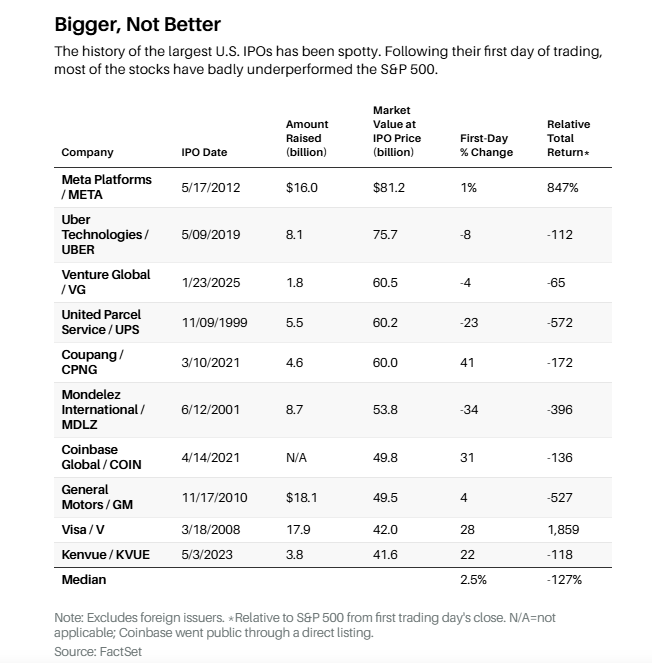

1. Space X vs. Top 100 IPOS

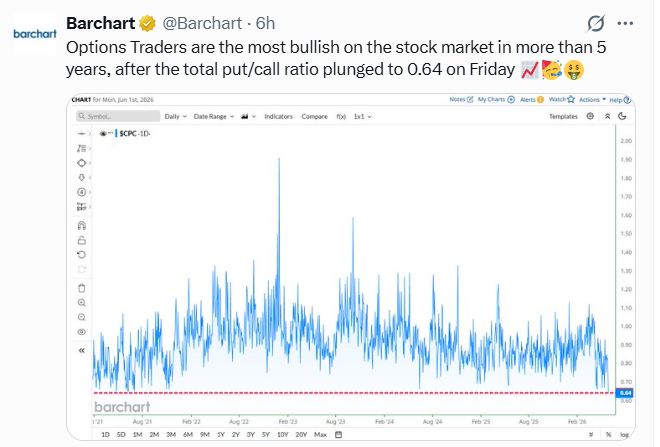

2. Options Traders Most Bullish in 5 Years

Barchart

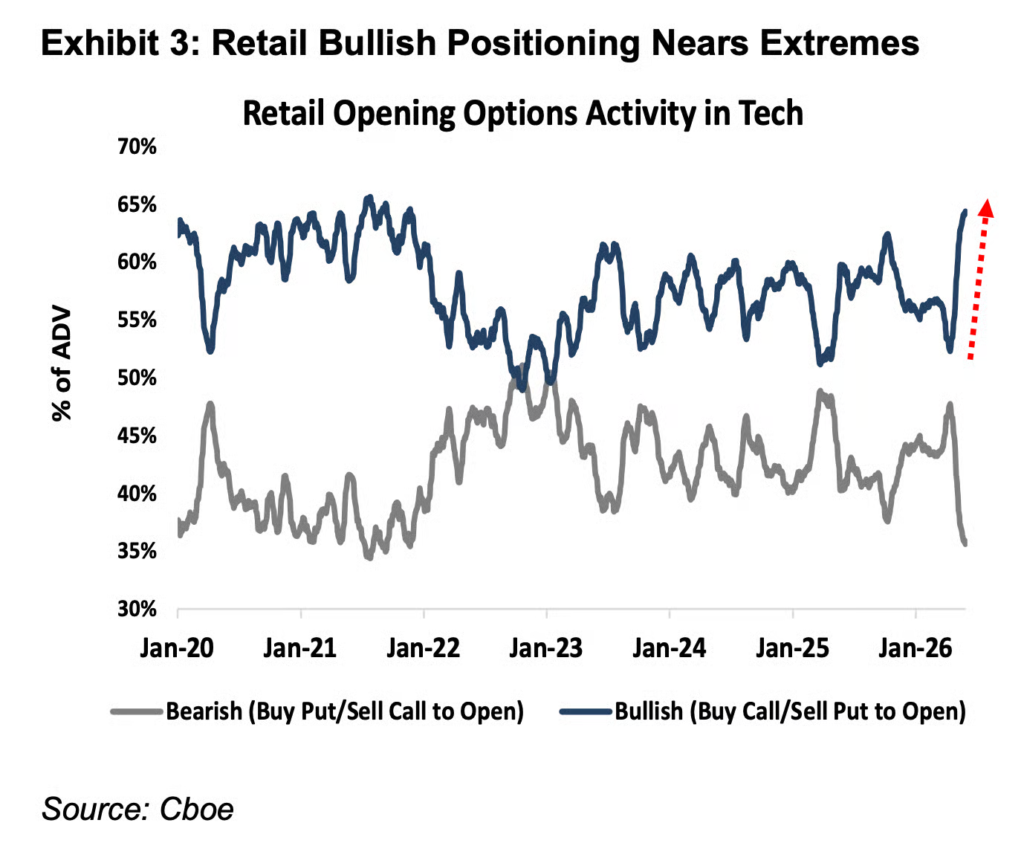

3. Retail Investor Optimism on Tech Stocks Near Record Highs

Retail opening options. “Retail optimism in Tech is reaching a near record, with bullish trades making up almost two-thirds of all retail opening options activity in the mega-cap Tech stocks (e.g. buying calls or selling puts to open).”

