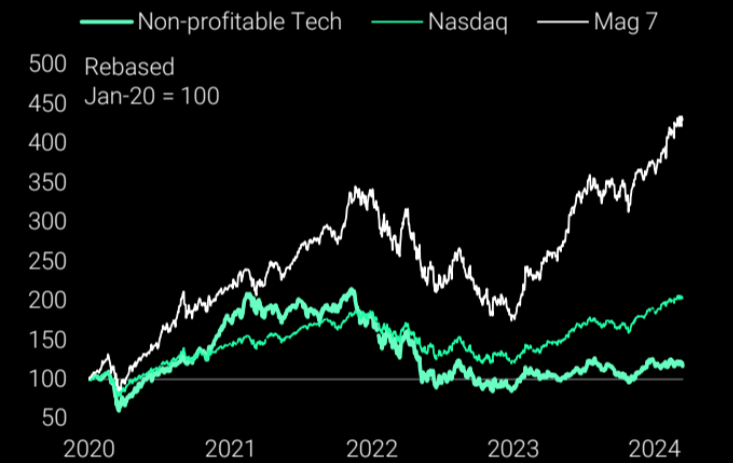

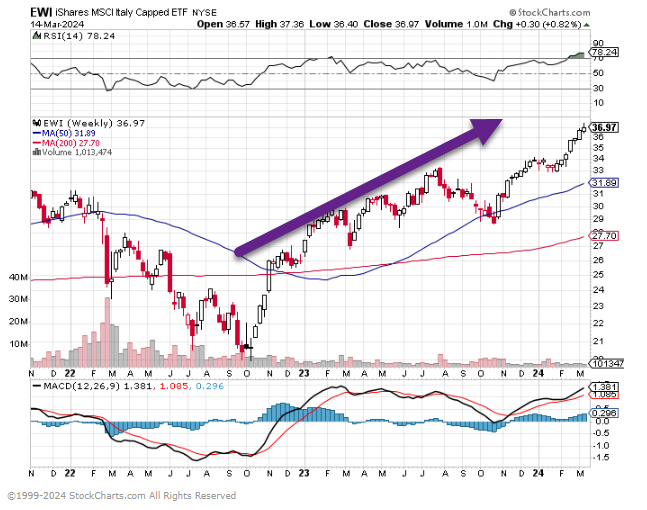

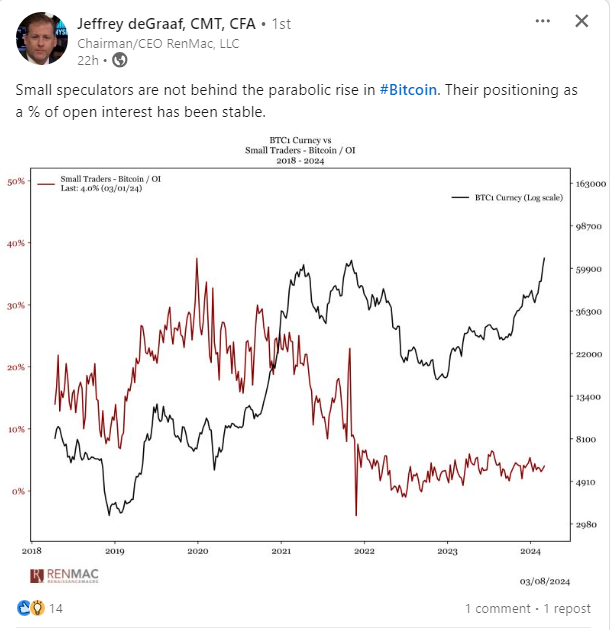

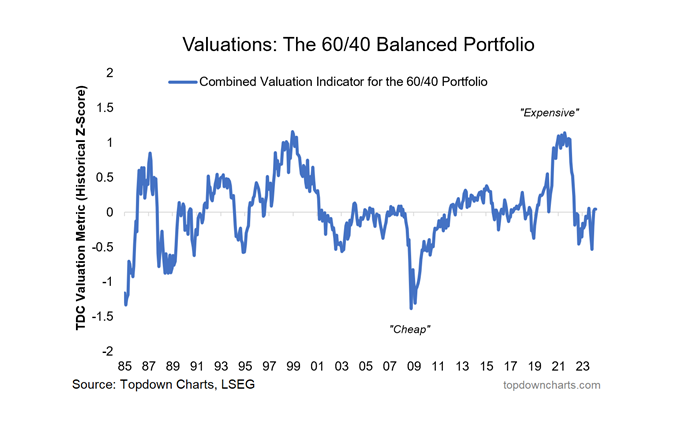

2.The Price Between Puts and Calls has Narrowed to Historic Low.

From Dave Lutz Jones Trading A closely-watched gauge of stock market sentiment has hit its most extreme level since 2008, as options traders increasingly focus on capturing further gains in soaring indices rather than worrying about a potential sell-off – Investors are so bullish that “fear of a crash-up” now trumps “any meaningful concern of a correction lower,” said Charlie McElligott, managing director of cross-asset strategy at Nomura, who wrote in a note to clients this week that markets “are foaming at the mouth, FT reports.

5.Copper Rally-Analysts Pointing Out Copper Rally as Positive Tell for China/International?

Copper Contract Rallying to 2023 Levels.

Copper Miners are Making Run at All-Time Highs.

