1. Dow Utilities, Industrials and Transports Still Below Highs.

Utilities -15% from highs

Utilities -15% from highs

Dave Lutz Jones Trading

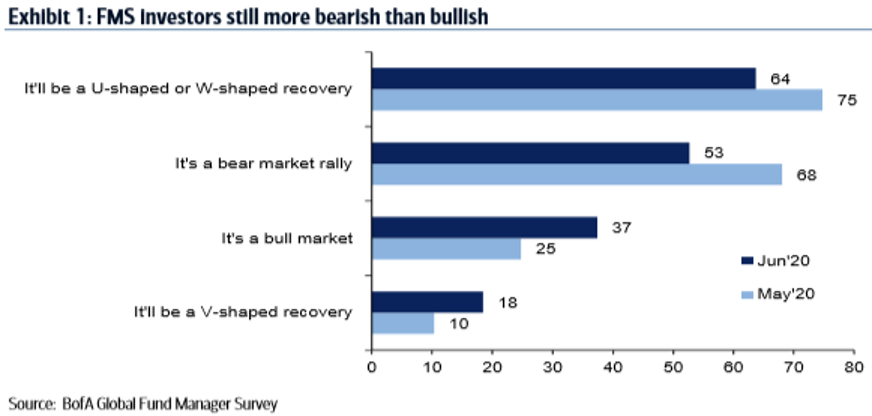

Pain trade is still up: Record net 78% of investors say stock market is “overvalued.” Most since start of the series in 1998. On the market rally, 37% say it’s a bull market while 53% say it’s a bear market rally

Among surveyed investors, 18% expect a V-shaped recovery and 64% expect a U- or W-shaped bounce – Second wave of Covid-19 remains biggest tail risk

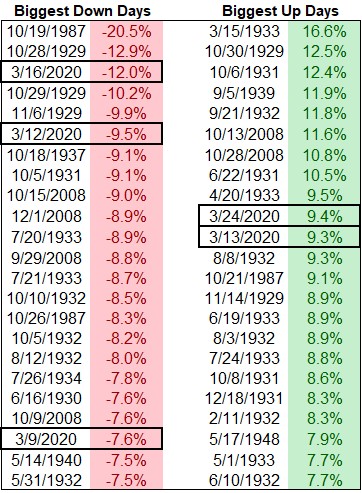

Not yet but it’s getting close. This year has 3 of the worst 25 losses and 2 of the 25 biggest gains for the S&P 500 since 1928:

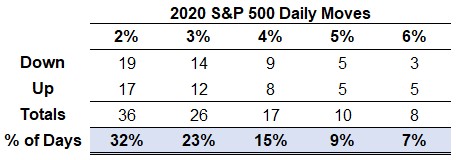

And the number of large daily moves is massive:

Read Full Story

https://awealthofcommonsense.com/2020/06/is-this-the-most-volatile-year-ever/

Found at Abnormal Returns Blog www.abnormalreturns.com

By Wolf Richter for WOLF STREET.

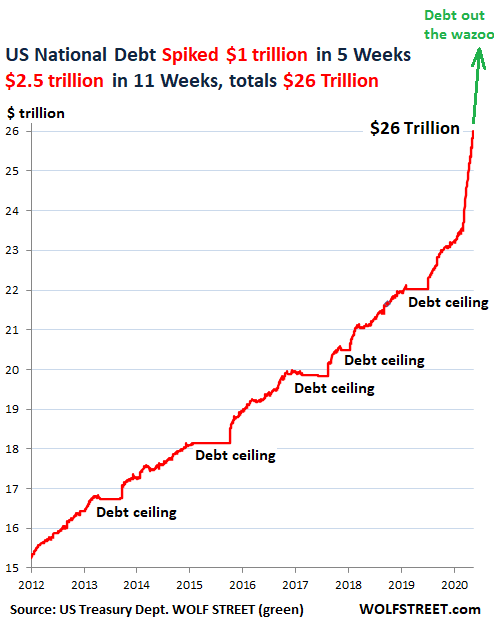

Trillions are now whooshing by at a breath-taking pace. The US gross national debt – the total of all Treasury securities outstanding – jumped by $1 trillion over the past five weeks, from May 4 through June 8, and by $2.5 trillion for the 11 weeks since March 23.

The total US national debt outstanding has reached $26 trillion, according to the Treasury Department. I’ve been fretting about this debt on my site since 2011. In recent years, I innocently added a green upward arrow with “Debt out the wazoo” to my gross-national-debt charts, unaware that this tongue-in-cheek label would turn into a factual, data-based technical term:

Wow, That Was Fast: Debt Out the Wazoo

by Wolf Richter • Jun 12, 2020 • 222 Comments https://wolfstreet.com/2020/06/12/wow-thats-fast-debt-out-the-wazoo/

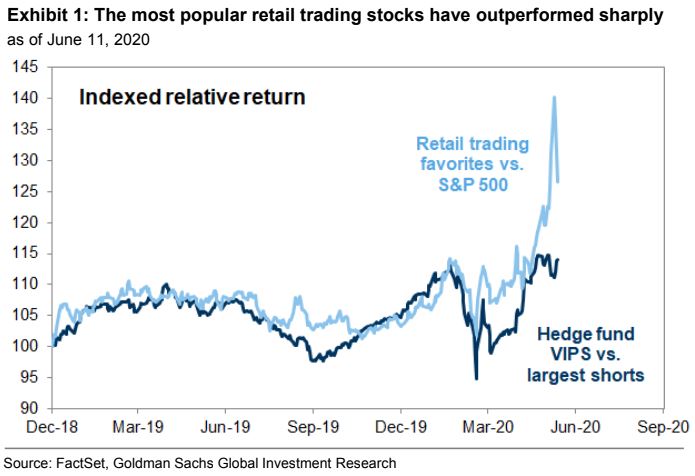

The Goldman analysts report that much of the outperformance by individual investors occurred in the middle of May, as upbeat data on declines in the spread of the deadly pandemic and less-bad economic reports encouraged bargain hunting in cyclicals, including small-capitalization stocks, and shares of companies that are economically sensitive and would therefore benefit from signs of improvement in the business climate.

Such stocks were “quickly embraced by value-seeking retail investors, and now make up a large portion of our retail basket,” Goldman researchers wrote (see attached chart).

A portfolio of stocks being bought by mom-and-pop investors is trouncing Wall Street pros — here’s what they’re buying-Mark DeCambre

Stone’s Weekly Market Guide – Week of June 15, 2020 Bill Stone

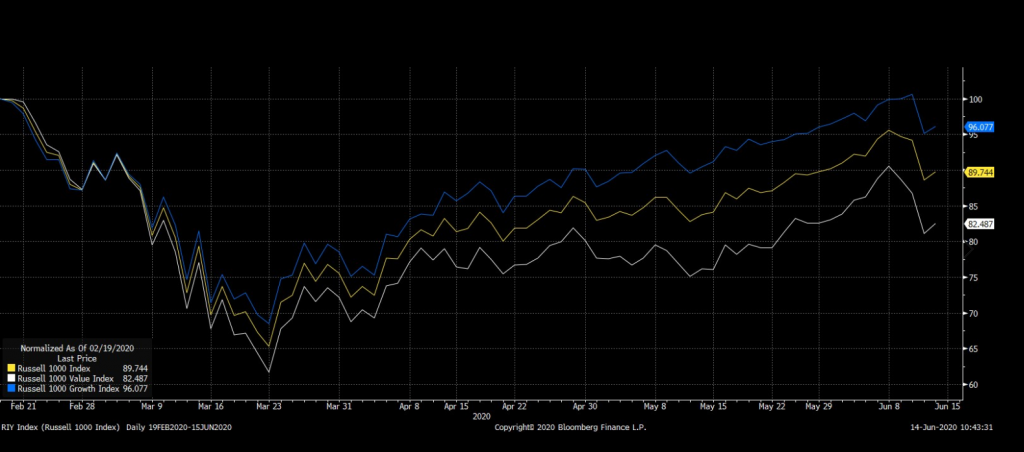

Chart of the Week: After a few weeks of outperformance, value went back to underperforming growth last week. For simplicity of explanation, this analysis uses the Russell indexes but other methodologies would have directionally the same results. Short-term, this poor performance is understandable since value stocks generally have more leverage to economic outcomes and more debt. The underperformance of value also holds since the February market peak with value fairing worse on the downside along with growth recently exceeding its February peak (see chart). Despite value being a factor that has led to long-term outperformance, the value has historically been subject to long periods of underperformance as the price of admittance to superior gains. Aside from some brief respites, value (+14.2% annualized) has underperformed growth (+19.2% annualized) by a wide margin since the global financial crisis bottom in March 2009.This differential means $100 became about $632 in growth versus $345 in value. Despite the grim performance comparison, the valuation differential between the two styles argues for at least a more balanced allocation between the two currently rather than focusing only on growth stocks. For those interested in more details, AQR recently wrote some excellent pieces about value underperformance linked here.

https://www.stoneinvestmentpartners.com/post/stone-s-weekly-market-guide-week-of-june-15-2020

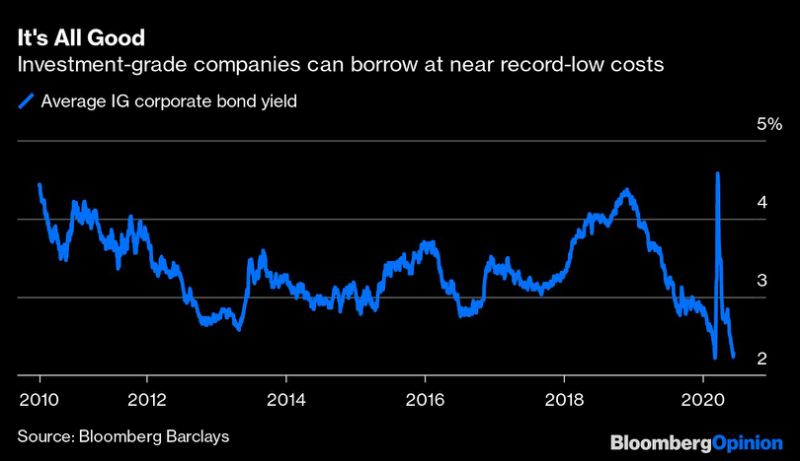

—Brian Chappatta

Fed Doesn’t Really Need to Buy Corporate Bonds

(Bloomberg Opinion) — The Federal Reserve realizes that it doesn’t have to buy U.S. corporate bonds, right?

