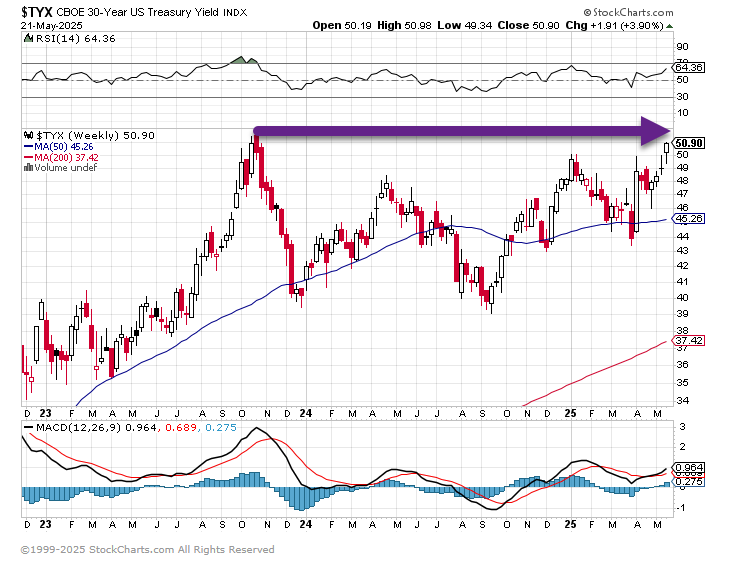

1. U.S. 30-Year Treasury Yield Close to Break-Out

StockCharts

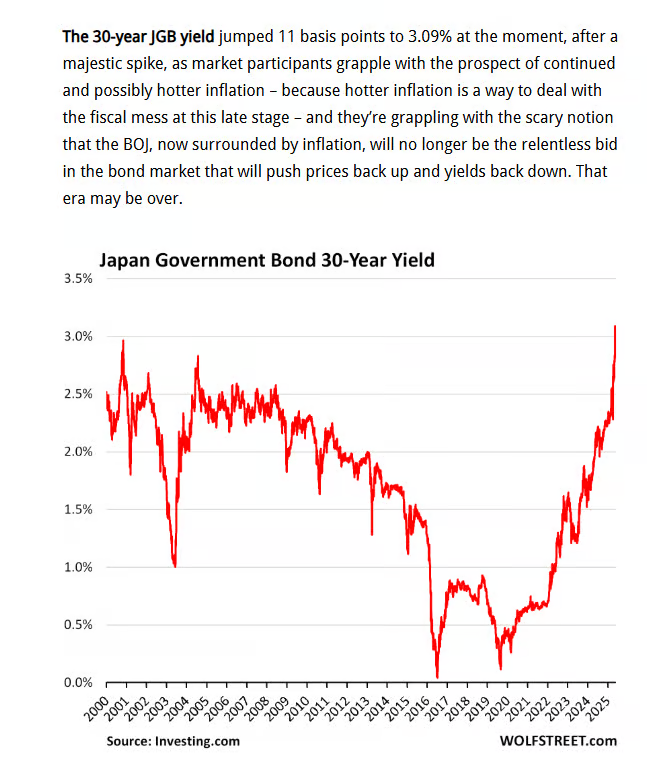

2. Japan 30-Year Bond Yield

Wolf Street

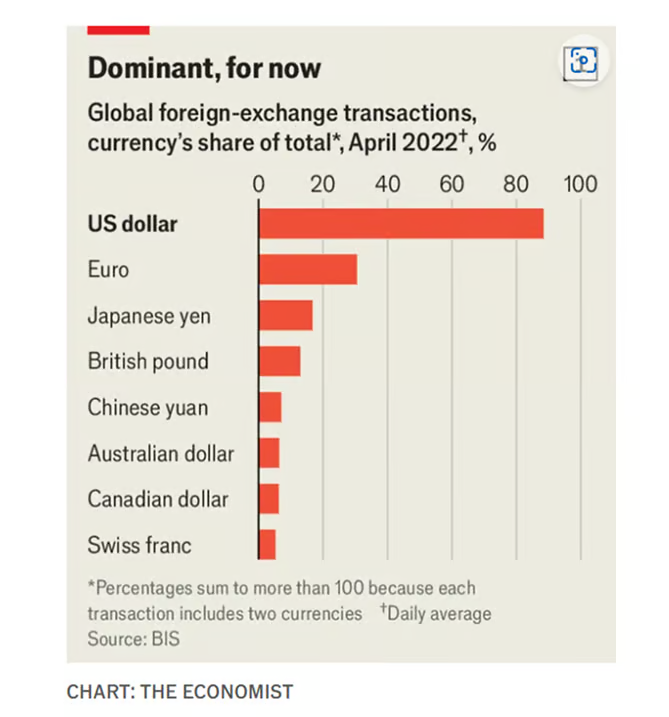

3. 85% of Global Foreign Exchange Transactions in U.S. Dollars

Cresset Capital

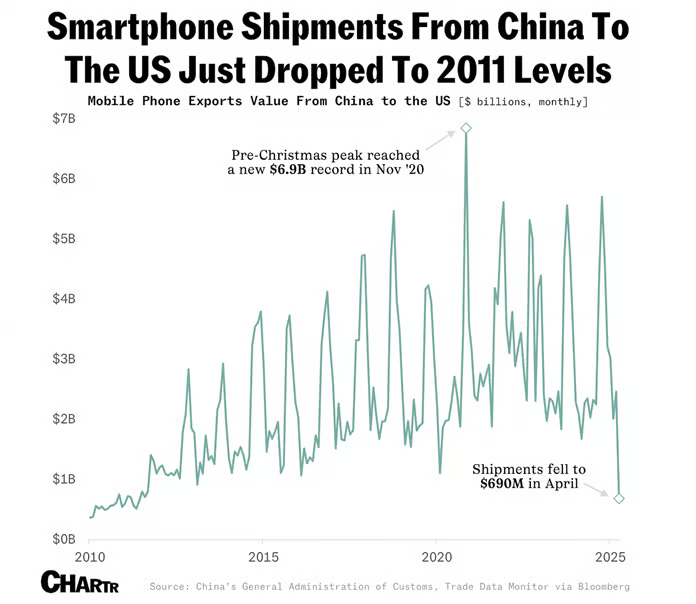

4. Smartphone Shipments to China Drop to 2011 Levels

Sherwood

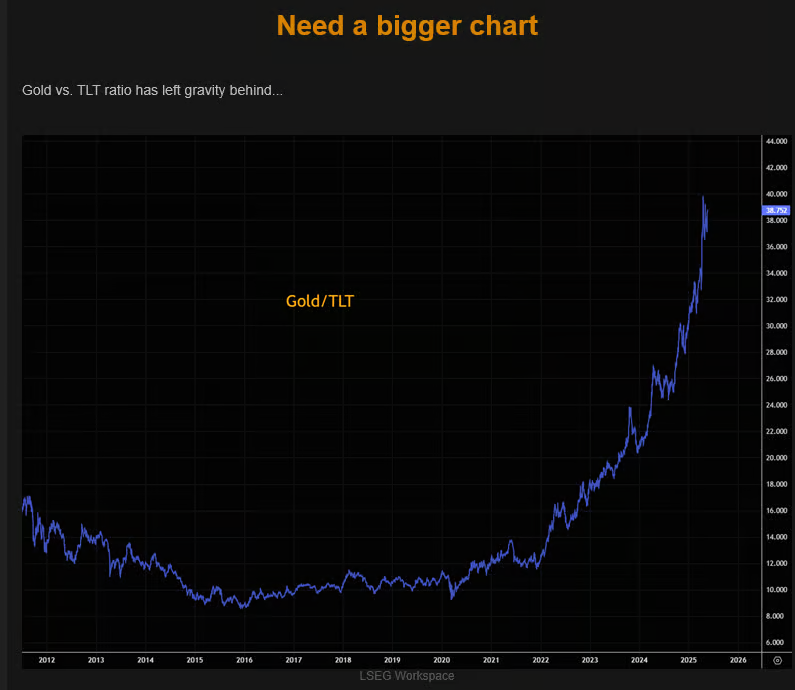

5. Gold vs. 20-Year Treasury Bond ETF

