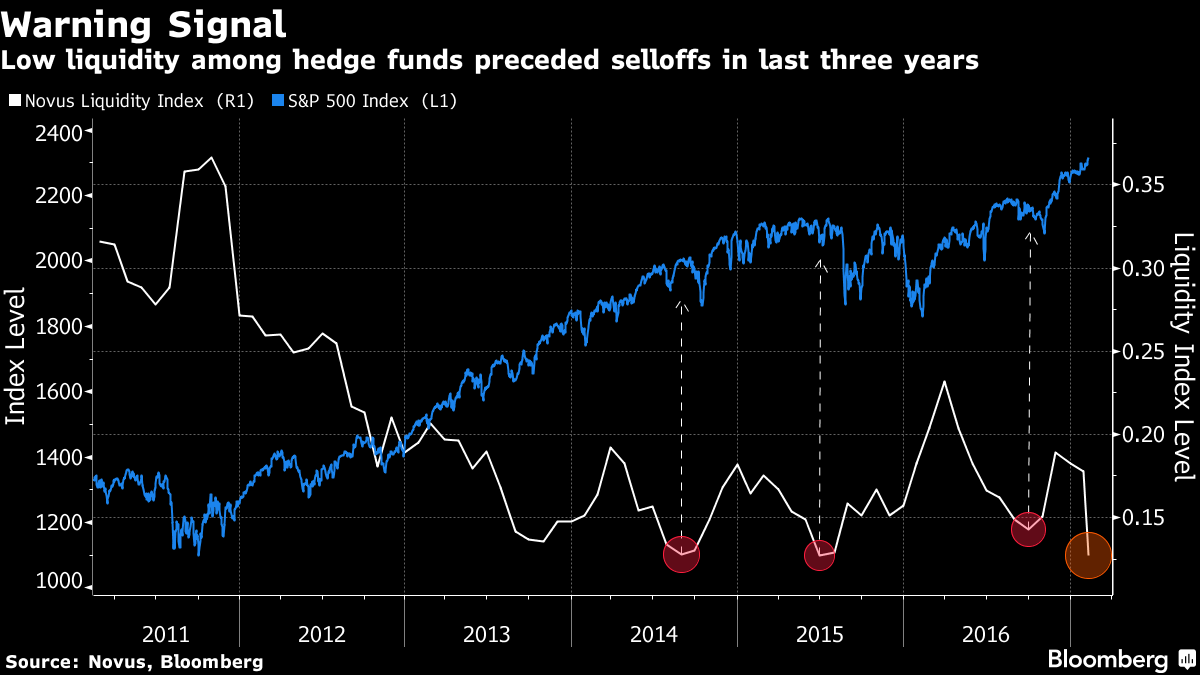

1.Low Liquidity Among Hedge Funds and Holding the Same Names Like Never Before

(Bloomberg) — There’s safety in numbers. Until a stampede starts.

That’s the theory underlying a study of hedge fund holdings by Novus Partners Inc., which sought to calculate how easily the market could absorb concerted selling by large money managers. Using an analysis that turns mainly on how much volume is occurring in stocks favored by professional speculators, Novus says liquidity is at an all-time low.

Read Full Article

Hedge Funds in Crowded Trades.

Found at Abnormal Returns Blog

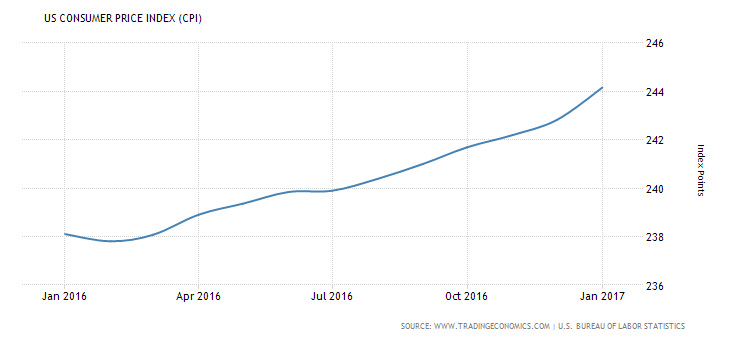

2.U.S. Consumer Prices Recorded Biggest Increase in 4 Years.

U.S. consumer prices recorded their biggest increase in nearly four years in January as

households paid more for gasoline and other goods, suggesting inflation pressures could be picking up.

The Labor Department said on Wednesday its Consumer Price Index jumped 0.6 percent last month after gaining 0.3 percent in December. January’s increase in the CPI was the largest since February 2013.

