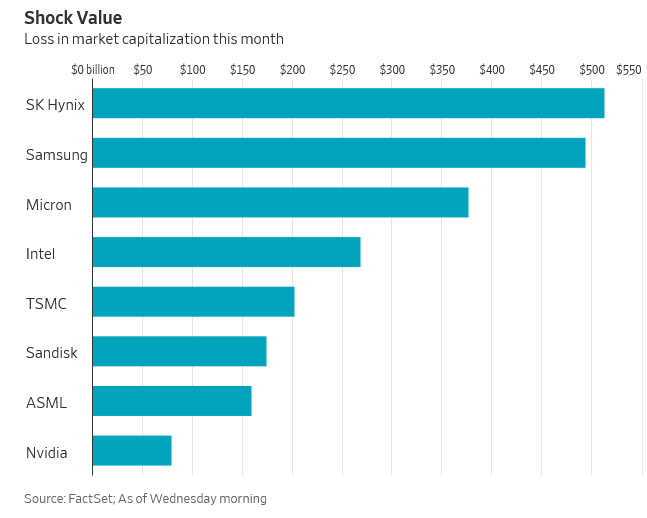

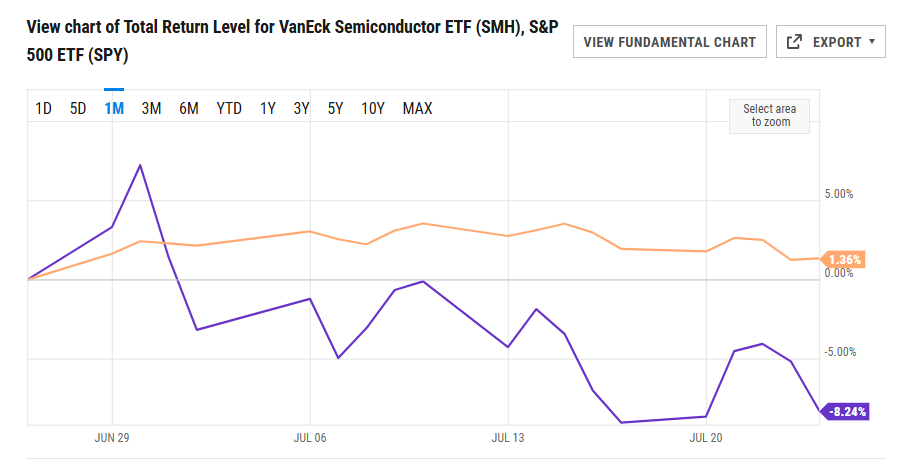

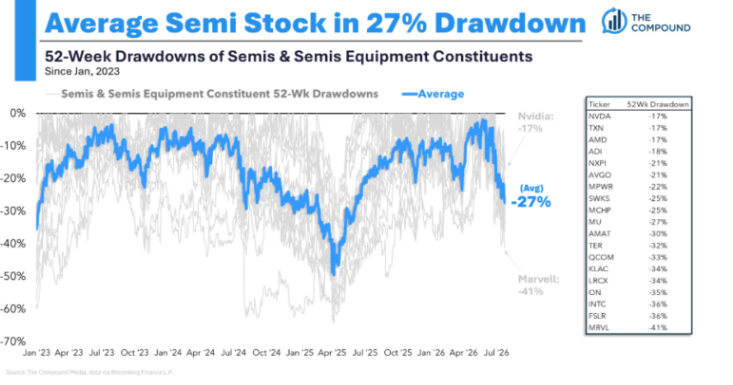

1. Average Semi Stock -27% from Highs

A Wealth of Common Sense

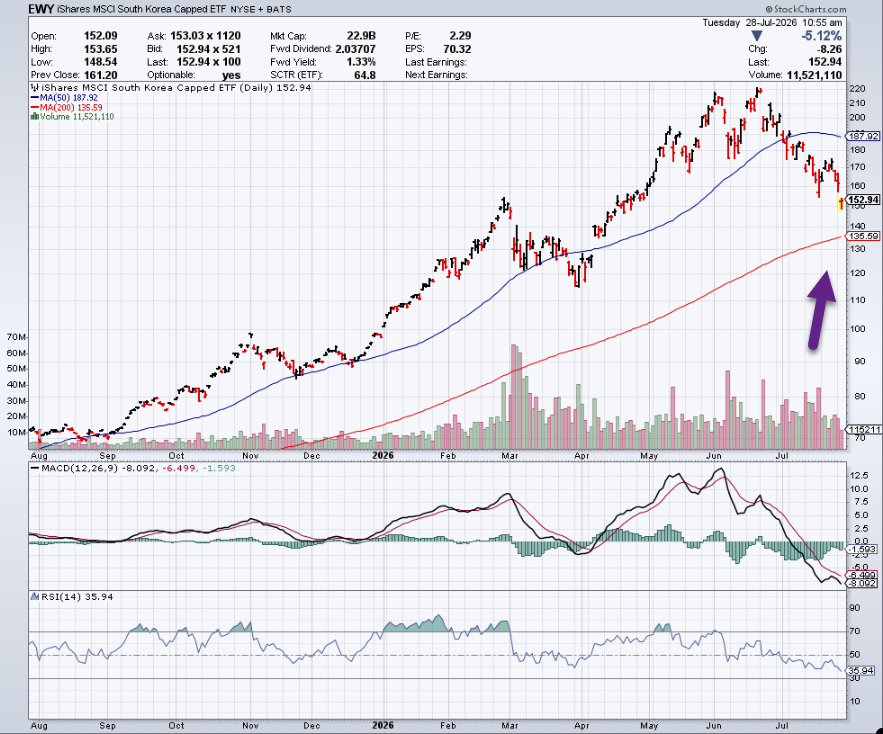

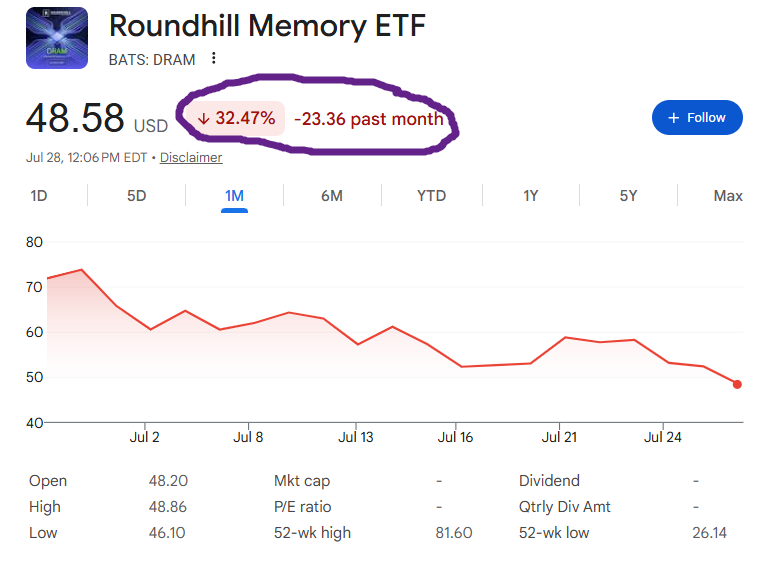

2. 3x Korea ETF -80% in 2 Mhs

zerohedge

3. QQQ 20 Points From 200-Day

StockCharts

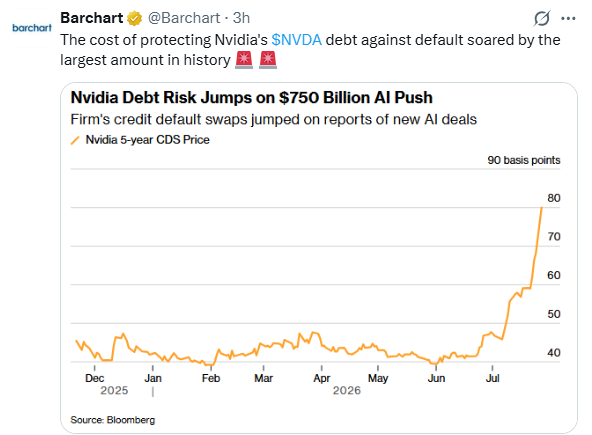

4. Cost of Protecting NVDA Against Default Rising….Stock at 18x Forward P/E

Barchart

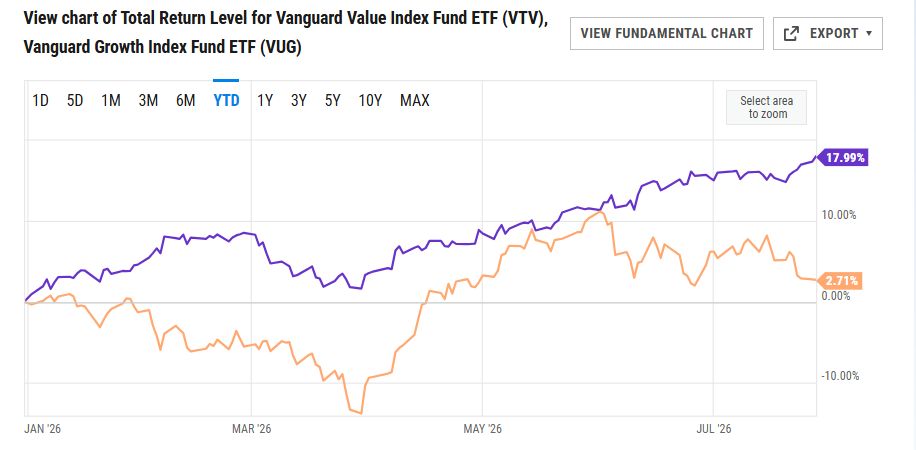

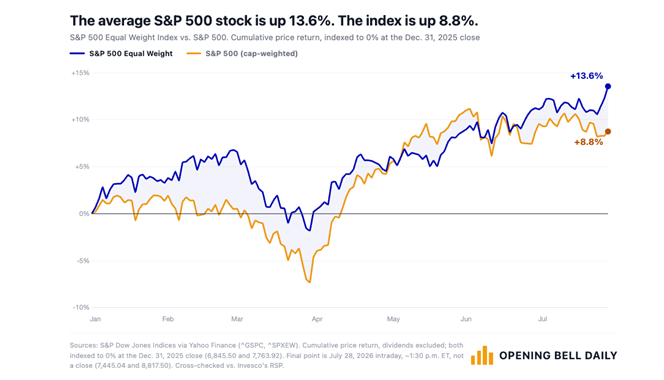

5. Market Holding Up in Tech Sell Off….Equal Weight Outperforming

Opening Bell Daily

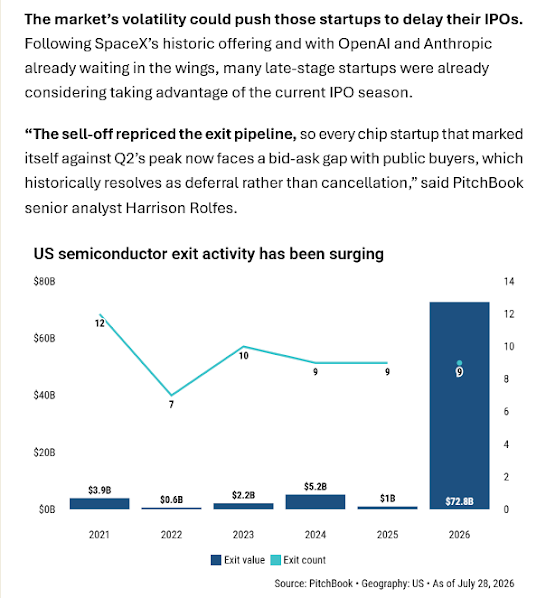

6. Semiconductor Related IPOs

PitchBook

7. Stocks Related to Infrastructure Build Out of AI Big Corrections….VRT -40% …MTZ -48%

StockCharts

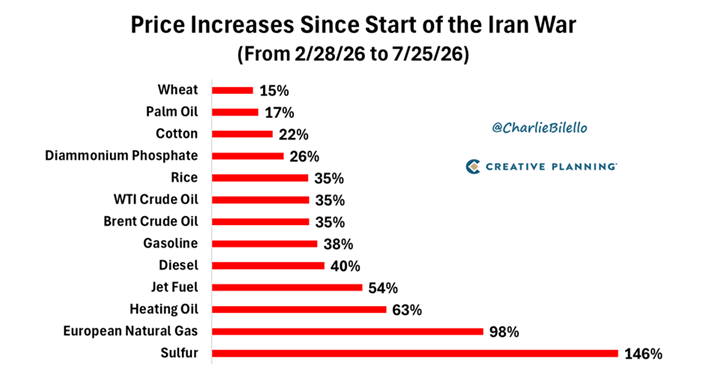

8. Updated-Price Increases Since Iran War

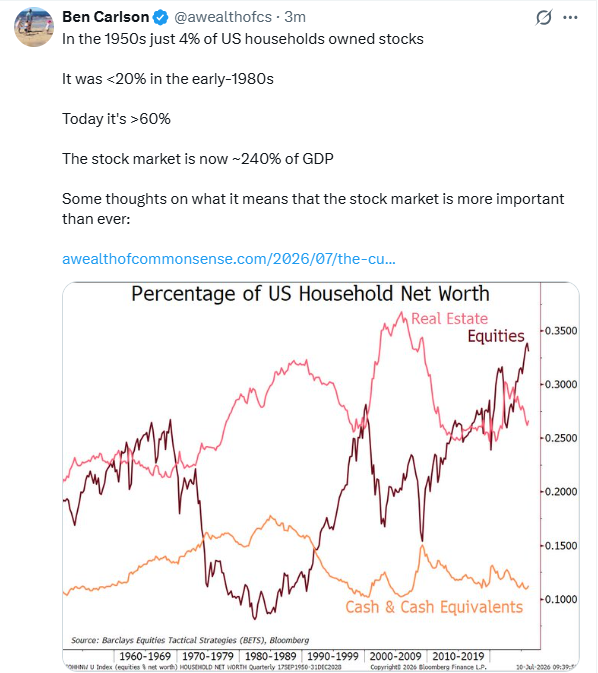

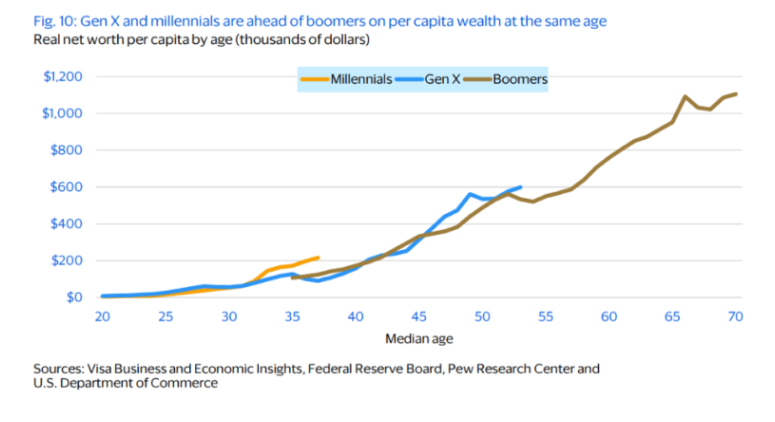

9. Gen X and Millennials Ahead of Boomers in Wealth

A Wealth of Common Sense

10. 10 Ways to Build and Expand Perspective

Psychology Today Robyne Hanley-Dafoe Ed.D.

