1. Nasdaq 100 60-Day Streak Over 20-Day Moving Average…Second Longest Ever.

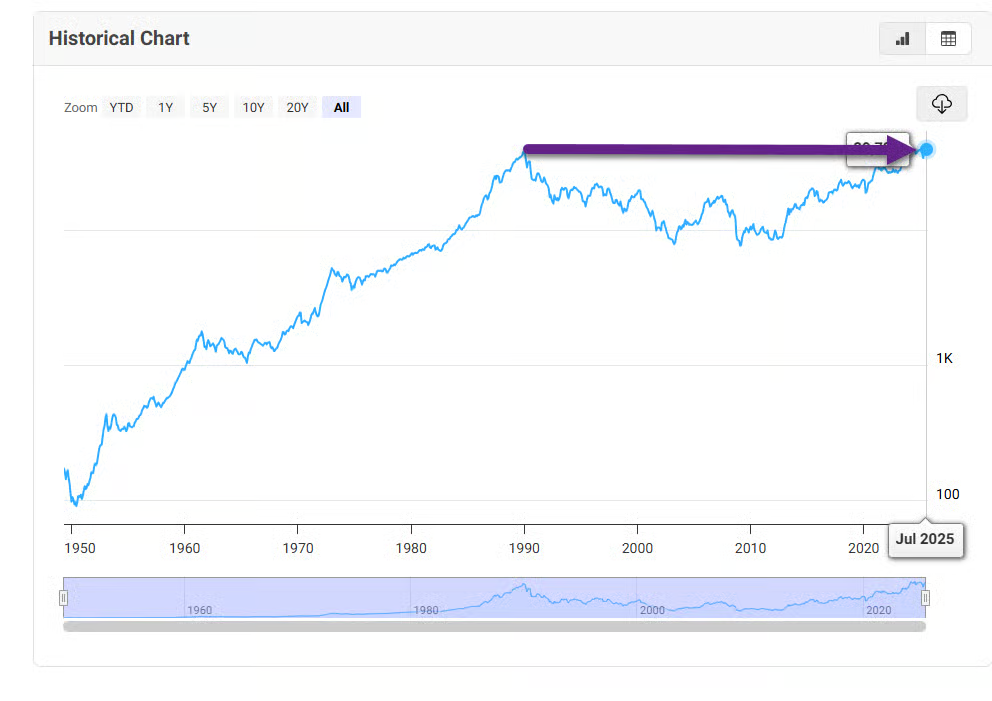

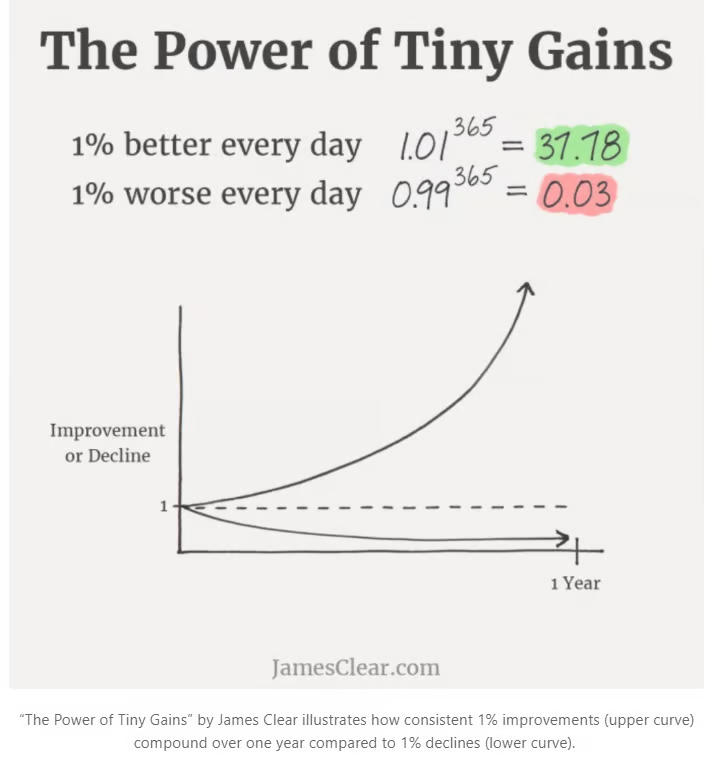

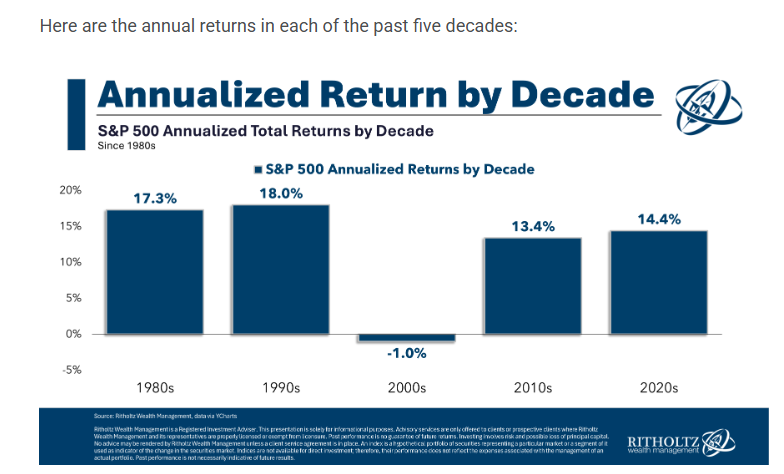