In the 12 months through January, the CPI increased 2.5 percent, the biggest year-on-year gain since March 2012.

The CPI rose 2.1 percent in the year to December.

Economists polled by Reuters had forecast the CPI rising 0.3 percent last month and advancing 2.4 percent from a year ago.

Inflation is trending higher as prices for energy goods and other commodities rebound as global demand picks up.

Found on Josh Brown Blog

http://thereformedbroker.com/2017/02/15/cpi-busts-out/

http://www.tradingeconomics.com/united-states/consumer-price-index-cpi

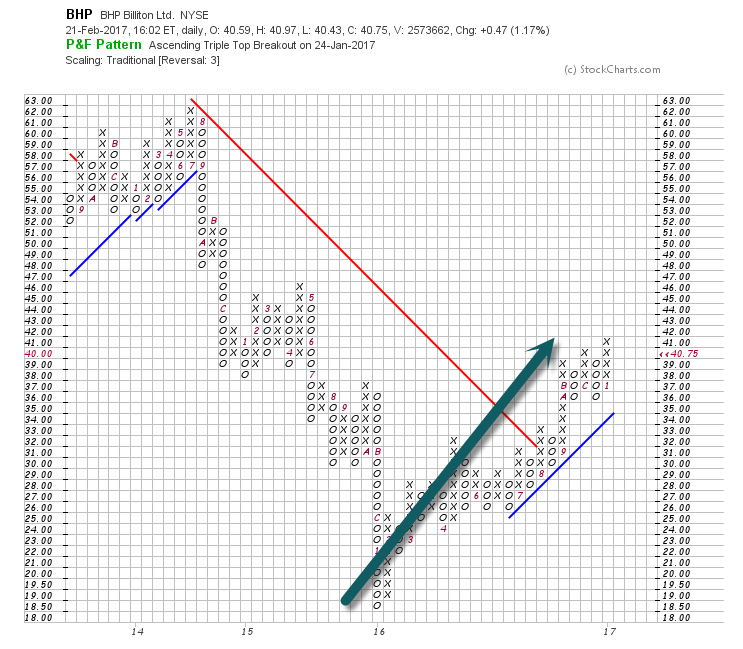

3.BHP +121% Off 2016 Lows…Commodities Tell? Global Growth Tell?

Buoyed by a resurgence in commodity prices, BHP Billiton (NYSE:BHP) swung back into the black during the fiscal first half of 2017, posting a net profit of $3.2B, compared with a loss of $5.7B in the same period a year earlier. The company said it would also raise its interim dividend to $0.40, up from $0.16, on the back of the uptick in earnings. BHP +1% premarket. www.seekingalpha.com

BHP breaks above red downtrend line from 2014

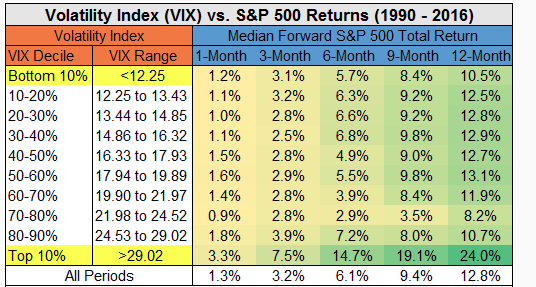

4.VIX in Bottom Decile is not that Dangerous…When VIX gets in Top Decile “Buy”

They say you should never short a dull market –>”when the VIX is in the bottom decile of historical readings, as it is now, the S&P 500’s forward returns are a hair below average but still solidly positive (1.2% in one month, 5.7% in six months and 10.5% in 12 months.) He also concludes it’s even more foolish to short a wild market: when the VIX is in its top decile, returns over the next year are a whopping 24% “

From Dave Lutz at Jones.

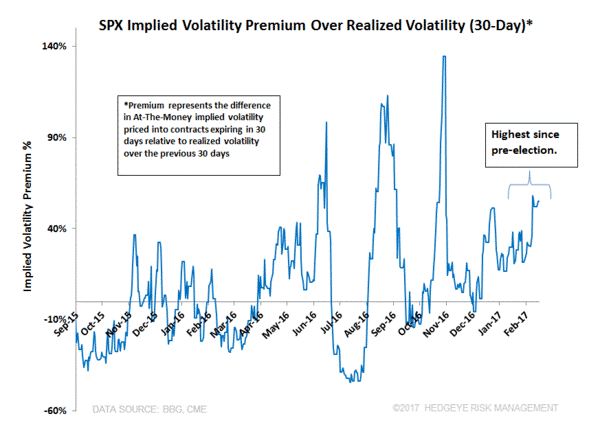

5.More Volatility Comments…Here’s What Volatility Reveals About This ‘Expensive’ U.S. Stock Market

Source: RoadTrafficSigns.com

The big money in markets is often made by seeing what others don’t. It’s about resisting the gravitational pull of consensus, treading lightly where consensus is right, while spotting subtleties where the herd might be wrong.