I ask this question only somewhat in jest. In a surprise move, the central bank announced Monday that it would start to buy individual company bonds under its $250 billion Secondary Market Corporate Credit Facility, specifically by following a diversified index of U.S. corporate bonds created expressly for its program. “This index is made up of all the bonds in the secondary market that have been issued by U.S. companies that satisfy the facility’s minimum rating, maximum maturity and other criteria,” the Fed said in a statement. Notably, issuers of bonds acquired through this program don’t need to provide certifications, unlike the stipulations for individual debt purchases.

It’s not immediately clear why this is necessary, nor how this will impact markets any differently than the facility’s current purchases of exchange-traded funds. So far, the secondary-market vehicle has bought about $5.5 billion of ETFs. As my Bloomberg Opinion colleague Tim Duy quipped on Twitter, it’s as if policy makers said “we want to expand beyond ETFs, so we will purchase individual bonds such that we mimic an ETF.”

Predictably, the largest investment-grade bond ETF, ticker LQD, surged in the wake of the announcement to its biggest intraday gain since April 9. That was the day the Fed changed the parameters of its credit facilities to allow for purchases of high-yield ETFs and debt from fallen angels that were investment grade as of March 22.

The most surprising part of this is there is virtually no evidence that the corporate-bond market needs this kind of intervention — it has been working nearly flawlessly for months. Sure, the credit ratings of several brand-name companies have been lowered since Covid-19 started to spread across America in March. Some even fell into junk, like Ford Motor Corp., Kraft Heinz Co. and Macy’s Inc. For countless others, their business model has radically changed for at least the next several months, if not years.

And yet the average yield demanded by investors for investment grade debt fell last week to just 2.23%

https://finance.yahoo.com/news/fed-doesn-t-really-buy-194612619.html

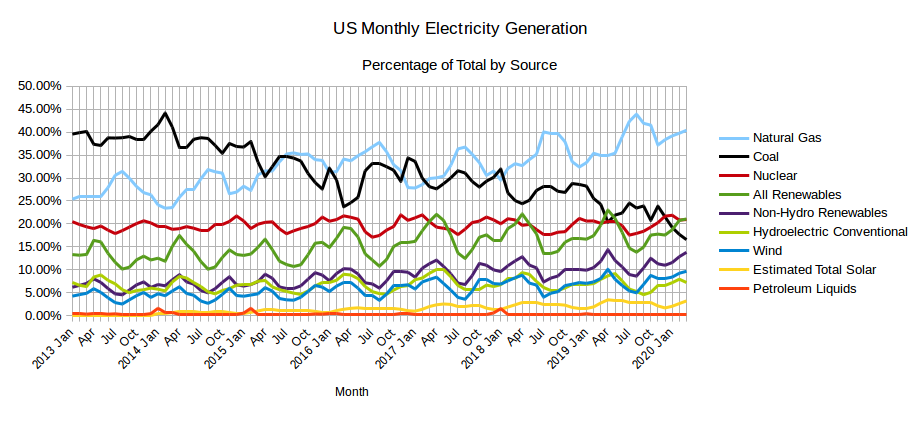

EIA’s Electric Power Monthly – May 2020 Edition with data for March

by ISLANDBOY posted on 06/02/2020

The EIA released the latest edition of their Electric Power Monthly on May 26th, with data for March 2020. The table above shows the percentage contribution of the main fuel sources to two decimal places for the last two months and the year 2020 to date.

The Table immediately above shows the absolute amounts of electricity generated in gigawatt-hours by the main sources for the last two months and the year to date. In March the absolute amount of electricity generated decreased slightly, joining the years 2015 and 2016 as the only years since 2013 that did not see a slight increase in electricity production between February and March. Coal and Natural Gas between them, fueled 56.95% of US electricity generation in March. The contribution of zero carbon and carbon neutral sources increased from 41.55% in February to 41.99% in March. The percentage contribution from Natural Gas in March edged back above 40% at 40.41%, increasing from 39.76% in February.

PEAK OIL BARREL http://peakoilbarrel.com/eias-electric-power-monthly-may-2020-edition-with-data-for-march/#more-27081

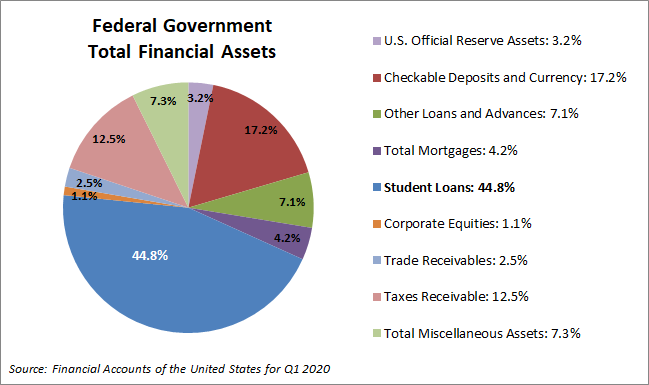

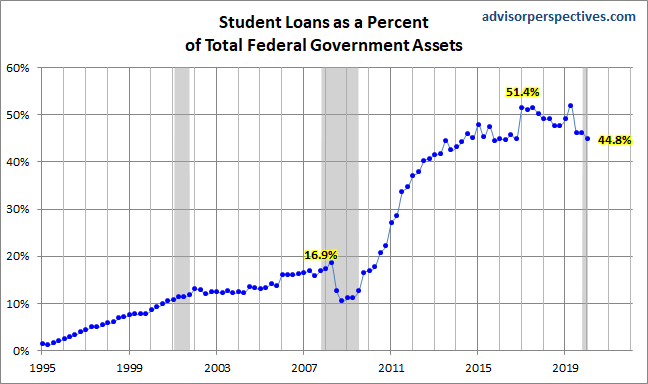

But back to our quiz. Student loans may be a liability on the consumer balance sheet, but they constitute an asset for Uncle Sam. Just how big? It’s about 44.8 percent of the total Federal assets. This is 10.8 times larger than the 4.2 percent for the Total Mortgages outstanding and 3.6 times the size of Taxes Receivable at 12.5 percent.

The 44.8 percent referenced is below its peak. Here is a look at how this metric has changed since 1995.

The Fed’s Financial Accounts: What Is Uncle Sam’s Largest Asset?-by Jill Mislinski, 6/12/20

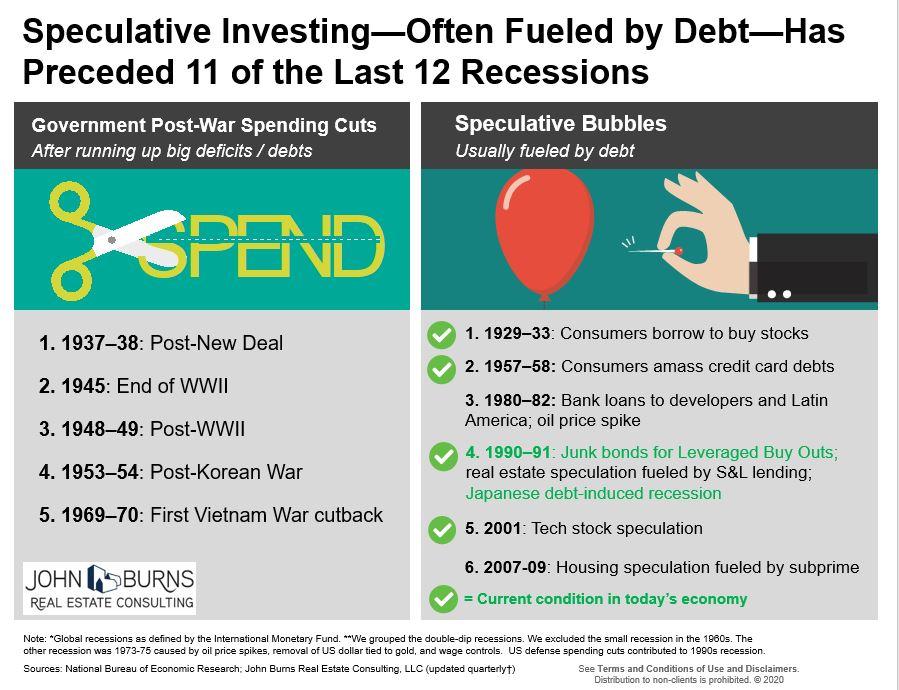

John Burns Real Estate

https://www.linkedin.com/in/johnburns7/

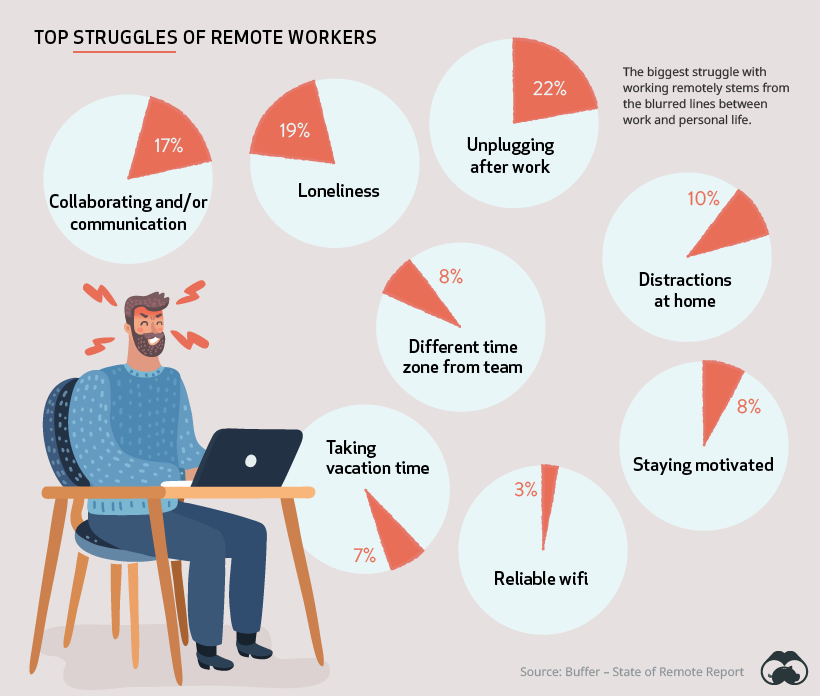

How People and Companies Feel About Working Remotely–Nick Routley

The way to create effective working teams starts here.