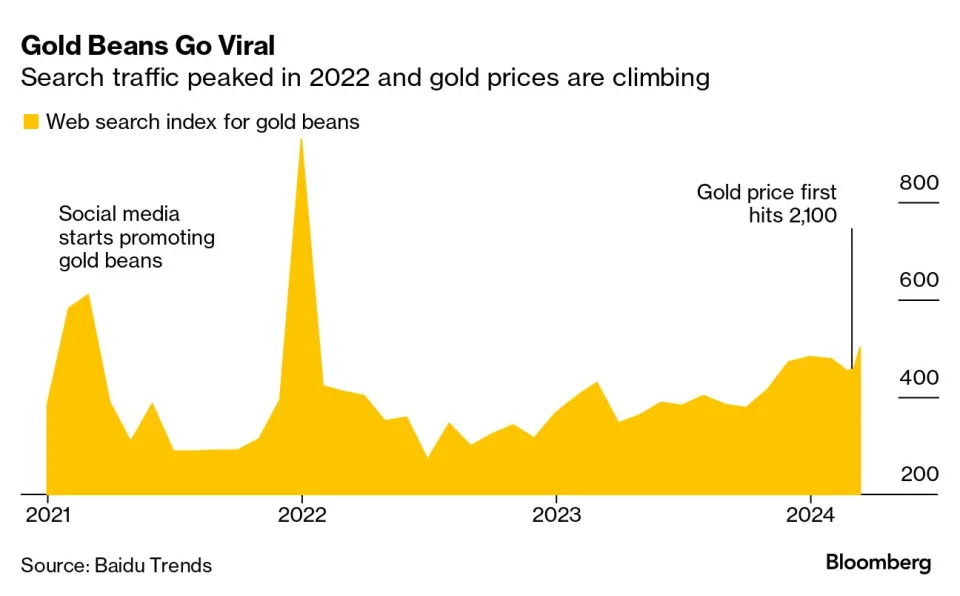

6.Meanwhile Chinese Young People are Loading Up on Gold.

Gold Beans All the Rage With China’s Gen Z as Deflation Bites

Bloomberg News

(Bloomberg) — With China’s deflation at its worst in 15 years, a volatile stock market and bank interest rates too low for her liking, 18-year-old Tina Hong is placing her financial security in gold beans.

Weighing as little as one gram, the beans — and other forms of gold jewelry — are increasingly viewed as the safest investment bet for young Chinese in an era of economic uncertainty. It’s part of a larger consumer trend for all things gold — from bullion to beans and bracelets — that has gripped the mainland.

“It’s basically impossible to lose money from buying gold,” reasoned Hong, a college freshman studying computer science in Fujian province who in January began buying gold beans because of their relatively low cost of about 600 yuan ($83) per gram. She has more than two grams of the beans and will continue buying them as long as costs are lower than international gold prices, she said.

Branded as an investment entry point for young consumers, the beans, which come in glass jars, are the latest hot-selling items in Chinese jewelry stores. Generation Z consumers — buffeted by high youth unemployment and the nation’s slide into deflation — are now among the top consumers of gold accessories in the world’s second-largest economy, according to the 2023 China Jewelry Consumer Trends Report by Chow Tai Fook Jewelery Group Ltd. The attraction of gold comes as people pull back on shopping amid months of disappointing growth.

China Gold Rush

A lack of faith in traditional investments has fueled this new China gold rush.

“Starlink Mission” (CC BY-NC 2.0) by Official SpaceX Photos

SpaceX CEO and terminally online memelord Elon Musk is becoming an increasingly vital figure in the US defense system.

The company that’s been in the news lately for its moonbound megarocket was awarded a $1.8 billion contract in 2021 to build a spy network of hundreds of Starshield satellites for the National Reconnaissance Office, Reuters reported over the weekend. The low-Earth orbit satellites would support ground forces and enhance the ability of the US to locate targets globally.

The SpaceX partnership reflects the US’ urgent efforts to win the latest iteration of the space race.

China announced plans earlier this month to create its own constellation of low-orbit satellites to compete with Starlink.

US intelligence officials warned in February that Russia is developing a nuclear space weapon capable of destroying satellites.

Musk’s satellites have been a geopolitical football: Ukraine has claimed that Russia is using thousands of Musk’s Starlink satellite terminals to gain a tactical advantage during its invasion, starting a squabble with the Biden administration. Starlink, however, is a separate entity from Starshield, which is designed for military or government uses.

Go down the rabbit hole: The New Yorker dug into the US government’s reliance on Musk for national security.—DL

“It’s easier to get a smart person to do something hard than to get them to do something easy that doesn’t matter.”

**

“When you know what needs to be done, inaction increases stress. You feel a lot less stress when you do the things within your control that move you closer to your objective. Action reduces stress.”

***

“A lack of routine causes more problems than poor choices. Routines turn desired behavior into default behavior.”

The Berachain blockchain platform is becoming a unicorn in a more than $69 million funding round co-led by Brevan Howard Digital and Framework Ventures, according to people familiar with the matter.

The project, which is raising the money by selling digital tokens, will be valued at $1.5 billion, the people said, asking not to be identified discussing private information. Berachain focuses on decentralized finance, or DeFi, which enables trading, lending and borrowing without the use of traditional intermediaries like banks.