The Market Ear

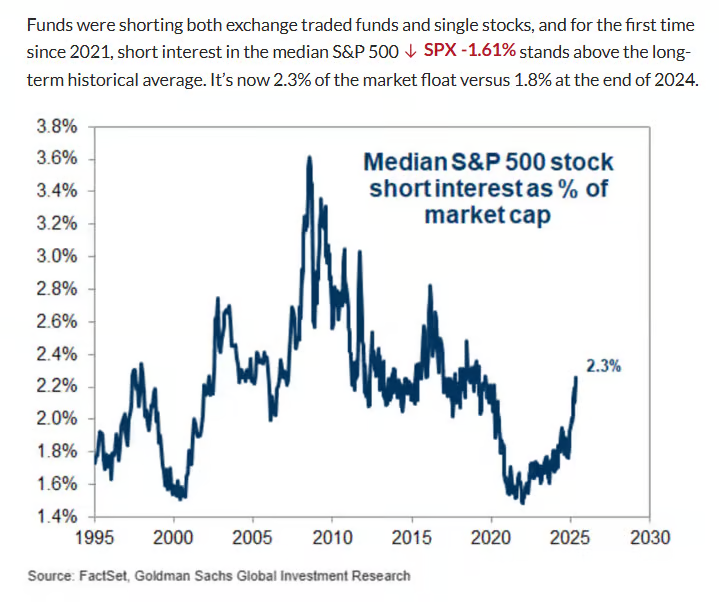

6. Hedge Funds Shorting Heavy Again

MarketWatch

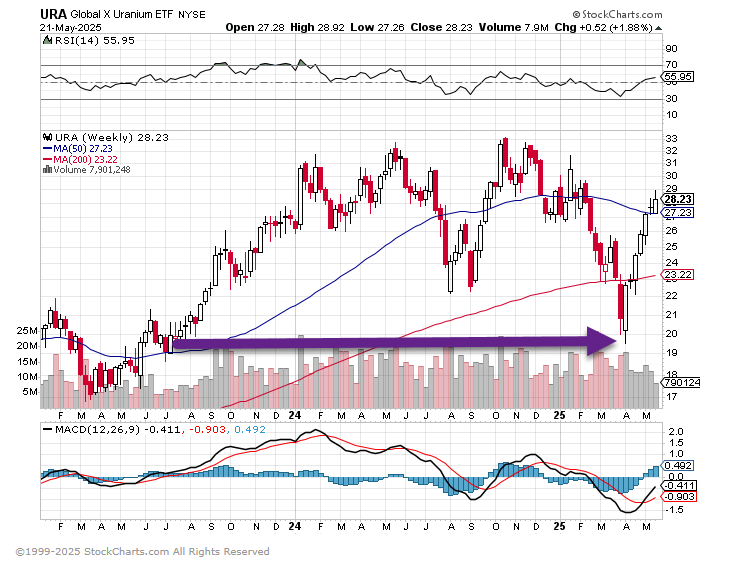

7. Uranium Held 2023 Low…+25% in One Month

StockCharts

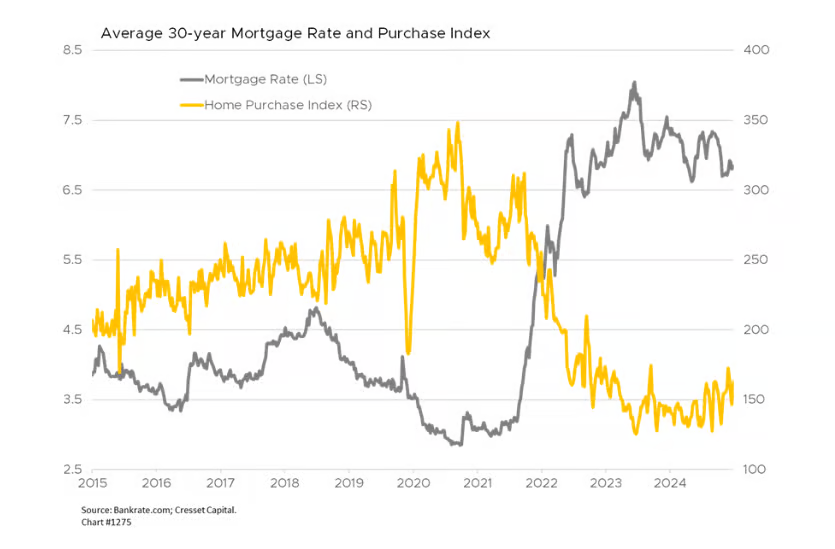

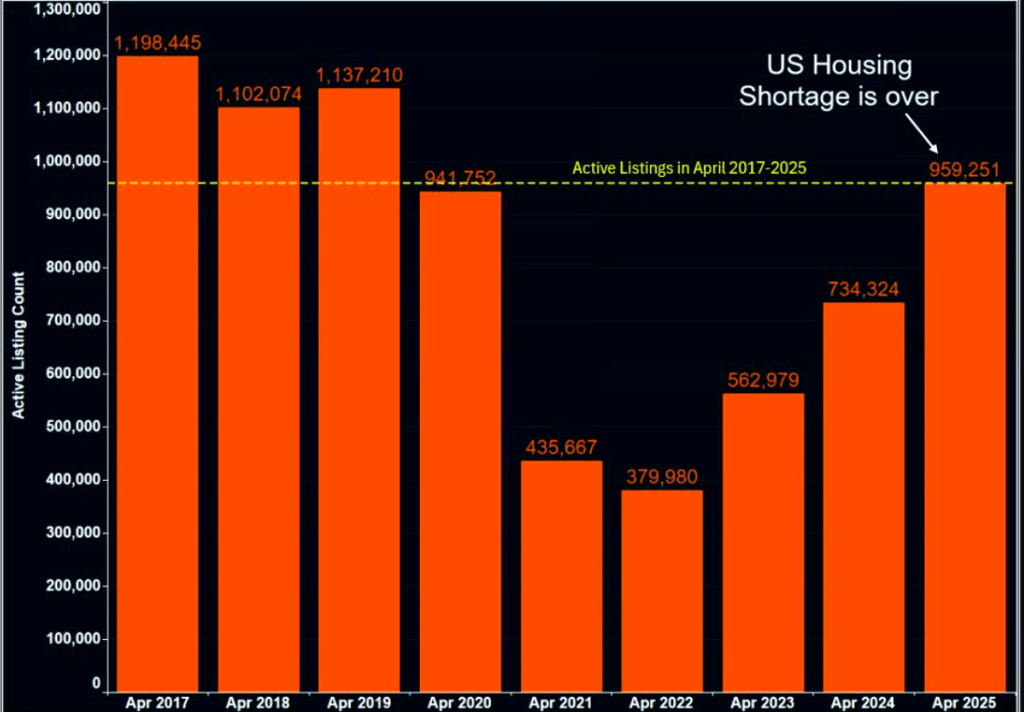

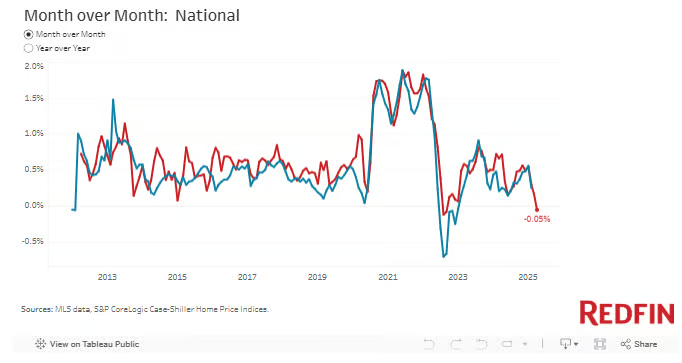

8. U.S. Housing Shortage Over? Listings Have Tripled Since 2022

Via Zach Goldberg Jefferies: With resale inventory on the U.S. Housing Market hitting nearly 1 million listings this spring. Listings bottomed in April 2022 at around 379k. Since then, they have nearly tripled. To the highest level of supply since 2019. Redfin: U.S. home prices ticked down -0.05% in April on a seasonally adjusted basis, the first month-over-month decline since September 2022 according to the Redfin Home Price Index (RHPI), which uses the repeat-sales pricing method to calculate seasonally adjusted changes in prices of single-family home. April marked only the third time that the RHPI has posted a month-over-month decline, with the other months—August and September in 2022—coming after a series of rapid interest rate rises. It’s worth noting that April’s decline (-0.05%, rounded to -0.1%) is minor and that RHPI data is subject to revision.

9. A 56-year-old Personal Trainer on how to Build Muscle after 40 — with Rucking, Bodyweight, and Short Workouts

- A personal trainer in his 50s got back in shape after colon cancer treatment with simple workouts.