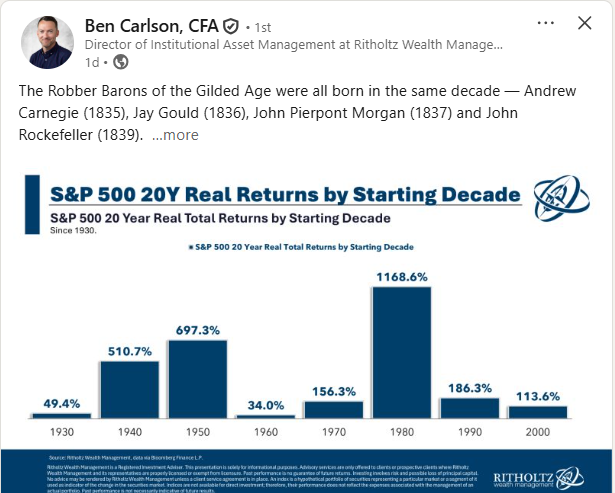

2. S&P 20-Year Return Blocks.

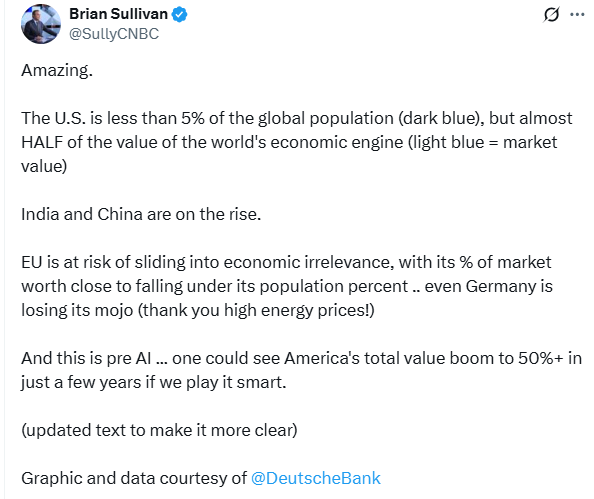

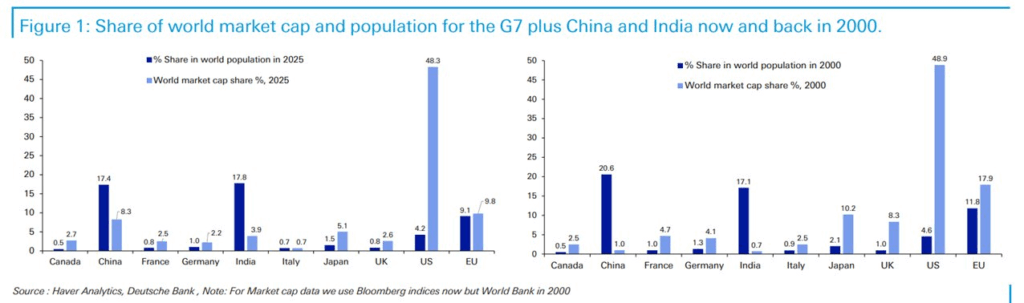

3. Reminder U.S. 5% of World Population But Half the World Financial Engine.

