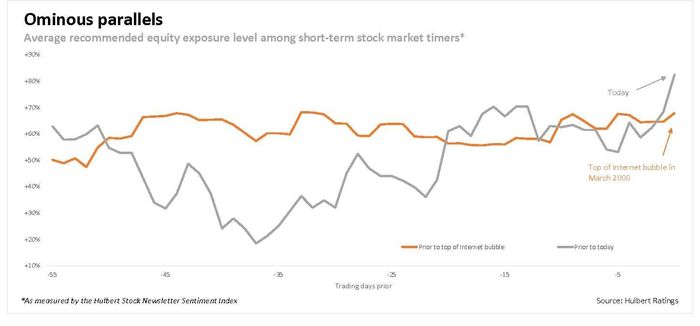

1. Short-Term Traders Record Bullish

Marketwatch – The chart plots the HSNSI over about three months of U.S. market trading days. The orange line reflects sentiment in the weeks leading up to the top of the internet bubble, while the gray line reflects sentiment over the weeks prior to now. By Mark Hulbert

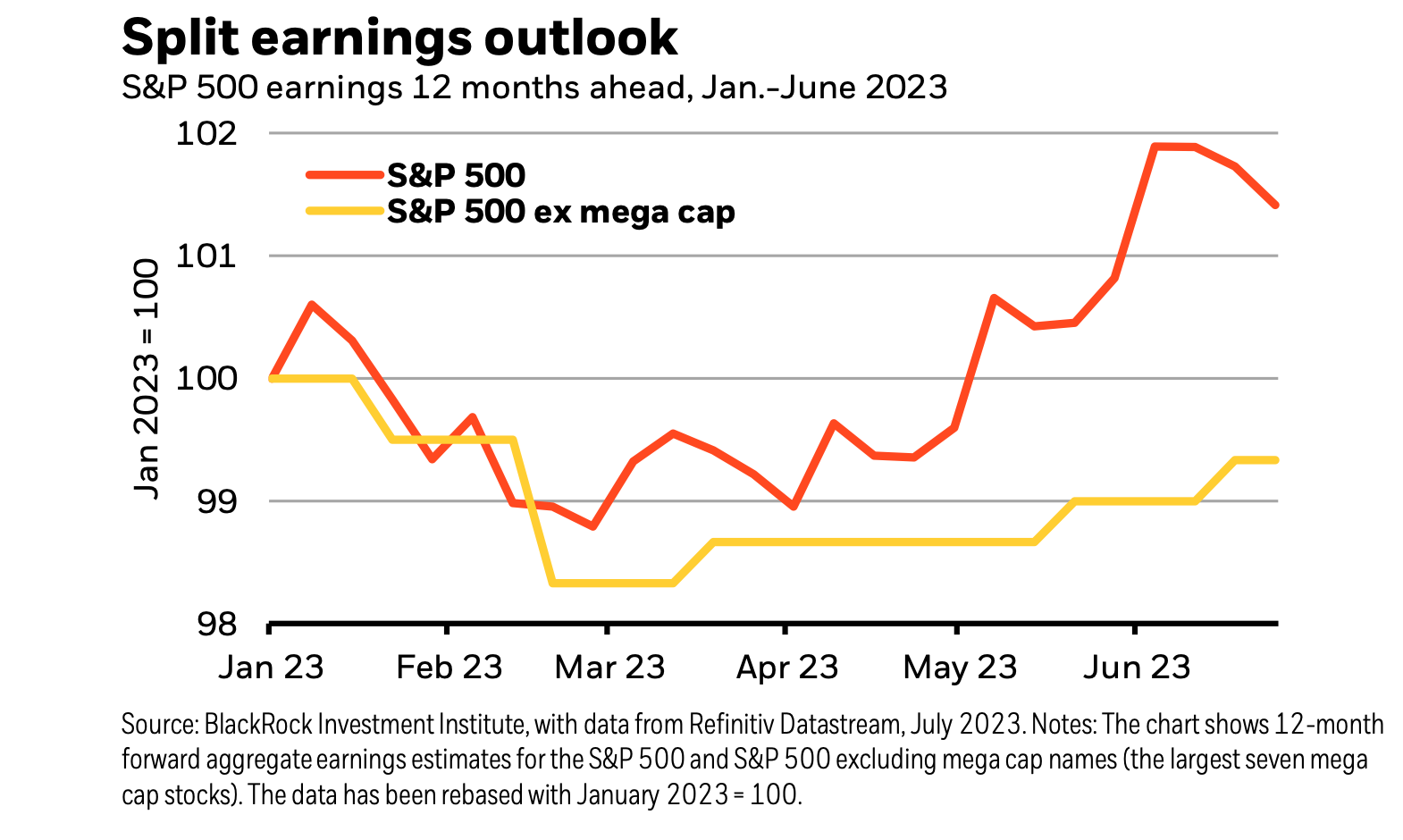

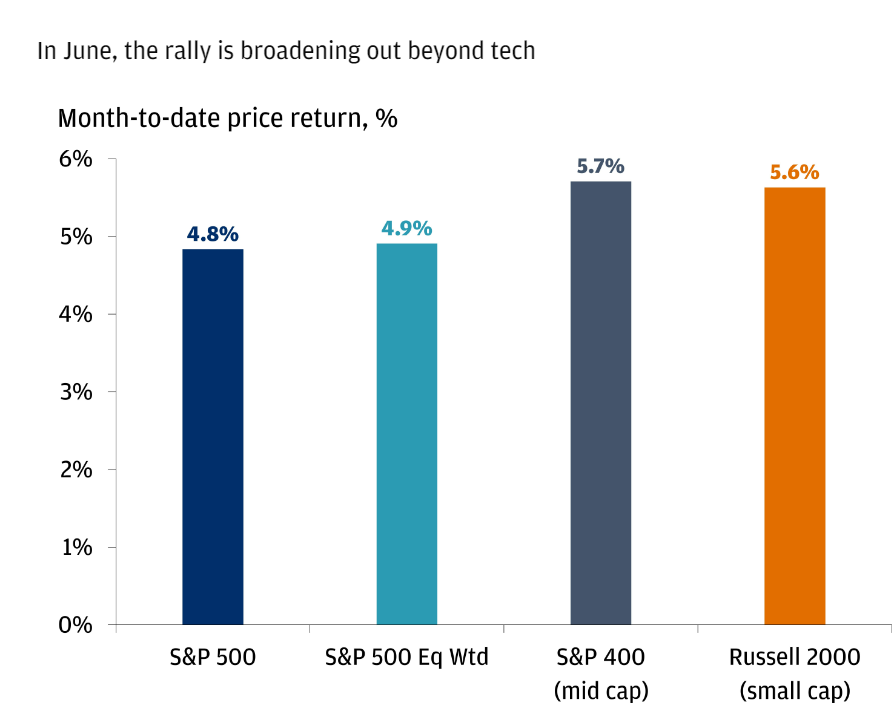

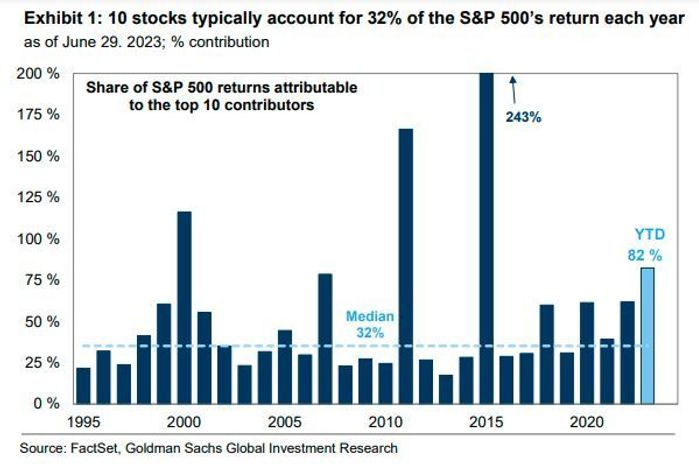

2. Mega-Cap Tech Earnings Growth vs. S&P

Blackrock Q1 earnings growth was flat to slightly negative, Refinitiv and Factset data show. That masks significant divergence: We see a common denominator between what’s driving market performance this year and earnings – the artificial intelligence (AI) buzz. S&P 500 earnings forecasts for the next 12 months have risen in recent months (dark orange line in the chart) along with the market rally driven by tech firms with the largest market capitalization. Stripping out those mega-cap tech stocks, forecasts are flat this year (yellow line). 2023 consensus estimates have been cut but remain well above our expectation. We expect Q2 data will be similar to Q1 as the reporting season kicks off this week, with a contraction hitting in the second half of 2023.

