Economic Leadership vs. America are Bleeding High Net Worth Citizens—China, UK, and India

First Trust Economic Blog

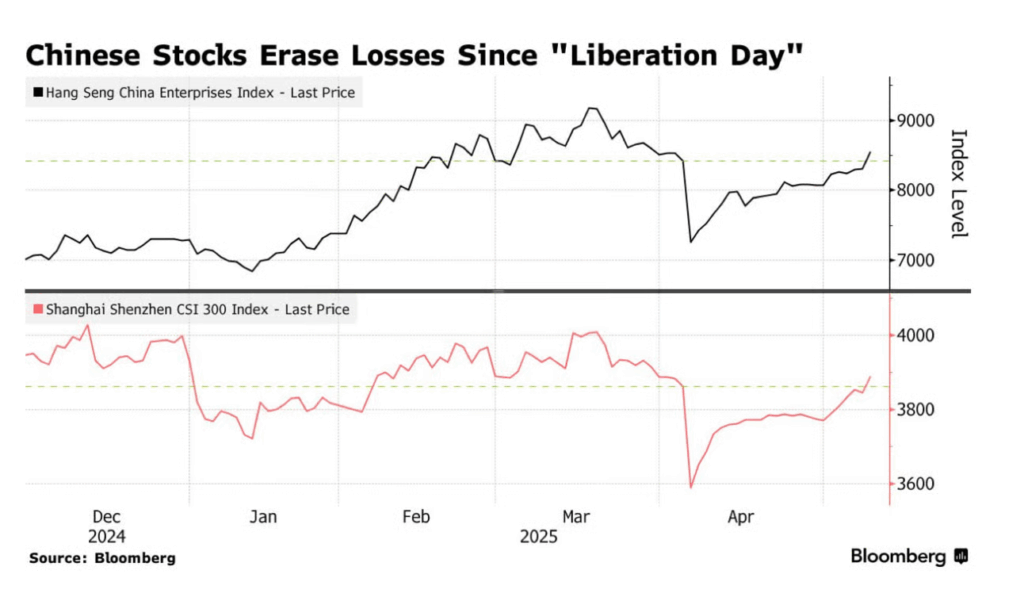

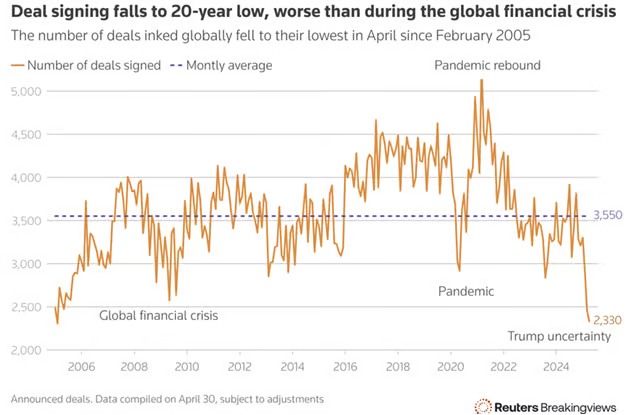

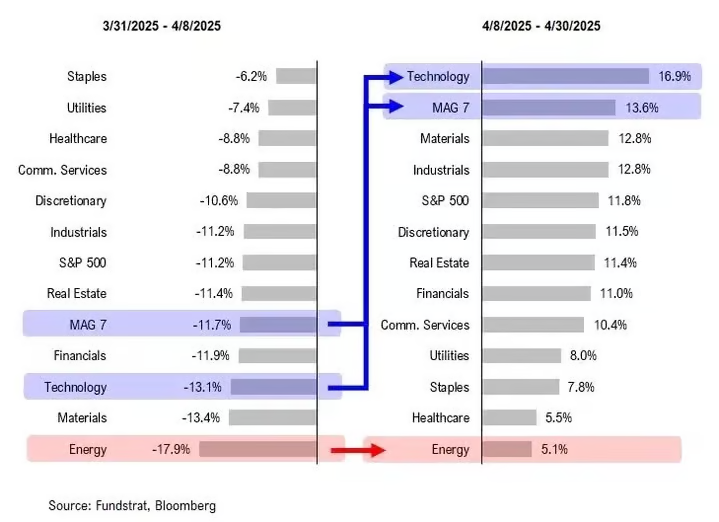

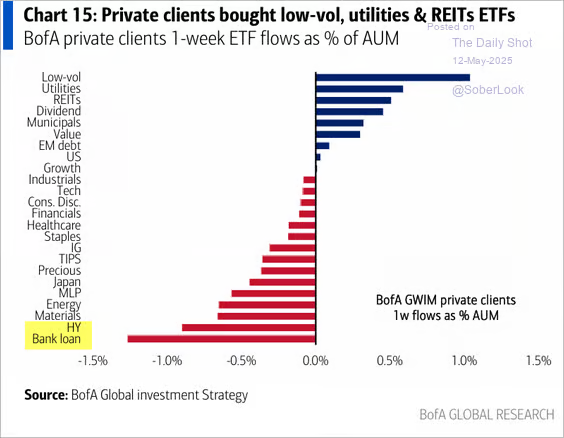

2. Investors Buying Defensive Sectors Pre-China Trade Announcement

Credit: BofA’s private clients have been exiting leveraged finance assets.