- His routine includes rucking, walking with a weighted pack to build muscle and endurance in less time.

- He recommends shorter, more consistent workouts instead of exhausting yourself for long-term gains.

Via Business Insider: Shorter workouts could be the key to getting in shape and staying that way into your 50s and beyond, according to a personal trainer who learned to work smarter instead of harder.

Bill Maeda, 56, said recovering from a health crisis taught him that short, simple, and consistent is key to building muscle and fitness long-term.

“My raw horsepower is less than it was 10 or more years ago, but I don’t care,” he told. “The difference is now, I’m moving better, and it’s fun.”

Inspired by Bruce Lee to start training at 8 years old, Maeda had been a personal trainer for decades, even landed a few movie roles with his muscular physique. But in 2012, he was diagnosed with stage 3 colon cancer in his early 40s, requiring major emergency surgery and half a year of chemotherapy.

Recovering from cancer made him realize that focusing on his physique over his health was like building a nice car without proper brakes or steering.

“I wanted a strong frame. I wanted a powerful engine, but I spent so much time building this car, I forgot how to drive it. That’s what I’m doing now,” he said.

Maeda slowly rebuilt his fitness, one rep at a time, and said shorter and simpler can be better for long-term gains.

Build a foundation on the basics: deadlifts, squats, push-ups

Maeda’s current workouts on social media often feature unusual exercises, but he said most people shouldn’t do complicated workouts unless they’ve mastered the basics. You don’t need elaborate movement to build muscle, and the risk of injury can increase as an exercise become more intricate.

“Well into my forties, I didn’t do anything fancy. It was deadlifts, squats, kettlebell swings, just a lot of very fundamental movements,” Maeda said. “Those are what built my physical base, what people see now, the muscle I carry.”

To gain muscle and strength, focus on progressive overload, performing the same exercises over time with gradually increasing weight.

From there, you can explore variations of exercise to keep workouts fun and challenging while improving mobility, agility, and balance.

“I do less of that heavy basic lifting because of the time I have now, I’d rather put it towards movements that spread the stress of what I’m doing more evenly throughout my body,” Maeda said.

Work out in less time by rucking

One regular part of Maeda’s fitness routine is rucking, or walking with weight. He typically carries a 45-pound backpack for 30 minutes a day, at least five days a week, while walking his dogs.

Working out too hard can backfire. A personal trainer shares 4 red flags and 4 green flags to optimize your routine.

He first starting rucking as he was slowly rebuilding his endurance after colon cancer. He began with short walks wearing a backpack full of bricks and added weight (and better gear through his partnership with fitness brand GORUCK) over time.

Building muscle and endurance comes from challenging your body over time. Rucking provides a convenient way to work the muscles during activities that are already a part of a routine, like walking dogs or taking a hike.

For Maeda, it added an extra challenge without taking more time out of his day.

“It got me to a point where just walking seemed like a total waste of time,” he said. “If I’m doing something that often and I can just put a 45-pound backpack on, that’s a lot of minutes under load.”

Ending a workout early can pay off

In his younger years, Maeda embraced the “no pain, no gain” mindset of tough exercise, but now warns against it

“I don’t personally recommend programs that are aggressive and based on sucking it up and willpower. Life is hard enough,” Maeda said.

He said it’s better not to be completely exhausted after exercise, so you’re energized and excited for the next workout, even if that means cutting your workout short.

“Consistency over days is way more important than a hard weekend warrior workout that means you’re sore for the rest of the week,” he said.

Try this no-equipment workout for beginners

Maeda recommends starting with a workout you can do at home.

To complete his “exercise ladder,” do:

- one squat, one push-up;

- two squats, two push-ups;

- three squats, three push-ups;

- continue up to five reps, or until the next set starts to feel daunting.

Over time, you can repeat the workout, aiming to reach a higher number of reps as you progress, or change up the exercises (doing lunges and pull-ups, or single-leg deadlifts and burpees).

10. 11 Personal Finance Goals for Your 40s

Via Art of Manliness: Years ago, we published articles on personal finance goals to strive for in your 20s and in your 30s.

Now that I’m in my 40s, I decided to revisit this series to see if I needed to update my financial goals in my first decade of midlife.