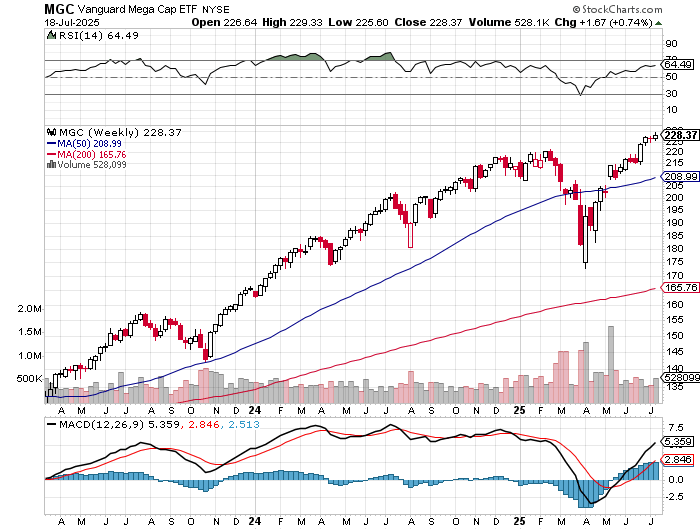

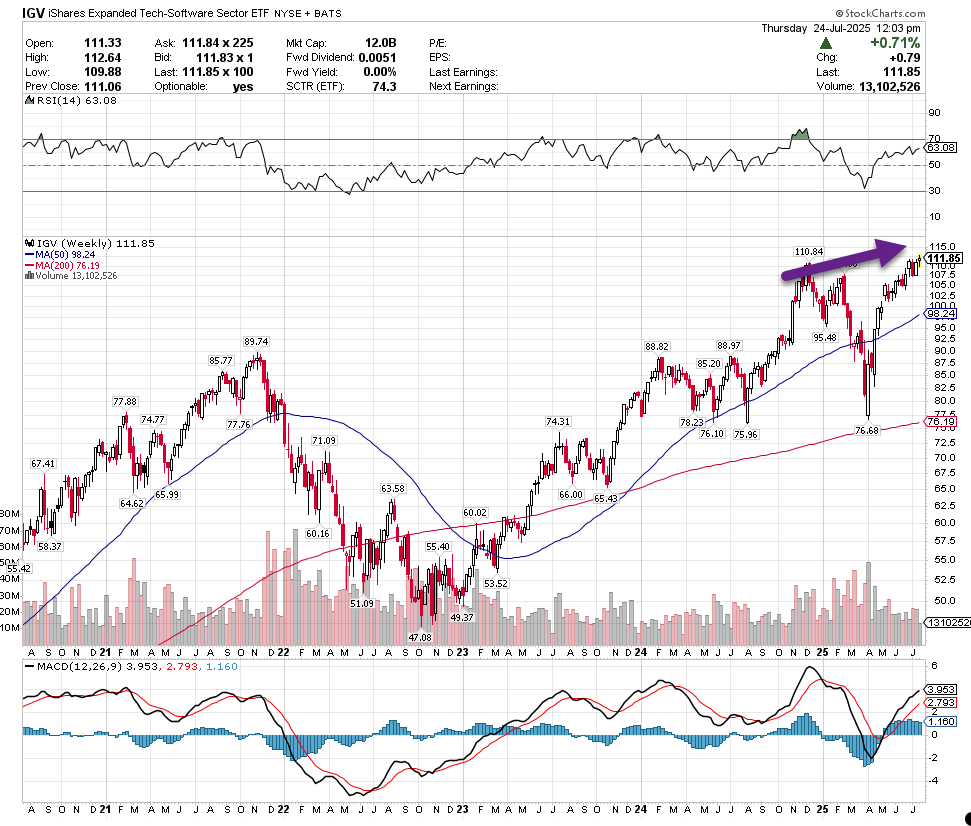

4. Software ETF Hits New Highs.

5. Big B Bill Cuts Off Clean Energy Subsidies….ETF +26% One-Month.

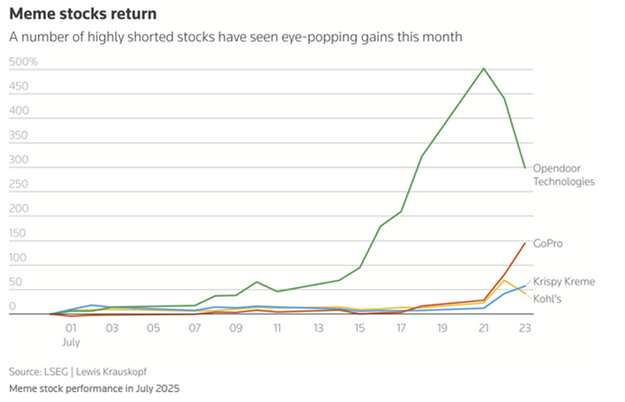

