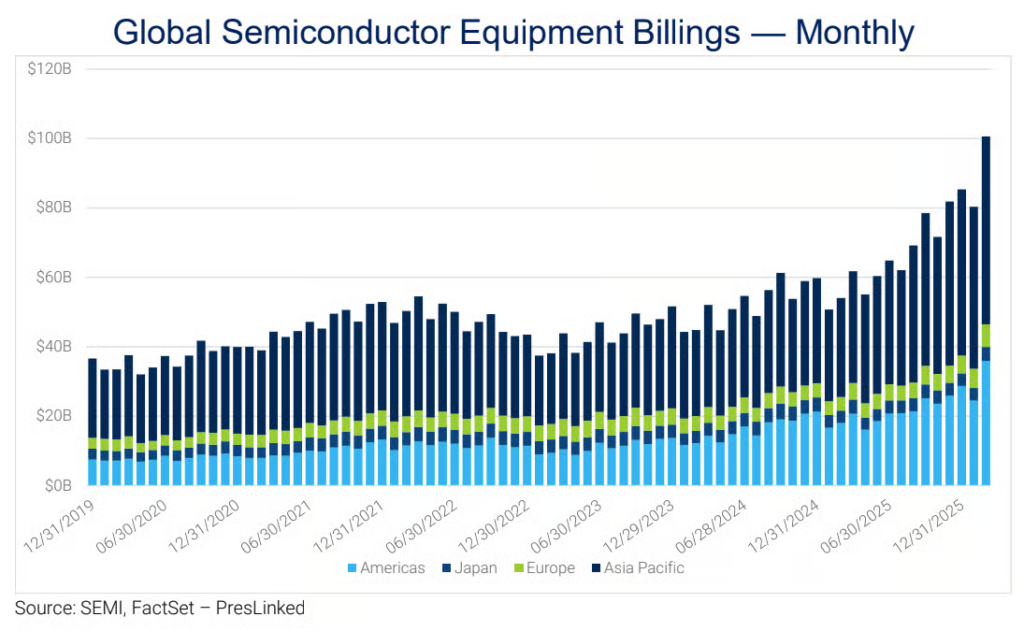

2. Global Semiconductor Billing Projected to Hit $1T

Global semis billings. “The [Semiconductor Industry Association] projects that the industry is on track to exceed $1 trillion in billings for the first time in 2026.”

