1.XES Oil and Gas Equipment ETF -20% Correction….EXXON Hits 10 Year Low.

XES ETF

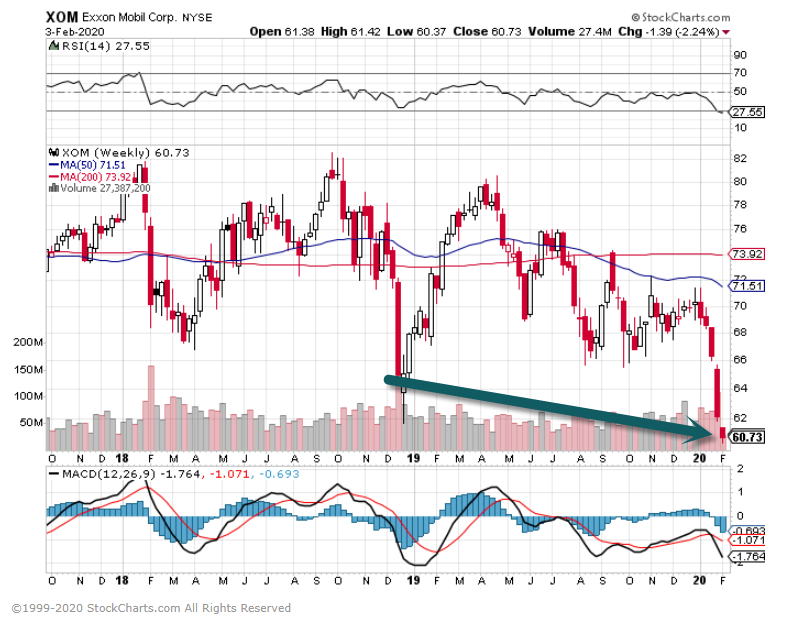

XOM breaks 2018 levels…hits 10 year lows.

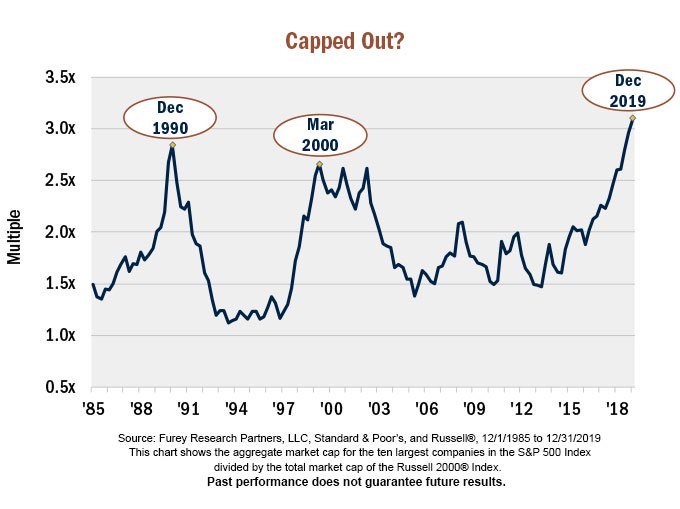

The march higher took on a familiar feel as larger names continued to outpace smaller. The pull of large companies has become so strong that, as shown [below] [to the right], the 10 largest companies in the S&P 500 have a combined market cap of MORE THAN 3X THE ENTIRE RUSSELL 2000® INDEX of small companies. This type of stampede into pricey mega-caps has historically ended poorly for those who followed the crowd.