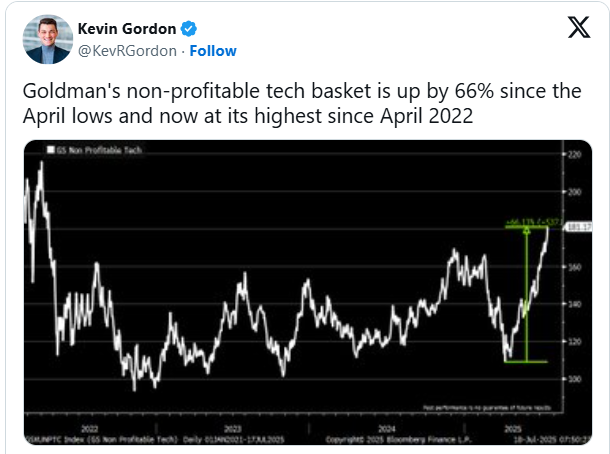

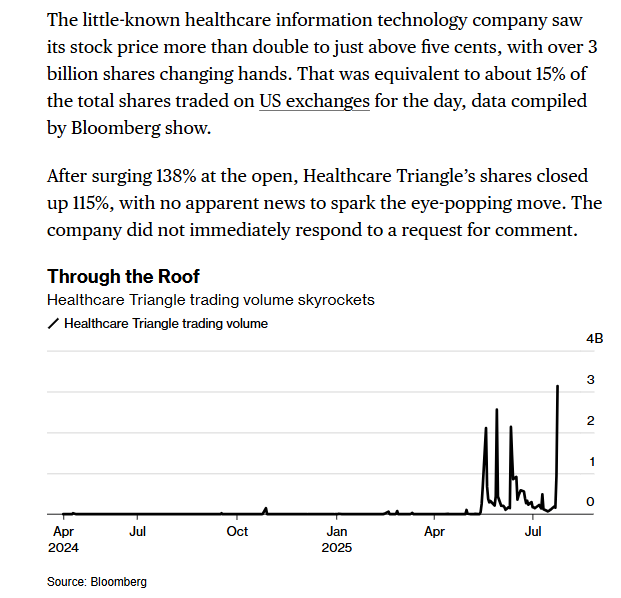

6. A Penny Stock Made Up 15% of Trading Volume.

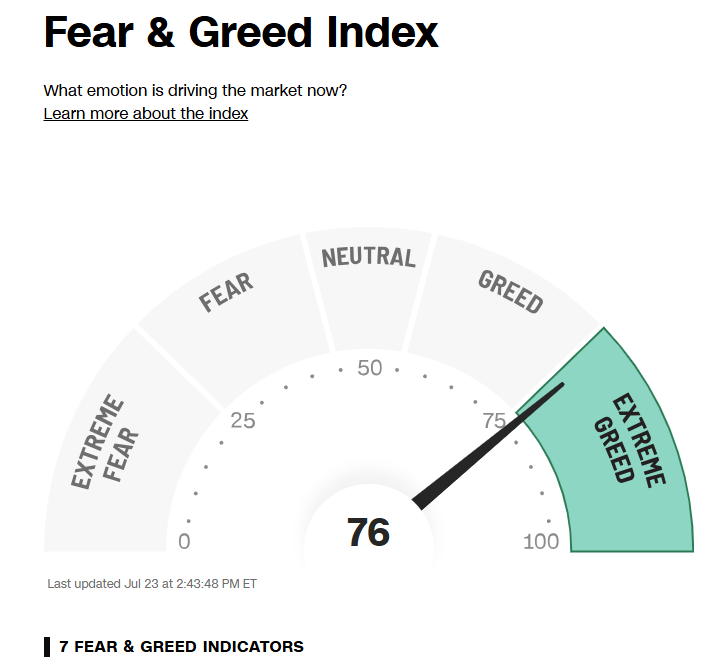

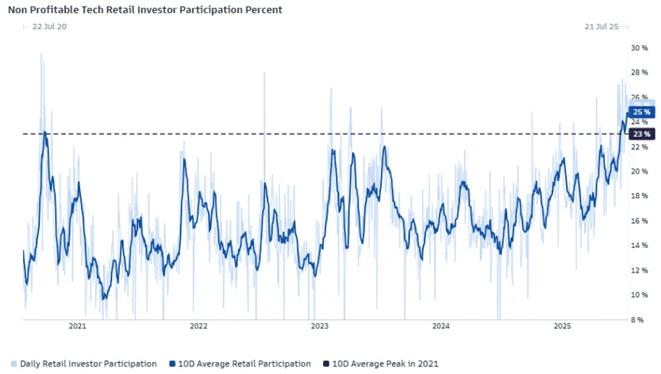

