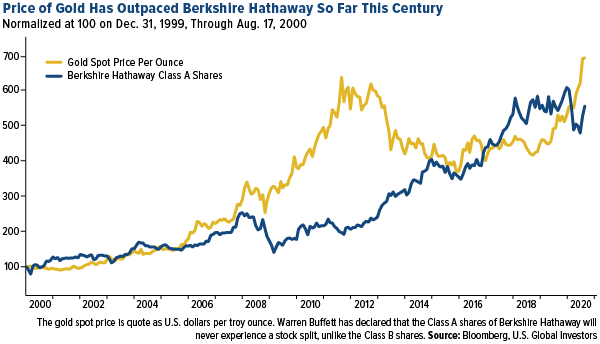

1. Gold Has Beat Buffett Berkshire Since 2000.

And Just Like That, Buffett Likes Gold by Frank Holmes of U.S. Global Investors,

2. Tesla Valued at $1 Million Per Vehicle vs. GM < $10,000 Per Vehicle.

Barrons

- Tesla is valued at, roughly, $1 million per vehicle delivered—and we’d rather let the trade play out heading into this week’s stock split than jump in right now.

- General Motors, on the other hand, is valued at less than $10,000 per car delivered, less than 1/100th of Tesla’s valuation, after dropping 21% this year. That’s far worse than the returns of the S&P 500 and Dow Jones Industrial Average.

Now Even a Tesla Dating App

If someone purchasing a top-of-the-line Tesla Model X a year ago had instead bought the company’s shares, he or she would be sitting on a paper profit of three-quarters of a million dollars by now. But then, while money can’t buy you love, that Tesla might.

Owners of a car that regularly needs to be hooked up to an outlet have just as much trouble hooking up as the rest of us. Now a new dating service, the Tesla Dating Co., seeks to make it easier.

“It became a big part of their identity,” says Ajitpal Grewal, the Canadian e-commerce entrepreneur who is developing the app. “Suddenly it hit me: These people would be perfect for each other.”

The site requires applicants to prove Tesla ownership before joining. Yet Chief Executive Officer Elon Musk, the man who named his four vehicle models so that they would spell “S-3-X-Y,” has no affiliation with Mr. Grewal’s venture

It is hard to imagine a similar app for, say, Fords or Toyotas, but then how many owners of those cars can name the chief executive of the manufacturer, much less worship him? This one describes itself as being for an “exclusive community of like-minded Elon stans…the kind of people that really understand you.”

Tesla Owners Can Find Their Electric Flame–A new dating app exclusively for Tesla owners helps the eco-conscious hook up with something other than a power outlet

3. Bank Stocks 0.9 times Estimated price to book(P/B) Versus a low of 0.6 Times During the Global Financial Crisis in Early 2009 and an Average of 1.1 Times Since 2005

Stone’s Weekly Market Guide– Bill Stone

Chart of the Week: Banks within the S&P 500 have recently begun to outperform the S&P 500 with the relative performance bottoming on August 6th. Interestingly, the outperformance coincided with the better than expected July jobs report and the low in 10-year U.S. Treasury yields. Not surprisingly, the bank index is typically positively correlated with Treasury yields but the correlation has been rising since the S&P 500 bottom in March (see chart). The July payrolls report, which reflected an almost 1.6 million increase in jobs, was a significant positive surprise with the U.S. economy losing some momentum due to the increase in COVID infections and some economists expecting further job losses. Outperformance of the banks has also helped spark outperformance from the value versus growth indexes, which also bottomed on August 6th. With the financial sector comprising 18.6% of the Russell 1000 Value index versus 10.0% of the S&P 500, the value outperformance is logical. Value strategies in general have been outperforming since at least early August although banks are certainly not the only reason for value outperformance. In our view the improved economic outlook, as signaled by the payrolls report, has helped drive the turn in value and smaller-cap stocks. With the benefit of some lucky timing and extreme relative valuations, we highlighted the opportunity in value and smaller stocks in our report on August 3. If in fact the economy continues to mend, bank stocks continue to look interesting at less than 0.9 times estimated price to book(P/B) versus a low of 0.6 times during the global financial crisis in early 2009 and an average of 1.1 times since 2005. The estimated dividend yield is also enticing at almost 3.6% if dividends remain unaffected by the need to conserve capital for loan losses.