Your 40s are an interesting time, money-wise. Many men enter their peak earning years during this decade. Yet their expenses often increase significantly at the same time. High-school-aged kids may need cars, and those same teenagers may subsequently need help paying for college. Your parents are retiring and aging into their 70s, and you’re starting to think about what financial support they may require in the last decades of their lives. Meanwhile, your own retirement shifts from a distant abstraction into an approaching reality.

During this decade where you’re both starting to enjoy the fruits of your labors, but feeling the pressure of additional demands, you want to make moves to ensure you’re on stable ground now and in the future.

Below are 10 goals, backed by research and the advice of personal finance experts, that will help you not just survive your 40s, but thrive in that decade and in the decades to come:

1. Consider Consulting a Financial Advisor

With higher income and more responsibilities, your financial life is more complex in your 40s.

So consider hiring a fee-only financial advisor to help you navigate these complexities. Fee-only financial advisors don’t make money from selling financial products like insurance or mutual funds, reducing conflicts of interest.

You can pay a fee-only financial advisor by the hour to get advice on planning for retirement, paying for college and potential weddings, updating your estate plan, and reviewing insurance.

If you’re looking for more comprehensive guidance, you can set up an arrangement where the financial advisor gets a percentage of the assets they manage for you.

2. Maintain a Robust Emergency Fund (6–12 Months of Expenses)

By now, you should have a solid emergency fund. In your 40s, the goal is to increase its balance to match the expenses you likely have as a middle-aged man.

Aim for at least six months of essential expenses, or up to a year if you’re in a volatile industry or single-income household. Job hunts for people in their 40s often take longer than for those who are younger. If you were to lose your income, a six-month cash reserve ensures you can keep paying the mortgage and feeding the family while you find your next role. It also prevents you from raiding retirement accounts or going into debt.

Keep this fund in a liquid, low-risk account. Don’t touch it unless it’s a true emergency; replenish it as soon as possible if used.

3. Maximize Your Income

For many men, their 40s are the highest-earning decade of life. The median annual salary for men usually peaks between 45 and 54. Make it a goal to leverage these years as much as possible to set yourself up for true financial security.

To make the most of this decade, you’ll want to maximize your income.

Raises won’t usually fall into your lap. You’ll need to ask for them proactively.

If your boss won’t budge on giving you a raise, consider switching roles or even companies. Changing jobs mid-career can often substantially increase your salary, but so can moving up the ranks at your current job; be sure to check out our podcast on getting a promotion for some solid advice on how to continue to work your way toward the literal or metaphorical corner office.

Additionally, look into creating extra income streams through side businesses or freelancing. At this stage in your career, you probably have valuable expertise others will pay for. Consider moonlighting as a consultant. The extra income you earn now could even evolve into part-time work after you retire.

It’s worth noting that your 40s are not only peak earning years, but may be the last years you have your kids at home. You don’t want to be so focused on maximizing your income that you miss out on maximizing the time you spend with them before becoming an empty nester. It’s a tough line to walk, but strive to strike a balance between filling up your financial treasury, and your memory bank.

4. Avoid Lifestyle Creep

It’s natural to want to reward yourself as your income rises — to finally get that dream car, upgrade to a bigger house, or take more vacations. And you should allow yourself to start splurging a little more in your 40s; you’ve earned it by grinding through your 30s.

But don’t go overboard; every dollar spent on upgrading your lifestyle is one less dollar available for debt reduction or savings. Remember, too, that the cost of another car or a bigger house isn’t just the initial purchase price, but what it will cost you in maintenance, insurance, etc.

Start enjoying yourself more in your 40s, while saving enough to ensure that the next four to five decades are enjoyable as well.

5. Double-Down on Retirement Savings (Aim for 3X Your Salary)

In your 40s, retirement is no longer the abstract-seeming thing it was in your 20s. It will potentially be a concrete reality for you in twenty or so years.

Experts suggest having about three times your annual salary saved by age 40. Don’t worry if you’re not there yet — many aren’t — but use that benchmark to motivate you.

In your 40s, strive to save at least 15% of your income (ideally 20% or more) for retirement. As you save for retirement, take full advantage of tax-advantaged accounts like 401(k)s and IRAs.

How should you allocate your retirement savings in your 40s? When I put this question to personal finance expert Nick Maggiulli, he suggested that for many, it might mean reducing risk due to the increased liabilities they likely have in midlife: “In your 40s and 50s, you should consider reducing this risk to fit your liability profile better. For example, you could consider going from an 80/20 stock/bond portfolio to a 70/30 (or something similar). The key here is not maximizing your net worth, but maximizing your chance of long-term survival.”