BY MARCEL SCHWANTES, FOUNDER AND CHIEF HUMAN OFFICER, LEADERSHIP FROM THE CORE@MARCELSCHWANTES

Getty Images

Now more than ever, companies need to create cultures centered on employees. Strong cultures create effective working teams that attract top talent, while weak cultures can quickly lead to burnout or employees heading for the exit.

Companies facing these high stakes are eager to create a place where employees want to go to work. But they can struggle to find the right person to own culture. Who will invest in leading their organization’s unique blend of people and purpose?

Latane Conant, CMO of 6sense, an account engagement platform, sees the tie between a company delivering great customer experiences and having great employee experiences. She has made it her mission to develop an employee-centered community unified by a common purpose.

Conant shared with me four key perspectives on how leaders can build meaningful company cultures:

1. Build trust through transparency

Companies need trust to create a productive community and culture, which derives from honesty and openness. While leaders may be forthcoming with each other, Conant says that transparency should be extended throughout the organization.

Conant advises executives to create a clear and transparent vision and detailed plans, and then revisit the company strategy regularly.

Conant also says marketing teams and its senior leaders must embrace and champion strategic transformation. “Marketing has to evangelize new strategies and set the tone for everybody else,” she said. “They have to wear it proudly, nail the pitch to their coworkers and be the cheerleaders your company needs to make the transformation work.”

2. Prioritize connection

In companies, connection happens constantly, and Conant says good cultures prioritize communication and connection. To foster healthy connections, she recommends shoutouts and public feedback recognizing employees working the strategic plan. She is also a firm believer in the all-hands meeting.

“Do not skip your all-hands meeting! It should be treated as a sacred space, where your employees gather to talk about what matters most,” Conant said. “Once you start blowing off the meeting or rescheduling it constantly, you lose your chance to keep everyone focused on the company’s strategic plan and vision.”

3. Lead by example

While leaders work to agree on company direction, Conant says they should also gather feedback on how teams perceive their leadership. Like the all-hands meeting, she encourages leaders to conduct at least biweekly one-on-one meetings with employees to have two-way conversations and help employees achieve their own career goals.

Conant also believes leaders show trust by providing examples of their own experiences — both successes and failures — when they talk with employees. While it’s scary to start, she says leaders who model the openness they preach will find it happening organically within their teams.

4. Have more fun

Conant encourages leaders to ask their employees what they enjoy doing, then incorporate fun into the day job. Make work a place people want to be — beyond perks like a snack-filled fridge.

Conant is also using data to evaluate her office’s “Fun Factor.” Her team deploys a biweekly survey asking how much fun employees had. She reviews the results and determines what changes to make to bring more fun into the job.

Most importantly, she says, leaders have to model fun. “If leaders want their employees to take part in trivia nights or karaoke, then they have to get up and sing along, too.”

Whether it’s championing the strategic plan, creating open and collaborative spaces or having fun, intentional planning and commitments to community help companies create a place employees want to be.

MAR 13, 2020

Like this column? Sign up to subscribe to email alerts and you’ll never miss a post.

The opinions expressed here by Inc.com columnists are their own, not those of Inc.com.

https://www.inc.com/mbvans/contest.html?cid=sf01003

Disclaimer

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania..

To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results.

Material compiled by Lansing Street Advisors is based on publically available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data.

Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only

SMH-Semiconductor ETF

CHIPS for America Act Would Strengthen U.S. Semiconductor Manufacturing, Innovation

Wednesday, Jun 10, 2020, 4:58pm

by Semiconductor Industry Association

New bipartisan legislation, introduced in the Senate by Sens. Cornyn (R-Texas), Warner (D-Va.), Risch (R-Idaho), Sinema (D-Ariz.), and Rubio (R-Fla.) and in the House by Reps. Matsui (D-Calif.) and McCaul (R-Texas), would counter competing nations’ massive government incentives and strengthen U.S. economy, national security

WASHINGTON—June 10, 2020—The Semiconductor Industry Association (SIA) today applauded the introduction in Congress of the Creating Helpful Incentives to Produce Semiconductors for America Act (CHIPS for America Act), bipartisan legislation that would invest tens of billions of dollars in semiconductor manufacturing incentives and research initiatives over the next 5-10 years to strengthen and sustain American leadership in chip technology, which is essential to our country’s economy and national security. The bill was introduced today by Sens. John Cornyn (R-Texas), Mark Warner (D-Va.), Jim Risch (R-Idaho), Kyrsten Sinema (D-Ariz.), and Marco Rubio (R-Fla.) in the Senate, and a House version is slated to be introduced Thursday by Reps. Michael McCaul (R-Texas) and Doris Matsui (D-Calif.).

“Semiconductors were invented in America and U.S. companies still lead the world in chip technology today, but as a result of substantial government investments from global competitors, the U.S today accounts for only 12 percent of global semiconductor manufacturing capacity,” said Keith Jackson, President, CEO, and Director of ON Semiconductor and 2020 SIA chair. “The CHIPS for America Act would help our country rise to this challenge, invest in semiconductor manufacturing and research, and remain the world leader in chip technology, which is strategically important to our economy and national security. We applaud the bipartisan group of leaders in Congress for introducing this bill and urge Congress to pass bipartisan legislation that strengthens U.S. semiconductor manufacturing and research.”

The U.S. currently maintains a stable chip manufacturing footprint, but the trend lines are concerning. There are commercial fabs in 18 states, and semiconductors rank as our nation’s fifth-largest export. However, significant semiconductor manufacturing incentives have been put in place by other countries, and U.S. semiconductor manufacturing growth lags behind these countries due largely to a lack of federal incentives.

The CHIPS for America Act includes a range of federal investments to advance U.S. semiconductor manufacturing, including $10 billion for a new federal grant program that would incentivize new domestic semiconductor manufacturing facilities. The bill also includes a refundable investment tax credit for the purchase of new semiconductor manufacturing equipment and other facility investments.

Research is critical to advancing semiconductor innovation in the U.S. American semiconductor design and manufacturing companies invest approximately one-fifth of revenue in R&D, almost $40 billion in 2019, representing the second-highest rate of research investment of any industry. Federal government investment in semiconductor research, however, is only a small fraction of total semiconductor R&D in the U.S. and has been relatively flat as a share of GDP for many years. Meanwhile, China and others are increasing their government research investments.

The CHIPS for America Act would make significant federal investments at the Department of Defense, the National Science Foundation, and the Department of Energy to promote semiconductor research and drive chip technology breakthroughs. The bill would establish a National Semiconductor Technology Center to conduct research and prototyping of advanced chips, as well as create a center on advanced semiconductor packaging. These investments are needed to enable U.S. companies to maintain their technological edge in semiconductor materials, process technology, architectures, designs, and applications.

“As global competitors invest big to attract advanced semiconductor manufacturing to their shores, the U.S. must get in the game and make our country a more competitive place to produce this strategically important technology,” said John Neuffer, President and CEO of the Semiconductor Industry Association. “We commend the bipartisan original cosponsors in both the Senate and House for their leadership in introducing this bold, timely legislation and urge Congress to move forward on a bipartisan basis to strengthen the bill and bolster domestic semiconductor manufacturing and research.”

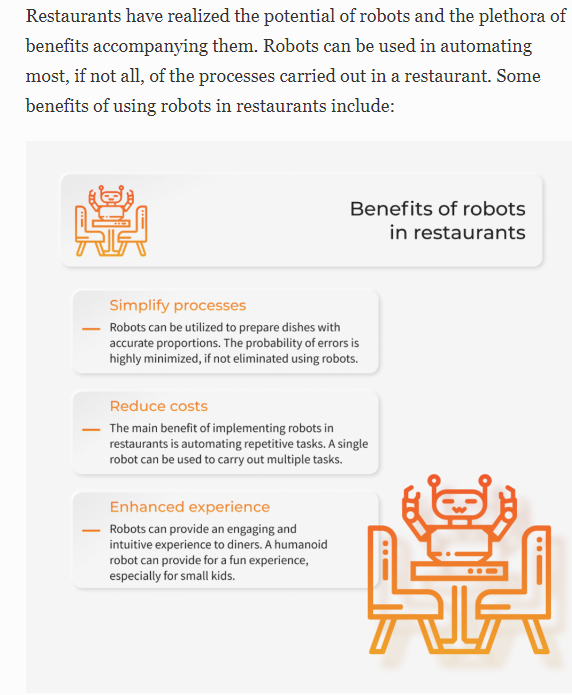

FORBES –Bon Appétit! Robotic Restaurants Are The Future-Naveen JoshiContributorCOGNITIVE WORLD

ROBO ETF Chart Hit New Highs in Rally.