S&P 500 Banks: Correlation, Valuation and Dividend Yield

4. New York Ultra Luxury Real Estate Seeing 50% Price Drops.

WSJ By Katherine Clarke–The Covid-19 crisis has delivered a stunning gut-punch to the New York City luxury real-estate market, applying downward pressure at a rate that surpasses both the 2008 financial crisis and the period immediately following the 9/11 terrorist attacks. In the West Chelsea district, a recently built ultra high-end boutique condominium known as the Getty slashed prices for its remaining units by as much as 46%. One full-floor, four-bedroom apartment at the Peter Marino-designed building was lowered to $10.475 million from $19.5 million.

Covid-19 Pounds New York Real Estate Worse Than 9/11, Financial Crash

The city’s high-end market was dealt an unprecedented blow by the coronavirus lockdown. Can it ever fully recover?

NYC Real Estate chart https://www.wsj.com/articles/covid-19-new-york-real-estate-11597939146?mod=itp_wsj&ru=yahoo

Movers in N.Y.C. Are So Busy They’re Turning People Away

With so many people fleeing the city, moving companies can barely keep up with the demand. By Julie Satow

o Squeezing a 350-pound sofa down four flights of a narrow prewar staircase isn’t easy on the best of days. Doing so in a heat wave while wearing a mask is a lot harder.

“Sweat is dripping down your face, it slips,” said Vladislav Grigor, a foreman and dispatcher at Empire Movers in Manhattan. “It is just terrible.”

While the work can be merciless, movers are busy this season, and glad of it.

For Mr. Grigor and his colleagues, it is fair to say this summer has been like no other. Not only is he having to meet the strenuous physical demands of his job during a steamy summer, but he is also having to do so while abiding by the new rules of social distancing.

On top of these challenges is just how overworked movers are. “It’s nuts out there,” Mr. Grigor said. “There is double the volume of customers — maybe more — than last year.”

According to FlatRate Moving, the number of moves it has done has increased more than 46 percent between March 15 and August 15, compared with the same period last year. The number of those moving outside of New York City is up 50 percent — including a nearly 232 percent increase to Dutchess County and 116 percent increase to Ulster County in the Hudson Valley.

5. Bus Companies Ferry 600 Million Passengers a Year vs. 700 Million for Domestic Airlines.

Bus companies, which every year shuttle hundreds of millions of Americans, most of them working class, are being forced by the pandemic to suspend service and close shop while trains and airlines stay afloat with federal aid.In the last round of stimulus grants and loans, airlines got $50 billion, Amtrak $1 billion, public transit agencies $25 billion and private bus companies no direct aid, said Peter Pantuso, president of the American Bus Association. “I don’t know how Congress can justify leaving us behind again.”

Bus companies ferry 600 million passengers a year, not far from the 700 million domestic airline passengers. They are asking for $10 billion through the Coronavirus Economic Relief for Transportation Act, introduced by Senators Jack Reed, a Rhode Island Democrat, and Susan Collins, Republican of Maine, in July but stuck in negotiations.

“Congress is feeling the heat to prevent a collapse of the entire sector,” said Joseph Schwieterman, a professor at DePaul University who specializes in transportation and urban planning. “There was such a mad rush with the first stimulus bill to save big companies that bus companies were lumped together with other small businesses.”

Bus Firms Fold as Pleas for Aid Go Unanswered, Stranding NeedyBy Emmy Lucas

Half of Russians would emigrate

6. Shorts Against U.S. Stocks Disappear as FOMO Sets In……

From Dave Lutz at Jones Trading

Short positions in US stocks have dropped to their lowest level in more than a decade, as this year’s record-breaking rally inflicts big losses on investors seeking to profit from declining share prices – Short interest as a proportion of market capitalization for the median stock in the S&P 500 index fell to 1.8 per cent at the beginning of this month, the lowest since 2004. That compares to 2 per cent at the start of the year, and an average of 2.4 per cent over the past 15 years – For tech and health stocks, the year’s best performing sectors, short positions relative to market value now stand at or close to the lowest level for the period, FT reports.

7. 20 Largest 5-Year Losses…Energy Dominates.