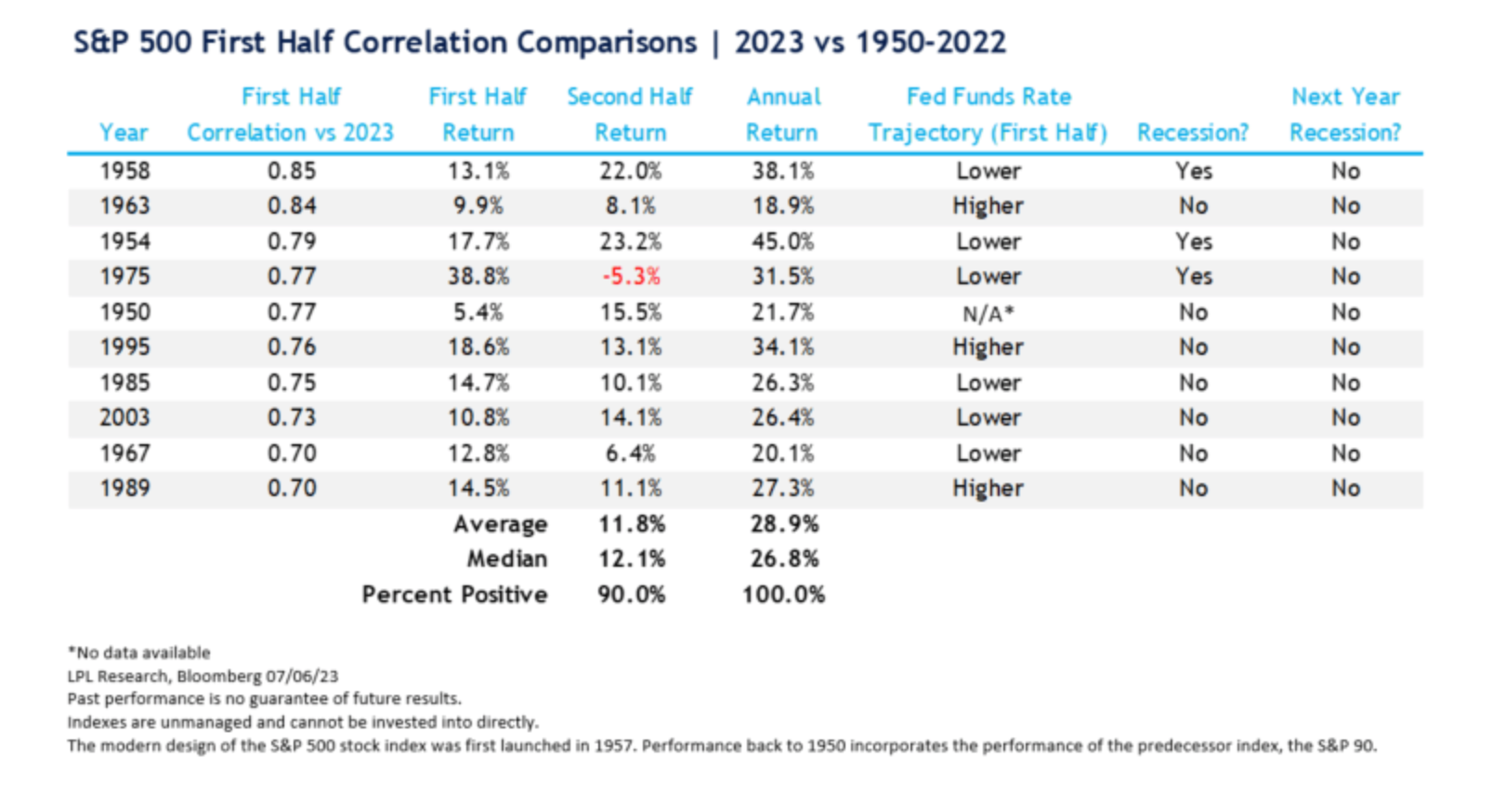

3. LPL Market History Similar to 2023

LPL Research

https://lplresearch.com/2023/07/07/correlation-comparisons/

4. Chinese Banks Price to Book 20 Year Move Downwards

The Bloomberg Intelligence gauge of Chinese bank stocks is trading at 0.27 times book value, just a whisker away from late October’s record low. That compares with 0.9 times for an index of global peers. The China gauge was little changed on Tuesday after registering mild gains early in the trading session.