The Daily Shot

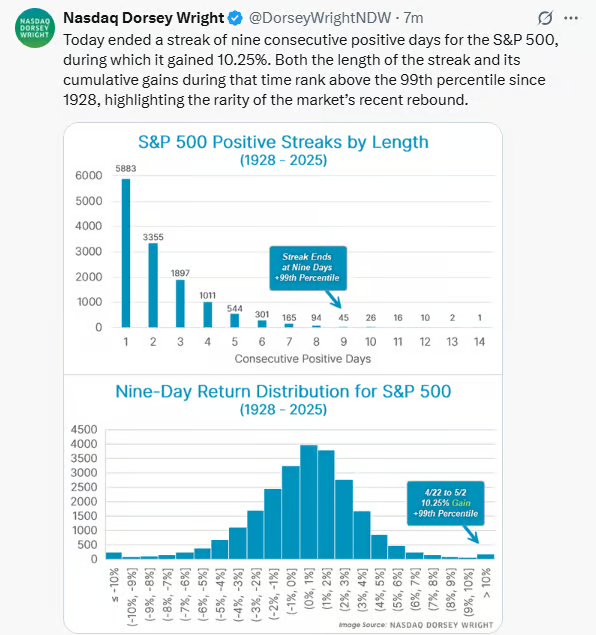

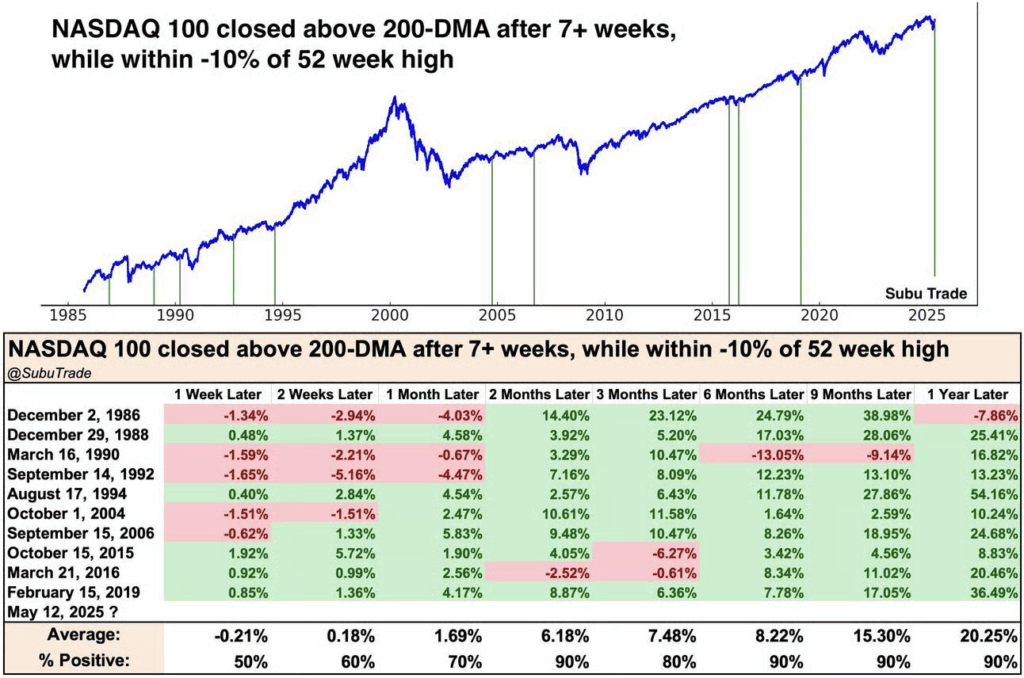

3. Investors Get Defensive but QQQ Closes Above 200-Day

Subu Trade

4. Coinbase Joins S&P 500—Sits $150 Off 2024 Highs

StockCharts

5. Charles Schwab $10 Trillion in Assets Under Management—Breaks Out to New Highs