Sean Ryan – FactSet

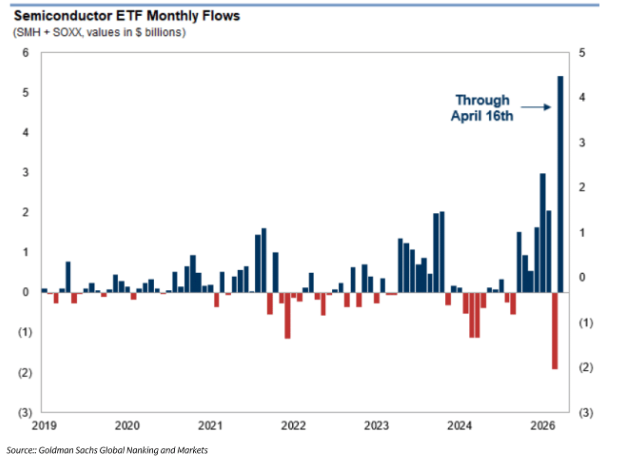

3. Semiconductor Monthly Flows

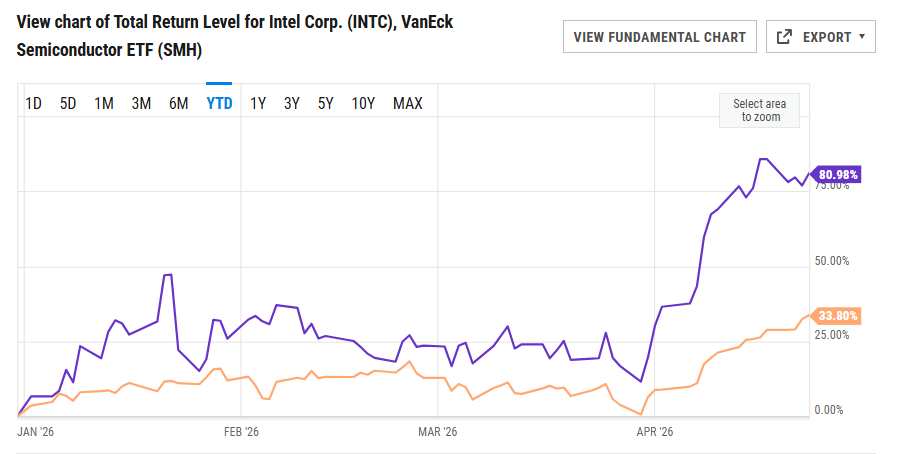

4. INTC vs. Semiconductor ETF SMH Before Last Nights Earnings …2026 INTC +81% vs. SMH +33%

YCharts

5. Intel Just Breaking Above 1999 Internet Bubble Highs

Google Finance

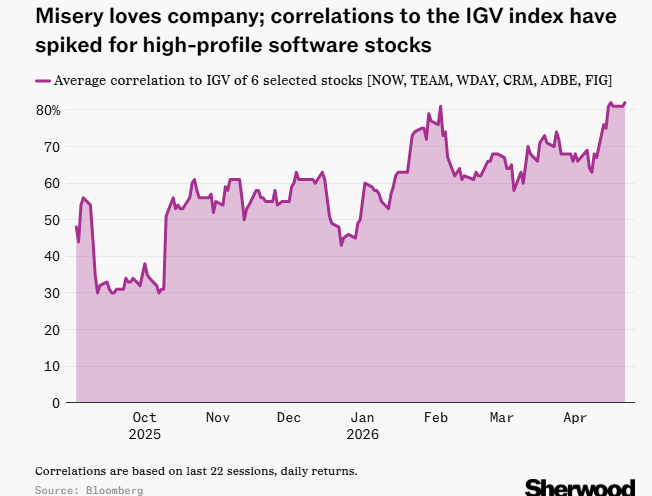

6. Software Stocks All Trading Together …80% Correlation…One Bad News=All Bad News

Sherwood Media, LLC

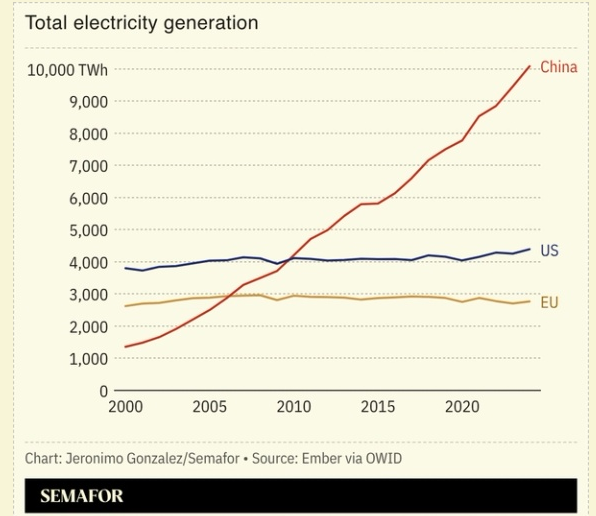

7. Total Electricity Generation

Semafor

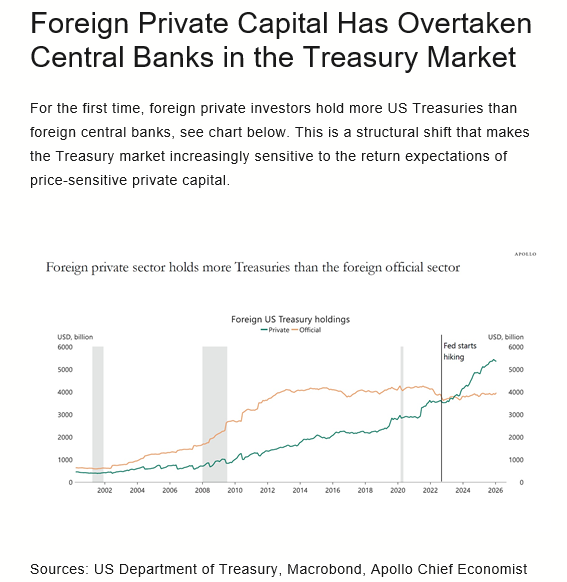

8. Foreign Private Capital More in Treasuries than Central Banks…Sell America Total BS

Apollo

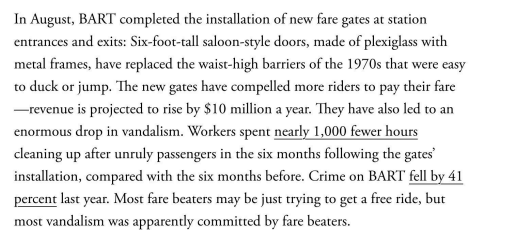

9. San Fran Rail System Crime Drops 41% and Workers Spent 1000 Less Hours Cleaning Up After Reducing Fair Jumping

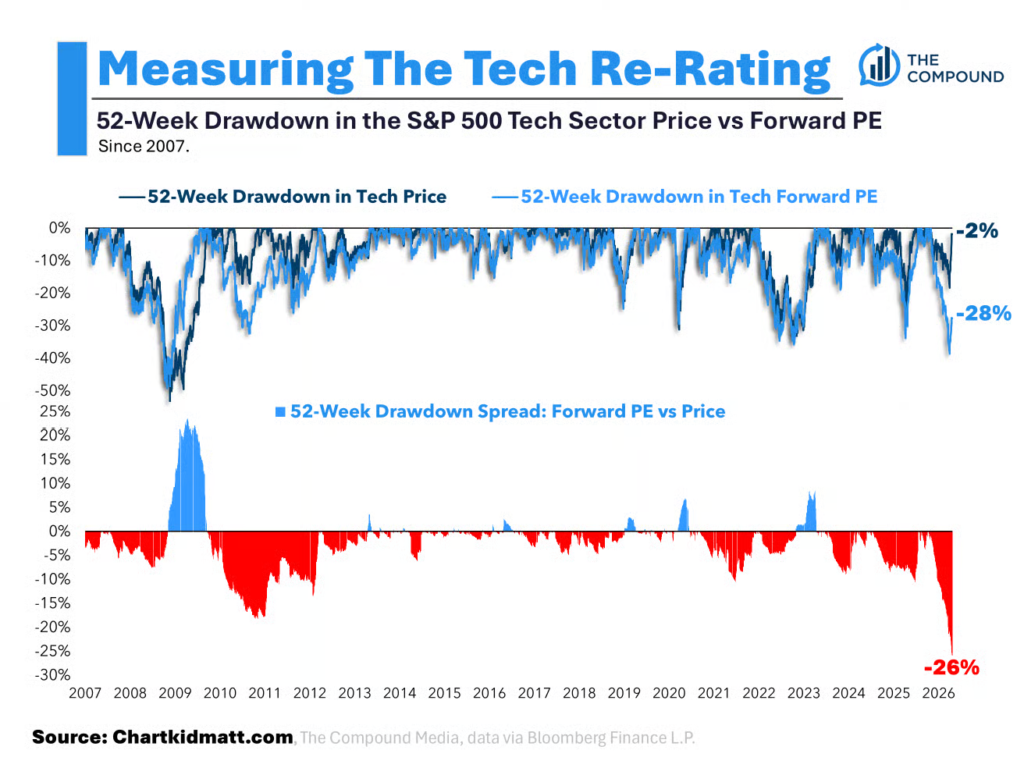

The gap between tech’s price and forward PE drawdown is the widest its been in nearly 20 years of data.