Berachain is one of the first crypto projects to achieve unicorn status — a valuation of at least $1 billion — in the current digital-asset bull run marked by record highs for Bitcoin. The fundraising signals venture capital investors are becoming more interested in crypto companies after deals collapsed last year.

Both Brevan Howard Digital and Framework Ventures declined to comment. Berachain didn’t immediately respond to a request for comment.

ARE YOU READY TO swap your office chair for a rocking chair? Hold that thought.

Before you dive into the world of endless vacations and gardening, consider that keeping a toe—and perhaps your whole foot—in the workforce might be the secret ingredient to a fulfilling retirement. Don’t believe me? Here are seven compelling reasons to keep working at least part-time.

1. Stay young at heart. Remember the excitement of landing your first job? That thrill doesn’t have to end. Continuing to work, even part-time, keeps your brain active and challenged. It’s like a gym membership for your mind, warding off the cobwebs and keeping you mentally sharp. Learning new skills and adapting to new environments can be the fountain of youth for your brain.

2. Social butterflies keep fluttering. One often-forgotten benefit of work is the social connections. Picture this: engaging conversations by the water cooler, team lunches, and the camaraderie of working toward a common goal. These interactions are invaluable and keep you connected to diverse groups of people, ensuring that your social life remains vibrant and dynamic.

3. Even more financial freedom. Who doesn’t love an extra bit of cash? Continuing to work means more financial breathing room. You can fund those dream vacations, spoil the grandkids or simply enjoy the peace of mind that comes with a steady income. It’s not just about the money. It’s about the freedom and choices that money can provide.

4. Purpose, passion and pride. Work can be a significant source of all three. Whether you’re mentoring younger colleagues, contributing to meaningful projects or just being part of a team, these experiences validate your skills and experience. It’s about feeling valued and knowing you’re making a difference.

5. Keep the doctors at bay. Believe it or not, working can be good for your health. Studies suggest that those who continue working tend to enjoy better mental and physical health. The combination of mental stimulation, social interaction and a sense of purpose creates a powerful health cocktail.

6. Flexibility is the new black. Retirement doesn’t have to be all or nothing. Many retirees find joy in flexible work arrangements like part-time jobs, consulting or freelance gigs. This flexibility allows you to balance work with leisure, family time and hobbies. With the right job, you get to design your golden years exactly how you want them.

7. The joy of lifelong learning. Ever wanted to try a completely different career or learn a new skill? Now’s your chance. Retirement can be the perfect time to explore new interests or passions in a low-pressure environment. Who says you can’t be an intern at age 60 or start a new venture at 70?

Bottom line: It’s your adventure. Retirement is a journey, not a destination. By incorporating work into your retirement plan, you’re not just adding years to your life—you’re adding life to your years. It’s about finding the right balance that makes you jump out of bed each morning, excited for the day ahead. So, what will your retirement adventure look like?

Dan Haylett is a financial planner and head of growth at TFP Financial Planning, a U.K. firm that specializes in modern-day retirement planning. Dan’s “pull back the duvet every morning” purpose is helping clients spend their time and money on what’s truly important to them.A version of the above article first appeared on Dan’s website, where you can also learn about his Humans vs. Retirement podcast. Follow him on X (Twitter) @DanHaylett. Dan’s previous article was The Changes Ahead.

5. Grayscale files plans for ‘mini’ bitcoin fund, two months after GBTC’s conversion to ETF

Marketwatch Christine Idzelis Grayscale Bitcoin Trust is the largest spot bitcoin ETF, but it’s been losing assets amid competition from cheaper rival funds

Grayscale Investments is planning a second exchange-traded fund tracking spot bitcoin prices, just two months after the firm’s flagship Grayscale Bitcoin Trust converted to an ETF, according to a regulatory filing. The Grayscale Bitcoin Mini Trust will trade under the ticker “BTC,” according to a filing Tuesday with the Securities and Exchange Commission. The firm has proposed spinning off part of its large Grayscale Bitcoin Trust GBTC, which trades under the symbol “GBTC,” to seed the new ETF, the filing shows. The “mini” bitcoin ETF’s fees were not disclosed in the SEC document. Mini versions of large funds elsewhere in the ETF industry charge lower fees than their flagship versions, as they aim to appeal to buy-and-hold investors rather than big institutions. The Grayscale Bitcoin Trust has seen billions of dollars in outflows since its conversion to an ETF on Jan. 11, the same day that less expensive spot bitcoin ETFs also began trading. Rival funds with lower costs than the Grayscale Bitcoin Trust’s 1.5% expense ratio have been attracting assets, including ETFs managed by BlackRock and Fidelity.