StockCharts

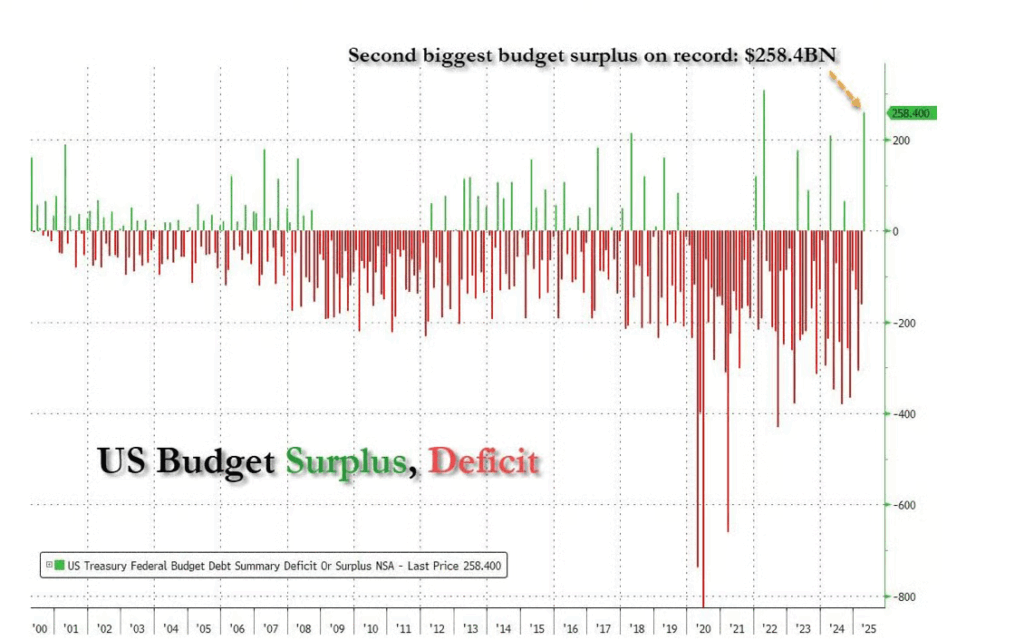

6. April Large Budget Surplus

Presenting Exhibit A: in April, the US Treasury generated a $258.4 billion surplus after last month’s $160.5 billion deficit; this the second biggest surplus on record, with just the $308 billion bumper surplus in 2021 bigger.