This one shocked me.

Below you’re looking at the 52-week drawdown in the S&P 500 technology sector price (dark blue line) vs the 52-week drawdown in the forward PE (light blue line).

Chart Kid Matt

The lines typically move together. Makes sense, right? But look at the recent divergence.

The tech sector is currently in a 2% drawdown from 52-week highs, but the multiple is off a whopping 28%.

See the 26% spread in the bottom pane? That’s the largest spread I can find going back to 2007.

The only way tech is nearing an all time high with the forward multiple in a 28% drawdown is because the forward earnings are ripping higher.

That feels healthy to me.

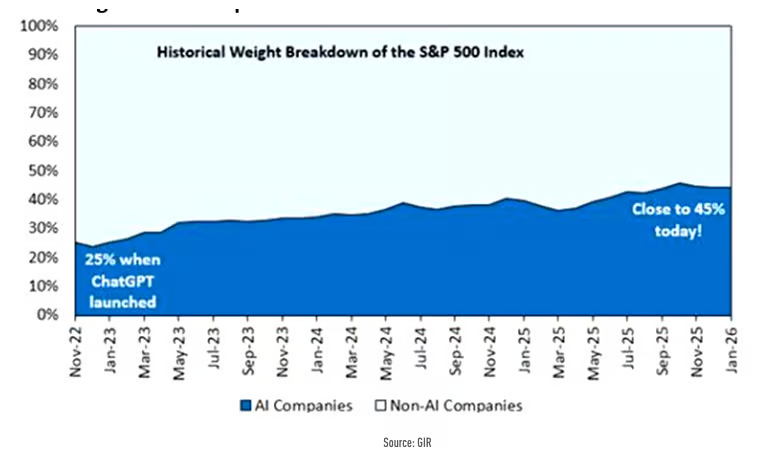

3. AI Companies Weight in S&P 45%

AI vs. SPX. “The weight of AI companies in S&P 500 is close to 45%”.

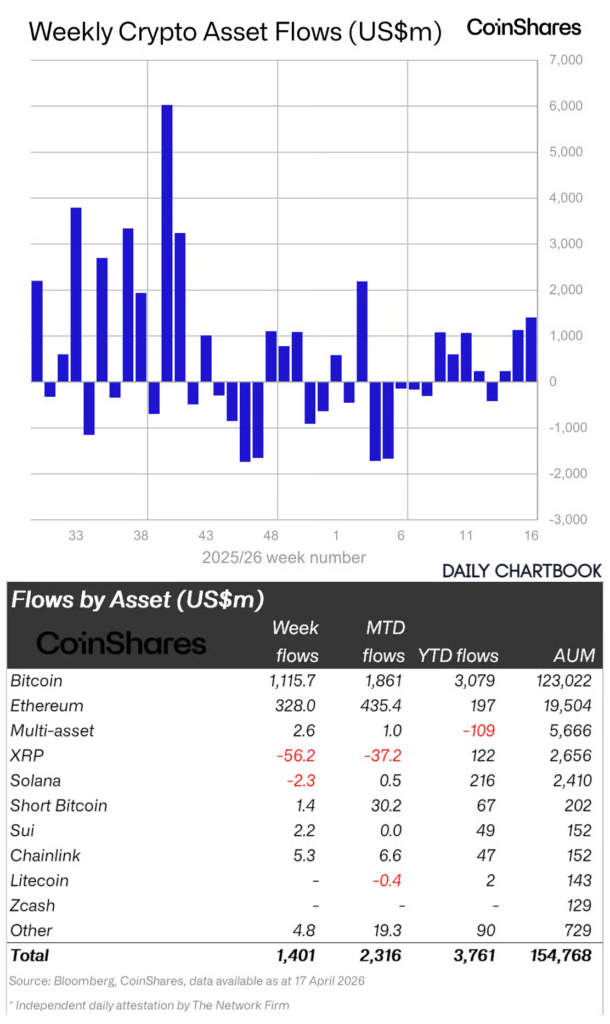

Crypto asset flows. “Digital asset investment products saw US$1.4bn of inflows, the third consecutive positive week and the strongest since January … Total AuM reached US$155bn, with flows representing 0.91% of AuM, the highest weekly intensity YTD.”