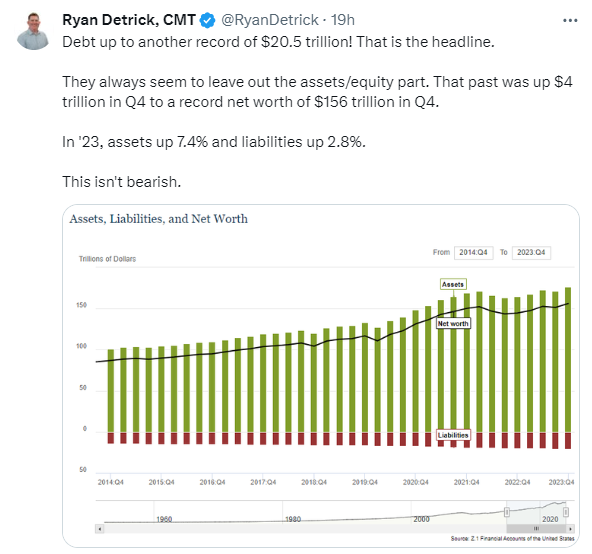

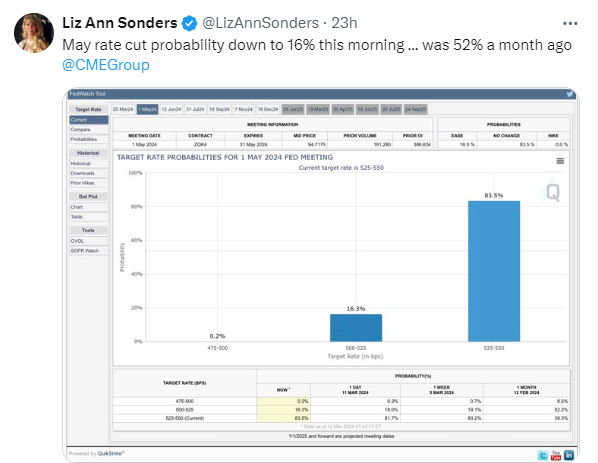

Dave Lutz Jones Trading For the world, it’ll represent closure to the era of negative rates, a radical policymaking approach that was also adopted by the European Central Bank and some continental peers in their battles against falling prices in the 2010s.

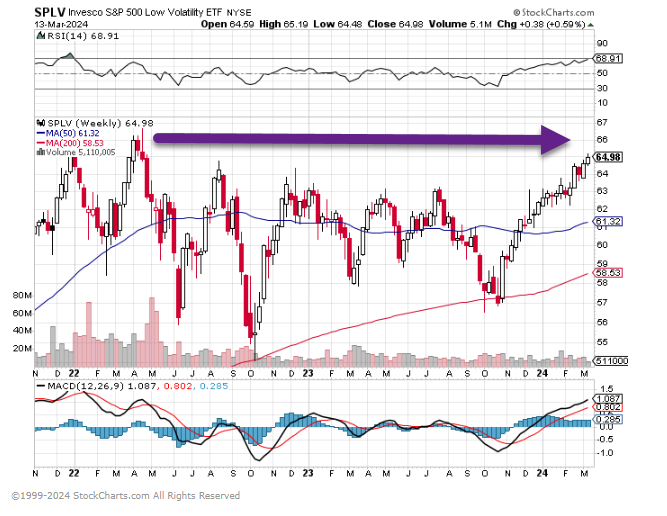

8. Will We See Rotation to More Value/Defensive Groups?

Low Volatility ETF still has not made new highs.

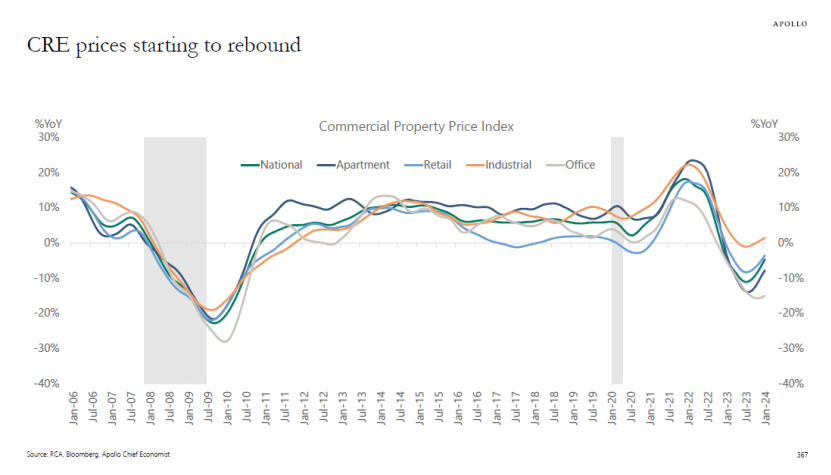

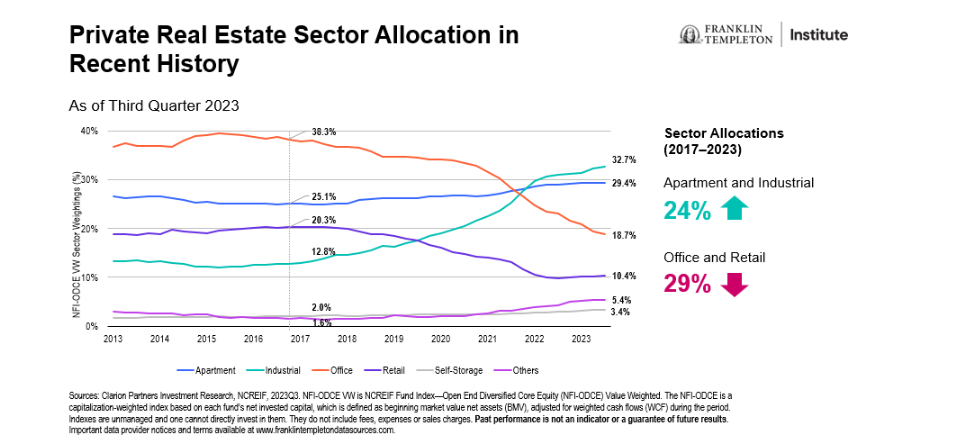

9. Commercial Real Estate Prices Starting to Recover

Torsten Slok, Ph.D.Chief Economist, Partner With no signs of a recession, commercial real estate prices are starting to recover, see chart below. This is helpful for the regional banks and for the broader economic recovery.

