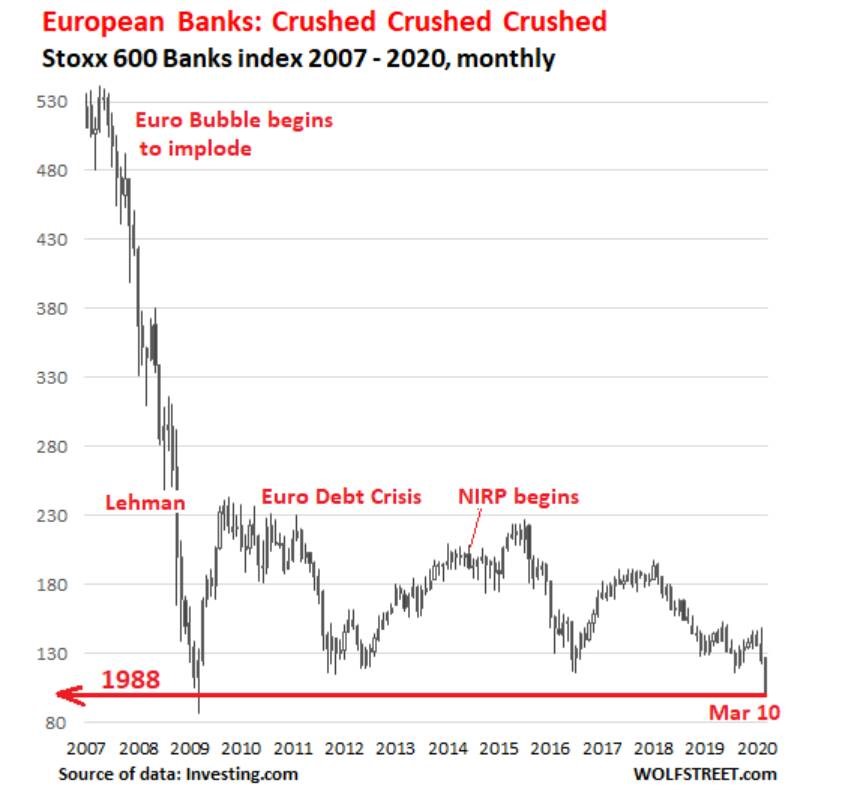

1.European Banks Hit 1988 Levels.

Wolf Street

2.Nasdaq Bank Index …-45% from Late 2018 Highs

Everything Is Going Wrong All at Once for U.S. Banks

Epidemic triggers risks from low interest rates, slow loan growth and sliding stock and energy prices

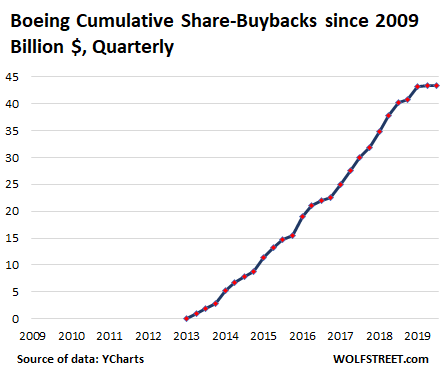

3.Boeing High was $432…$154 Last Price.

BA -64% from highs

BA spent a ton of cash in stock buyback bonanza now short cash…Look for more companies to have this problem if market downturn continues.

Wolf Street

This mad scramble for cash and the existential urge to “preserve cash in challenging periods” comes after this master of financial engineering – instead of aircraft engineering – blew, wasted, and incinerated $43.4 billion on buying back its own shares, from June 2013 until the financial consequences of the two 737 MAX crashes finally forced the company to end the practice. That $43.3 billion would come in really handy right now:

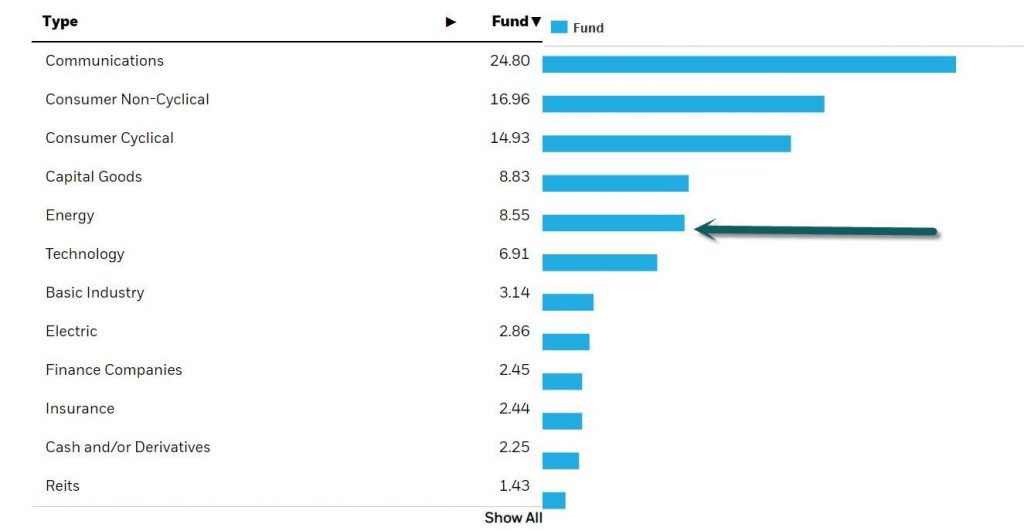

4.High-Yield ETF Energy Exposure 8.5%

$88 Billion in energy bonds due this year

Exposure Sector Breakdown

https://www.ishares.com/us/products/239565/ishares-iboxx-high-yield-corporate-bond-etf

5.NY FED will Infuse $1.5 Trillion into Market.

| ECONOMY The Fed Hits the Pedal Fed Chair Jerome Powell’s had a big March trying to support the financial markets in these times of crisis. Last Tuesday, he took the roadster out of the garage by cutting interest rates. On Monday, he pulled out of the driveway—raising limits on repurchasing operations—before turning onto the highway Wednesday (jacking lending up to $500+ billion from under $200 billion). Yesterday, he gunned it up the on-ramp. The New York Fed will infuse $1.5 trillion into financial markets in an effort to calm the typhoon-esque waters. It’ll do that via three separate $500 billion repo (repurchasing agreement) offerings. The first began yesterday; the second will last for three months; and the third will stay for just one. The injection could broaden the Fed’s portfolio by over 35%. Zoom out: The markets barely noticed Powell’s rate cut last week. Now, the Fed is using longer-term asset purchases to stabilize markets, a move it last made to shoulder them through the 2008 financial crisis. |

Morning Brew https://www.morningbrew.com/

6.Bitcoin No Safe Haven…Plunges -27% in One Day.