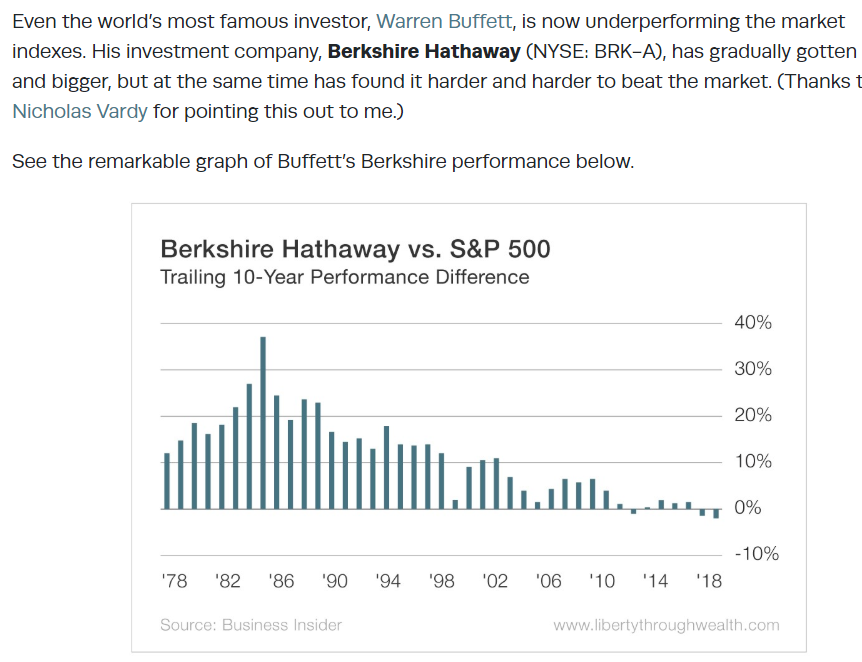

Why the Hot Hand of Investing Never Lasts–By Mark Skousen https://investmentu.com/wealth-creation-hot-hand-investing/

Continue readingAri Levy@LEVYNEWSLorie Konish@LORIEKONISH

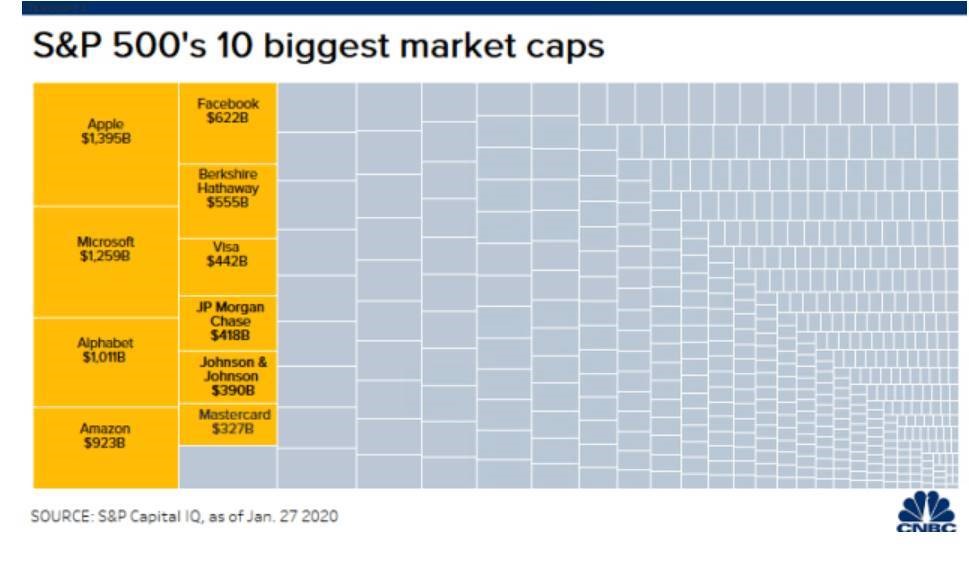

https://www.cnbc.com/2020/01/28/sp-500-dominated-by-apple-microsoft-alphabet-amazon-facebook.html

Continue reading

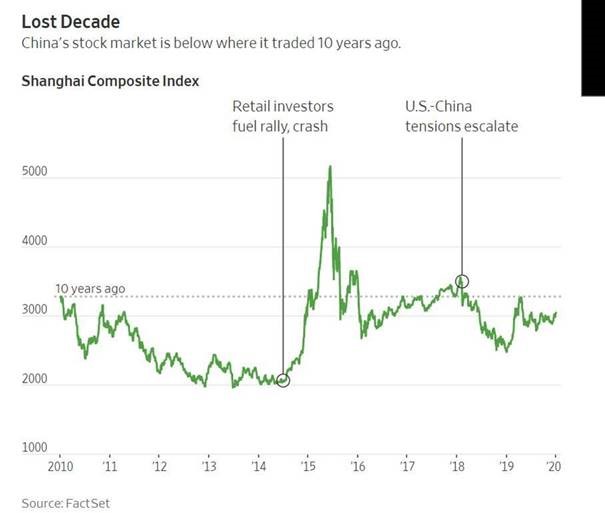

It Was a Lost Decade for China’s Stock Market, but Investors Bet on Better Times Ahead-https://www.wsj.com/articles/it-was-a-lost-decade-for-chinas-stock-market-but-investors-bet-on-better-times-ahead-11578133803

Continue reading