10. 6 Signs That You’re Stuck in a Negative Narrative

Psychology Today Steven C. Hayes, Ph.D. How to overcome the story of “not good enough.” KEY POINTS

The stories you tell yourself about yourself shape how you think, feel, and act.

However, more than what you think, it matters how you react to your own thinking.

By holding your thoughts lightly, you can notice that these are just stories.

Pay attention to these six signs, and practice holding your beliefs with more lightness and flexibility.

What you think about yourself and the world around you tremendously affects your life and overall well-being. For instance, if you think you are worthy of love and capable of confronting and overcoming life’s challenges, you are more likely to act in ways that confirm these thoughts. On the other hand, if you think the opposite is true—that you’re unworthy and incompetent—odds are you will act in alignment with those as well. The stories you tell yourself about yourself (that is, what you believe about yourself), shape how you think, feel, and act.

However, this is only part of the truth and maybe not even the biggest part. Because more than what you think, it matters how you react to your own thinking. For instance, you might think, “I will never be good enough.” But you are kind, caring, and compassionate towards yourself. It’s possible! And you know that because if you look more closely at your experience, negative thoughts don’t always land in the same way. Sometimes therapists use the term belief to talk about thoughts that are implicitly adopted and are then complied with, or fought with—and from that point of view, the real action is not what you think so much as what you believe. In my own work, we usually say people are fused with these thoughts, or that they become entangled with these thoughts, but I’ll practice what I’m preaching here and in this post, I’ll use the term belief to refer to thoughts that are adopted as a basis of action. (Settle down Steve, this ain’t gonna kill you!)

By holding your thoughts lightly, you can notice that these are just stories your mind tells you about yourself. And even though they feel true (or sometimes even are objectively true), they don’t have to dominate your life. Thoughts are just thoughts, they don’t hold power over you unless you get caught up in them.

This is often easier said than done, because we all hold onto beliefs about ourselves that seem as self-evident as the fact that fire is hot, or that water makes things wet. And much too often, we don’t even realize when we’re in the grip of our own beliefs, unable to distinguish them from what is while letting ourselves be guided by them in unhelpful or self-destructive ways. For this reason, it’s important to learn how to notice when we’re stuck in a narrative that negatively affects our lives. Looking out for the following six signs may help.

Sign #1 Overidentification With Labels

The human mind is a master at categorizing. We give names to all the birds in the sky, all the fish in the sea, and literally everything else, because it helps us make sense of the world and allows us to make better decisions that ensure our survival. Scriptural stories note how powerful this is (for example, Genesis 2: 18-20) but so do science and practical experience. For instance, if someone shouts “tiger,” we don’t need to see the animal ourselves to know that we better start running. But as useful as this ability can be, it can also turn on us, especially when we apply it to ourselves. Words can never capture the true complexity of life, and instead reduce everything to a mere label. And when we forget this fact, which we quite often do, we mistake the label for the real thing. We then reduce ourselves to being our job, to our role within our family, to a slur somebody once called us, to a mental health diagnosis we once received, and so on. We are then no longer a living being of unfathomable complexity, but we are “a janitor,” “a mom,” “a loser,” or just “depressed.” The first sign that we’re stuck in a narrative is that we overly identify with such labels.

Sign #2 Repetition of Negative Patterns

Few habits always have “good” or “bad” results, their usefulness depends on the circumstances. Take a process such as shutting down your deepest feelings. That process is a lousy basis for a fruitful relationship, but learning how to do that for short periods can be essential if you’re working as a first responder. Similar action, different context. article continues after advertisement That said, if you repeatedly engage in unhelpful habits, see if you aren’t stuck in an unhelpful narrative. Despite what your mind may tell you about how you “have to” do what it says, it may be time to break its grip.

Sign #3 Blaming External Factors

Often, there are real forces holding people back in life; especially in a world that struggles to treat everyone with respect and dignity. But life also asks us to look at our own lives and discern what is within our ability to change. If all you see are external reasons to blame for your misery, see whether you are stuck in a negative narrative. There are always some aspects within our control, even if it’s just our own perspective. By taking responsibility for ourselves, and making active choices in alignment with our goals and values, we are likely to move the needle in a better direction—step by step.

Sign #4 Difficulty Letting Go

Some experiences have such a strong impact, that they continue to haunt you long after they have passed. Maybe someone hurt you in a devastating way, and although you no longer speak to that person, their image and words still echo in your memories. And whenever you remember, and wrestle with that memory, you might feel your heart beating faster and your body tensing up. Again and again, you feel compelled to engage with that memory, imagining things going differently, and hoping to find a solution or even closure, which will never come. Learning to let go can be hard, seemingly impossible even, especially if you can still feel the pain. And if you were to let go, you might have to let the people who have wronged you off the hook. But letting go is not about other people; it’s about being kind and compassionate towards yourself. It’s about noticing the toll this endless fighting has on you, and with patience and kindness reclaiming your focus and pulling it away from the itching wound and instead on the things you care deeply about.