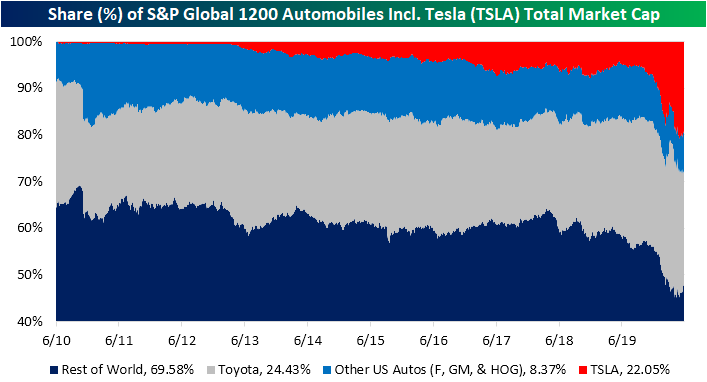

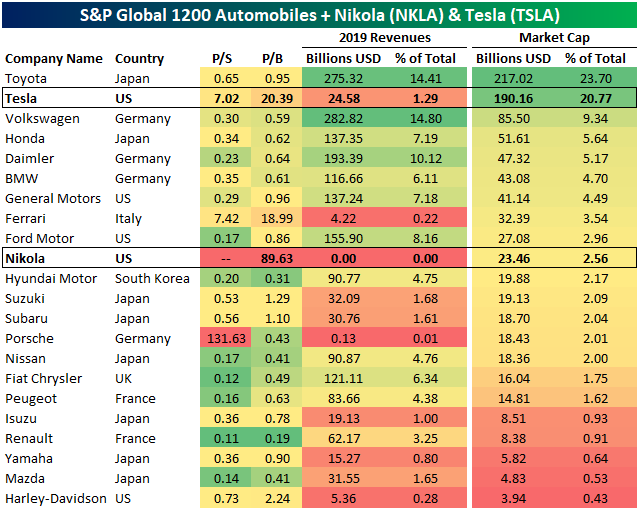

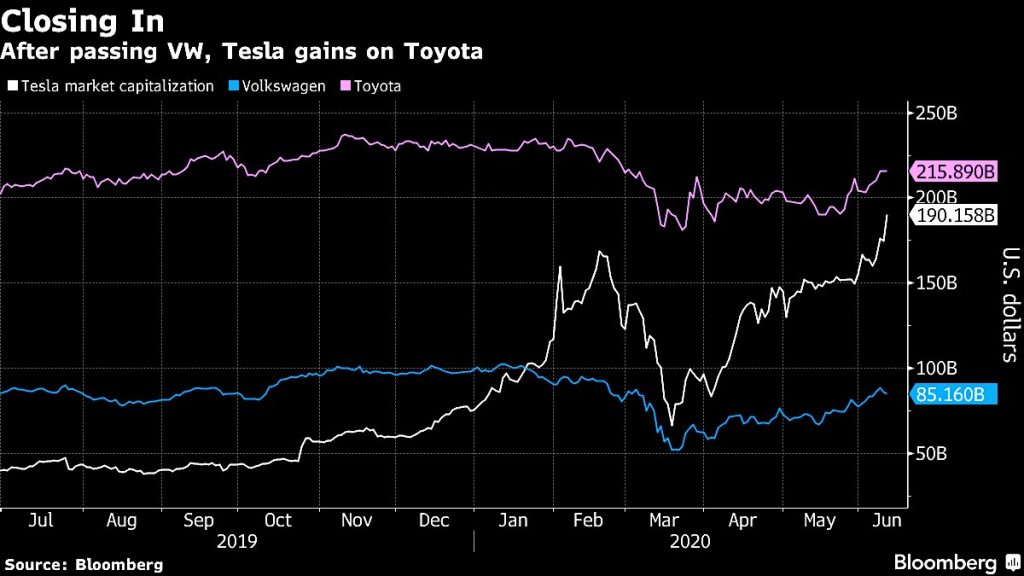

In today’s Chart of the Day, we detailed Tesla’s (TSLA) rise above $1,000 and what other stocks like Google (GOOGL) and Amazon (AMZN) have looked like when they first crossed $1,000. With TSLA reaching these kinds of levels, it also now has a record share of the total market cap of global automobile makers. Including the electric car company with the other 20 companies in the S&P Global 1200 Automobile Index, TSLA accounts for just over 22% of the total market cap. That is the second-largest of any company behind only Toyota whose $210.69 bn (USD-adjusted) accounts for 24.43%. As we have detailed in the past, TSLA’s market cap is now significantly larger than other US automobile producers like Ford (F), General Motors (GM), and Harley Davidson (HOG). In fact, it is now more than double the market caps of those companies combined! The rest of the world’s automobile companies including Japanese names like Honda and German names like BMW and Daimler (Mercedes) account for 69.58% of the total market cap.

Although TSLA accounts for a massive share of world automaker’s market cap, it still makes up for a very small share of these companies’ total revenues. In fact, its $24.58 bn in sales in 2019 only accounted for 1.29% of all these companies’ total revenues. Albeit it is a high growth name, that leaves it with one of the higher valuations on a P/S and P/B basis. A similar dynamic can be seen for other high-end brands like Italian brand Ferrari and German brand Porsche. The same can be said for another electric vehicle stock that has received a large amount of headline attention recently, Nikola (NKLA). NKLA likewise is another name with a fairly large disparity between its sales and share of market cap. Another high growth name and recent IPO, Nikola actually had no revenues in 2019 but is valued at $23.46 bn or 2.56% of total market cap. That is more than some other major global brands like Hyundai, Suzuki, and Subaru to name a few. Click here to view Bespoke’s premium membership options for our best research available.

https://www.cbinsights.com/research/personal-finance-apps-strategies/

Dave Lutz at Jones Trading.

Zerohedge

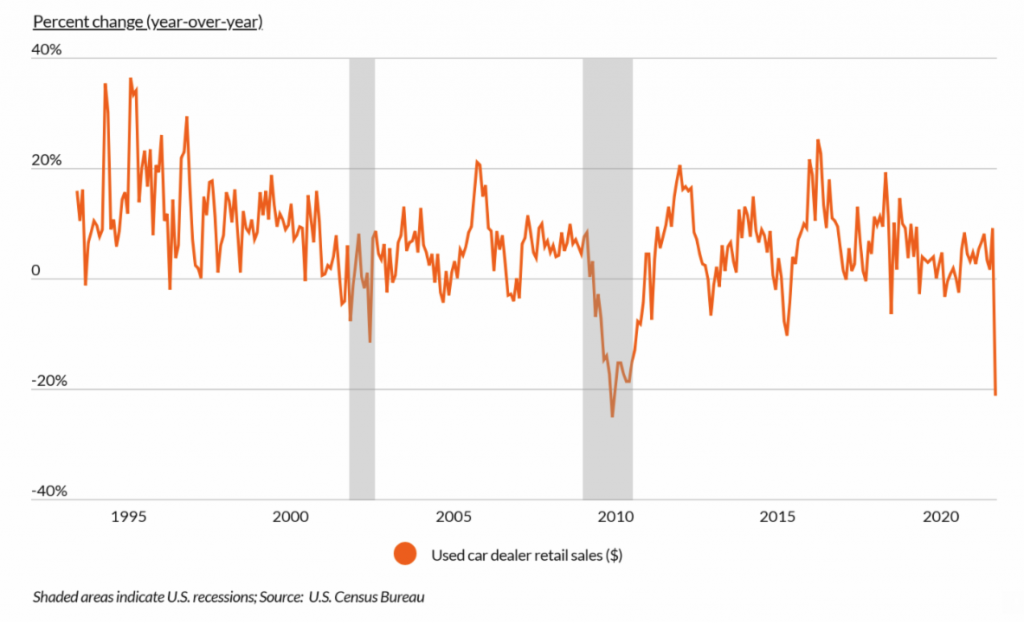

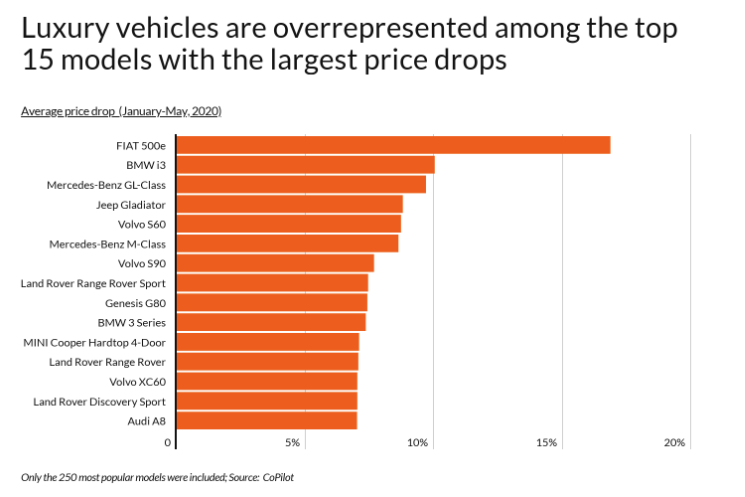

But at the same time, used car prices have been tanking. Over the last few months we detailed how used car prices were set to cripple what little interest in new cars remains, how dealers are scrambling to desperately offer incentives and how ships full of vehicles are being turned away at port cities due to a lack of space and inventory glut.

Today, we want to take a look at where the used car price plunge – which continues to put pressure on the industry – is having the biggest impact. A new report from CoPilot, a car shopping app, looks at the recent drop in used car prices in the U.S.

Research firm Manheim has indicated that wholesale prices dropped as much as 11% in April, but also that this price drop hasn’t fully hit the retail market yet. The report predicts that since “dealers have largely avoided purchasing new inventory in recent weeks, they aren’t in a rush to cut prices as a way to move their existing inventory.”

Where Used Car Prices Are Crashing The Most In The USby Tyler Durden

https://www.zerohedge.com/personal-finance/where-used-car-prices-are-crashing-most-us

The Economy Is Reeling. The Tech Giants Spy Opportunity.

Many companies are retreating. But Amazon, Apple, Facebook, Google and Microsoft are placing bets to get even bigger.