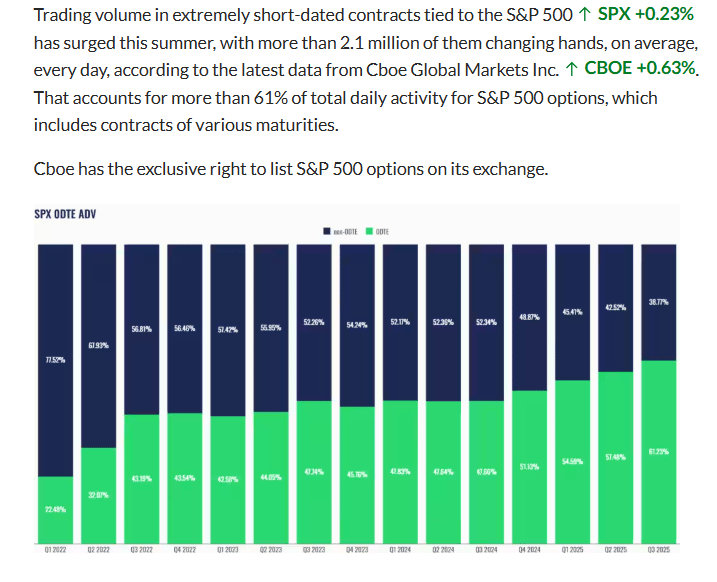

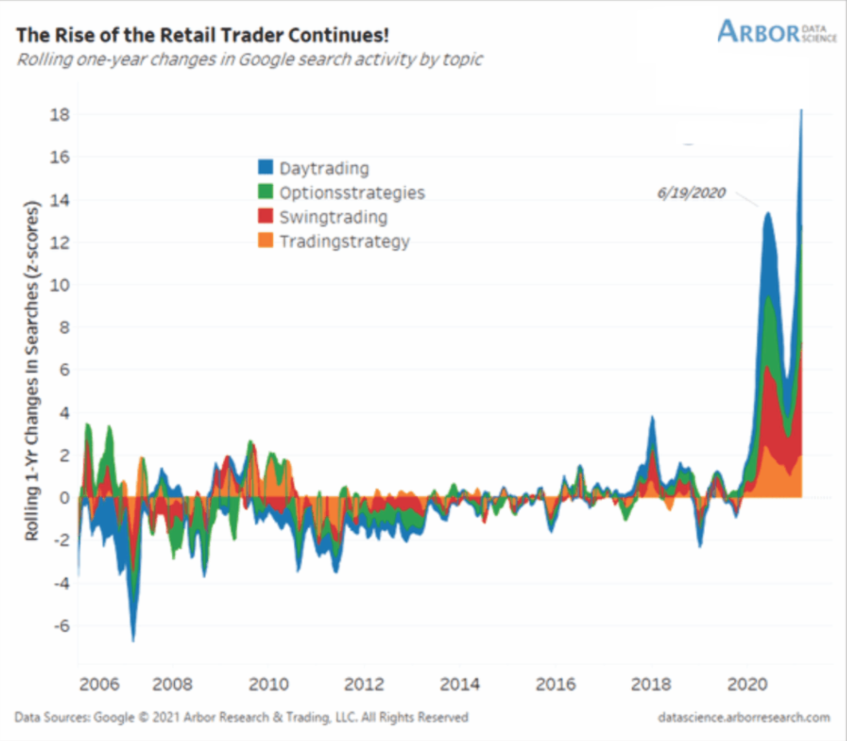

7. Google Search for Day Trading and Options Strategies.

https://www.advisorperspectives.com/commentaries/2025/07/24/retail-speculation-back-vengeance