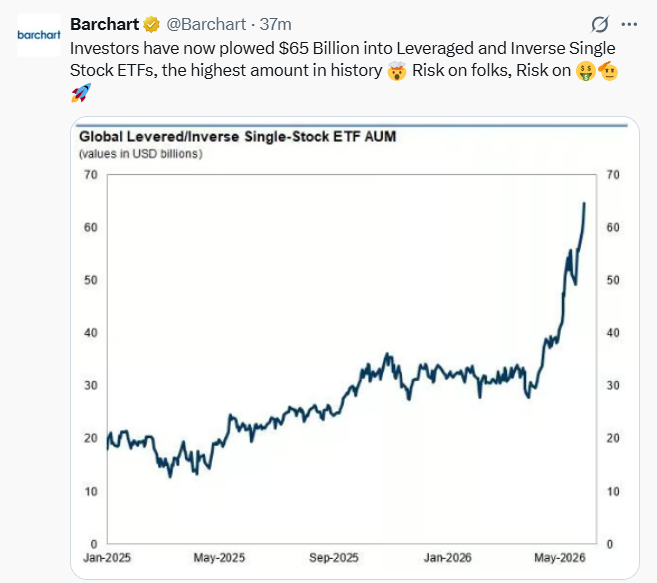

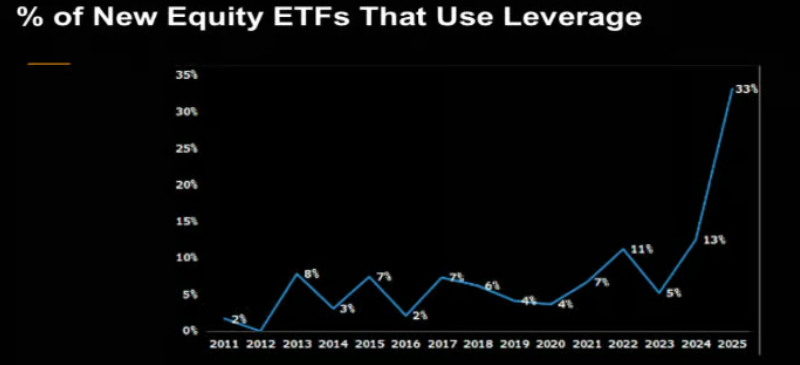

4. ETFs Using Leverage Skyrocketing-Irrelevant Investor

The Irrelevant Investor

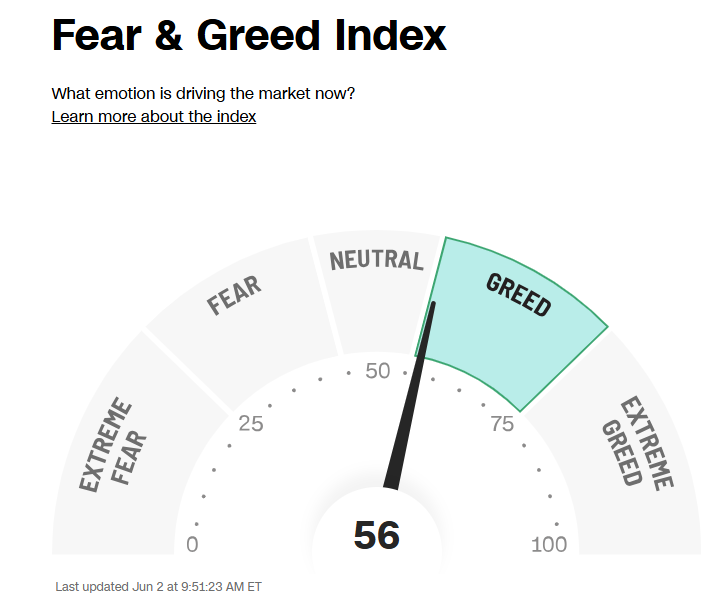

5. Fear and Greed Index Never Hit “Extreme Fear” on this Rally

CNN