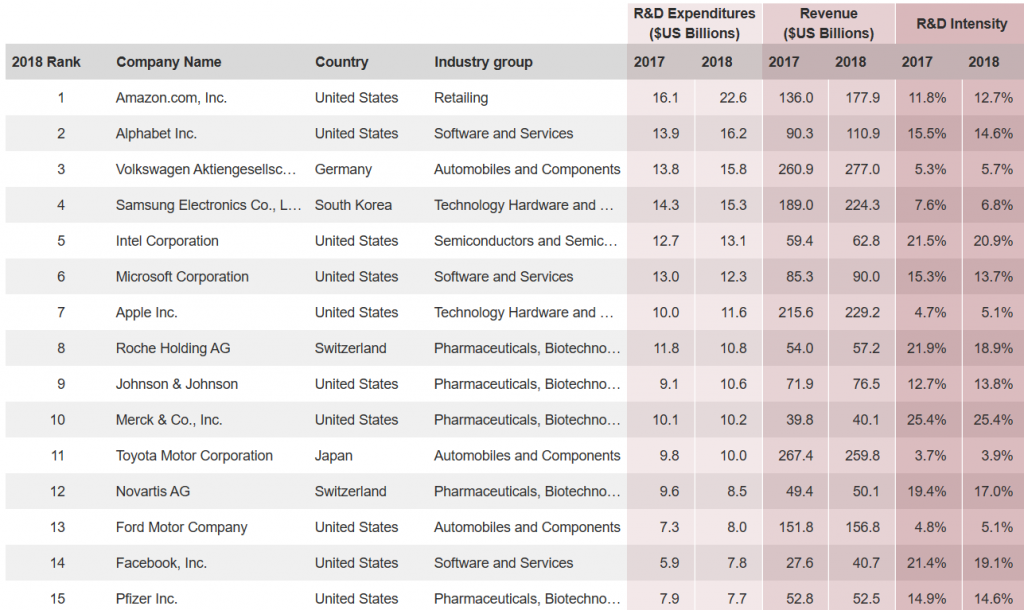

PWC

The 2018 Global Innovation 1000 study

The Global Innovation 1000 study analyses spending at the world’s 1000 largest publicly listed corporate R&D spenders. The interactive data tool below lists the Top 25 largest corporate R&D spenders from the years 2012-2018 worldwide. You can use the tool to filter by year, company name, country, and industry group to view R&D expenditures, Revenue, and R&D intensity (R&D expenditure as a percentage of Revenue). In order to see the complete list of Top 1000 corporate R&D spenders from the years 2012-2018 see the “Download the Data” section. Click here for the methodology.

https://www.strategyand.pwc.com/gx/en/insights/innovation1000.html#VisualTabs1

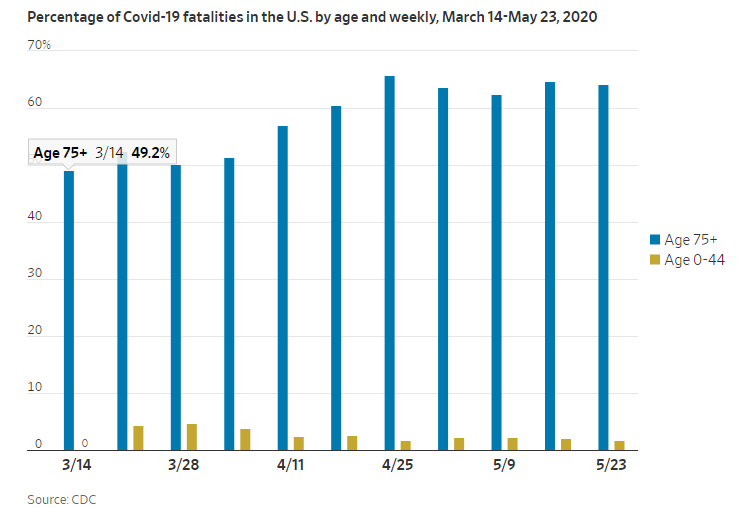

About 80% of Americans who have died of Covid-19 are older than 65, and the median age is 80. A review by Stanford medical professor John Ioannidis last month found that individuals under age 65 accounted for 4.8% to 9.3% of all Covid-19 deaths in 10 European countries and 7.8% to 23.9% in 12 U.S. locations.

The Covid Age Penalty-New patient data offers a guide to opening while protecting seniors.By The Editorial Board

https://www.wsj.com/articles/the-covid-age-penalty-11592003287

By Jordan Valinsky, CNN Business

Updated 6:46 AM ET, Wed June 10, 2020

New York (CNN Business)Nearly three months after Covid-19 upended daily life, one thing is becoming increasingly clear: Americans are dealing with coronavirus by drinking. A lot.

Since March 7, alcohol sales have grown nearly 27%, according to Nielsen. Two big winners are domestic beers and spiked seltzer, with the former being practically on life support just a year ago.

Customers have been turning away from domestic brews, instead preferring pricier imports, such as Corona, appropriately, and lower-calorie alternatives like White Claw or even straight-up liquor, particularly tequila. But the affordability and larger pack sizes have helped sales of domestic brands, such as Busch Light, Miller Lite and Natural Light, surge higher.

Budget beer has boomed for two reasons: price and familiarity, according to Daniel Blake, vice president of US value brands at Anheuser-Busch. He believes shoppers were in a “stock up” mode as people sheltered in place and had to limit their trips. People were also buying “larger and more trusted brands with an emphasis on affordability,” he told CNN Business.

Blake oversees marketing for Busch Light and Natural Light. Both beer brands have created viral promotions, including Busch Light’s dog adoption campaign that gave 500 people a three months’ supply of beer. Sales have risen since mid-March because they both “bring fun into [buyers’] lives and also do good.”

He said that the beer brands aren’t changing their marketing and are launching new products to sustain growth. For example, Busch Light is adding a limited-time apple-flavored beer in July. Natural Light is rolling out a variety pack of its Natty Light Seltzer brand with a new strawberry-kiwi flavor.

Natty Light Seltzer launched last summer and he said sales “exceeded our expectations.” Anheuser-Busch (BUD) has a number of spiked seltzer brands as it tries to dethrone White Claw and Truly from the top two spots — both combined have a market share of 77%. The remaining top three brands — Bud Light Seltzer, Corona Seltzer and Smirnoff — make up a combined 16% of sales, according to Nielsen.

The category is keeping its monster-growth pace, leading to several brands launching new spiked seltzers at a dizzying clip. Last month, Anheuser-Busch launched Social Club Seltzer, a premium seltzer with cocktail flavors, like an Old Fashioned.

Seltzers have racked up nearly $1 billion in sales from March 7 to May 30, according to Nielsen. In comparison, spiked seltzer sales totaled $1.5 billion in all of 2019. That makes it an enviable category for large and small alcohol companies to dip their toes into, even if competition keeps tightening.

“Within the hugely successful and growing hard seltzer segment, new and ‘old’ brands alike can succeed even if their market share is relatively small or declining, because the total pool of sales of hard seltzer within US retail is growing at such a high rate,” Danelle Kosmal, VP of Beverage Alcohol at Nielsen, told CNN Business.

“As such, with new launch after new launch, manufacturers may lose market share but continue growing their sales,” she added.

https://www.cnn.com/2020/06/09/business/budget-beer-spiked-seltzer-sales-coronavirus/index.html

Dr. Mercola (of the Mercola Video Library) interviewed three centurions for this very information, and many other people have as well. Quite a few of us (more now than ever) have relatives or know someone who is 100 or over.

One lady I know is 104 is full of sassy attitude and enjoys talking to people and sharing her wealth of wisdom. From my conversations with her and the interviews, here’s what we discovered about the secrets to living a happy and fulfilling life.

1. Happiness comes from what we do

At 100 years old, or older, people don’t seem to sit around and smile about the things they accumulated in life. Rather, it’s more about their life experiences. Happy memories can go a long ways toward happiness later on!

One man over 100 years old said he did all he wanted to do. Now he wants to be helpful and keep going.

“I have so many beautiful memories,” said a woman over 100. “I got to do all the things I wanted to.”

That tells us to jump in and live life – remember that it’s about really living and making memories with people we love.

Science backs this up as well. We know people derive more happiness that is long-term from experiences such as vacations rather than from possessions.

2. Happiness comes from a positive attitude and optimism

People over 100 seem to remember life through rose tinted glasses, making it sound like an adventure even through hard times, like war.

“I’ve always been lucky,” says one centurion despite living through 2 great wars!

She also talked about how “everything makes me happy. I love talking to people… going shopping.”

Common advice from people who are doing well at 100 is to “Decide to be content.” Others say, “Don’t chase happiness. Just be satisfied.”

Deciding life is good changes our perception and makes life better, and apparently it helps you live much longer!

3. Happiness comes from living in the NOW

Age is only a number. You live for the day and keep going.

This is wisdom from someone with a very long past-but they enjoy the present.

The past is the past; we can’t change it. But we can rob ourselves of our present happiness and good emotional health by hanging onto old regrets, grudges, and pain.

To experience the ultimate feelings of inner calm and living in the now, I highly recommend that you follow this link to 7 Minute Mindfulness…

You’ll gain inner peace, happiness and feel ‘uncluttered’ in your life.

4. Love and Partnership is critical for long life

Centurions often talk about their “good” marriage, all their happy memories, and all their good times together. It’s another area where they might be applying rose-tinted glasses, but it’s apparent that they got emotional support and felt like they have a life partner.

They also say that people today give up too easily these days-so there was hard work involved, but at the end of their life that part isn’t really important anymore.

“Being happily married and happy in general is the remedy for all illness.”

We don’t have studies on how marriage or long-term relationships affect life span, but you don’t have to be a scientist to take note: centurions all speak about their decades long marriage with a smile on their face.

Even people who have been widowed for a few decades say they have many, many warm memories about their married life, and that still makes them happy.

5. Eat natural, real food to feel good and live long

Many people who are 100 say they feel strong and like they’re 69 or 79. These are the people who stay active physically and mentally, and have a lot to share with other people.

Many people over 100 talk about eating fresh food that they grew themselves.

And older people will tell you over and over: eat in moderation!

6. Learn to adapt for a better and longer life

“Life goes on regardless” is a common theme. People who live well into old age understand that there is hardship in life but they know life goes on and they must too.

If you live 7, 8, 9, 10 or more decades, you’re going to see a lot of change.

People who adapt and change with the times do better. It’s part of having a positive attitude-they’re excited for new opportunities instead of fearing change.

7. Help others

Helping others is one way to build relationships and connections, and it makes you feel great.

It’s another common theme among people who live to be over 100.

Being kind and helping others gives you a sense of purpose too, and it fights depression and anxiety. Not only that, it’s a way of staying active and productive after you retire.

It’s a win-win for everyone involved, and being older and retired can mean having more time for volunteering.

8. Always keep learning!

Older people will advise to get a good education to help you go far in life, and science has shown that people with a Bachelor’s degree actually do live about a decade longer than people who don’t have one. (From the U.S. Centers for Disease an Control Prevention)

Older people will tell you to keep learning all through life, both in and out of school.

