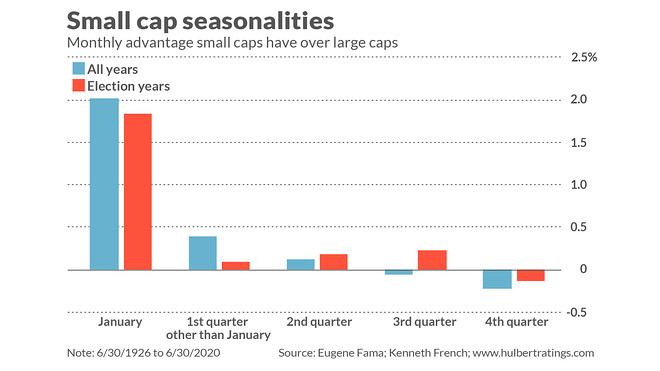

1. Small Caps Lag In 4th Quarter

Now is not a good time to be actively investing in small-cap U.S. stocks. That’s because small-caps typically lag their larger counterparts during the fourth quarter.

Take a look at the accompanying chart, which plots the average monthly return advantage that the smallest stocks have over the largest. (The exact definitions of these two hypothetical portfolios are provided on the website maintained by Dartmouth College professor Ken French.)