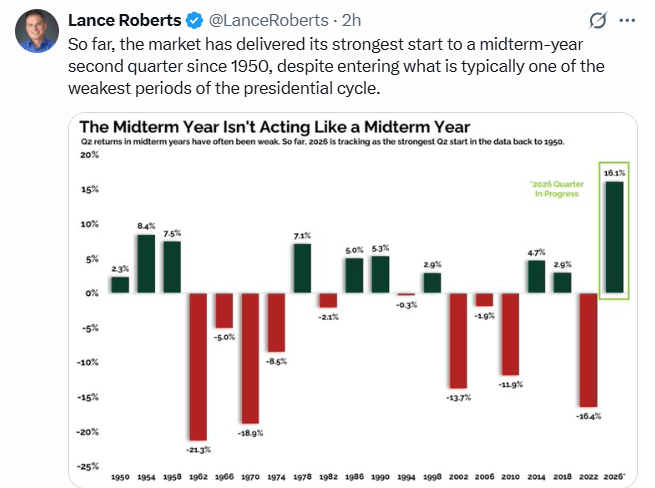

6. Record Mid-Term Election Year Stat

Lance Roberts

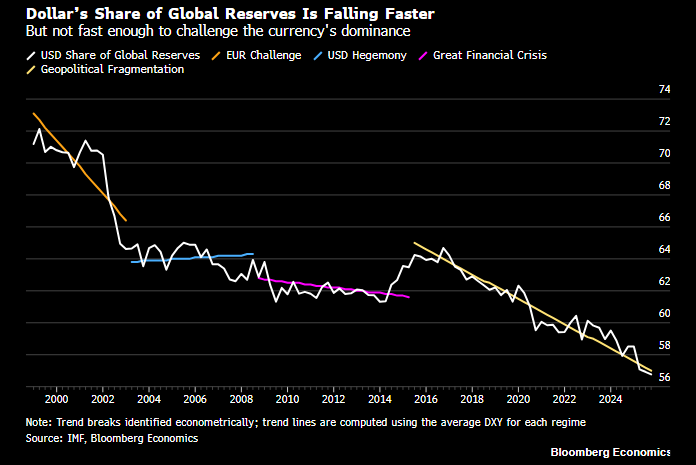

7. Dollar Shrinking Share of Global Reserves

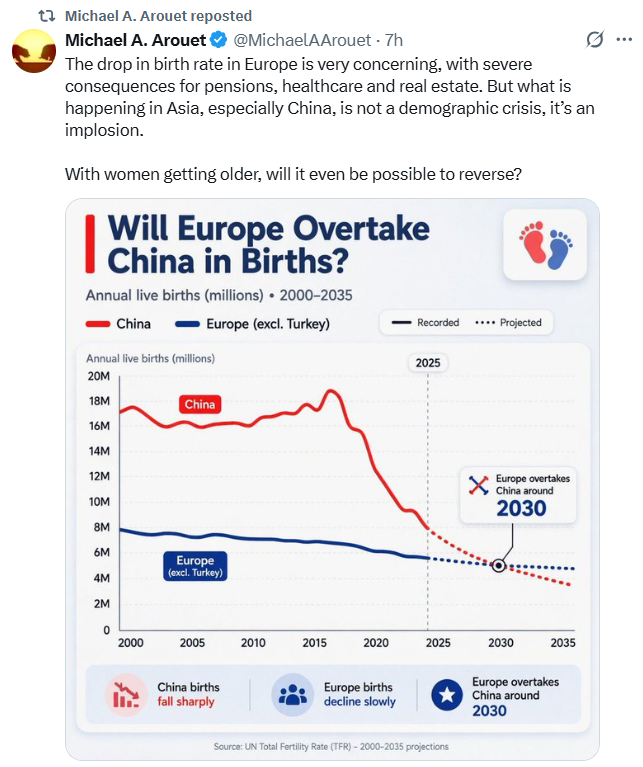

8. Demographics is Destiny….Europe and China Dropping Birth Rates