Where Consensus Could Be Wrong: Volatility

#Volatility #ElectionDay

One subtlety we’ve been watching recently is volatility. Volatility, of course, is the measurement of the daily market fluctuations. In times of fear, the volatility of an asset rises. In times of buoyancy, all is well. The market simply floats higher and volatility falls.

We have a nuanced view of volatility here at Hedgeye. Conceptually, there are two types of volatility we’re looking at, realized volatility (i.e. the volatility of an asset historically) and implied volatility (i.e. investors’ expectations of future volatility that’s embedded in options markets).

These volatility readings are painting a clear picture for investors today. As the stock market continues to make all-time highs, historical or realized volatility is falling to cycle lows. Meanwhile, fearful traders expect rising future volatility in the stock market and are buying downside protection in options markets to stave off the pain of an impending correction.

The Chart of the Day below from today’s Early Look is a visual representation of precisely that. The S&P 500 implied volatility premium on a 30-day basis is 52.2%. That’s a fancy way of saying investors are fearful of downside risks as historical volatility continues to fall. Note: A premium this high in the stratosphere hasn’t been hit since before Election Day.

Where Do We Go From Here?

#Economy #RetailSales #Inflation

Investors must put this volatility measure in the context of where we’re at in the economic cycle. Unsurprisingly, U.S. economic growth and inflation drive financial market returns. We believe both growth and inflation are accelerating.

Retail sales and inflation reports last week were near or above 5-year highs.

With this positive backdrop, we think equity markets can head higher from here. In other words, investors betting on significant future downside will get squeezed out of those positions.

It might actually be more risky piling into sectors like Consumer Staples (XLP) and Utilities (XLU), which are typically equity exposures investors buy when future downside is expected. In these sectors, implied volatility premiums are infinitesimal, 0.3% for Consumer Staples and 4.8% for Utilities. Implied volatility premiums this low suggest investor complacency.

Bottom Line

The prevailing market trends say stick with U.S. equities here.

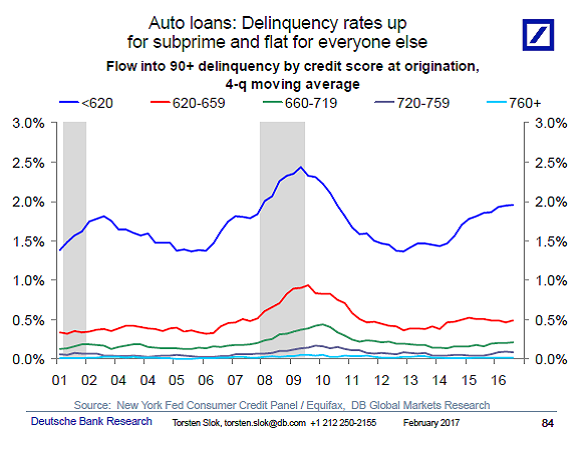

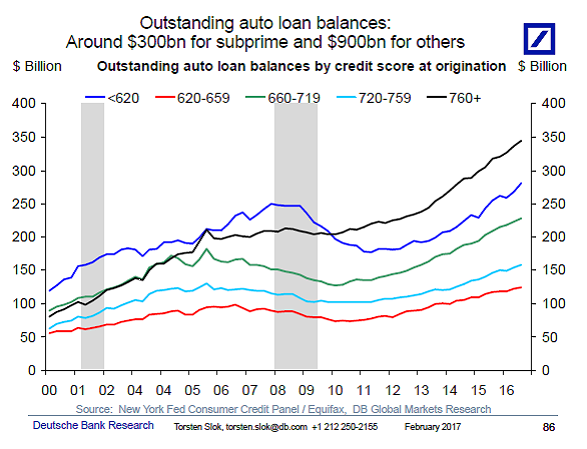

6.Auto Loan Delinquency Up But Not Big Enough to Move Macro Needle.