https://www.coindesk.com/price/bitcoin

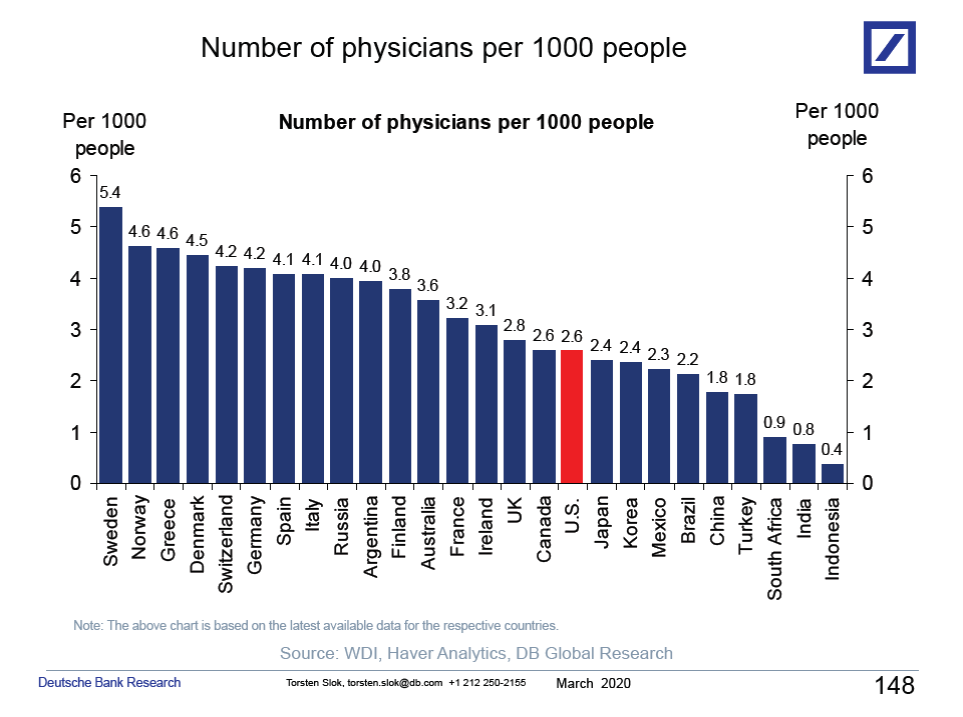

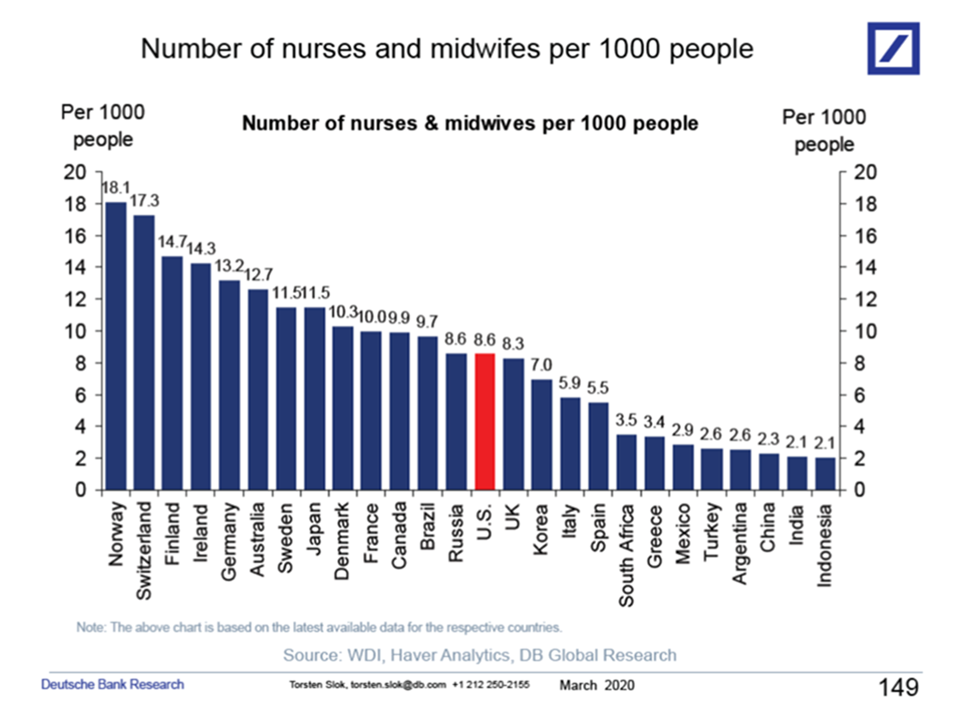

8.Great Charts From Torsten Slok on Doctors and Nurses.

The capacity of the healthcare system in different countries is becoming very important, see charts below and also the piece here from my colleagues in healthcare research: Cross Healthcare Research – DB’s Initial Covid-19 Projections

———————————————–

Let us know if you would like to add a colleague to this distribution list.

Torsten Sløk, Ph.D.