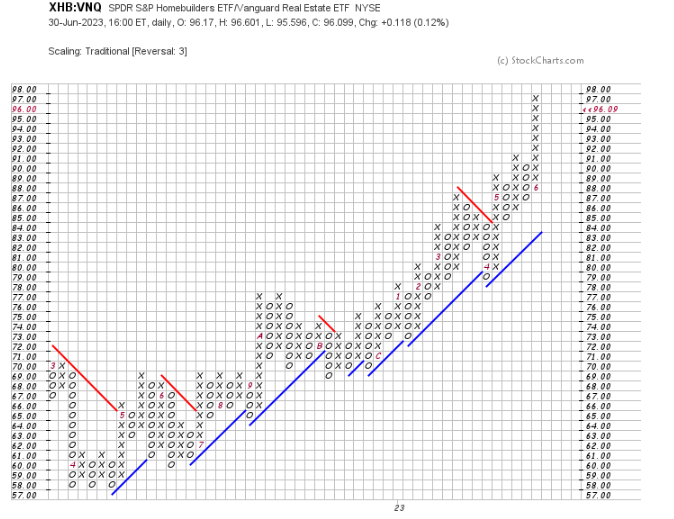

5. Small Cap Homebuilders 2-3x Off 2022 Lows

BZH Homes almost 3x…50 week thru 200 week to upside

TMHC straight up no pullback in 2023

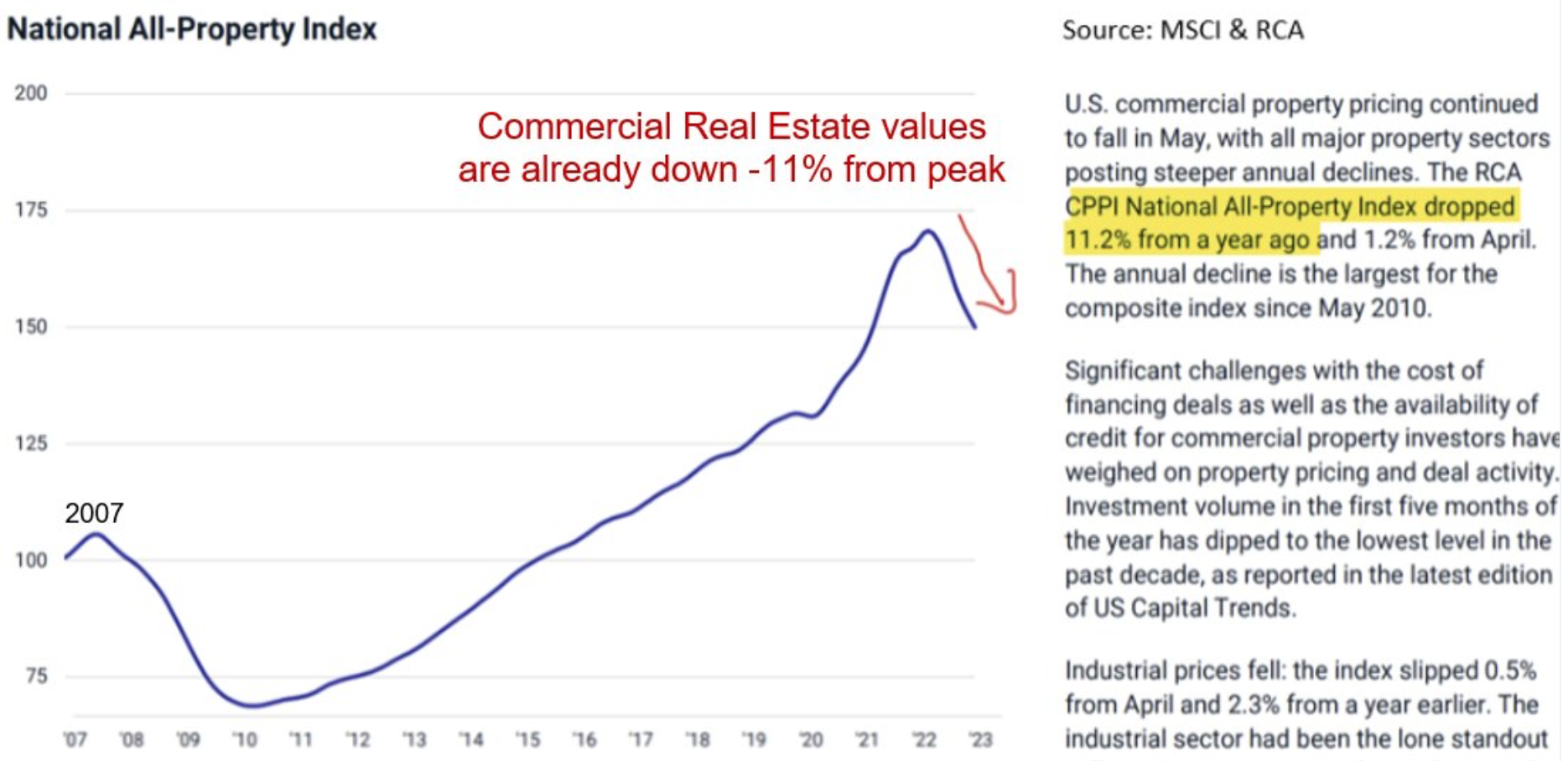

6. Commerical Real Estate -11% from Peak

Nick Gerli @nickgerli1

https://twitter.com/nickgerli1

7. Overstock Becoming Bed Bath and Beyond

50day thru 200day to upside.

8. Pedestrian Fatalities Up 83% in 13 Years

At least 7,500 pedestrians died last year in America, the highest figure recorded for more than 40 years, according to the latest data from the GHSA.

Although only a preliminary result — with data so far collated from 49 states — the numbers confirm that the trend of rising pedestrian fatalities has yet to stop. Indeed, fatalities are up more than 80% compared with the safest year on record, 2009, when ~4,100 pedestrians lost their lives.