6. Eliminate Non-Mortgage Debt and Work Toward Being Mortgage-Free

Ideally, you’ll have paid off all non-mortgage debt in your 30s. If you haven’t, make that a priority in your 40s. Aggressively tackle any lingering debts, like car loans and student loans.

Once you’ve eliminated all non-mortgage debt, start focusing on your mortgage. While you don’t necessarily need to pay it off during your 40s, you should have a clear plan for eliminating it as soon as financially feasible.

If you can swing it, start making extra principal payments. Even one extra payment a year (or adding, say, $200 extra each month) can knock years off a 30-year loan. Check with your lender that extra payments go toward the principal.

7. Bolster Kids’ College Funds (But Not at the Expense of Retirement)

In your 40s, your children may be in high school, and college costs are looming. Ideally, you started a 529 account for your kids in your 30s; if not, start one now. With 529 accounts, gains and distributions/withdrawals for education aren’t taxed.

As you save for your kids’ education, don’t do so at the expense of your retirement. Your retirement should always be the priority when saving. Your kids have options for education financing, but you don’t have one for retirement.

8. Plan for Aging Parents and Family Care Responsibilities

More than half of 40-somethings are either raising children under 18 or financially supporting adult children, and have at least one parent aged 65 or older. About a quarter of adults in their 40s and 50s actively provide financial assistance or regular care to their aging parents — a percentage that only increases as members of this “sandwich generation” and their parents grow older.

Prepare for a future with aging parents by talking to Mom and Dad about their financial health. Do they have sufficient retirement savings, a will, power of attorney, or healthcare directives? Knowing this upfront can prevent surprises during a crisis.

Second, discuss future care preferences. When their health declines, would your parents prefer living with family or moving into an assisted living facility? Clarifying this sets expectations and shapes future plans. If you have siblings, hold a meeting to define roles and discuss shared costs.

Finally, consider preparing financially by creating a “parent fund” for predictable expenses like medical bills or housing.

Check out the book Mom and Dad, We Need to Talk: How to Have Essential Conversations With Your Parents About Their Finances. I thought it had a lot of good advice.

9. Do an Insurance Check-up

If you bought term life insurance in your 30s (as we recommended), revisit your coverage. Major changes — like more kids, a bigger mortgage, or a higher income — might require additional coverage. A common guideline is 10–15X your annual salary, ensuring your family could replace your income if needed. Term policies are still affordable in your 40s (though premiums rise), so lock in coverage until kids graduate college and your mortgage is paid off.

Also consider umbrella insurance to protect accumulated wealth from liability lawsuits, and disability insurance to replace your income if you can’t work.

10. Do an Estate Plan Check-Up

You should have started your estate planning in your 30s; in your 40s, it’s time to do a check-up.

- Revisit and update your will to reflect current realities, like new assets or guardians for your kids.

- Double-check beneficiary designations on retirement accounts, insurance, and investments; these override your will, so accuracy is crucial.

- Ensure you have durable powers of attorney (for financial decisions) and healthcare proxies, naming people you trust.

- Explore advanced strategies like trusts or charitable giving if your estate is sizable.

- Communicate with your spouse and estate executor about your plans and where key documents are stored.

11. Plan Your Next Chapter of Life

Having a clear retirement vision guides your financial choices today. Outline your ideal retirement. When will you retire? Where will you live? How will you spend your time? Cruising? Volunteering? Working part-time? Answers to these big-picture questions will shape how you save in your 40s.

Next, calculate your retirement “number.” Most aim for savings that generate 70–80% of pre-retirement income annually. Use retirement calculators or a financial planner to check your progress, adjusting your savings or expectations if needed.

Finally, prepare for potential healthcare costs. You might live into your 90s, so your savings could need to last over 30 years after you retire.

Your 40s are a busy and sometimes stressful decade, but with thoughtful planning and strategic actions, you can balance today’s demands with tomorrow’s dreams. Use these goals as your financial roadmap, and you’ll enter your 50s with confidence and clarity, knowing you’ve laid a strong foundation for the years ahead. I’ll see you in 10 years with an article on financial goals for that decade of life!