Sign #5 Consistent Negative Self-Talk

Most of us tend to speak to ourselves in a manner we would rarely, if ever, use when talking to our friends and loved ones. We are then harsh in our judgments, and quick to punish ourselves with critical insults: “How could I be so stupid?!” “I’m a disappointment.” “I’ll never get it right.” And so on. This is often an automatic process, and we do it so quickly and naturally that we hardly ever notice it, let alone how it’s affecting our well-being. You might have been led to believe that you need to be strict with yourself so that you stop messing up. But what does your experience tell you about how well that works? If you’re being honest with yourself, you likely agree that this approach didn’t deliver the promised results. You are not a horse to be whipped, you are instead deserving of kindness, patience, and compassion—especially when you make a mistake or when you are vulnerable. Changing your inner monologue requires active practice, but you can develop a more caring tone in time.

Sign #6 Unwillingness to Consider Alternatives

When we’re stuck in a negative narrative, life appears very much one-sided. Our vision gets closed down, and we become convinced that reality is just as our mind tells us it is. This is relatively easy to spot in other people, but it is much harder to notice the impact of beliefs on ourselves. When we wear red-tinted glasses, we don’t see our glasses; instead, we see the world as red. As a result, we feel compelled to act as if the world were red, not realizing that different views and perceptions are available, ones that are just as valid. article continues after advertisement

If we’re overly concerned about our looks, we may perceive a romantic rejection as proof of our physical inadequacies. We do not notice that it may have nothing to do with ourselves. When we become stressed about all the chores we must do on any given day, we may overlook the fact that not doing them is also an option. There are always different points of view available, some of which are more empowering than others. And by noticing the stories our mind tells us about ourselves, we can more consciously choose which we will ascribe to and which we will let go. In effect, we may not be able to choose our thoughts but we can choose our beliefs. ___ The narratives we tell ourselves about ourselves, and the world we live in, have a powerful impact on our mental well-being especially when we believe them. By consciously noticing these narratives – a skill you can practice in your daily life – you can learn to choose how to engage with them: whether you want to let them drive your actions or acknowledge their presence without being dictated by their demands. It’s a matter of continuously training your awareness. And whenever you get sucked back in, you can consciously refocus on what matters to you. Again and again.

Pay attention to these six signs, and practice holding your beliefs with more lightness and flexibility. You soon notice it will help you make new, better choices.

Found at Dollar and Cents Blog Joe Weisenthal summarized the atmosphere of the current crypto environment beautifully in the Bloomberg Markets newsletter last week: All that being said, there is something about this upturn that’s a little bit different than in the past. Typically there’s some sort of story or pretense that rides alongside the price. In 2021 there was a lot of talk about “DeFi” and how the various chains had the opportunity to disintermediate finance in some novel way. Other things in past cycles you heard about where how gaming would all go on chain, with people being able to own their own characters or their character skins or whatnot. Tokens were going to replace frequent flyer miles. Ethereum was going to be the new World Computer. Real-world assets would all be tokenized, creating smoother more liquid markets for various things that are currently hard to trade. None of this has panned out so far. At all. But not only has none of this panned out, there’s not some new “fundamental” story that’s being told about this rally. There’s not some new crypto use case that people are excited about that wasn’t being talked about 3 years ago. The only thing people are talking about really is flows. There’s the new inflows from the ETFs.

10. How to Build a High-Performance Leadership Team

From INC.com

As a leader, you set the tone for your leadership team.