Be curious-it makes life more interesting and fun. And it helps you stay engaged with life and the changing technology and times. That helps you adapt too.

9. Practice mindfulness

People over 100 tend to live in the moment as it comes, rather than worrying about plans, regrets, and getting caught up in pressure and worry.

They cherish special time with family and friends, the colours and smell of a new flower in spring, or the feel of the grass on their feet.

When life is enjoyed in the moment, it’s just better…

…And people who live in the moment more tend to live longer, happier lives!

For the ULTIMATE experience of mindfulness, I highly recommend that you check out 7 Minute Mindfulness.

This method will make your mind as calm as water…

I’m talking about a method that will allow you to sink into relaxation, and feel abundantly positive and happy within minutes…

It will fill your life with joy and satisfaction…

And teach you how to easily defeat any life problems that you may be facing.

And it only takes 7 minutes!

Actively practicing mindfulness is one of the best things you can do for yourself.

When we disconnect from the mental chatter (the past, future, worry, expectations and judgements), we are able to approach life with greater perspective – we tend to see the opportunities, instead of carrying around the weight of worry and mental baggage.

There’s a wealth of research on the long term and short term health benefits of mindfulness, including boosting your immune system, Preventing cellular aging, and reducing the likelihood of age-related diseases. (UCLA)

If you’d like disconnect from the mental chatter but don’t have time for long drawn out meditation, then try 7 Minute Mindfulness.

In just 7 minutes you can release the stress that builds up, wipe away the mental chatter, and relax your mind and body… so you can enjoy a long and prosperous life!

Originally published at anxiety-gone.com.

Follow us here and subscribe here for all the latest news on how you can keep Thriving.

Stay up to date or catch-up on all our podcasts with Arianna Huffington here.

— Published on December 27, 2018

By Greg Thurston, Creator of 7 Minute Mindfulness

Disclaimer

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania..

To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results.

Material compiled by Lansing Street Advisors is based on publically available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data.

Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only

Friends,

I apologize for almost a month of missed blog posts but I have launched a new firm Lansing Street Advisors. The blog suffered in the short-term transition but we are planning a comeback that is stronger than ever. Please enjoy today’s post and the daily should be back in your inbox starting Monday but most important there is much more to come around Lansing Street Advisors. Thanks for reading and hope your families are healthy.

Matt

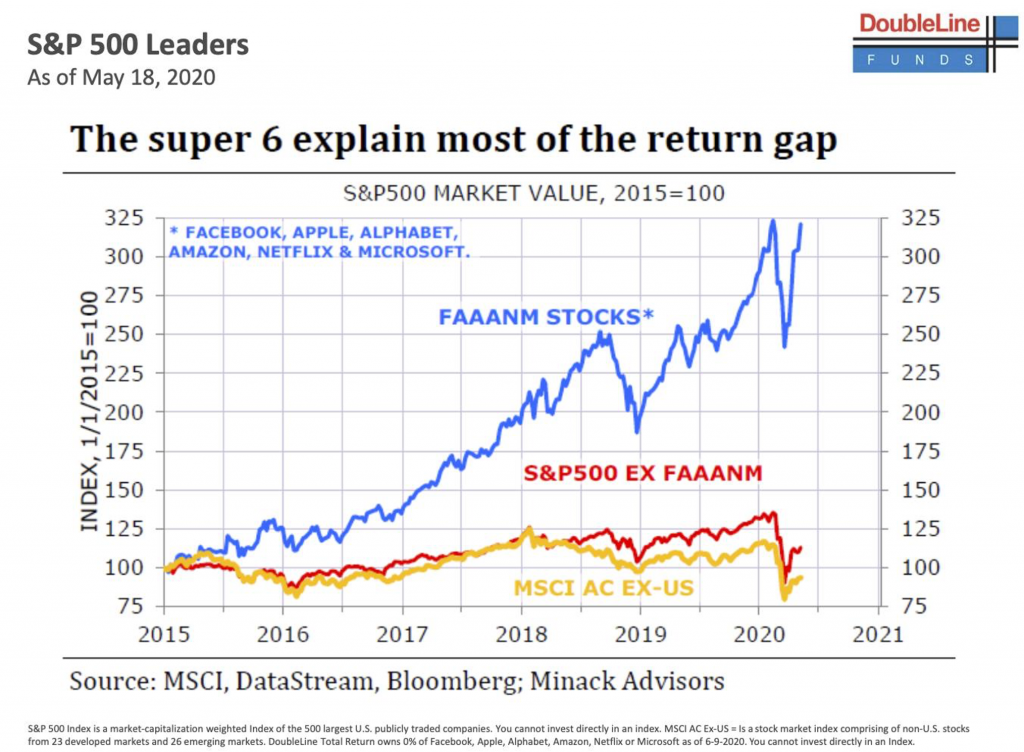

Jeff Gudlach DoubleLine.

Take these six stocks out of the market and the USA has returns similar to the rest of the world over the last five years! That’s the story of the stock market in a nutshell.

#doubleline #gundlach #investing #wealthmanagement #fang #faang #covid19 #covid #stocks

David DeWitt, CFP DeWitt Capital Management, Author & Expert in MLPs Dtdewitt@dewittcm.com 610.975.4435

Posted June 11, 2020 by Joshua M Brown

In the state of Texas, hospitalizations for the virus are up 42% since Memorial Day. The state of Arizona just issued a warning that they’re getting close to full capacity in their hospitals. Many states that have reopened are experiencing surges of cases and deaths, along similar trajectories of the spikes seen in the early days for New York, New Jersey, California, Michigan, etc.

And while this uptick in cases hits dozens of states, the S&P 500 grinds ever higher, led by the now-expected large cap growth rally. This is also being accompanied by a surge in corporate credit enthusiasm along with a three-ring circus of speculative feats, penny stock freak shows and momentum magic acts.

Why isn’t the market spooked by what some are describing as the virus’s “second wave”?

I have a few reasons I’ve listed. I may not know much about virology, epidemiology or public health, but I know a lot about people and investor attitudes, so here is my best attempt to understand it:

1. We did this already. It’s easy to scare investors. It’s harder to keep them scared. There’s a lot of regret from investors who sold toward the bottom as stocks recovered right in their faces just weeks later. There is an unwillingness to have the same thing happen again, to the same people, so the hesitance to swing back to cash on virus headlines is high. The White House has stopped talking about this subject. Let’s assume half of the investor class takes its cues from the President because of party affiliation and decides to ignore it too. Maybe more than half.

2. The Fed is literally telling us, in word and in deed, that they believe the best way to satisfy their dual mandate of price stability and full employment is to continue to purchase tens of billions worth of securities every month, from corporate bonds to Treasurys. They are not going away. They are saying they are not going away. The message has gotten through. And as they buy low risk assets from the holders, those holders turn around and put that cash into higher risk assets. The Fed takes your place in the money markets while you run off and join Ringling Brothers.

3. We are better equipped to handle new cases. Think about how much medical professionals, EMTs, nurses, doctors and hospitals have learned since February. There’s no way we’ll be as overwhelmed on a patient by patient basis as we were in New York this winter. Right?

4. Nursing homes. Everyone I talk to points out the statistic of how many of the deaths occurred in nursing homes versus outside of them. The last person to relay a stat to me said 30%. The person before that said 25%. Who knows what data they’re quoting, from what date and from what place? It’s just what they believe – that infections among the most vulnerable populations made the virus look much more deadly than it is. I know this is very controversial, and I’m not saying it’s true – I think this is just what people feel now. So they are less afraid for their lives, and acting that way with their investment portfolios.

5. Gains embolden us. This is a fact. We are less afraid, as an investor class, when it seems like money is growing on trees. That’s what 50% rebounds in large, well-known stocks will do. That’s what “the best 50-day period for US stocks ever” will do. Money attracts money.

6. It’s global. Stock markets around the world are rallying as central banks around the world do some version of what the Federal Reserve has done. European stimulus and even policy change have gone further than ever. Italy is selling a new class of sovereign bonds to its citizens that include a coupon linked to the future GDP growth of the country’s economy (they’re called Futura, nice). Chinese stocks are on fire, German stocks are up 20% in a month, etc.

7. Casino! Popular sports commentators (and their legions of followers) have pivoted to playing the stock market in the absence of games to bet on. We haven’t seen this much excitement from retail investors in 20 years. I was there last time, there are a lot of similarities but valuations are more reasonable and there are way less IPOs dumping new shares on us now. New brokerage account openings are skyrocketing. Fidelity is running ads on active trader subreddits. Barstool’s Dave Portnoy has introduced perhaps hundreds of thousands of young men to the game they never knew they could love. This may not be moving the $1.5 trillion market cap for Apple, but it is definitely influencing the prices of smaller stocks and more speculative ETFs. We’ll see if this phenomenon persists as the NBA gets started in July and the NFL season approaches.

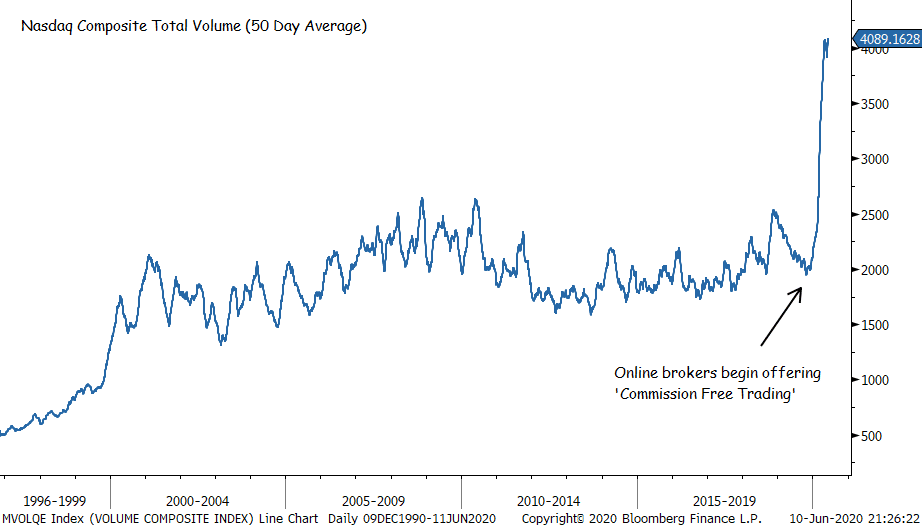

UPDATED!!! Including this chart from my pal Jon Krinsky – Nasdaq trading volumes have exploded!