Michael A. Arouet

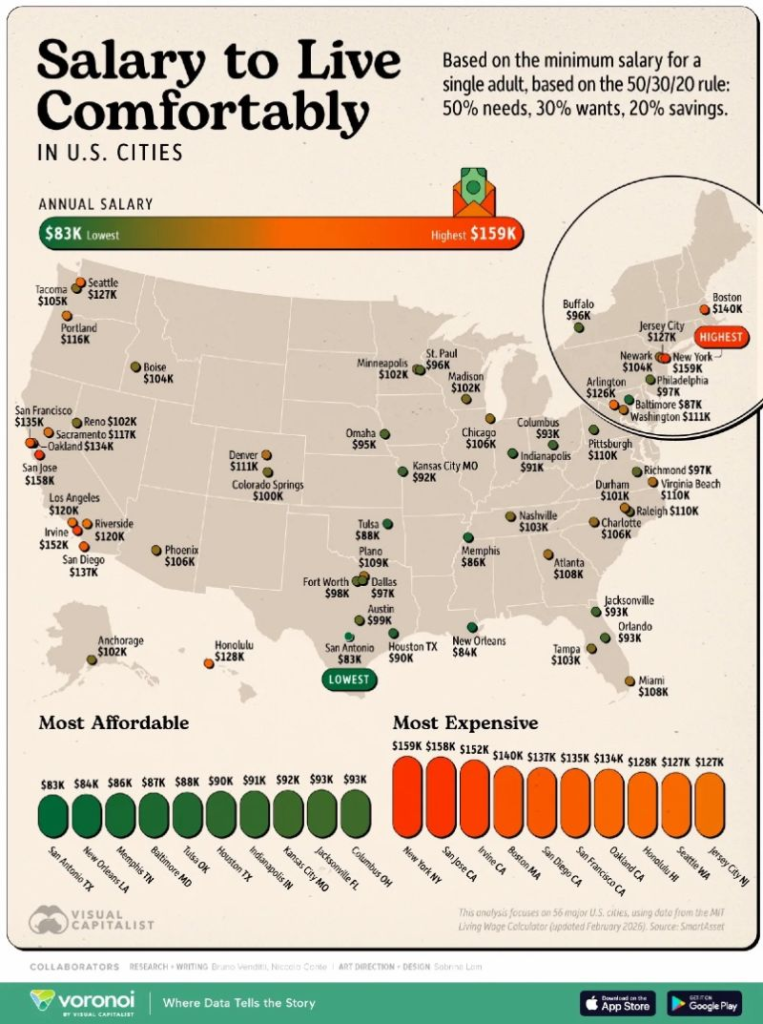

9. Salary to Live Comfortably in America

10. Rethinking famous college admissions-Seth’s Blog

Even if you’re not applying, this thought experiment gives a glimpse into how the world is about to be rewired.