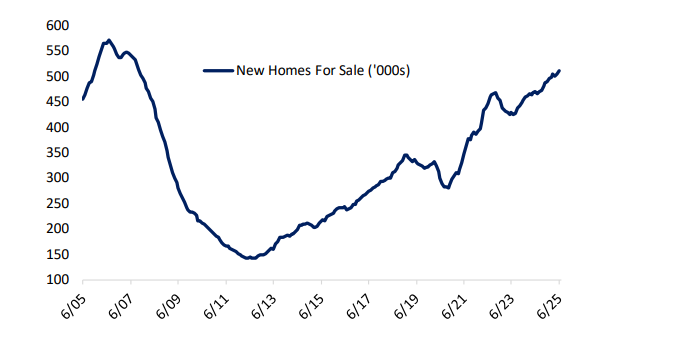

8. Increase in New Homes for Sale.

Bespoke.

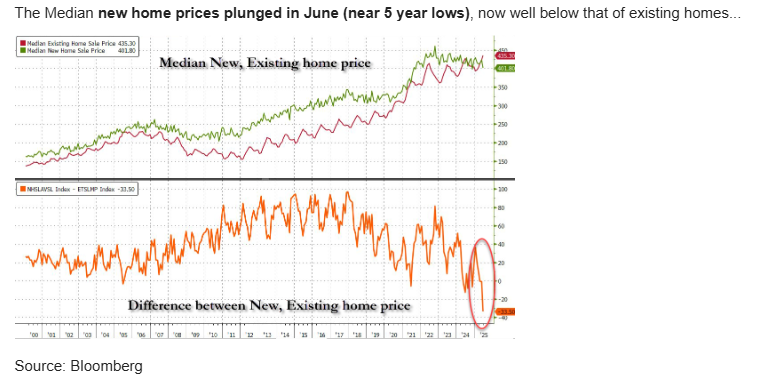

9. The Median Price of New Home Below Existing Home Price.

https://www.zerohedge.com/personal-finance/us-new-home-sales-disappoint-june-prices-plunge

10. 7 Steps to a Super Brain-Mark Hyman

The good news is that with these seven strategies, you can eliminate the bad stuff to cultivate your best brain ever.

- Eat real food. When I say real food, I mean whole, organic, fresh, local and unprocessed food. If it has a label or a barcode, you should probably avoid it. If your great-grandmother wouldn’t recognize it, don’t eat it. Processed junk foods mostly exist in the middle aisles of the grocery stores, so avoid those aisles!

- Eat lots of colorful fruits and vegetables. These colorful super-foods come loaded with brain-boosting stuff like phytonutrients. The dark, deep reds, yellows, oranges, greens and blues mean these foods contain powerful anti-inflammatory, detoxifying antioxidants and energy-boosting, brain-powering molecules. Enjoy an array of colorful plant foods like blueberries and dark leafy greens like kale, Swiss chard, spinach, watercress, and arugula.

- Go for slow carbs, not no carbs. Cauliflower and an ice cream sundae fall under the “carbs” category, but you know the former is healthy and the latter isn’t. Eating whole plant foods with plenty of fiber, including small amounts of beans, non-gluten whole grains, nuts and seeds, keeps toxins moving out of your body and keeps your gut bacteria healthy. A healthy gut means a healthy brain!

- Eat plenty of healthy fat. I provide an excellent, detailed healthy fat food plan in my new book Eat Fat, Get Thin. Fat is actually very good for your brain. In fact, 60 percent of your brain is made up of DHA – an omega-3 fat that you get from algae and fish. My brain worked pretty well before, but embracing fat (even good saturated fats like coconut oil and MCT oil) pushed my mental clarity through the roof.

- Optimize protein. We need about 30 grams of protein per meal to build muscle. When you lose muscle, you age faster and your brain takes a huge hit! Eat protein at every meal, including omega-3 eggs, protein shakes nut butters, even fish for breakfast.

- Stop poisoning your brain. Eliminate sugar, high-fructose corn syrup, trans fats, food additives and preservatives, all of which poison your brain and disrupt your biochemistry. If it’s not real food, don’t eat it.

- Supplement. A high-quality multivitamin, as well as magnesium, vitamin D3, omega-3 fatty acids, probiotics, folic acid, B6 and B12 are all necessary for your brain to function optimally. You can find the cleanest and best versions of these essential nutrients along with other brain-boosting supplements here.