James Butterfill – CoinShares

5. Apple Gained $3.66 Trillion in Market Cap Under Cook

Bloomberg

6. Increase in Private Security for Execs-Ed Elson

Prof G Media

7. More Private Security in U.S. than Police

Perplexity

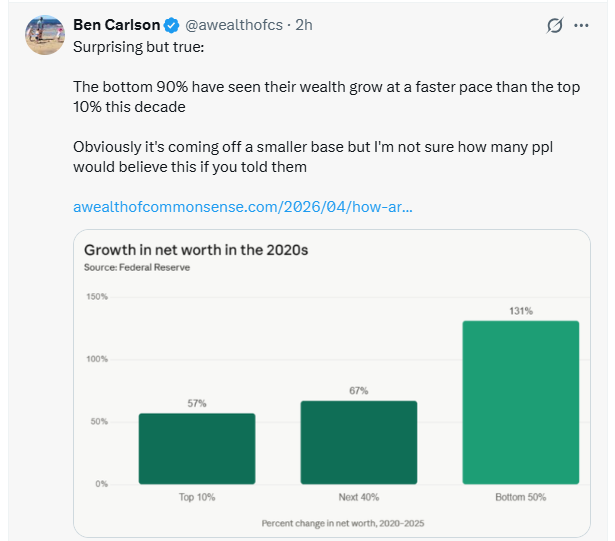

8. Growth in Net Worth 2020s

A Wealth of Common Sense

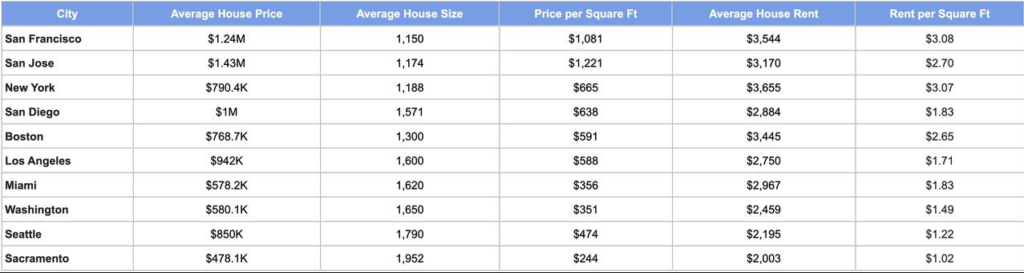

9. These Are The US Cities Where No One Can Afford A Large Home

by Tyler Durden An April 2026 housing report by Highland Cabinetry highlights a growing affordability crisis across major American cities, revealing that the true cost of housing goes beyond total price and is better understood through the lens of cost per square foot. By analyzing home prices, rental costs, and average property sizes across 40 large cities, the study shows where Americans are paying the most for the least amount of living space. This approach offers a clearer picture of value, emphasizing how much space residents actually receive for their money rather than just the overall cost of buying or renting a home.

ZeroHedge

10. In 1 Sentence, a Retired Electrician Just Explained How to Motivate Anyone (Even Yourself)

Forget purpose. This is more important.

EXPERT OPINION BY MINDA ZETLIN, AUTHOR OF ‘CAREER SELF-CARE: FIND YOUR HAPPINESS, SUCCESS, AND FULFILLMENT AT WORK’ @MINDAZETLIN

Experts often say that the secret to motivation is purpose. They say we all need to know that what we do is contributing to some greater good. That’s always seemed problematic to me, though. Let’s say you work for a fast fashion company doing analysis on sales trends. I suppose you could try to believe that you spend your days crunching the numbers so your company’s sales team can sell more products and that will help more people look a little more stylish, thus making the world a bit better but … that seems like stretch. And indeed, many companies do twist themselves into knots to find reasons why what they do supposedly makes the world better. (This was beautifully lampooned in the series Silicon Valley.)

It’s not about purpose

Forget purpose, Baker argues in his piece. When he retired a couple of years ago, the change hit him hard, he said. At first he thought the problem was a lack of purpose, but it wasn’t. It was a lack of people who needed him. When people need an electrician, they usually need one really badly. When Baker stopped doing that work, people stopped asking for his help, and it was a disconcerting change. “It’s the silence that gets you,” he writes. “The phone that doesn’t ring. The empty calendar. The feeling that nobody needs what you’ve got anymore.”

Eventually, he figured out that he, and his retired friends, really needed to be needed. So he began volunteering, teaching household repairs to young people who were eager to learn them. That turned things around. “Here’s what I’ve learned,” he writes. “You don’t need a massive audience. You don’t need to matter to everyone. You just need to matter to someone.”

Featured Video

Vibe-Coding for Beginners in Five Easy Steps

That last sentence says it all, and not just for retired people. It applies to you and me and everyone who works in your company, or any company. If you want to demotivate someone quickly, make them feel like their mistakes really don’t matter because no one is paying attention. If you want to motivate someone quickly, make them feel like the whole place would tumble down without them. Ask for their help. Tell them you depend on them. It may go against the grain to say that. You may fear they’ll respond by asking for a raise, and they might. But there’s no quicker way to build motivation and loyalty.

We all need to feel needed

Being needed trumps purpose every time. In fact, I think, at least some of the time, when we talk about purpose, that sense of being needed is really what we mean. We can see this clearly with someone who feels their purpose is to provide for their family. We can also see it in people whose job is to save lives, doctors or first responders, for example. But it’s true for all of us.

Whether we’re saving people trapped in a burning building, or preserving a species facing extinction, or even helping colleagues who need marketing data they can rely on, all of us need to feel needed. We want to know that, as Baker puts it, our work matters to someone, even if it doesn’t matter to everyone. For many entrepreneurs, the thought that their employees are depending on them for their livelihoods can be one of the most powerful motivators there is.

It will work on you, too

Next time you want to motivate an employee, or get someone on board for your project or idea, tell them how badly you need them. Next time you want to motivate yourself, focus on the employees and customers who need you. Then watch what happens. And see how much of a difference it can make.