The top 10 most selective colleges in the US admit about 5% of those who apply. They’re not selling education as much as a label, a rare chance for someone to slot themselves into a category in our economic and cultural hierarchy.

If all the famous schools wanted to do was be elite, they could use a formula–grades plus SAT plus something–and algorithmically draw a line and pick everyone over that line.

But it’s more complicated than that.

First, they want to find some sort of balance, to create a reasonably diverse group of backgrounds that coalesce into a community. They don’t want 100 kids from the same high school…

Second, they have special cases, many of which they don’t want to talk about in public, involving alumni, outgroup dominance considerations, and sports, which in many cases can count for as much as 50% of the incoming body.

Third, they use variable pricing, with many students ultimately paying different tuition. Few can afford to be fully need-blind in selection.

The end result is complicated, onerous and mostly a charade. 50,000 applicants coming into each institution cannot possibly be reviewed coherently or consistently. And uncertainty takes a toll, not just on the students, but the schools and their teams as well.

It’s expensive and time-consuming, and fraught with worry. The typical fancy college applicant applies to nearly ten schools. Some kids get into a few schools, some to none at all. And essays in the age of AI are now officially meaningless.

[I’ve written earlier that they should have two sorts of rejection letters. Half the people should get one saying that they simply didn’t get in. The other half should receive a letter saying that they were good enough to get in, but didn’t get lucky.]

This is what you’d invent if it were 1952.

If we rethink it, it might be more like this:

- Each applicant ranks the schools they apply to. That’s a forced ranking, and binding.

- The application is online and interactive. It shifts in real time based on the answers applicants give. I’d prefer we get rid of standardized testing, but I’d imagine some sort of asynchronous vetted skills testing can be referred to by the applicant.

Sit down at 10 am on the day of your choosing, and all your applications will be done by 3 pm. Chaperones, video, and real-time snippets make it likely that the real applicant actually is the one engaging with the application.

It’s easy to imagine that this is simply a digital form of the existing application, but it’s not. It works with the student, finding their strengths, asking follow-up questions, presenting them in the best light for their skill set. Get some math questions right and it will ask you some more. Talk about your work at the Fuller Center and it will dive deeper. It’s not adversarial; instead, it’s a scout and a coach.

Even better, it’s not just one session–it’s a series of conversations, over time. And as a coach, the process can advise the student on their forced rankings, helping them reconsider preferences based on their interactions. - The schools have to be very clear to the system about the balances they seek, the trade-offs they’re making and what’s important to them. This won’t be easy at first, because naming it is uncomfortable. In fact, this is the hardest part of the transition.

[Hard indeed: Lawsuits will be an inevitable outcome. Discovery in the SFFA case against Harvard put the previously unrevealed rules into the record—the admission rates by legacy status and athletic skill. Naming the trade-off is what turns it into a lawsuit.] - Then, on selection day, the AI system, which has read every single application, applies game theory and ranking to create the best possible allocation of seats, aid and students. The Gale-Shapley stable-matching algorithm is already used in medical residency placement. It leads to its own game theory implications, of course.

This shift saves money, reduces anxiety, is probably more fair. It’s auditable and improvable and uses far less time as well. It used to be impossible. Now that it’s not just possible but easy, the pressure falls on the constituents who’d prefer to avoid it.

Is it better to believe that you got into a famous college because of a mysterious, perhaps human, definitely flawed, and easily gamed system, or would we prefer a different sort of black box, one that puts data to work in a coordinated and prioritized way?

Systems change is difficult and unpredictable, and I’m not holding my breath. Just imagine, though, how many processes we live with now that will be rebuilt on top of widespread coordination.

June 1, 2026