ZeroHedge

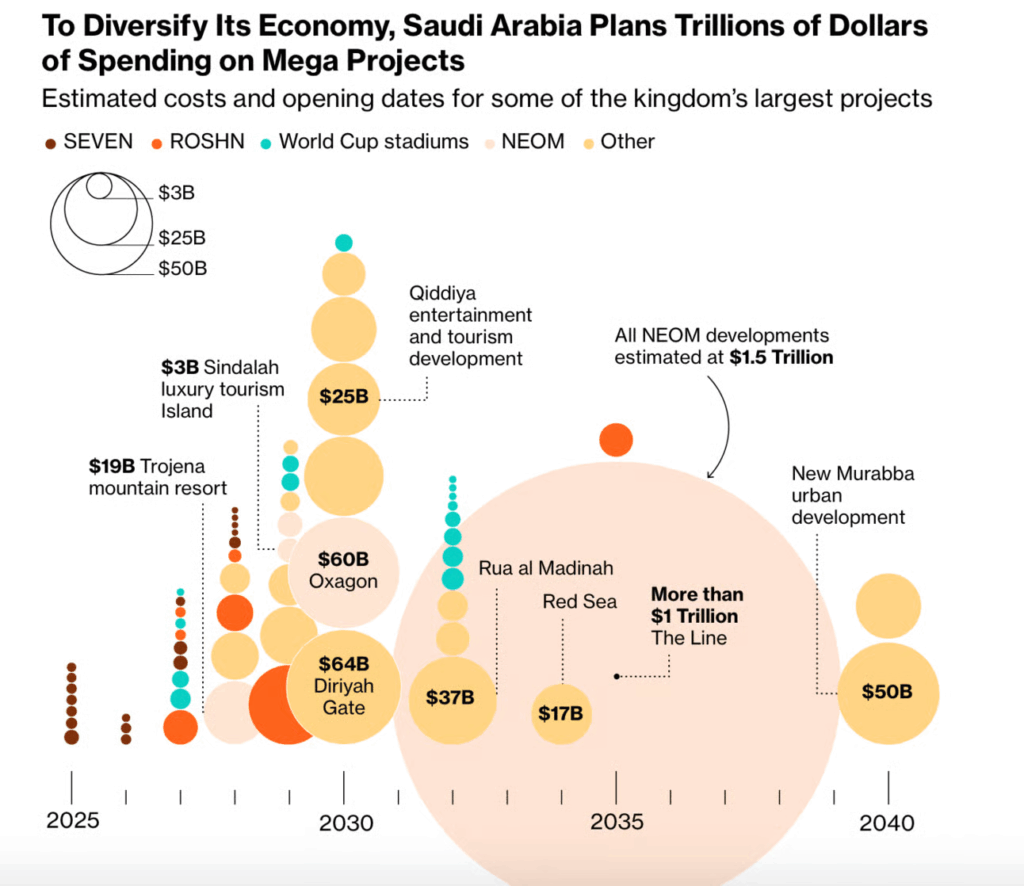

7. Trump in Saudi Arabia Asking for Investment in U.S. but MBS Betting Trillions on Home Mega Projects

Bloomberg

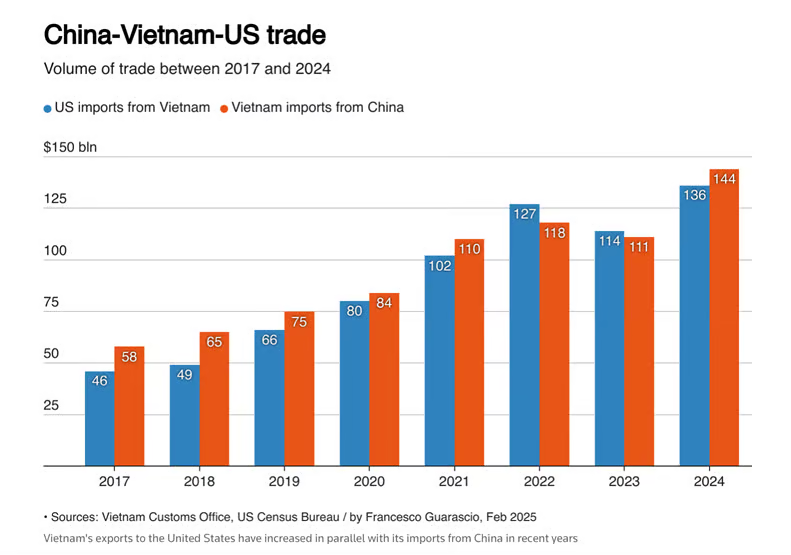

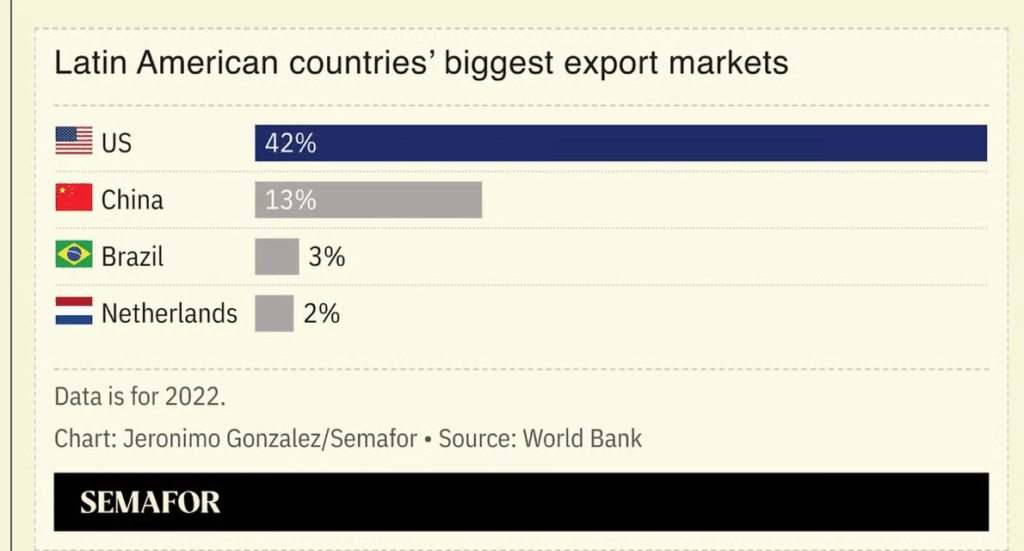

8. Latin American Exports 42% to U.S.

Semafor

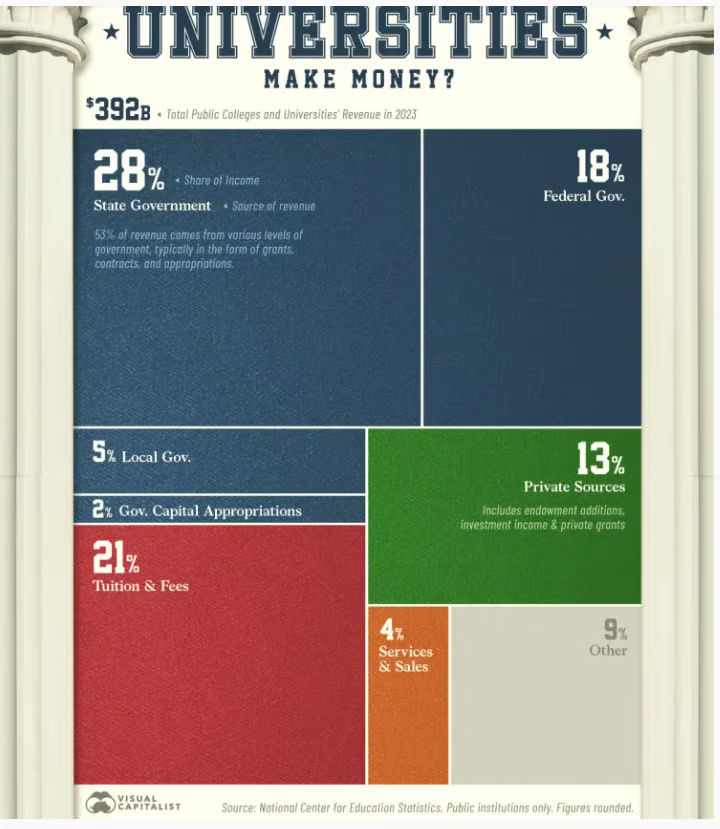

9. How Do Universities Make Money?

Voronoi

10. Stop Chasing Comfort, Start Building the Future You

Stop Chasing Comfort, Start Building the Future YouThe future you is an unfinished prototype.

KEY POINTS

- Growth comes from embracing discomfort, not from seeking comfort or immediate results.

- Identity evolution requires releasing outdated roles and accepting productive discomfort.

- Mental toughness and resilience are built by pushing through perceived limits, not avoiding them.

- Psychological safety and feedback are essential for personal development and successful transitions.

Via Psychology Today: In a world obsessed with instant results, busyness is often mistaken for progress. Meetings, emails, and endless tasks can create the illusion of momentum, but are we moving forward? True growth doesn’t come from checking boxes; it comes from leaning into the uncomfortable, uncertain work of becoming who we’re meant to be.

Psychologists like Walter Mischel and Carol Dweck have shown that while we’re wired for immediate gratification, lasting development requires embracing productive discomfort. Discomfort, in the right context, isn’t a warning sign; it’s proof that growth is happening.

The best leaders, teams, and organizations don’t avoid discomfort, they use it. It’s their edge for innovation, resilience, and transformation.—Brene Brown, University of Houston

The future you is an unfinished prototype

Through repeated endurance challenges, I discovered the true power of the 40 Percent Rule: the real limit isn’t physical, it’s mental. Discomfort wasn’t a sign to stop; it was my mind clinging to the familiar. Resilience isn’t just about pushing through, it’s about realizing how much more you’re capable of.

These experiences revealed something deeper: discomfort isn’t the enemy, it’s the entry point. Life’s transitions, whether chosen or forced, are often uncomfortable. But that discomfort? It’s not just to be survived, it’s a catalyst for growth.

Five ways to embrace it.

1. Lean Into Stretch Experiences

Growth rarely happens in comfort. Transitions often feel heavy because we carry the weight of outdated expectations and identity scripts. Our narrative identity is the evolving story we tell ourselves about who we are. To move forward with intention, we must first release what no longer serves us. Rituals of release, like writing a letter to your former self and burning it or leaving behind a symbolic object on a walk, can create psychological closure, a process linked to emotional integration and renewal.