Chief Economist

9.Mortgage rates increased

By Jacob Passy

The rise in mortgage rates had nothing to do with markets and everything to do with lenders

Rates on 30-year mortgages rose this past week as lenders grappled with a surge in refinance demand.

Even as concerns mounted regarding the coronavirus pandemic, mortgage rates increased this past week as lenders sought to stem the tide of people looking to refinance their home loans.

The 30-year fixed-rate mortgage averaged 3.36% for the week ending March 12, up from 3.29% the previous week, Freddie Mac FMCC, -22.09% reported Thursday.

The 15-year fixed-rate mortgage, meanwhile, fell two basis points to an average of 2.77%. The 5-year Treasury-indexed adjustable-rate mortgage averaged 3.01%, down sharply from 3.18% last week.

Last week, 30-year fixed-rate mortgages hit an all-time low since Freddie Mac started tracking loan rates in 1971. That triggered an avalanche of mortgage applications from borrowers looking to lock in the lowest interest rates they’ve likely seen in their lifetimes. Refinancing volume hit its highest level since April 2009, the Mortgage Bankers Association reported Wednesday.

Mortgage rates were driven lower largely by the steady decline in bond yields in response to concerns about the economic impact the COVID-19 coronavirus outbreak would have. Mortgage rates typically track the yield on the 10-year Treasury note TMUBMUSD10Y, 0.846% , which actually touched an all-time low of 0.39% this past week.

So, why then did mortgage rates increase? That comes down to a lender’s capacity. Experts had warned that most lenders did not have the staff to handle an increase, in part because lenders had been letting go of employees in 2018 and 2019 in anticipation of higher rates causing lower demand for loans. “Most big lenders were scaling back their mortgage business,” said Vishal Garg, founder and CEO of Better.com, an online direct mortgage lender.

‘Each employee is processing 2.5 to 3 times as many loans as they were a year ago.’

— Tendayi Kapfidze, chief economist at LendingTree

Without the staff to handle the deluge of applications, lenders are facing an uphill battle to close loans. Some companies are now offering rate locks as long as 100 days, in anticipation of how long it may take to close loans at the moment, said Tendayi Kapfidze, chief economist at LendingTree TREE, -10.58% .

“Basically, each employee is processing 2.5 to 3 times as many loans as they were a year ago,” he said. “That really tells you the kind of jam lenders are in.”

Therefore, lenders have turned to the main tool in the arsenal to reduce demand: Rates. Many major lenders have opted to increase rates in an effort to dissuade people from applying for mortgages right now and give them a chance to work through the applications they’ve already received.

Read more:As recession fears mount, here’s why home prices may not plunge alongside the stock market

But those who are looking to buy a home or refinance their existing mortgage who have not applied yet need not despair. The Mortgage Bankers Association now expects that lenders will write $1.2 trillion in refinances this year, double its previous forecast. That would represent the largest volume of refinances since 2012. Therefore, economists expect that rates will remain low, and possibly go down again, for the foreseeable future.

“All else equal, if refinancing activity begins to slow, then rates will almost certainly trend back down,” said Zillow ZG, -14.93% economist Matthew Speakman.

“But of course, all else is not equal, and markets are now in the midst of their most tumultuous stretch since the financial crisis,” Speakman added. “More dramatic moves for mortgage rates appear likely, as investors continue to try and best position themselves to deal with the challenges posed by this environment.”

Analysts have said that the housing industry could be a bright spot amidst the turmoil that has sent the Dow Jones Industrial Average DJIA, -9.98%, S&P 500 SPX, -9.51% and Nasdaq COMP, -9.43% into bear-market territory, but much will depend on whether the outbreak rattles consumer confidence to the point where people refrain from buying homes.

10.3 Core Critical Thinking Skills Every Thinker Should Have

Christopher Dwyer Ph.D.