The Capital Spectator–Investing, Asset Allocation, Economics & The Search For The Bottom Line

Found at www.abnormalreturns.com

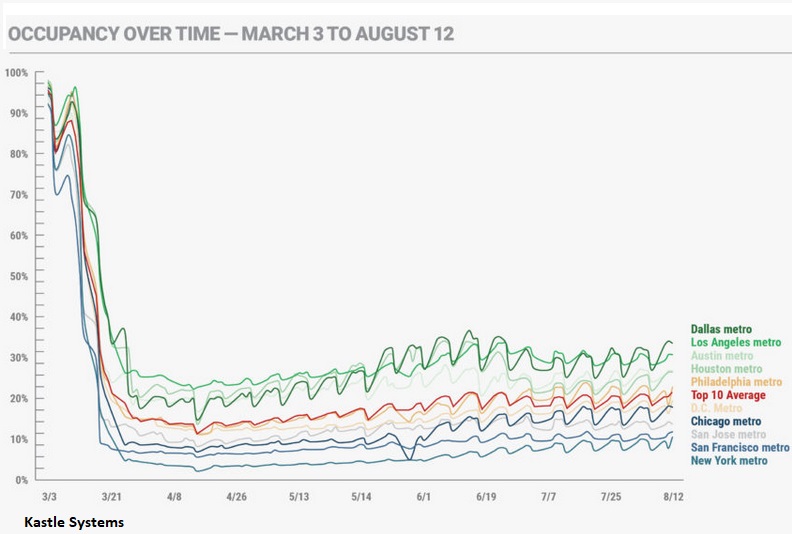

8. Occupancy of Offices in Major Cities.

On Tuesday, August 18, during morning rush hour, I walked through and around the Financial District of San Francisco and took photos to document the spookiness of it all. Pedestrians used to rush to work on crowded sidewalks, balling up at red lights, then stream across the intersection, and disappear into the entries of office towers as they went, and cars used to be stuck in traffic, and thick throngs of people would pour out of the Montgomery BART and Muni Metro station.

I started taking photos at Columbus Street where it ends at Montgomery Street, and then turned south into Montgomery Street and walked through the Financial District to the Montgomery Station at Market Street. Then I zigzagged back through the Financial District.

What you will see are streets and sidewalks and entrances into office towers that were eerily deserted during what used to be “rush hour,” with just a sprinkling of pedestrians, a few cars, the occasional skateboarder, some guys working on construction projects, and curiosities where you might be tempted to think, “only in San Francisco.”

With hindsight, it was the last beautiful sunny morning before the thick acrid smoke from the wildfires moved into San Francisco.

The data of how work-from-home impacts office patterns in a city like San Francisco are grim. According to Kastle Systems – which provides access systems for 3,600 buildings and 41,000 businesses in 47 states, and therefore has a large sample of how many people are entering offices during the Pandemic – office occupancy in San Francisco was still only at 13.6% of where it had been at the beginning of March, meaning it was still down by 86.4%, just above New York City:

Haunting Photos of San Francisco’s Desolate Financial District During Morning “Rush Hour”: Visual Effects of Work-from-Homeby Wolf Richter • Aug 22, 2020

9. Buffett Indicator Blows Thru 1999 Highs In Middle of Pandemic….Market Cap to GDP Chart.

By Shawn Langlois https://www.marketwatch.com/story/market-timing-when-clocks-have-no-hands-warren-buffetts-warning-is-as-relevant-now-as-it-was-in-2000-2020-08-23?mod=home-page

10. How To Be Successful—Sam Altman

I’ve observed thousands of founders and thought a lot about what it takes to make a huge amount of money or to create something important. Usually, people start off wanting the former and end up wanting the latter.

Here are 13 thoughts about how to achieve such outlier success. Everything here is easier to do once you’ve already reached a baseline degree of success (through privilege or effort) and want to put in the work to turn that into outlier success. [1] But much of it applies to anyone.

1. Compound yourself

Compounding is magic. Look for it everywhere. Exponential curves are the key to wealth generation.

A medium-sized business that grows 50% in value every year becomes huge in a very short amount of time. Few businesses in the world have true network effects and extreme scalability. But with technology, more and more will. It’s worth a lot of effort to find them and create them.

You also want to be an exponential curve yourself—you should aim for your life to follow an ever-increasing up-and-to-the-right trajectory. It’s important to move towards a career that has a compounding effect—most careers progress fairly linearly.

You don’t want to be in a career where people who have been doing it for two years can be as effective as people who have been doing it for twenty—your rate of learning should always be high. As your career progresses, each unit of work you do should generate more and more results. There are many ways to get this leverage, such as capital, technology, brand, network effects, and managing people.

It’s useful to focus on adding another zero to whatever you define as your success metric—money, status, impact on the world, or whatever. I am willing to take as much time as needed between projects to find my next thing. But I always want it to be a project that, if successful, will make the rest of my career look like a footnote.

Most people get bogged down in linear opportunities. Be willing to let small opportunities go to focus on potential step changes.