There’s a growing audience of Inc.com readers who receive a daily text from me with a self-care or motivational micro-challenge or tip. Often, they text me back and we wind up in a conversation. (Want to know more? Here’s some information about the texts and a special invitation to a two-month free trial.) Many of my subscribers are entrepreneurs or business leaders. They know how important it is to motivate the people who work for them, and to stay motivated themselves. Feeling needed can be a powerful way to make that happen.

3. Retail Trading Coming Back Strong? HOOD +33% 5 days

Google Finance

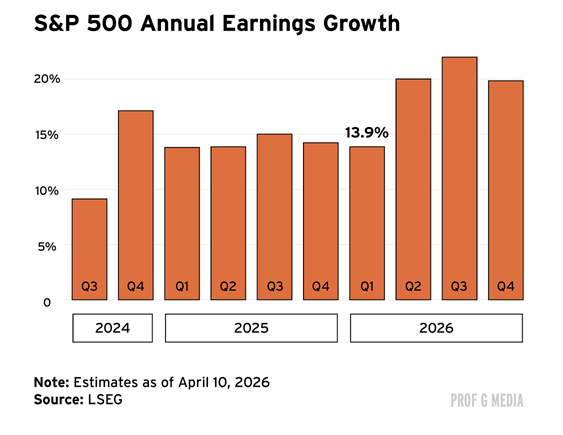

4. Double Digit Earnings Growth Predicted for 2026

Prof G Markets

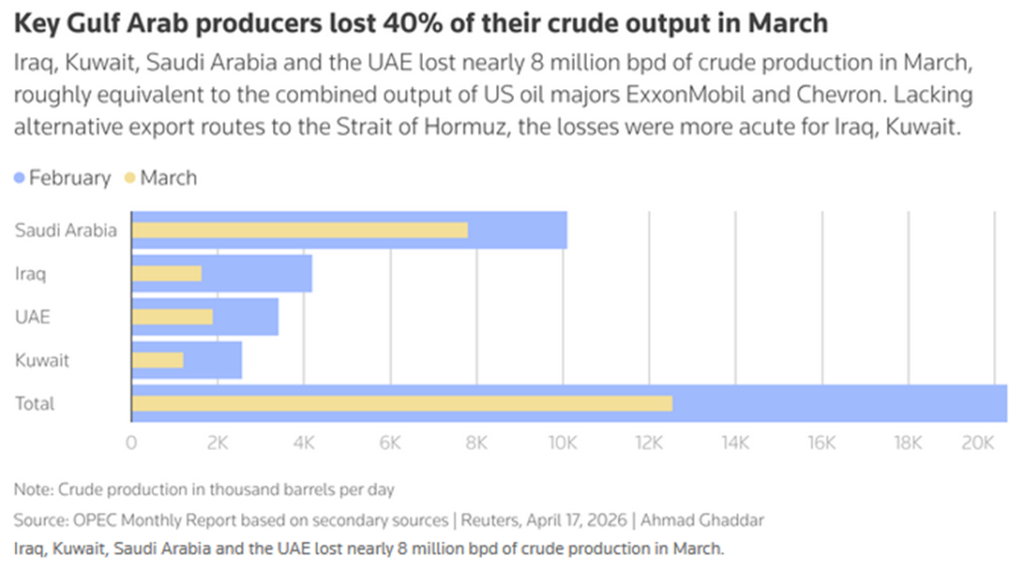

5. Key Arab Oil Producers Lost 40% of Output in March

Dave Lutz Jones Trading

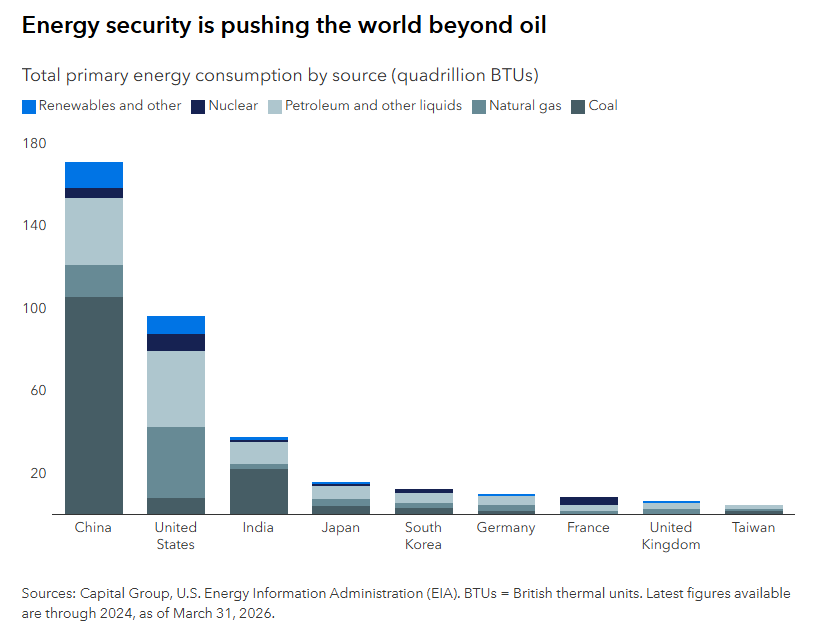

6. Energy Security Pushing World Beyond Oil-Capital Group

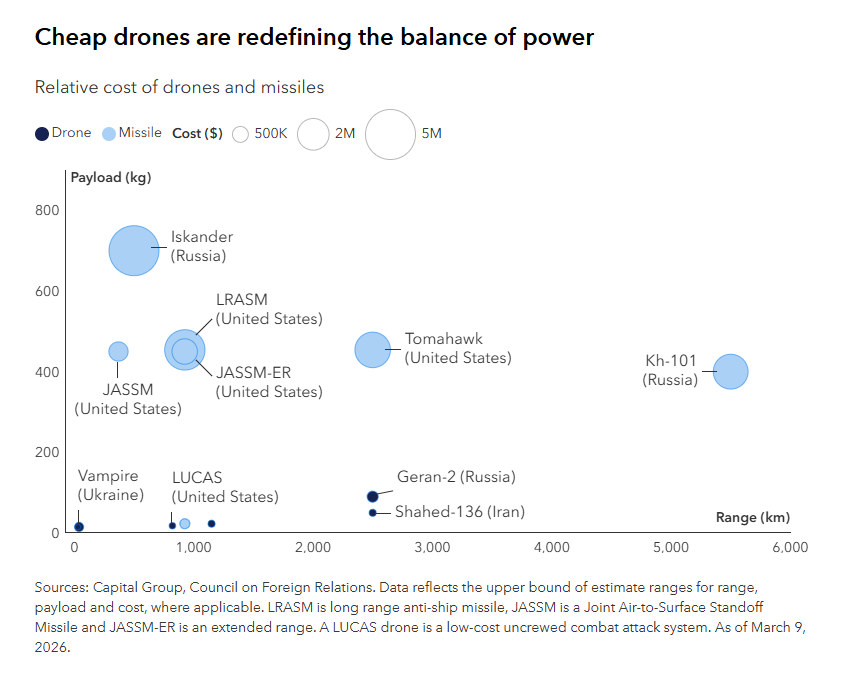

7. Cheap Drones New Warfare.

Capital Group

8. N. Korea $285m Cyber Heist