Why are pedestrians at risk? Federal reports identify a few factors, including more dangerous driving during the pandemic as well as a lack of awareness and enforcement of laws that are intended to keep pedestrians safe. One author, Angie Schmitt, who explores the phenomenon in a recent book, also blames the rise in larger, heavier vehicles, as well as a generally aging population — who can be more vulnerable to accidents — for the increase in pedestrian fatalities.

Town planners have also been in the firing line. New lanes of traffic are often added to ease congestion, but that ends up limiting space for pedestrians. One traffic engineer blames the rise of “stroads”. The word refers to those that are some combination of “streets” — lower speed avenues where people can shop, dine and walk — and “roads” — which are designed to get cars from A to B quickly and efficiently. Places where the two are combined, without proper infrastructure like crosswalks and lighting, are reportedly responsible for a majority of the fatalities. Www.chartr.com

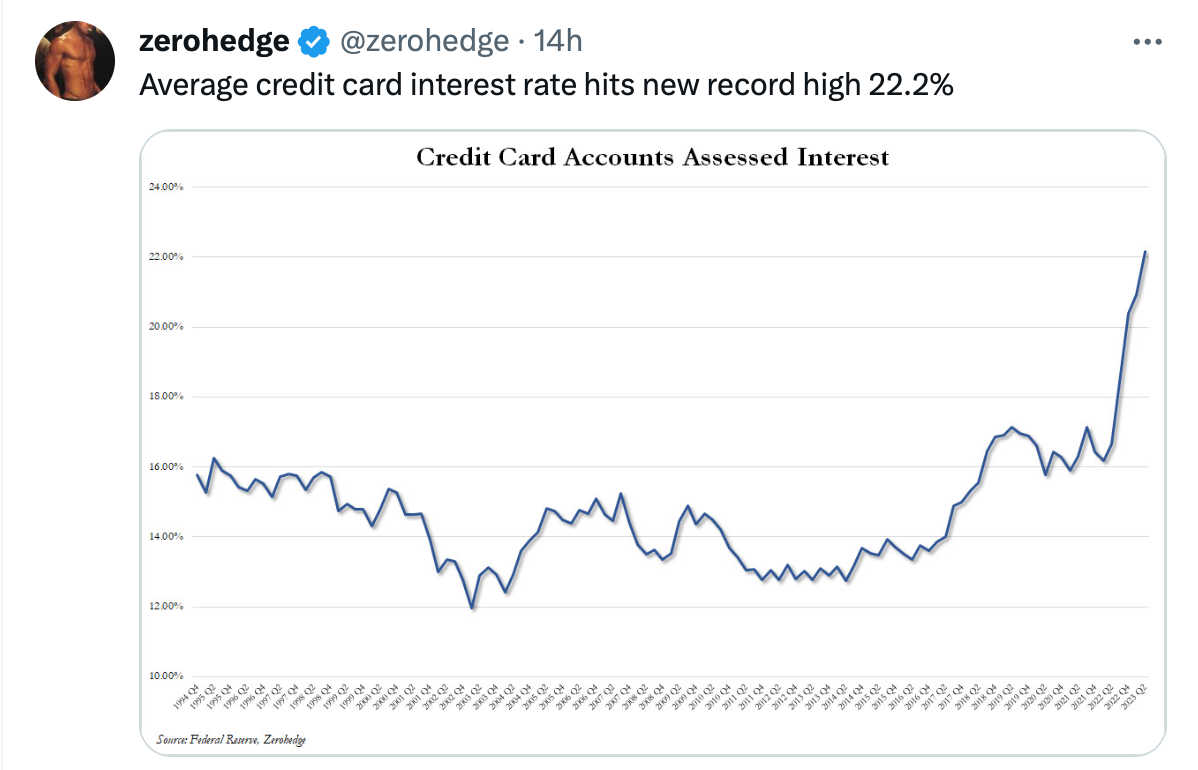

9. Average Credit Card Interest Hits Record High 22.2%

10. Surprising Solutions for Overthinking-Psychology

Quick, practical solutions for people who self-sabotage by overthinking.