I think the biggest competitive advantage in business—either for a company or for an individual’s career—is long-term thinking with a broad view of how different systems in the world are going to come together. One of the notable aspects of compound growth is that the furthest out years are the most important. In a world where almost no one takes a truly long-term view, the market richly rewards those who do.

Trust the exponential, be patient, and be pleasantly surprised.

2. Have almost too much self-belief

Self-belief is immensely powerful. The most successful people I know believe in themselves almost to the point of delusion.

Cultivate this early. As you get more data points that your judgment is good and you can consistently deliver results, trust yourself more.

If you don’t believe in yourself, it’s hard to let yourself have contrarian ideas about the future. But this is where most value gets created.

I remember when Elon Musk took me on a tour of the SpaceX factory many years ago. He talked in detail about manufacturing every part of the rocket, but the thing that sticks in memory was the look of absolute certainty on his face when he talked about sending large rockets to Mars. I left thinking “huh, so that’s the benchmark for what conviction looks like.”

Managing your own morale—and your team’s morale—is one of the greatest challenges of most endeavors. It’s almost impossible without a lot of self-belief. And unfortunately, the more ambitious you are, the more the world will try to tear you down.

Most highly successful people have been really right about the future at least once at a time when people thought they were wrong. If not, they would have faced much more competition.

Self-belief must be balanced with self-awareness. I used to hate criticism of any sort and actively avoided it. Now I try to always listen to it with the assumption that it’s true, and then decide if I want to act on it or not. Truth-seeking is hard and often painful, but it is what separates self-belief from self-delusion.

This balance also helps you avoid coming across as entitled and out of touch.

3. Learn to think independently

Entrepreneurship is very difficult to teach because original thinking is very difficult to teach. School is not set up to teach this—in fact, it generally rewards the opposite. So you have to cultivate it on your own.

Thinking from first principles and trying to generate new ideas is fun, and finding people to exchange them with is a great way to get better at this. The next step is to find easy, fast ways to test these ideas in the real world.

“I will fail many times, and I will be really right once” is the entrepreneurs’ way. You have to give yourself a lot of chances to get lucky.

One of the most powerful lessons to learn is that you can figure out what to do in situations that seem to have no solution. The more times you do this, the more you will believe it. Grit comes from learning you can get back up after you get knocked down.

4. Get good at “sales”

Self-belief alone is not sufficient—you also have to be able to convince other people of what you believe.

All great careers, to some degree, become sales jobs. You have to evangelize your plans to customers, prospective employees, the press, investors, etc. This requires an inspiring vision, strong communication skills, some degree of charisma, and evidence of execution ability.

Getting good at communication—particularly written communication—is an investment worth making. My best advice for communicating clearly is to first make sure your thinking is clear and then use plain, concise language.

The best way to be good at sales is to genuinely believe in what you’re selling. Selling what you truly believe in feels great, and trying to sell snake oil feels awful.

Getting good at sales is like improving at any other skill—anyone can get better at it with deliberate practice. But for some reason, perhaps because it feels distasteful, many people treat it as something unlearnable.

My other big sales tip is to show up in person whenever it’s important. When I was first starting out, I was always willing to get on a plane. It was frequently unnecessary, but three times it led to career-making turning points for me that otherwise would have gone the other way.

5. Make it easy to take risks

Most people overestimate risk and underestimate reward. Taking risks is important because it’s impossible to be right all the time—you have to try many things and adapt quickly as you learn more.

It’s often easier to take risks early in your career; you don’t have much to lose, and you potentially have a lot to gain. Once you’ve gotten yourself to a point where you have your basic obligations covered you should try to make it easy to take risks. Look for small bets you can make where you lose 1x if you’re wrong but make 100x if it works. Then make a bigger bet in that direction.

Don’t save up for too long, though. At YC, we’ve often noticed a problem with founders that have spent a lot of time working at Google or Facebook. When people get used to a comfortable life, a predictable job, and a reputation of succeeding at whatever they do, it gets very hard to leave that behind (and people have an incredible ability to always match their lifestyle to next year’s salary). Even if they do leave, the temptation to return is great. It’s easy—and human nature—to prioritize short-term gain and convenience over long-term fulfillment.

But when you aren’t on the treadmill, you can follow your hunches and spend time on things that might turn out to be really interesting. Keeping your life cheap and flexible for as long as you can is a powerful way to do this, but obviously comes with tradeoffs.

6. Focus

Focus is a force multiplier on work.