WSJ

SEOUL—The largest cryptocurrency heist this year didn’t begin with malicious code, but with handshakes.

At a major cryptocurrency conference last fall, members purporting to work at a new quantitative trading firm approached representatives of Drift Protocol, a major player in the world of so-called decentralized finance with roughly half a billion dollars in assets. The two parties then spent months discussing a commercial partnership, both in person and over Telegram.

The relationship ended with the heist of roughly $285 million, according to TRM Labs, a blockchain analytics company that tracks crypto movements and analyzed the hacking episode.

Google

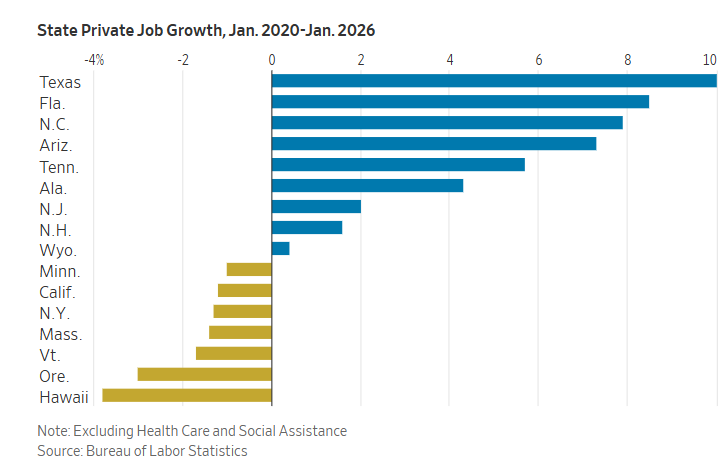

9. State Tax and Jobs Divide….Migration to Low Tax States.

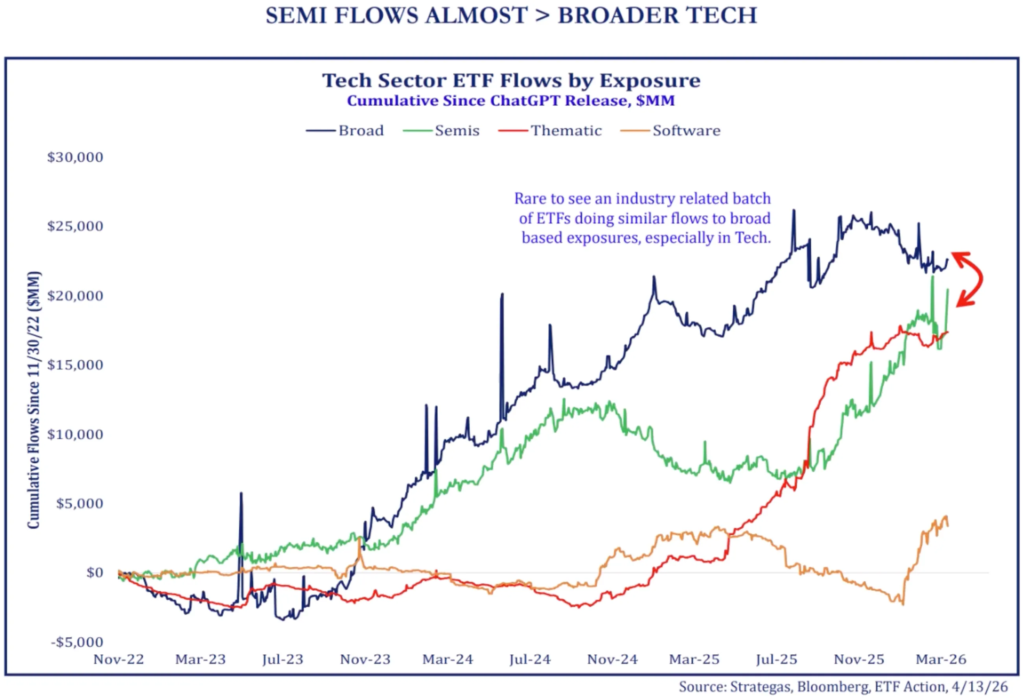

Tech sector ETF flows. “Chart shows you Tech sector ETF flows by different exposures since ChatGPT’s release roughly 3 years ago … this is pretty rare, to see an industry group overtake the broader sector exposure in our work.”