8. Treatments and vaccines. Stock market participants tend to be optimists. I can’t know for sure, but I would guess two thirds of them believe that, between J&J, Moderna, Astra Zeneca and the hundreds of other trials taking place, something big is coming in the vaccine space. Enthusiasm for improved treatments is probably running on a parallel course.

9. Masks. They cost nothing and they work. In metropolitan areas around the country, people are wearing them. Takeout from restaurants, counters retrofitted with plexiglass and clear acrylic shields, delivery – we may not have the “old economy” but the new post-virus economy features businesses scratching and clawing their way back, which I love to see. Investors have decided that life will go on in the towns they live in, so why wouldn’t they invest accordingly?

10. Statistics. You can make a statistic say whatever you want, depending on when you start counting from. A lot of the data we’re seeing – in both corporate earnings reports and the overall economy – is coming off the bottom. Some of the percentage gains, for things like housing and airport traffic, are almost cartoonishly outsized. A Harvard economics professor remarked recently that Trump will have some of the best economic growth data in history to run on this summer because we are rebounding off of such low levels from the spring. You can fool a lot of people this way, and investors can always be relied upon to fool themselves.

Anyway, that’s what I think is going on. What do you think? Tell me here.

DAVE LUTZ at Jones Trading

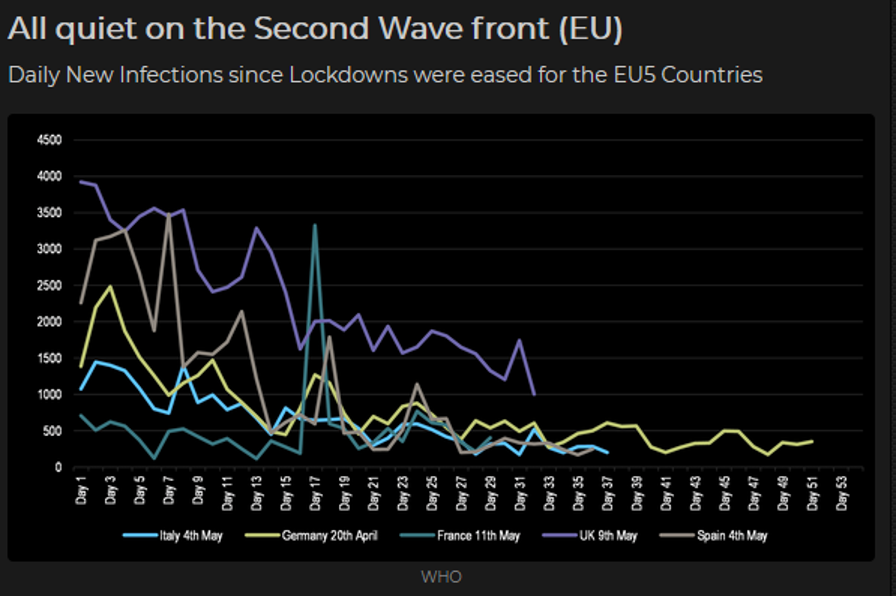

“It’s not a second wave, they never really got rid of the first wave,” says Dr. Scott Gottlieb on outbreaks in Arizona, Texas, South Carolina and North Carolina. There has been little evidence of a “Second Wave” in European countries that unlocked before the USA.

Electric truck maker Nikola looks like Tesla 2.0 — except even riskier…Formed thru a Reverse Merger ….Zero Trucks Sold.

A week before Nikola, the electric truck start-up, debuted its shares on the public market, it was time to spin up the hype machine. For some reason its founder and chief executive, Trevor Milton, wanted to talk about how much he loves Tesla.

You’d think he’d count Tesla as a rival, if not an enemy. Each aims to capture the market for long-haul diesel trucks. Each seeks to claim the mantle of brilliant inventor Nikola Tesla, who helped bring electricity to the masses by championing alternating current technology. Whenever the subject comes up, Tesla Chief Executive Elon Musk dumps on Nikola’s core technology, electric fuel cells, deemed by Musk as irredeemably inferior to Tesla’s own lithium ion battery power systems. “Fool cells,” he calls them.

But here was Milton, blowing kisses. “There are probably no bigger fans around the world than Nikola employees. Look at our parking lot. Teslas all over the place,” he said.

“We’re huge fans and the reason is this: Tesla paved the way for EVs” while traditional car companies “talked trash on them all day, every day. But they got it done.”

It’s easy to see why Milton, 38, might want to bill his company as the second coming of Tesla. Nikola’s position is similar to Tesla’s when the electric-car maker started out in the early 2000s: a renegade start-up promoting untried technology to push internal combustion incumbents out of the driver’s seat.

Like Tesla, Nikola also must raise loads of money to fund operations and capital expenses from investors willing to bear year after year of losses.

It’s worked for Tesla: Look at its jaw-dropping stock price. The company has never earned an annual profit, its growth rate is slowing and a viral plague has pushed the world economy into deep recession. Yet Tesla investors remain so optimistic they’ve pushed the stock to almost $900, giving the company a market capitalization of about $162 billion. If you were Milton, wouldn’t you want in on that kind of action?

Both Milton and Musk have become billionaires thanks to new investment dollars flowing into their companies, not on company profits. Nikola’s revenue is negligible, a few hundred thousand dollars a year from engineering contracts. Since its founding in 2015, it has lost a cumulative $188.5 million. Whereas Tesla had debuted a car before its IPO in 2010, the low-production Roadster, Nikola has yet to sell a single truck.

Glory days may lie ahead, but the only trucks either company has to show are prototypes. Both have announced ambitious timelines while raising money and then let the schedules slip. Nikola claims $10 billion worth of “orders” for 14,000 semi trucks, but government filings make clear that those are more like expressions of interest, cancelable, with no deposit money required. Musk says there’s strong demand for the Tesla Semi, but he hasn’t released any order or reservation numbers at all. He also has claimed advances in battery technology that will allow its big-rig haulers to travel 500 miles between charges, but hasn’t yet demonstrated such performance in real life.

Another parallel: Milton and Musk have both been criticized for the way they’ve advanced their own interests during the COVID-19 crisis. Musk restarted production at its Fremont assembly plant May 11, defying orders from the Alameda County public health department.

Milton, meanwhile, was taken to task on CNBC for initially declining requests to return $4 million in federal Paycheck Protection Program forgivable loans meant to help small businesses. This, despite $85 million cash in Nikola’s bank account as of the end of 2019, and with a go-public deal in the works to provide Nikola with $735 million in new capital.

About that deal, consummated Thursday: It was financed by a complicated financial arrangement that avoided a traditional initial public offering, or IPO. Basically, a shell company was created and listed on Nasdaq. That company bought Nikola and folded it into the shell in what’s known as a reverse merger, raising the company’s valuation to $12 billion, up from $3 billion just last fall.

$10 to $93

John Burns Real Estate https://www.linkedin.com/in/johnburns7/

From Capital Group American Funds –Digitization of daily life is here to stay

Some of the recent demand activity reflects an amplification of already established trends. Cloud demand, for example, was sky-high before the COVID-19 outbreak. But the events of 2020 have kicked that theme into overdrive. In the stay-at-home era, e-commerce, mobile payments and video streaming services have soared in popularity, occasionally pushing the limits of technology. While the levels of online activity are likely to moderate, the pandemic could be a catalyst for even stronger e-commerce growth in the years ahead.

“The response to the COVID-19 crisis — keeping everyone at home — has accelerated this powerful trend of digitizing the world,” explains Capital Group portfolio manager Mark Casey, Co-President of Fundamental Investors®.

“Services that were already useful have in some cases become almost essential. Many people felt compelled to try grocery delivery for the first time, for example, and subscriptions to Netflix skyrocketed.”

There’s also room to advance, Casey adds. While e-commerce has grown in popularity, it still represents only about 11% of U.S. retail sales last year, and mobile payments stood at similarly low levels. “Given where we are now in the consumer-technology space, the growth potential is truly exciting.”

U.S. Midyear Outlook: From recession to recovery

https://www.capitalgroup.com/advisor/insights/articles/us-midyear-outlook-2020.html

By Roger Morris

Among the many ways the novel coronavirus outbreak has affected the wine and hospitality industries is the rejuvenation of the 375-milliliter bottle of wine. Easily shippable for virtual tastings and a sensible substitute for by-the-glass service, the small-format bottle is especially suited to pandemic life.

“Most people don’t want to open three or four [standard] bottles of wine at home to do a traditional tasting, so the half bottles have been a very nice alternative,” says Laura Kirk Lee, vice president of sales and marketing for Knights Bridge Winery. “We find that our guests enjoy the opened bottles with dinner after the virtual tasting.”

Rachel Martin, vintner/owner of Oceano Wines, sent half-bottles of her Chardonnay along with recipes and videos as “care packages” to members of The Supper Club in Los Angeles, San Francisco and Austin. “In St Louis, I hosted an Oceano virtual tasting block party where we sent a couple of cases of half bottles to residents, and they distributed them to their friends and family,” she says.

Frank Pagliaro, owner of Frank’s Wine in Wilmington, Delaware, increased his selection of half bottles by 60% to accommodate virtual tastings. Suzie Kukaj-Curovic, director of public relations for Freixenet Mionetto USA, says smaller-format sales have increased, though modestly, at less than 10%.

Will this enthusiasm continue once customers regain greater access to winery tasting rooms and in-store retail tastings?

“We had started offering virtual tastings before Covid-19 because we wanted to stay connected,” says James Blanchard of Blanchard Family Wines. “We’ve been selling a lot of 375s, and I think our virtual tastings will continue for some time.”

Other wineries express similar sentiments about continuing online tastings even after tasting rooms reopen. At a recent webinar sponsored by Silicon Valley Bank, winery consultant Paul Leary emphasized the importance for producers to maintain contacts forged during the pandemic. “The worst thing we can do is to go back to our old ways,” he says. “You now have the opportunity to go directly into the customers’ dining rooms.”