Almost everyone I’ve ever met would be well-served by spending more time thinking about what to focus on. It is much more important to work on the right thing than it is to work many hours. Most people waste most of their time on stuff that doesn’t matter.

Once you have figured out what to do, be unstoppable about getting your small handful of priorities accomplished quickly. I have yet to meet a slow-moving person who is very successful.

7. Work hard

You can get to about the 90th percentile in your field by working either smart or hard, which is still a great accomplishment. But getting to the 99th percentile requires both—you will be competing with other very talented people who will have great ideas and be willing to work a lot.

Extreme people get extreme results. Working a lot comes with huge life trade-offs, and it’s perfectly rational to decide not to do it. But it has a lot of advantages. As in most cases, momentum compounds, and success begets success.

And it’s often really fun. One of the great joys in life is finding your purpose, excelling at it, and discovering that your impact matters to something larger than yourself. A YC founder recently expressed great surprise about how much happier and more fulfilled he was after leaving his job at a big company and working towards his maximum possible impact. Working hard at that should be celebrated.

It’s not entirely clear to me why working hard has become a Bad Thing in certain parts of the US, but this is certainly not the case in other parts of the world—the amount of energy and drive exhibited by entrepreneurs outside of the US is quickly becoming the new benchmark.

You have to figure out how to work hard without burning out. People find their own strategies for this, but one that almost always works is to find work you like doing with people you enjoy spending a lot of time with.

I think people who pretend you can be super successful professionally without working most of the time (for some period of your life) are doing a disservice. In fact, work stamina seems to be one of the biggest predictors of long-term success.

One more thought about working hard: do it at the beginning of your career. Hard work compounds like interest, and the earlier you do it, the more time you have for the benefits to pay off. It’s also easier to work hard when you have fewer other responsibilities, which is frequently but not always the case when you’re young.

8. Be bold

I believe that it’s easier to do a hard startup than an easy startup. People want to be part of something exciting and feel that their work matters.

If you are making progress on an important problem, you will have a constant tailwind of people wanting to help you. Let yourself grow more ambitious, and don’t be afraid to work on what you really want to work on.

If everyone else is starting meme companies, and you want to start a gene-editing company, then do that and don’t second guess it.

Follow your curiosity. Things that seem exciting to you will often seem exciting to other people too.

9. Be willful

A big secret is that you can bend the world to your will a surprising percentage of the time—most people don’t even try, and just accept that things are the way that they are.

People have an enormous capacity to make things happen. A combination of self-doubt, giving up too early, and not pushing hard enough prevents most people from ever reaching anywhere near their potential.

Ask for what you want. You usually won’t get it, and often the rejection will be painful. But when this works, it works surprisingly well.

Almost always, the people who say “I am going to keep going until this works, and no matter what the challenges are I’m going to figure them out”, and mean it, go on to succeed. They are persistent long enough to give themselves a chance for luck to go their way.

Airbnb is my benchmark for this. There are so many stories they tell that I wouldn’t recommend trying to reproduce (keeping maxed-out credit cards in those nine-slot three-ring binder pages kids use for baseball cards, eating dollar store cereal for every meal, battle after battle with powerful entrenched interest, and on and on) but they managed to survive long enough for luck to go their way.

To be willful, you have to be optimistic—hopefully this is a personality trait that can be improved with practice. I have never met a very successful pessimistic person.

10. Be hard to compete with

Most people understand that companies are more valuable if they are difficult to compete with. This is important, and obviously true.

But this holds true for you as an individual as well. If what you do can be done by someone else, it eventually will be, and for less money.

The best way to become difficult to compete with is to build up leverage. For example, you can do it with personal relationships, by building a strong personal brand, or by getting good at the intersection of multiple different fields. There are many other strategies, but you have to figure out some way to do it.

Most people do whatever most people they hang out with do. This mimetic behavior is usually a mistake—if you’re doing the same thing everyone else is doing, you will not be hard to compete with.

11. Build a network

Great work requires teams. Developing a network of talented people to work with—sometimes closely, sometimes loosely—is an essential part of a great career. The size of the network of really talented people you know often becomes the limiter for what you can accomplish.

An effective way to build a network is to help people as much as you can. Doing this, over a long period of time, is what lead to most of my best career opportunities and three of my four best investments. I’m continually surprised how often something good happens to me because of something I did to help a founder ten years ago.

One of the best ways to build a network is to develop a reputation for really taking care of the people who work with you. Be overly generous with sharing the upside; it will come back to you 10x. Also, learn how to evaluate what people are great at, and put them in those roles. (This is the most important thing I have learned about management, and I haven’t read much about it.) You want to have a reputation for pushing people hard enough that they accomplish more than they thought they could, but not so hard they burn out.