Next, seek out stretch experiences: take a solo trip, learn a new skill, or pursue a goal that intimidates you. These challenges activate the growth mindset, the belief that abilities evolve through effort. Stretching yourself builds confidence, neural adaptability, and a deeper capacity for uncertainty.

The goal isn’t to erase the past. It’s to loosen your grip on who you were, so you can grow into who you’re becoming.

2. Invite Honest Feedback and Self-Reflection

Life transitions often trigger identity dissonance: the uncomfortable gap between your past self and your emerging one. Clinging to outdated roles, like the overachiever, the people-pleaser, or the expert, can lead to identity foreclosure, where we lock ourselves into fixed narratives too early or for too long.

To evolve, we need mirrors. Honest feedback from trusted mentors, friends, or colleagues can offer blind-spot clarity and help expand our sense of self. At the same time, self-reflection practices like journaling, mindfulness, or even voice-memo reflection can deepen self-concept clarity and a stable, coherent understanding of who you are across time.

Treat identity as a draft, not a declaration, ask: What part of me is ready to be released? What values no longer fit?

This isn’t about erasing the past. It’s about consciously reauthoring the story of you.—Cory Muscara, author and former monk

3. Focus on Progress, Not Perfection

Nature doesn’t grow in straight lines, and neither do you. Progress is often irregular, nonlinear, and full of feedback loops. Instead of forcing a rigid plan, consider a fractal mindset: the idea that small, self-similar shifts across different areas of life can lead to exponential transformation.

This is how change works in the real world: through micro-adjustments.Shift your morning routine by five minutes. Reframe one piece of internal dialogue. Swap one unhelpful habit for something nourishing. Each act wires your brain for change, reinforcing the principle of neuroplasticity, that your brain is always capable of rewiring toward who you’re becoming.

Progress isn’t about having it all figured out. It’s about showing up, again and again, with just enough curiosity and courage to take the next small step.—Woody Allen, filmmaker

4. Expose Yourself to Controlled Discomfort

Just like in physical training, emotional resilience is built by repeated exposure to challenge, not all at once, but in small, deliberate doses. This controlled exposure is a principle rooted in cognitive-behavioral therapy, where gradual, repeated contact with discomfort rewires our response to stress.

Proactively shake up your routine: Disrupt yourself before the world does. With time, these intentional acts of discomfort increase your psychological flexibility and the ability to adapt, recover, and respond creatively under pressure.

But true growth isn’t just about leaving your comfort zone occasionally, it’s about disrupting patterns intentionally before life forces your hand. If you only stretch when circumstances demand it, you’re always in reaction mode. And that’s the real power of resilience.—Unknown

5. Cultivate Psychological Safety for Yourself

Transitions feel destabilizing because they disrupt our sense of control or our internal locus of control, the belief that we can influence our outcomes. When that center is shaken, it’s easy to feel unmoored. But discomfort doesn’t have to break you, it can become the raw material for reinvention.

Uncertainty, when approached with intention, becomes a laboratory for growth. Acknowledge your fears without giving them the microphone. This is the essence of cognitive reappraisal, the ability to reinterpret challenges in ways that empower rather than paralyze.

Treat your transition like an art project. Surround yourself with people who value growth over perfection. Learn to say no to misaligned obligations and protect your energy for what aligns with your evolving self.

What can you experiment with? Which constraints can be reframed as creative catalysts? The goal isn’t to eliminate uncertainty, it’s to become someone who thrives within it.—Viktor Frankl, neurologist and psychologist

The Competitive Advantage of Embracing Discomfort

The challenge is not to seek the easiest path but to identify the right kind of discomfort, the kind that fuels progress rather than paralyzing fear. It’s the discomfort that helps us grow as humans and challenges us with the fundamental question: What am I supposed to be learning from this experience?

Growth requires a mindset shift: challenges aren’t roadblocks, they’re signs we’re operating at our edge, where real development takes place. The “future you” isn’t a finished product; it’s a prototype in motion. Time spent in uncertainty, awkwardness, or even doubt isn’t a detour; it is the path forward.

The real question isn’t just Where do I want to go? But, am I willing to embrace the discomfort it takes to get there? When we do, today’s challenges become stepping stones.

True transformation begins not in mastering the present, but in daring to evolve into what’s next.—Søren Kierkegaard, philosopher and theologian.