I’m getting questions from clients asking if the recent increase in subprime auto loan delinquency rates is a problem. Delinquency rates for people with credit scores lower than 620 have moved higher but for households with credit scores above 620 delinquency rates are moving sideways, see the first chart below. Also, while subprime auto loan origination has increased to 2006 levels we have seen an even bigger increase in origination and amount outstanding for prime borrowers, see the second and third chart. Finally, it is important to remember that total household net worth currently stands at $90 trillion, and in that perspective, total outstanding subprime auto loans at less than $300bn seems very small. The 2006 subprime mortgage market was much bigger than today’s subprime auto loan market, and there was much more leverage in the financial system in 2006 compared with today. The bottom line is that the increase in delinquency rates for subprime auto loans may be a worry for those holding the debt, but it is not a problem for the macro economy.

Let us know if you would like to add a colleague to this distribution list.

Torsten Sløk, Ph.D.

Chief International Economist

Managing Director

Deutsche Bank Securities

60 Wall Street

New York, New York 10005

Tel: 212 250 2155

7.Rents Slowing Down…Banks Pulling Back on Apartment Lending.

Banks Retreat From Apartment Market

A pullback in lending is forcing builders to scramble for financing to finish projects; ‘I haven’t seen anything this seismically different since 2008’

New apartment construction is seen underway in St. Petersburg, Fla. Photo: Scott Keeler/Tampa Bay Times/Zuma Press

By

Laura Kusisto

The Wall Street JournalThe apartment sector, which contributes some $284 billion to the economy annually, has been a winning bet for investors since the housing crash, as the economy recovered and more renters sought out units. Since 2010, average U.S. apartment rents have increased by 26%, according to data tracker MPF Research, a division of RealPage.“Our business has radically changed,” said Toby Bozzuto, president and chief executive of the Bozzuto Group, which owns or manages 59,000 apartments in cities across the U.S. “I haven’t seen anything this seismically different since 2008, when credit dried up.”

Now banks are in retreat, forcing developers to look to nontraditional lenders and seek more expensive types of financing to complete projects, said apartment executives, industry analysts, mortgage brokers and bankers.

“We had fairly robust growth in our construction, real estate construction book, and that’s slowing now,” said P.W. Parker, chief risk officer of Minneapolis-based U.S. Bancorp, during an earnings call last month. “Multifamily is an area that, if you look at the forecasts, there are forecasts pretty broad-based of potential rent declines in a lot of the major cities. So we’re being more cautious there.

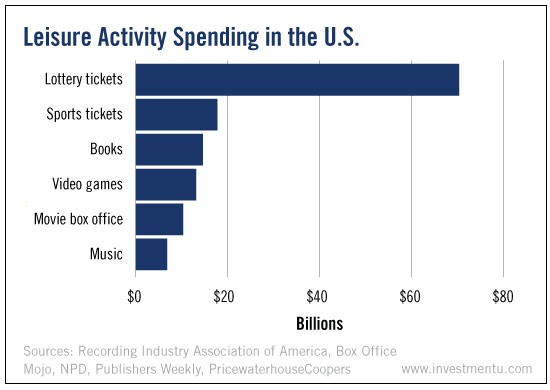

8.The amount Americans threw away on lottery tickets was $7.4 billion more than what was spent on all other forms of entertainment combined.

https://www.wsj.com/articles/banks-retreat-from-apartment-market-1487678401

9. Read of Day…How Higher Education Fueled Working-Class Anger

”Read Full Story http://www.investmentu.com/article/detail/53531/lottery-tickets-70-billion-tax-killing-retirement#.WK3pmG8rJhE

Published on February 21, 2017

Jeff Selingo

New York Times bestselling author, Washington Post columnist, higher education strategist, LinkedIn Top 10 Influencer

In the last few weeks I attended several higher education conferences where the talk among campus officials in the hallways and in sessions was usually centered around the same topic: President Trump. What’s clear in these conversations is that the much-discussed education divide that separated the electorate last fall between those with a college degree and those without has not dissipated since the election.

But the disdain academics exhibit for Trump these days ignores the role that their own colleges and universities played over the past two decades in fueling the working-class anger that led to his 2016 victory.

The story begins in the 1990s, when a college degree became increasingly necessary for economic success. The manufacturing sector, with its middle-class jobs requiring only a high-school diploma, had mostly collapsed the previous decade.