Wines in cans, another 375-ml option, have also grown in popularity during the shutdown. It raises the issue of whether some wineries will see half bottles as a suitable alternative for consumers.

“The question is whether the consumer trend will trade down to value over premium wines, like the previous recession, and what will premium wines do [to] make up sales—reduce price or seek alternate packaging in 375 ml,” says Todd Nelson, director of marketing for Winesellers, Ltd. “I don’t know if this kind of trend to smaller formats will translate very much for the high-end premium.”

Rob McMillan, EVP for the Silicon Valley Bank Wine Division, points out that sales of half-bottles increased 20% in 2019 while standard 750-ml bottles declined slightly. This growth trend continued into the first quarter of 2020. In his annual report, McMillan gave another reason for increased interest in premium 375-ml bottles.

“As boomers retire, they will join millennials as frugal consumers and change their consumption and spending,” he says. “But as any wine lover will tell you, it’s hard to drink good wine and go backward to lesser-quality wine.”

It is still too early for most restaurants, many of which have pivoted to takeout and delivery sales, to reorder wines of any size. Nevertheless, wineries have begun to order additional half bottles for upcoming bottling runs. “We are getting more requests than normal for 375-ml bottles,” says TJ Hauser, president of Hauser Packaging. “It’s too early to tell if wineries are using them as a stopgap for virtual tastings or whether 375s will become a more permanent trend in the industry.”

Jason Haas, Tablas Creek Vineyard partner and general manager, has decided to give the format a second look.

“Before the pandemic, we saw a sustained decrease in the interest in half-bottles, to the point that we’ve been considering eliminating them,” he says. “But for virtual tastings, they’re really ideal. It’s definitely opened up new connection possibilities with our customers, but will people still want to do virtual tastings once they can visit wineries again? Right now, we’re in a holding pattern.”

Instead of eliminating the format, Haas says Tablas Creek will be reordering the same numbers of half-bottles for the next bottling period in case the resurrected interest becomes permanent.

The types of molecules also ranged widely, with some involved in fueling and metabolism, others in immune response, tissue repair or appetite. And within those categories, molecular levels coursed and changed during the hour. Molecules likely to increase inflammation surged early, then dropped, for instance, replaced by others likely to help reduce inflammation.

“It was like a symphony,” says Michael Snyder, the chair of the genetics department at Stanford University and senior author of the study. “First you have the brass section coming in, then the strings, then all the sections joining in.”

Interestingly, though, different people’s blood followed different orchestrations. Those who showed signs of insulin resistance, a driver of diabetes, for instance, tended to show smaller increases in some of the molecules related to healthy blood sugar control and higher increases in molecules involved in inflammation, suggesting that they were somewhat resistant to the general, beneficial effects of exercise. The levels of other molecules ranged considerably in people, depending on their current aerobic fitness.

Over all, the researchers were taken aback by the magnitude of the changes in people’s molecular profiles after exercise, Dr. Snyder says. “I had thought, it’s only about nine minutes of exercise, how much is going to change? A lot, as it turns out.”

This study was small, though, and looked at a single session of aerobic exercise, so cannot tell us anything about the longer-term molecular effects of continued training or of how, precisely, changes in molecular levels subsequently alter health. It also did not include young volunteers under 40.

Dr. Snyder and his colleagues are planning follow-up experiments with more volunteers and sustained exercise programs. They hope to establish whether certain molecular responses to exercise might distinguish people who would benefit from emphasizing resistance exercise over endurance training and whether specific molecular profiles indicate who has higher or lower aerobic endurance. This information could allow physicians and researchers to check fitness with a simple blood draw instead of a treadmill stress test.

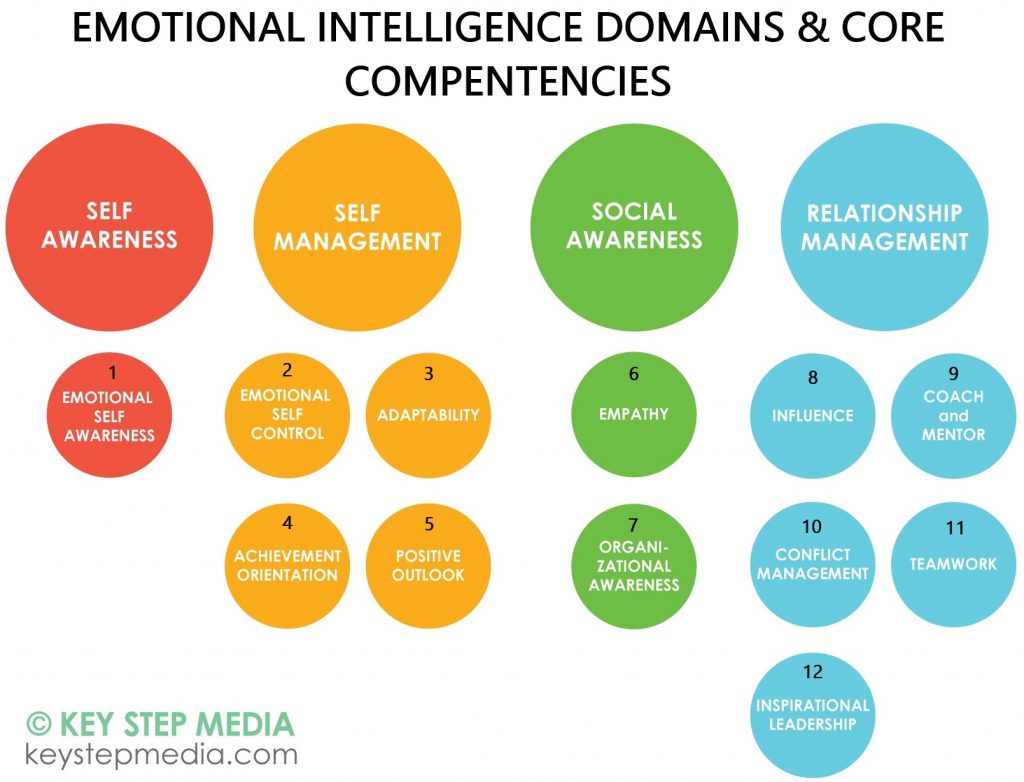

Daniel Goleman, Contributor@DANIELGOLEMANEI

What makes someone great at their job? Having knowledge, smarts and vision, to be sure. But what really distinguishes the world’s most successful leaders is emotional intelligence — or the ability to identify and monitor emotions (of their own and of others).

Companies today are increasingly looking through the lens of emotional intelligence when hiring, promoting and developing their employees. Years of studies show that the more emotional intelligence someone has, the better their performance.

What most people fail to realize, though, is that mastering emotional intelligence doesn’t come naturally. Tom, for example, considers himself an emotionally intelligent person. He’s a well-liked manager who is kind, respectful, nice to be around and sensitive to the needs of others.

And yet, he often wonders, I have all the qualities of emotional intelligence, so why do I still feel stuck in my career?

This is a common trap: Tom is defining emotional intelligence too narrowly. By focusing on his sociability and likability, he loses sight of all other essential emotional intelligence traits he may be lacking — ones that can make him a stronger, more effective leader.

After spending 25 years writing books and fostering research on this topic, I’ve found that emotional intelligence is comprised of four domains. And nested within these domains are 12 core competencies.

(Click here to enlarge chart)

Don’t shortchange your development by assuming that emotional intelligence is all about being sweet and chipper. By reviewing the competencies below and doing an honest assessment of your strengths and weaknesses, you can better identify where there’s room to grow.

1. Self-awareness

Self-awareness is the capacity to tune into your own emotions. It allows you to know what you are feeling and why, as well as how those feelings help or hurt what you’re trying to do.

Do you have the core competency of self-awareness?

Developing the skills:

Every moment is an opportunity to practice self-awareness. One of the biggest keys is to acknowledge your weaknesses. If you’re struggling with something at work, for example, be honest about the skills you need to work on in order to succeed.

Be conscious of the situations and events in your life, too. During times of frustration, pinpoint the root and cause of your frustration. Think about any signals that accompany how you feel in that moment.

2. Self-management

Self-management is the ability to keep disruptive emotions and impulses under control. This is a powerful skill for leaders, especially during a crisis — because will people look to them for reassurance, and if their leader is calm, they can be, too.

What core competencies of self-management do you have?

Developing the skills:

During moments of distress, do not brood or panic. Take a deep breath and check in with your emotions. Instead of blowing up at people, let them know what’s wrong and offer some solutions.

Accept that there will always be sudden changes and challenges in life. Try to understand the context of the given situation and adjust your strategy or priorities based on what is most important at the time.

3. Social awareness

Social awareness indicates accuracy in reading and interpreting other people’s emotions, often through non-verbal cues. Socially aware leaders are able to relate to many different types of people, listen attentively and communicate effectively.

What core competencies of social awareness do you have?

Developing the skills:

First and foremost, social awareness requires good listening skills. Do not talk over someone else or try to hijack the agenda. Ask questions and invite others to do the same.

Challenging your prejudices and discovering commonalities is also key. Practice putting yourself in other people’s shoes. When we do this, we are often more sensitive to what that person is experiencing and are less likely to tease, judge or bully them.

4. Relationship management

Relationship management is an interpersonal skill set that allows one to act in ways that motivate, inspire and harmonize with others, while also maintaining important relationships.

Which core competencies of relationship management do you have?

Developing the skills:

If you’re a constantly negative person, you’ll have a very difficult time managing long-term relationships. Instead of focusing on “the worst that can happen,” try to see yourself as an agent of positive change.

Don’t be afraid to go against the grain of conventional norms or take risks, either. These kinds of people ultimately leave the people they work with feeling inspired, motivated and connected.

Daniel Goleman is a psychologist and best-selling author of “Emotional Intelligence” and “Social Intelligence.” His latest book is “What Makes a Leader: Why Emotional Intelligence Matters.” Daniel received his PhD in psychology and personality development from Harvard University. His work has appeared in The New York Times and Harvard Business Review. Follow him on Twitter @DanielGolemanEI.

Disclaimer

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania..

To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results.

Material compiled by Lansing Street Advisors is based on publically available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data.

Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only