Everyone is better at some things than others. Define yourself by your strengths, not your weaknesses. Acknowledge your weaknesses and figure out how to work around them, but don’t let them stop you from doing what you want to do. “I can’t do X because I’m not good at Y” is something I hear from entrepreneurs surprisingly often, and almost always reflects a lack of creativity. The best way to make up for your weaknesses is to hire complementary team members instead of just hiring people who are good at the same things you are.

A particularly valuable part of building a network is to get good at discovering undiscovered talent. Quickly spotting intelligence, drive, and creativity gets much easier with practice. The easiest way to learn is just to meet a lot of people, and keep track of who goes on to impress you and who doesn’t. Remember that you are mostly looking for rate of improvement, and don’t overvalue experience or current accomplishment.

I try to always ask myself when I meet someone new “is this person a force of nature?” It’s a pretty good heuristic for finding people who are likely to accomplish great things.

A special case of developing a network is finding someone eminent to take a bet on you, ideally early in your career. The best way to do this, no surprise, is to go out of your way to be helpful. (And remember that you have to pay this forward at some point later!)

Finally, remember to spend your time with positive people who support your ambitions.

12. You get rich by owning things

The biggest economic misunderstanding of my childhood was that people got rich from high salaries. Though there are some exceptions—entertainers for example —almost no one in the history of the Forbes list has gotten there with a salary.

You get truly rich by owning things that increase rapidly in value.

This can be a piece of a business, real estate, natural resource, intellectual property, or other similar things. But somehow or other, you need to own equity in something, instead of just selling your time. Time only scales linearly.

The best way to make things that increase rapidly in value is by making things people want at scale.

13. Be internally driven

Most people are primarily externally driven; they do what they do because they want to impress other people. This is bad for many reasons, but here are two important ones.

First, you will work on consensus ideas and on consensus career tracks. You will care a lot—much more than you realize—if other people think you’re doing the right thing. This will probably prevent you from doing truly interesting work, and even if you do, someone else would have done it anyway.

Second, you will usually get risk calculations wrong. You’ll be very focused on keeping up with other people and not falling behind in competitive games, even in the short term.

Smart people seem to be especially at risk of such externally-driven behavior. Being aware of it helps, but only a little—you will likely have to work super-hard to not fall in the mimetic trap.

The most successful people I know are primarily internally driven; they do what they do to impress themselves and because they feel compelled to make something happen in the world. After you’ve made enough money to buy whatever you want and gotten enough social status that it stops being fun to get more, this is the only force I know of that will continue to drive you to higher levels of performance.

This is why the question of a person’s motivation is so important. It’s the first thing I try to understand about someone. The right motivations are hard to define a set of rules for, but you know it when you see it.

Jessica Livingston and Paul Graham are my benchmarks for this. YC was widely mocked for the first few years, and almost no one thought it would be a big success when they first started. But they thought it would be great for the world if it worked, and they love helping people, and they were convinced their new model was better than the existing model.

Eventually, you will define your success by performing excellent work in areas that are important to you. The sooner you can start off in that direction, the further you will be able to go. It is hard to be wildly successful at anything you aren’t obsessed with.

One of the biggest reasons I’m excited about basic income is the amount of human potential it will unleash by freeing more people to take risks.

Until then, if you aren’t born lucky, you have to claw your way up for awhile before you can take big swings. If you are born in extreme poverty, then this is super difficult 🙁

It is obviously an incredible shame and waste that opportunity is so unevenly distributed. But I’ve witnessed enough people be born with the deck stacked badly against them and go on to incredible success to know it’s possible.

I am deeply aware of the fact that I personally would not be where I am if I weren’t born incredibly lucky.

Thanks to Brian Armstrong, Greg Brockman, Dalton Caldwell, Diane von Furstenberg, Maddie Hall, Drew Houston, Vinod Khosla, Jessica Livingston, Jon Levy, Luke Miles (6 drafts!), Michael Moritz, Ali Rowghani, Michael Seibel, Peter Thiel, Tracy Young and Shivon Zilis for reviewing drafts of this, and thanks especially to Lachy Groom for help writing it.

https://blog.samaltman.com/how-to-be-successful

Found at Barry Ritholtz Blog https://ritholtz.com/2020/08/weekend-reads-432/

Disclosure

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania..

To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results.

Material compiled by Lansing Street Advisors is based on publicly available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data.

Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only.