EXPERT OPINION BY DAVID FINKEL, CO-AUTHOR OF ‘SCALE: SEVEN PROVEN PRINCIPLES TO GROW YOUR BUSINESS AND GET YOUR LIFE BACK’ @DAVIDFINKEL In today’s rapidly changing business landscape, the success of an organization depends heavily on the strength of its leadership team. A high-performance leadership team can drive innovation, foster a positive workplace culture, and guide the company toward its strategic goals. However, building such a team is not without its challenges. Here are some essential tips for creating and nurturing a high-performance leadership team. 1. Define Clear Roles and Responsibilities One of the fundamental building blocks of a high-performance leadership team is clarity regarding each member’s roles and responsibilities. Ambiguity and overlapping duties can lead to confusion and inefficiency. Start by defining specific roles and expectations for each team member. Make sure everyone understands their unique contributions and how they fit into the larger team structure. 2. Cultivate Diversity Diversity within your leadership team can be a powerful asset. A group of individuals with different backgrounds, perspectives, and skill sets can bring a broader range of ideas and approaches to problem-solving. Encourage diversity in terms of gender, ethnicity, age, and professional experiences. Embrace the value that diverse viewpoints can bring to your team’s decision-making process. 3. Nurture Effective Communication Open and transparent communication is the lifeblood of any successful leadership team. Foster an environment where team members feel comfortable sharing their thoughts, concerns, and feedback. Encourage active listening and respectful dialogue during meetings. Effective communication enables leaders to align their efforts, make informed decisions, and resolve conflicts constructively. 4. Lead by Example As a leader, you set the tone for your leadership team. Demonstrate the qualities and behaviors you expect from your team members. Lead with integrity, accountability, and a strong work ethic. Your actions will influence the team’s culture and inspire them to strive for excellence. 5. Foster Trust and Collaboration Trust is a cornerstone of high-performance teams. Create an atmosphere of trust by honoring commitments, being consistent in your actions, and valuing each team member’s contributions. Encourage collaboration by facilitating teamwork, joint problem-solving, and cross-functional initiatives. When team members trust one another, they are more likely to collaborate effectively. 6. Invest in Professional Development High-performing leadership teams are committed to continuous growth and learning. Invest in the professional development of your team members by providing access to training, workshops, and leadership programs. Equip them with the skills and knowledge needed to stay ahead in an ever-evolving business landscape. 7. Set Ambitious Goals Challenge your leadership team by setting ambitious yet achievable goals. Well-defined objectives provide a clear sense of purpose and direction. Encourage your team to embrace these goals and work collectively to attain them. Celebrate achievements along the way to maintain motivation and momentum. 8. Emphasize Accountability Accountability is vital for the success of any high-performance team. Ensure that team members take ownership of their responsibilities and deliver results as promised. Establish a system of accountability that holds individuals and the team as a whole responsible for meeting performance expectations. 9. Promote a Growth Mindset Encourage a growth mindset within your leadership team. Emphasize the importance of learning from failures and viewing challenges as opportunities for growth. A growth mindset fosters resilience and innovation, enabling your team to adapt to changing circumstances effectively. 10. Regularly Evaluate and Adjust Building a high-performance leadership team is an ongoing process. Regularly assess the team’s performance, strengths, and areas for improvement. Adjust your strategies and goals as needed to ensure that your team remains adaptable and responsive to the organization’s evolving needs. A high-performance leadership team is the backbone of a successful organization. By following these tips and investing in the development of your team, you can create a cohesive and effective group of leaders. Remember that building and nurturing a high-performance team is a continuous journey that requires dedication, communication, and a commitment to excellence. With the right approach, your leadership team can help your organization thrive in today’s competitive business environment. Now accepting applications for Inc.’s Best Workplace awards. Apply by February 16 for your chance to be featured! The opinions expressed here by Inc.com columnists are their own, not those of Inc.com. How to Build a High-Performance Leadership Team | Inc.com