This shift in the economy coincided with a sea change in college admissions. The ease of travel and declining cost of communications meant that admissions was no longer a local game where even selective colleges with large endowments and strong brand names recruited mostly in surrounding states. When the U.S. News & World Report rankings became an annual publication in the late 1980s, colleges jockeyed to move up the rankings in order to gain prestige. To do that, they had to find better students outside their usual recruitment zone. And for schools a few rungs down the rankings ladder, it required luring top-notch students with boatloads of financial aid—even if their families didn’t need the money to send their kids to college.

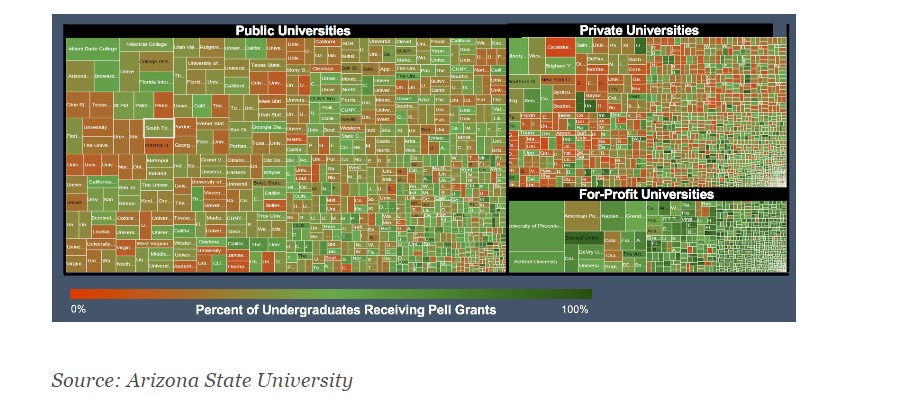

Access to higher education for students at all income levels, which had been prevailing policy since the signing of the Higher Education Act in 1965, was shoved aside. In the drive for prestige, selective colleges in particular became less economically diverse, full of wealthy students and a few smart kids lucky to get a Pell grant (which mostly go to students from families making less than $50,000 annually). In 2013-14, only 22 percent of students received Pell grants at top universities, compared to around 38 percent everywhere else. Students on Pell grants tend to be clustered at less-selective public and private colleges, and poor-performing for-profit colleges.

Pell Grants by undergraduate enrollment, 2014

Source: Arizona State University

This economic disparity is well known in higher education, but the extent of it became clear last month when researchers released the most comprehensive look to date at the financial background of students on college campuses. The results of the study—gleaned from analyzing the tax records of some 30 million students born between 1980 and 1991 and linked to nearly every college in the country—were startling.

At 38 colleges, including five in the Ivy League, there are more students from families in the top 1 percent in income than the bottom 60 percent. What’s more, about 25 percent of the richest students attend a selective, elite college. By comparison, less than one-half of 1 percent of children from the bottom fifth of U.S. families by income attend an elite college.

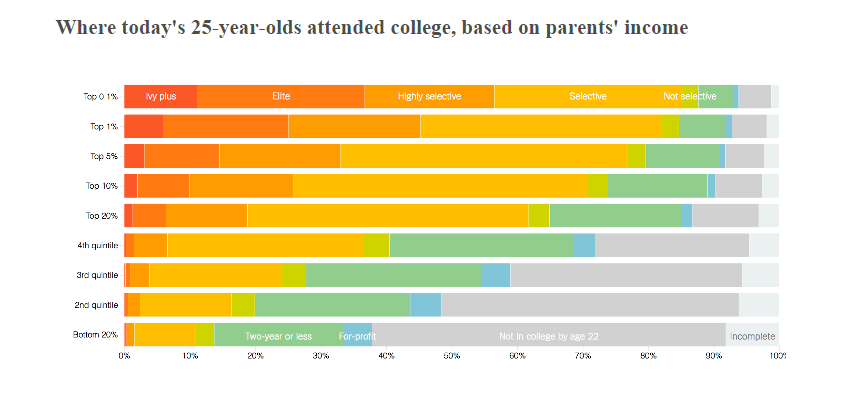

Where today’s 25-year-olds attended college, based on parents’ income

Source: New York Times

As the economic divide grew ever wider among students on campuses over the last two decades, countless students graduated from college without the benefit of ever really knowing classmates from working-class families. Some of them then came to Washington to work on Capitol Hill, in the White House and in federal agencies to develop policies that would impact people without a college degree. They had little idea what it was like to lack a credential that carried so much weight in the job market.

Instead of being shocked by Trump’s win, higher education leaders should look internally at their own strategies that focused on gaining prestige and often exacerbated the growing economic divide by favoring students from wealthy and middle-class families.