- Get curious: Perspective grows every time we are exposed to different ideas, people, and experiences. Read books written by people whose lives look different from yours. Listen to podcasts that challenge you. Ask someone, “Tell me more,” and listen to understand rather than just waiting to respond. Curiosity stretches perspective.

- Zoom in, zoom out: When something feels overwhelming, zoom in first. Name what’s happening and feel what you’re feeling. Then zoom out. Ask yourself, “Will this matter in a week?” “In a year?” “How does this fit into the bigger story of my life?” Distress narrows our focus until everything feels urgent. Perspective helps us respond to what is important versus simply reacting to what feels loud.

- Notice the stories you are telling yourself: The way we narrate our own lives becomes the perspective we live inside of. “I’m a bad sleeper” is a very different sentence than “I’m someone who can sleep well under the right conditions.” The facts of the night might be identical. The story you carry forward is not.

- Collect evidence: Our brains naturally collect evidence that confirms what we already believe. If we believe we’re failing, we’ll notice every mistake. If we believe we’re making progress, we’ll start noticing growth. When you catch yourself telling a difficult story, try asking yourself, “What evidence supports this?” and “What evidence challenges it?” Perspective grows when we consider the whole picture, not just the pieces our brain highlights first.

- Change your physical view: Sometimes changing your physical perspective helps to change your mental one. Get outside, stand under the big sky, walk beside water, look out over a landscape. There is something about being reminded of how vast the world is that helps us right-size many of our worries.

- Borrow someone else’s perspective: Sometimes we’re standing too close to the problem. Ask a trusted friend, “What am I missing?” or “Help me think this through.” The people who love us can often see possibilities that we’ve temporarily lost sight of ourselves.

- Practice the power of “yet”: The attitude we bring to our learning and challenges is extremely important. For example, “I don’t know how to do this” and “I don’t know how to do this yet” send our brain two very different messages. “Yet” leaves room for growth, learning, and hope.

- Recognize dual truths: Our brains are hardwired to focus on the negative, and in the midst of life’s storms, that makes perspective genuinely hard to hold o. Perspective expands when we stop believing we have to choose between two competing truths. For example, you can be disappointed and proud of how hard you tried. You can be grieving and grateful. You can feel uncertain and hopeful.

- Try “Unfortunately… Fortunately…”: This has become a family favourite of ours. It allows us to hold two truths at the same time, without pretending the hard part is not hard. Unfortunately, I’m stuck in traffic. Fortunately, I get more time to listen to my favourite podcast. Unfortunately, the presentation didn’t go the way I’d hoped. Fortunately, I know exactly what I’ll do differently next time.

- Build a gratitude practice: Our first thoughts of the day are the most powerful thoughts for the day. As soon as you are conscious or awake, say “Thank you.” Waking up to a new day is something to be grateful for. Then take a moment to hold space for what you have and what you get to do today.

Final Thoughts

Every day we have opportunities to zoom in with honesty and zoom out with wisdom. We can get a little more curious, gently challenge the stories our brains automatically tell us, and remember that one bad hour is exactly that: an hour. Perspective widens what we can see and what feels possible. It helps us make what matters most matter most.