Critically thinking about critical thinking skills

I recently received an email from an educator friend, asking me to briefly describe the skills necessary for critical thinking. They were happy to fill-in-the-blanks themselves from outside reading; but, wanted to know what specific skills they should focus on teaching their students. I took this as a good opportunity to dedicate a blog entry here to such discussion, in order to provide my friend and any other interested parties with an overview.

To understand critical thinking skills and how they factor into critical thinking, one first needs a definition of the latter. Critical thinking (CT) is a metacognitive process, consisting of a number of skills and dispositions, that when used through self-regulatory reflective judgment, increases the chances of producing a logical conclusion to an argument or solution to a problem (Dwyer, 2017; Dwyer, Hogan & Stewart, 2014). On the surface, this definition clarifies two issues: first, critical thinking is metacognitive – simply, it requires the individual to think about thinking; second, its main components are reflective judgment, dispositions and skills. Below the surface, this description requires clarification; hence the impetus for this entry – what is meant by reflective judgment, disposition towards CT and CT skills? Reflective judgment (i.e. an individuals’ understanding of the nature, limits, and certainty of knowing and how this can affect their judgments [King & Kitchener, 1994]) and disposition towards CT (i.e. an inclination, tendency or willingness to perform a given thinking skill [Dwyer, 2017; Facione, Facione & Giancarlo, 1997; Ku, 2009; Norris, 1992; Siegel, 1999; Valenzuela, Nieto & Saiz, 2011]) have both already been covered on this blog; so, consistent with the aim of this piece, let’s discuss CT skills.

CT skills allow individuals to transcend lower-order, memorization-based learning strategies to gain a more complex understanding of the information or problems they encounter (Halpern, 2014). Though debate is ongoing over the definition of CT, one list stands out as a reasonable consensus conceptualization of CT skills. In 1988, a committee of forty-six experts in the field of CT gathered to discuss CT conceptualisations, resulting in the Delphi Report; within which was overwhelmingly agreement (i.e. 95% consensus) that analysis, evaluation and inference were the core skills necessary for CT (Facione, 1990). Indeed, over 30 years later, these three CT skills remain the most commonly cited.

1. Analysis

Analysis is a core CT skill used to identify and examine the structure of an argument, the propositions within an argument and the role they play (e.g. the main conclusion, the premises and reasons provided to support the conclusion, objections to the conclusion and inferential relationships among propositions), as well as the sources of the propositions (e.g. personal experience, common belief and research). When it comes to analysing the basis for a standpoint, the structure of the argument can be extracted for subsequent evaluation (e.g. from dialogue and text). This can be accomplished through looking for propositions that either support or refute the central claim or other reasons and objections. Through analysis, the argument’s hierarchical structure begins to appear. Notably, argument mapping can aid the visual representation of this hierarchical structure and is supported by research as having positive effects on critical thinking (Butchart et al., 2009; Dwyer, 2011; Dwyer, Hogan & Stewart, 2012; van Gelder, Bisset & Cumming, 2004).

2. Evaluation

Evaluation is a core CT skill that is used in the assessment of propositions and claims (identified through the previous analysis) with respect to their credibility; relevance; balance, bias (and potential omissions); as well as the logical strength amongst propositions (i.e. the strength of the inferential relationships). Such assessment allows for informed judgment regarding the overall strength or weakness of an argument (Dwyer, 2017; Facione, 1990). If an argument (or its propositions) is not credible, relevant, logical and unbiased, you should consider excluding it or discussing its weaknesses as an objection.

article continues after advertisement

Evaluating the credibility of claims and arguments involves progressing beyond merely identifying the source of propositions in an argument, to actually examining the ‘trustworthiness’ of those identified sources (e.g. personal experiences, common beliefs/opinions, expert/authority opinion and scientific evidence). This is particularly important because some sources are more credible than others. Evaluation also implies deep consideration of the relevance of claims within an argument, which is accomplished by assessing the contextual relevance of claims and premises – that is, the pertinence or applicability of one proposition to another.