Todd Sohn – Strategas

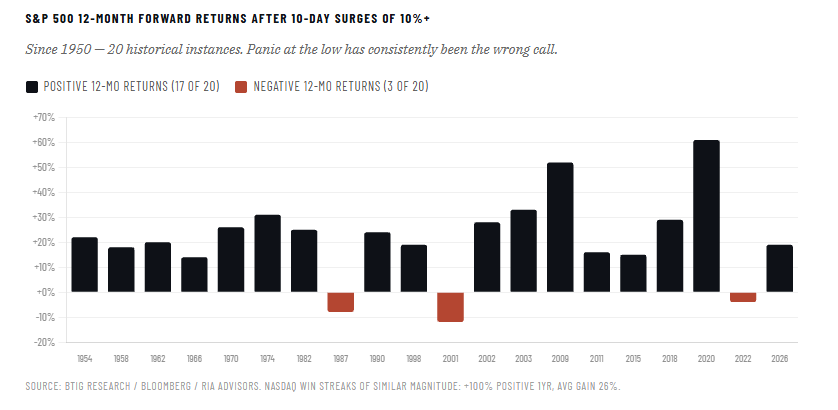

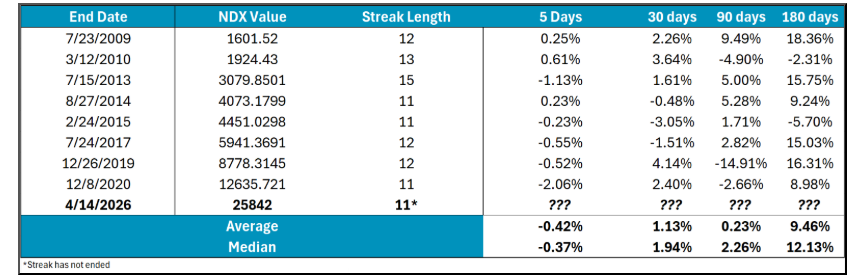

2. History of 12 Day Win Streaks for Nasdaq

Nasdaq Dorsey Wright

3. Israel Stock Market New All-Time Highs

Barchart

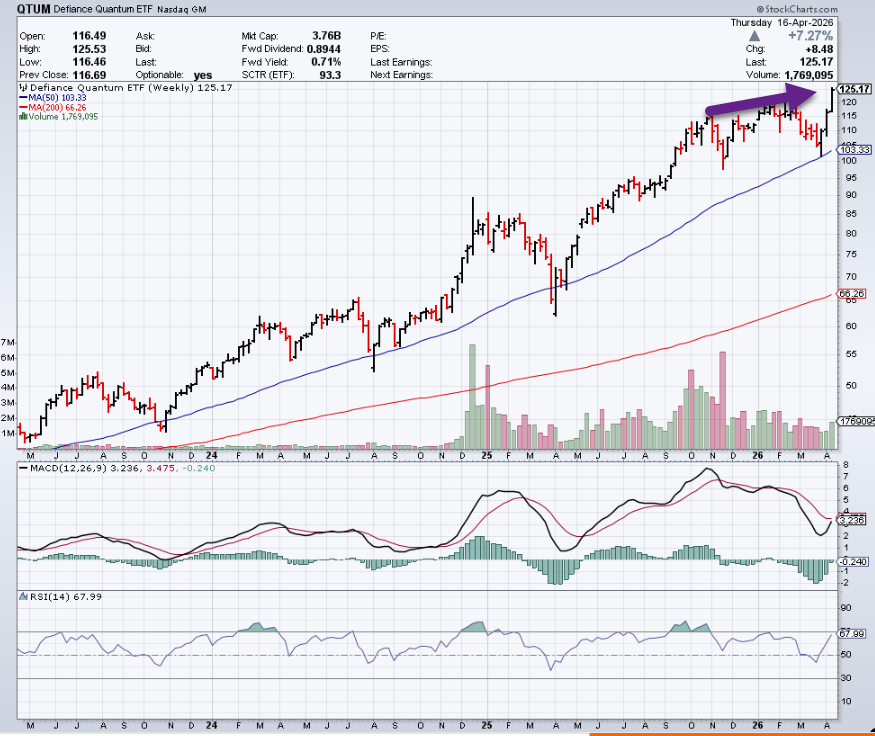

4. Quantum Computing Stocks New Highs

StockCharts

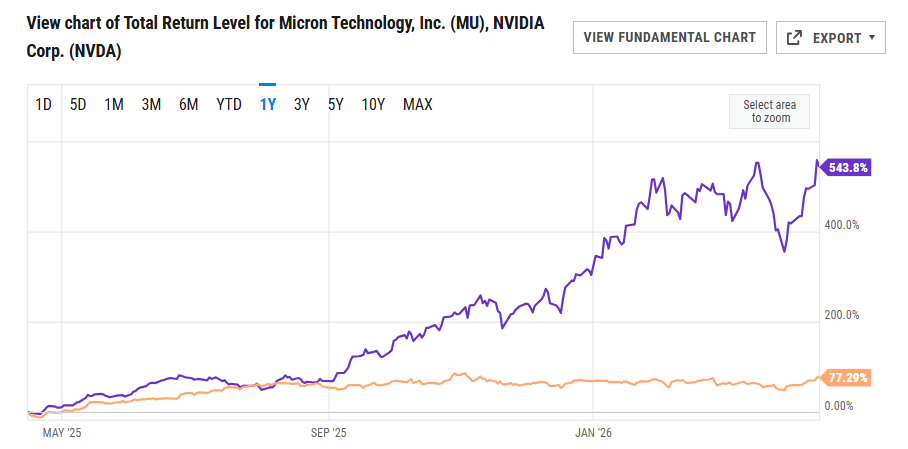

5. MU vs. NVDA One-Year Chart…Even on 3-Year Chart

Ycharts

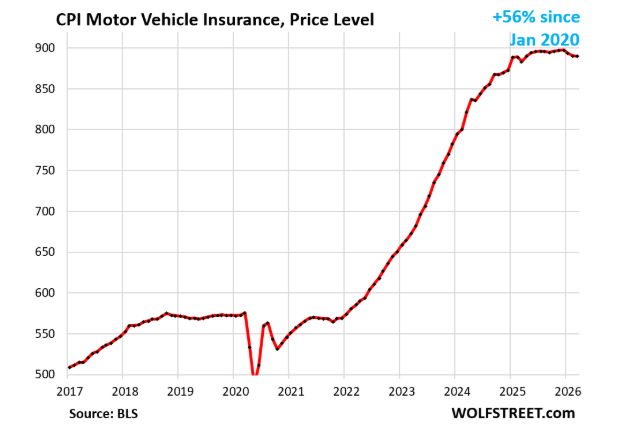

6. Inflation in Car Insurance

Wolf Street

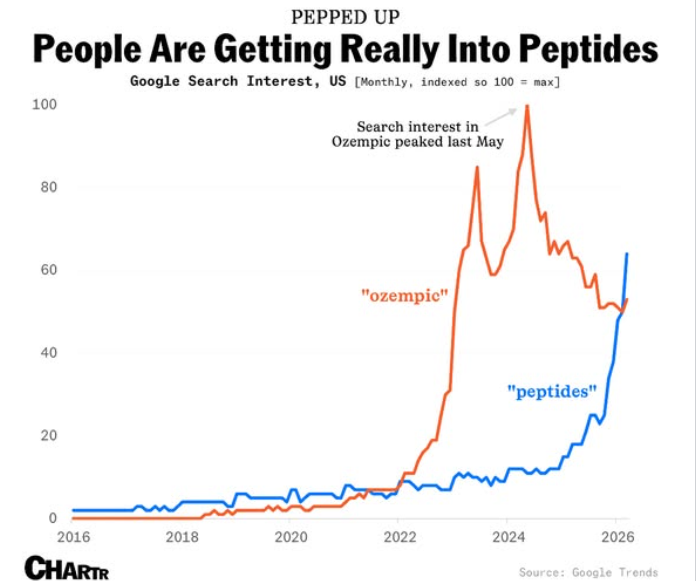

7. Peptides Moving to FDA Reviews

8. HIMS Talking Peptides…Stock +35% 5 Days

Google finance

9. Russian Blogger Gets 20m Views—“The People are Hurting”

Kremlin acknowledges criticism after blogger warns Putin ‘squeezed’ Russians could erupt

Accuses officials of misinforming him about problems

Video appeal gets more than 20 million views

Kremlin responds and says issues are being addressed

MOSCOW, April 16 (Reuters) – The Kremlin took the unusual step of publicly acknowledging sharp criticism of the authorities from a celebrity blogger on Thursday, saying work was under way to address a slew of problems identified by social media influencer Viktoria Bonya.

Bonya, who is well known inside Russia for her appearances on reality TV shows and other programmes, has a huge social media following, and a video appeal she made to President Vladimir Putin this week was watched more than 20 million times and liked over 1 million times on Instagram.

