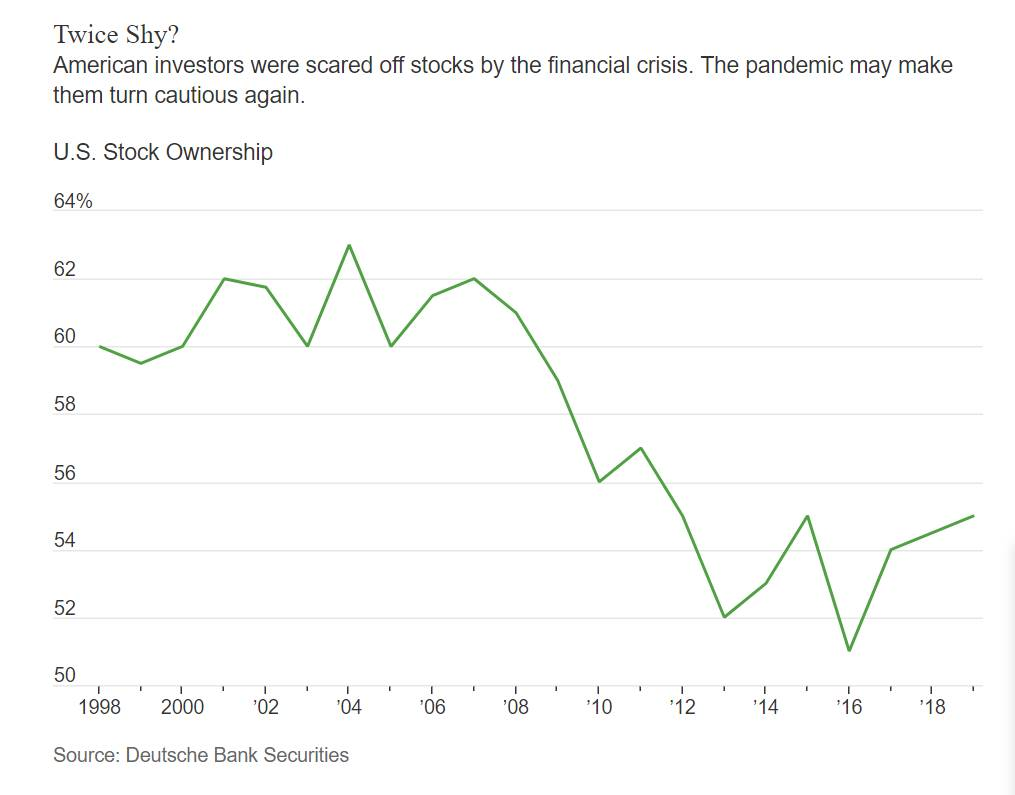

1.Stock Ownership by American Investors Never Came Close to Recovering to 2000 and 2008 Levels

Barrons

Get Ready for a PostCoronavirus World. The Economy Will Never Be the Same.–By Reshma Kapadia

Continue readingBarrons

Get Ready for a PostCoronavirus World. The Economy Will Never Be the Same.–By Reshma Kapadia

Continue reading

https://www.latimes.com/business/story/2019-08-16/tsa-airport-security-wait-times-drop-lax-analysis

Continue reading

https://money.cnn.com/quote/etf/etf.html?symb=IWM

Continue readingMax Gains During Bear Market

https://www.ssga.com/us/en/institutional/etfs

Continue readingThe Black Swan Has Landed–April 1, 2020–Matt Topley

Money talks

But it doesn’t sing and dance and it don’t walk

And long as I can have you here with me

I’d much rather be forever in blue jeansHoney’s sweet

But it isn’t nothing’ next to baby’s treat

And if you’d pardon me, I’d like to say

We’d do okay forever in blue jeans

Neil Diamond https://www.azlyrics.com/lyrics/neildiamond/foreverinbluejeans.html

Money talks but it can’t sing, it can’t dance and it can’t walk. Pop star, Neil Diamond, understood this long before the coronavirus put our lives on hold. But the plan the Fed and Congress put in place to rain money everywhere will hopefully allow us to sing, dance and walk until this crisis is over.

First, my thoughts and prayers go out to everyone impacted by the pandemic, especially patients and all the brave medical personnel on the front lines. In this new reality, it may seem like working from home in blue jeans is going to last forever; it won’t. We’ll eventually get back to normal, but I believe Congress won’t be able to bail out corporations as easily today as it did with banks, airlines and cruise lines during the 2008-09 global financial crisis. It is my opinion that taxpayers and voters won’t put up with airlines spending 96 percent of their free cash flow on stock buybacks and they won’t tolerate helping “American” cruise lines stay afloat, when those companies—domiciled offshore– pay almost no U.S. taxes.

When we got through the global financial crisis in 2009, I was emotionally exhausted. But I consoled myself with the fact that it would be at least a quarter of a century before we’d have to live through volatility like that again. But here we are, barely a decade later, and it’s déjà vu all over again. Just a few weeks ago, we had a perfect storm of plummeting stocks, plunging oil prices and rock bottom interest rates all at the same time. This perfect storm caused the worst liquidity crisis since 2008. At one point there was a bid/offer spread of 100 basis points on U.S. Treasuries, leaving the rest of the bond market frozen. An entire frightening week went by in which no corporation could borrow money in the credit markets.

Meanwhile, the stock market saw the fastest 30 percent drop in history. In fact, it was only the fourth time in 75 years that a conservative 60/40 portfolio was down 20 percent. Not only that, but the stock market volatility index (aka the VIX) reached a high of 82.69 breaking the previous record set in 2008

Consider this: During one two-week stretch in March, the Dow Jones Industrial Average experienced its best single day since 1933 as well as its two worst since days since the Black Monday crash of 1987.

According to Dorsey Wright research, the Dow registered 10 separate days in March 2020 that ranked among the largest single-day moves since 1985. The Dow had five of its 20 best single day returns in March 2020 as well as five of its 20 worst single-day returns. To put these extremes into perspective, we have seen only two days since 2009 that ranked in the 20 best or 20 worst days since 1985 – December 26, 2018 when the Dow gained 4.98% and August 8, 2011 when the index lost 5.55%. No other month since 1985 has had nearly as many eye-popping single-day moves as March 2020 did.

I know it’s hard to fathom, but in March, we surpassed the crashes of 1929 and 1987 with the fastest 30 percent correction ever. Even during the Internet bubble of 2000, it took over 250 days for the market to lose 20 percent–it took just 22 days during the March madness of 2020.