With respect to balance, bias (and potential omissions), it’s important to consider the ‘slant’ of an argument – if it seems imbalanced in favour of one line of thinking, then it’s quite possible that the argument has omitted key, opposing points that should also be considered. Imbalance may also very well imply some level of bias in the argument – another factor that should also be assessed. However, just because an argument is balanced does not mean that it isn’t biased. It may very well be the case that the ‘opposing views’ presented have been ‘cherry-picked’ because they are easily disputed (akin to building a strawman); thus, making supporting reasons appear stronger than they may actually be – and this is just one example of how a balanced argument may, in fact, be biased. The take home message regarding balance, bias and potential omissions should be that, in any argument, you should construct an understanding of the author or speaker’s motivations and consider how these might influence the structure and contents of the argument.

Finally, evaluating the logical strength of an argument is accomplished through monitoring both the logical relationships amongst propositions and the claims they infer. Assessment of logical strength can actually be aided through subsequent inference, as a means of double-checking the logical strength. For example, this can be checked by asking whether or not a particular proposition can actually be inferred based on the propositions that precede it. A useful means of developing this sub-skill is through practicing syllogistic reasoning.

3. Inference

Similar to other educational concepts like synthesis (e.g., see Bloom et al., 1956; Dwyer, 2011; 2017), the final core CT skill, inference, involves the “gathering” of credible, relevant and logical evidence based on the previous analysis and evaluation, for the purpose of drawing a reasonable conclusion (Dwyer, 2017; Facione, 1990). Drawing a conclusion always implies some act of synthesis (i.e. the ability to put parts of information together to form a new whole; see Dwyer, 2011). However, inference is a unique form of synthesis in that it involves the formulation of a set of conclusions derived from a series of arguments or a body of evidence. This inference may imply accepting a conclusion pointed to by an author in light of the evidence they present, or ‘conjecturing an alternative’, equally logical, conclusion or argument based on the available evidence (Facione, 1990). The ability to infer a conclusion in this manner can be completed through formal logic strategies, informal logic strategies (or both) in order to derive intermediate conclusions, as well as central claims.

article continues after advertisement

Another important aspect of inference involves the querying of available evidence, for example, by recognising the need for additional information, gathering it and judging the plausibility of utilising such information for the purpose of drawing a conclusion. Notably, in the context of querying evidence and conjecturing alternative conclusions, inference overlaps with evaluation to a certain degree in that both skills are used to judge the relevance and acceptability of a claim or argument. Furthermore, after inferring a conclusion, the resulting argument should be re-evaluated to ensure that it is reasonable to draw the conclusion that was derived.

Conclusion

Overall, the application of critical thinking skills is a process – one must analyse, evaluate and then infer; and this process can be repeated to ensure that a reasonable conclusion has been drawn. In an effort to simplify the description of this process, for the past few years, I’ve used the analogy of picking apples for baking. We begin by picking apples from a tree. Consider the tree as an analogy, in its own right, for an argument, which is often hierarchically structured like a tree-diagram. By picking apples, I mean identifying propositions and the role they play (i.e. analysis). Once we pick an apple, we evaluate it – we make sure it isn’t rotten (i.e. lacks credibility, is biased) and is suitable for baking (i.e. relevant and logically strong). Finally, we infer – we gather the apples in a basket and bring them home and group them together based on some rationale for construction – maybe four for a pie, three for a crumble and another four for a tart. By the end of the process, we have baked some apple-based goods, or developed a conclusion, solution or decision through critical thinking.

Of course there is more to critical thinking than the application of skills – a critical thinker must also have the disposition to think critically and engage reflective judgment. However, without the appropriate skills – analysis, evaluation and inference, it is not likely that CT will be applied. For example, though one might be willing to use CT skills and engage reflective judgment, they may not know how to do so. Conversely, though one might be aware of which CT skills to use in a given context and may have the capacity to perform well when using these skills, they may not be disposed to use them (Valenzuela, Nieto & Saiz, 2011). Though the core CT skills of analysis, evaluation and inference are not the only important aspects of CT, they are essential for its application.