In her video appeal, Bonya – who lives outside Russia – said she supported Putin, but said that officials were not telling him the truth about the country’s real problems, that the Russian people were suffering, and that they were being squeezed so hard by corrupt officials that they might one day erupt.

“You know what the risk is?” she said. “That people will stop being afraid and they’re being squeezed into a coiled spring and that one day that coiled spring will shoot out.”

10. Saudi Fund to Back Away From LIV Golf Under Mounting Financial Pressures

The Saudi league, established in 2022, attracted some of the sport’s biggest stars with huge contracts

Yasir al-Rumayyan, left, the head of Saudi Arabia’s sovereign wealth fund, presenting a trophy at the LIV Golf championship in Michigan in 2025.Credit…Raj Mehta/Getty Images

Saudi Arabia’s sovereign wealth fund is on the verge of announcing it will withdraw financial support from LIV Golf, the upstart golf circuit it launched four years ago to compete with the PGA Tour, a person familiar with the matter said Wednesday.

The Saudi league splashed into professional golf in 2022, attracting some of the sport’s biggest stars with contracts that exceeded — by tens of millions of dollars — their career earnings with more established circuits like the American-run PGA Tour.

The move comes as Saudi Arabia’s $1 trillion sovereign wealth fund announced a new five-year strategy on Wednesday, with the fund’s governor saying it would slow down some of its biggest projects as it focuses on “increasing the efficiency of investments.”