If you think in-depth, you probably find that your tendency to overthink is both a strength and a weakness.

You may desire to retain the benefits of thoughtfulness while eliminating the self-defeating aspects of overthinking.

Attempt one of these three techniques to achieve that. Choose whichever strategy naturally appeals to you.

1. Execute once, then optimize.

Try taking this approach: Whenever you do anything for the first time, don’t try to optimize it. Instead, adopt the approach that you will execute once, with basic thinking, then optimize your approach the second and subsequent times you do whatever it is.

For example, I recently decided to buy a choline supplement. I got bogged down in factors like which brand to buy, which dose, which form, where to buy it from, and when. By employing the execute once approach, I selected an acceptable option, aware that I could obsess about the best choice during my next purchase.

The benefits? You’ll make quicker decisions, and probably learn more through your experience than from delaying.

2. Put your thoughts in a suitcase.

Anxiety tries to be helpful by not allowing us to forget about potential threats. It nags us by knock, knock, knocking to remind us of our worries and insecurities.

For example, filling out child development questionnaires on my baby’s milestones was stressing me out. I wanted to tell the pediatrician I didn’t want to do them but was worried she would think I was being neglectful. In reality, I’m hypervigilant about milestones; I didn’t need the questionnaires to make me even more so.

If you try to stop having a thought, anxiety tends to just get louder. However, what can sometimes work is imagining putting that thought aside somewhere safe where you won’t forget about it. The imagery I like is to imagine putting my worries in a suitcase, and then carrying it but not interacting with it.

This technique can create sufficient psychological distance from thoughts, enabling me to make more skillful choices in my actions. In this case, there was no reason to expect the pediatrician, who has always been supportive, would think I was being neglectful—and in fact, she reacted supportively again when I broached this topic.

3. Reflect on the benefits of both impulsive and well-thought-out decisions.

Remember I said at the outset that overthinking is both a strength and a weakness? People who overthink tend to be very willing to engage in meta-cognition, that is, thinking about their thinking. You can use that to your advantage here.

Try thinking of examples of good decisions you and others have made. What actions have led to awesome outcomes for you and other people you know?

Next, reflect on whether these were always well-thought-out decisions. In Stress-Free Productivity, I wrote about how some of my best decisions weren’t very well thought through. For example, I’ve put less research into house purchases than into some minor decisions, and yet these house purchases have turned out to be some of my best decisions. I also put relatively minimal thought into choosing a Ph.D. advisor, and yet that worked out wonderfully.

Sometimes good decisions are the result of exhaustive research and accurate perceptions, but not always. Other factors, like serendipity, or meeting the right person at the right time, can be influential too.

When you see this diverse pattern, it can help free you up. Overthinking is not the sole path to success. Engaging in random conversations, acting on instinct or impulse, or exploring topics that trigger your curiosity, even when you should be focused elsewhere, can also yield positive outcomes.

Sometimes it’s enough to recognize that you currently don’t overthink every decision, and that can work out fine, and even well. You can begin to see yourself as someone who sometimes overthinks, but not always.

It’s important not to be ashamed of overthinking. I’m being genuine when I say that it’s both an important strength and a frustrating weakness. Acknowledge the benefits of thinking deeply, but also master skills to dial it back when that is advantageous. This will give you maximum flexibility, lower stress, and the best results.

How did this article change your view of overthinking? What strategy are you excited to try?

To find a therapist, visit the Psychology Today Therapy Directory. https://www.psychologytoday.com/us/blog/in-practice/202307/3-surprising-solutions-for-overthinking

The remainder of this post and the opportunity to reflect, share, and discuss in the comments are reserved for the community of subscribers. If you would like to support my work and join the conversation, consider subscribing.

The remainder of this post and the opportunity to reflect, share, and discuss in the comments are reserved for the community of subscribers. If you would like to support my work and join the conversation, consider subscribing.