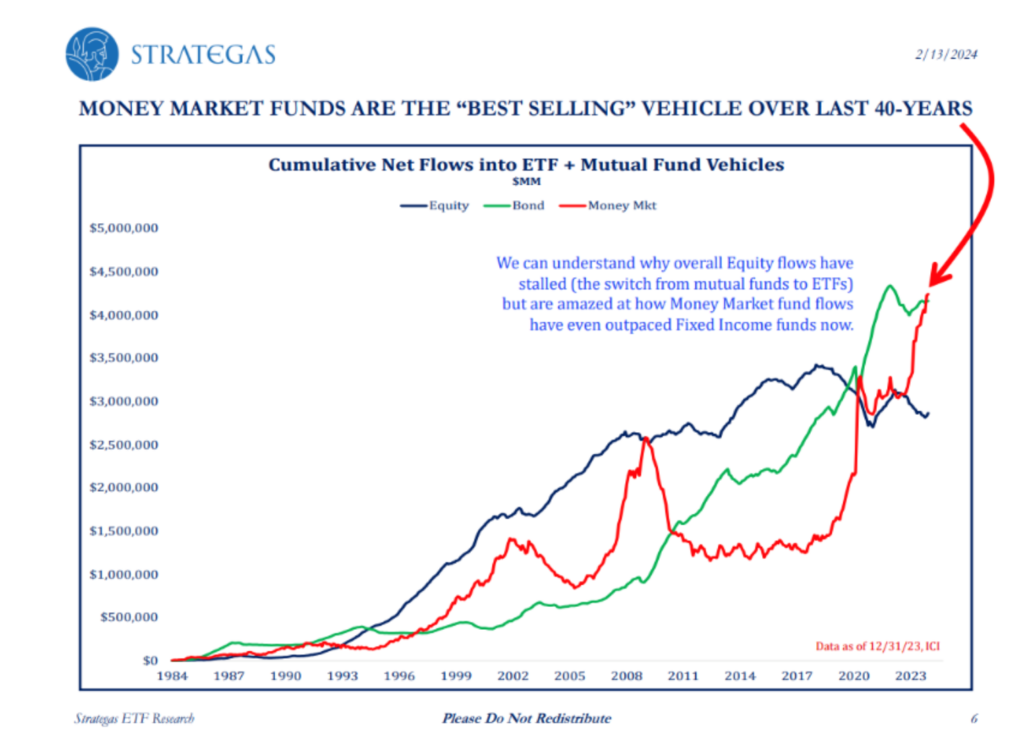

6. The Best Selling Investment Vehicle of 40 Years is Money Market Fund

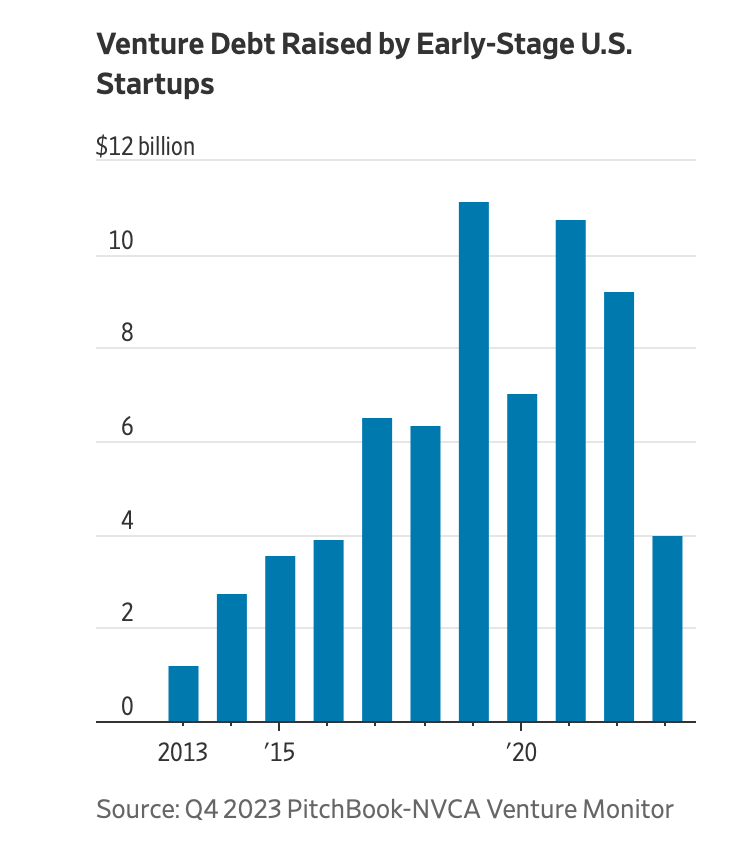

7. Venture Funding Down -50-60%

Pitchbook-Debt funding to early-stage startups, referring to companies at the Series A and B stages, plunged almost 57% to about $4 billion in 2023, while funding to seed and pre-seed startups shrank about 59% to just $610,000, according to PitchBook-NVCA.

9. Boomers Are Expected To Pass $90 Trillion In Assets Onto Millennials — Leaving Them To Become The ‘Richest Generation In History’

Jeannine Mancini-Yahoo Finance

In an unprecedented financial shift, millennials are on the cusp of becoming the richest generation in history, with $90 trillion expected to be passed down to them over the next two decades. This transfer of wealth, highlighted in Knight Frank’s 2024 Wealth Report, promises to reshape the economic landscape and alter the current power dynamics heavily influenced by the baby boomer generation. The report, drawing on recent findings, forecasts a seismic change in the distribution of wealth, with millennials positioned to inherit assets that will significantly elevate their financial standing. This generational wealth transfer is not merely a redistribution of existing wealth but signals a broader transformation in the avenues for wealth creation. As highlighted by Mike Pickett, a director at Cazenove Capital, the diversity of opportunities for generating wealth has expanded, encompassing everything from digital platforms to entrepreneurial ventures, marking a shift towards first-generation wealth creation. Don’t Miss:

Investing in real estate just got a whole lot simpler. This Jeff Bezos-backed startup will allow you to become a landlord in just 10 minutes, and you only need $100.

Despite this optimistic outlook, the journey to financial prosperity has been fraught with challenges for millennials. Many have grappled with an increasingly unattainable housing market, a competitive job landscape reshaped by the global pandemic and the burden of student debt. Additionally, the anticipation of inheritance reveals a gap in expectations, with a significant portion of millennials expecting a larger inheritance than their boomer parents plan to leave. The focus on housing remains a critical concern for millennials struggling to secure a foothold in the property market. This challenge extends to ultra-high-net-worth individuals within the generation, underscoring the importance of real estate as a key area of investment. The report indicates a keen interest among affluent millennials, both male and female, in expanding their property portfolios in the coming year, mirroring a similar sentiment among wealthy Gen Zers. The Knight Frank report also sheds light on the increasing number of ultra-high-net-worth individuals globally, projecting a significant rise in their numbers, particularly in India and mainland China. This growth underscores the expanding landscape of wealth and the critical role of the financial sector in catering to the needs of an increasingly affluent millennial cohort. As millennials stand on the brink of a historic wealth influx, the report calls on the financial sector to adapt its services to meet the unique needs and preferences of this generation. This adaptation is crucial for managing the wealth accumulated during the pandemic and for supporting the diverse and innovative paths millennials are taking toward financial independence and wealth creation.

Last November, Michael Morell, a former deputy director of the Central Intelligence Agency, hinted at a big change in how the agency now operates. “The information that is available commercially would kind of knock your socks off,” Morell said in an appearance on the NatSecTech podcast. “If we collected it using traditional intelligence methods, it would be top secret-sensitive. And you wouldn’t put it in a database, you’d keep it in a safe.”

In recent years, U.S. intelligence agencies, the military and even local police departments have gained access to enormous amounts of data through shadowy arrangements with brokers and aggregators. Everything from basic biographical information to consumer preferences to precise hour-by-hour movements can be obtained by government agencies without a warrant.

Most of this data is first collected by commercial entities as part of doing business. Companies acquire consumer names and addresses to ship goods and sell services. They acquire consumer preference data from loyalty programs, purchase history or online search queries. They get geolocation data when they build mobile apps or install roadside safety systems in cars.

But once consumers agree to share information with a corporation, they have no way to monitor what happens to it after it is collected. Many corporations have relationships with data brokers and sell or trade information about their customers. And governments have come to realize that such corporate data not only offers a rich trove of valuable information but is available for sale in bulk.