College leaders are beginning to take notice. In December, a handful of selective colleges and universities announced an effort to identify, recruit, and support highly qualified low-income students. The American Talent Initiative aims to boost the number of Pell grant recipients at the 270 colleges with the highest graduation rates by 50,000 within 10 years (an increase of more than 10 percent).

This effort is a good start to reverse the trends of the last two decades, but it might be too little, too late. Higher education lost an entire generation of students who will become leaders in the future and missed out on an opportunity to have an undergraduate experience full of students from different economic backgrounds.

Jeffrey Selingo is author of There Is Life After College: What Parents and Students Should Know About Navigating School to Prepare for the Jobs of Tomorrow. You can follow his writing here, on Twitter @jselingo, on Facebook, and sign up for free newsletters about the future of higher education at jeffselingo.com.

He is a regular contributor to the Washington Post’s Grade Point blog, a professor of practice at Arizona State University, and a visiting scholar at Georgia Tech’s Center for 21st Century Universities.

Cross-posted from The Washington Post

10.Self-Leadership Secrets of an Extreme Athlete

What could the sport of running teach us about the secrets of self-leadership and reaching our business finish lines?

I’ve been a fan of Dean Karnazes ever since I read his book Ultramarathon Man several years ago, so I eagerly devoured his newest, The Road to Sparta, which tells the story of history’s first-ever marathon.

Some of us know the popular version of the story, where after the Athenians defeated Persian invaders at the battle of Marathon 490 B.C., a messenger ran 26 miles to share the exciting news.

But Karnazes shares the real story, where the runner, whose name was Pheidippides, actually ran more than 150 miles all the way from Athens to Sparta, then back again, before the battle.

That’s 300 miles.

Why would a person willingly go through something like that?

“Western culture has things a little backwards right now,” Karnazes said. “We equate comfort with happiness. And now we’re so comfortable we’re miserable. There’s no struggle in our lives.”

That observation doesn’t just apply to running. That applies to all of life, including leading our organizations. When it comes to work, comfort equals boredom.

Engagement and even happiness come when we’re gunning toward major goals. I’m talking about the kind of achievements that push us outside our comfort zone.

Maybe it’s launching a new product line, starting a new career, or growing a sales channel by double digits. If staring down the goal makes you feel uneasy, you’re on the right track.

This ‘Discomfort Advantage’ is only one of the lessons running can teach us. Here are three leadership takeaways I discovered when I read The Road to Sparta:

- Leverage your unique abilities.

When Karnazes was a child, he went to a basketball camp coached by the legendary John Wooden. A small kid, Karnazes struggled to get rebounds like the bigger children. But Wooden could see his spirit and gave him some advice: “Do what you can.” Instead of going for rebounds, he started playing the backcourt. And he dominated.

When we compete head-to-head as if our abilities are the same as others, we sometimes miss playing to our strengths. It’s like we tilt the playing field against ourselves. Instead, we need to focus on what makes us unique. Steve Jobs is one of the best examples of this in recent years. Apple played its own game and rose to dominance.

- Let passion outrun balance.

We have to be careful that our jobs don’t dominate our lives, but there’s a natural tension in play if we really love what we do. “People speak of finding balance,” says Karnazes. “To me, that’s a misplaced ambition. If you have balance, you do everything okay. … Balance doesn’t lead to happiness—impassioned dedication to one’s life purpose does.”

What else could lead a person to run 153 miles through Greece? What else could lead an entrepreneur to do what the market believes is impossible? Balance is desirable, but it’s not the endgame. Finding and achieving your life’s purpose is.

- Celebrate your wins.

When we reach our goals, we need to take the appropriate time to celebrate. That’s a critical way to honor our work. But it’s also a key component of living a full life.

Hosting another run in Greece called the Navarino Challenge, Karnazes was surprised at how the townspeople came out to celebrate the winners. “These people were all willing to put aside what they were doing and join together,” he remembered, “rejoicing in the moment.”

“If we always made decisions with our heads instead of our hearts, we’d probably live much more orderly lives,” he says, “but they would much less joyous. … How many people spend their entire lives striving for something with their nose to the grindstone, only to wake up one day and realize they haven’t really lived at all?”

Trade on your unique abilities, stay fueled by passion for your work, and take time to celebrate your accomplishments.

Those three takeaways might serve an athlete. But I’m confident they’ll serve leaders even more.

Originally published by Michael Hyatt on December 16, 2016

http://www.earlytorise.com/self-leadership-secrets-extreme-athlete/