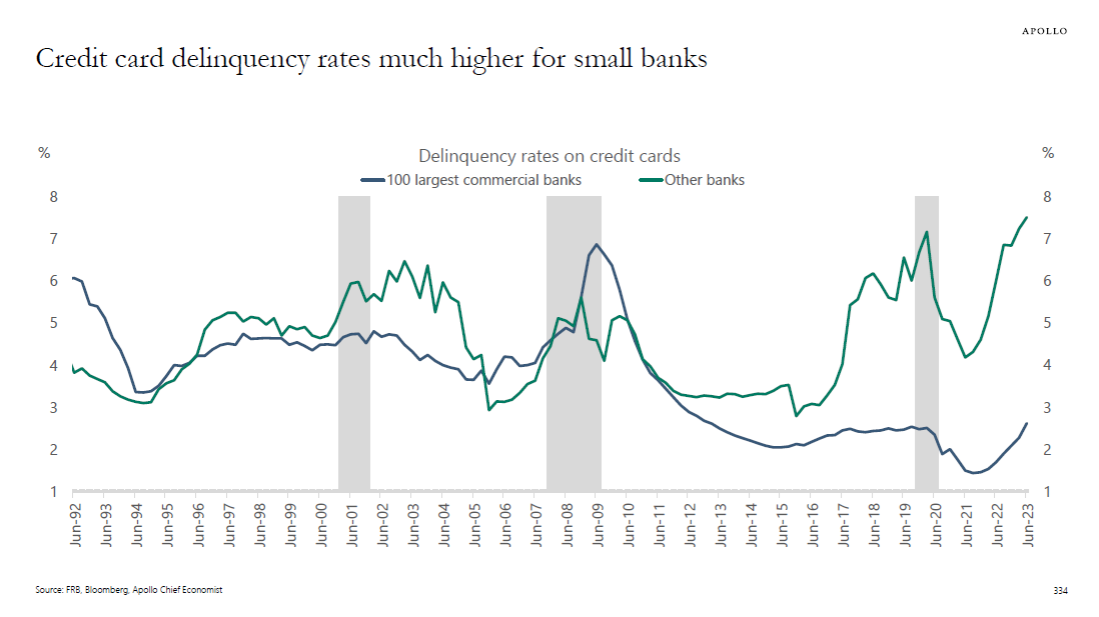

6. Credit Card Delinquency Rates Much Higher for Small Banks.

Despite the unemployment rate being at the lowest level in 50 years, credit card delinquency rates at small banks are at the highest level on record, see chart below. Imagine where these lines will be once the labor market finally begins to soften. Torsten Slok, Ph.D.Chief Economist, PartnerApollo Global Management

7. China Evergrande Group is Now a Penny Stock…$340B in Debt.

3. Shrinking Number of Stocks vs. Growing Number of Private Equity Backed Companies

Callum Thomas Privatization: This should be a shocking chart for passive index investors — more and more of the universe of US companies are ending up in the hands of private equity, with relatively fewer staying or joining public markets. One implication would be potentially a less diversified listed market over time, but also potential risks in private markets due to less transparency and greater leverage that typically comes with private equity investors. It also gives nod to the flood of capital into alternative assets in the zero-interest rate period and in the wake of the dot-com and financial crisis bear markets (that in-part drove investors into the ostensibly lower volatility of private equity vs listed companies).

A once-hot sliver of the exchange-traded funds universe focused on thematic investing is having another difficult year.

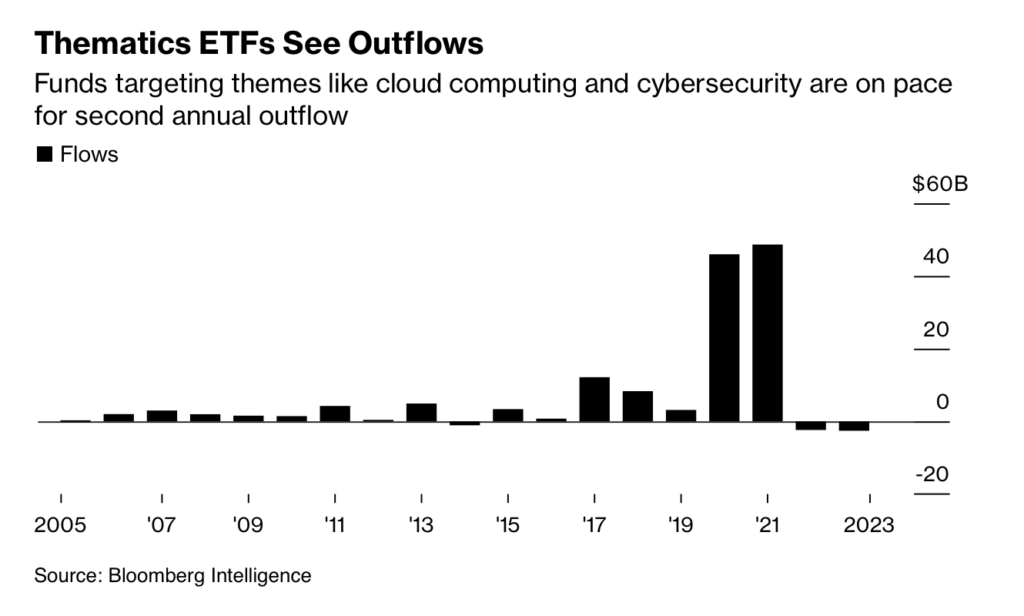

Investors have yanked roughly $2.6 billion from these types of ETFs so far in 2023, putting them on pace for their worst year of outflows in data going back to 2001, according to Bloomberg Intelligence. If the trend holds it will be the second consecutive year of cash leaving thematic funds, the first such losing streak of the last two decades.

Much of the cash drainage can be attributed to funds that are part of the ARK Investment Management suite, where the firm’s Innovation fund (ticker ARKK) has seen more than $450 million flee this year. Money has also come out of the ARK Next Generation Internet ETF (ARKW), as well as out of the ARK Genomic Revolution ETF (ARKG), among others.

5. Chinese Small Cap Stocks Approaching 10-Year Lows

ECNS Chinese small cap ETF broke 10-year in late 2022….Now making another run at new low.

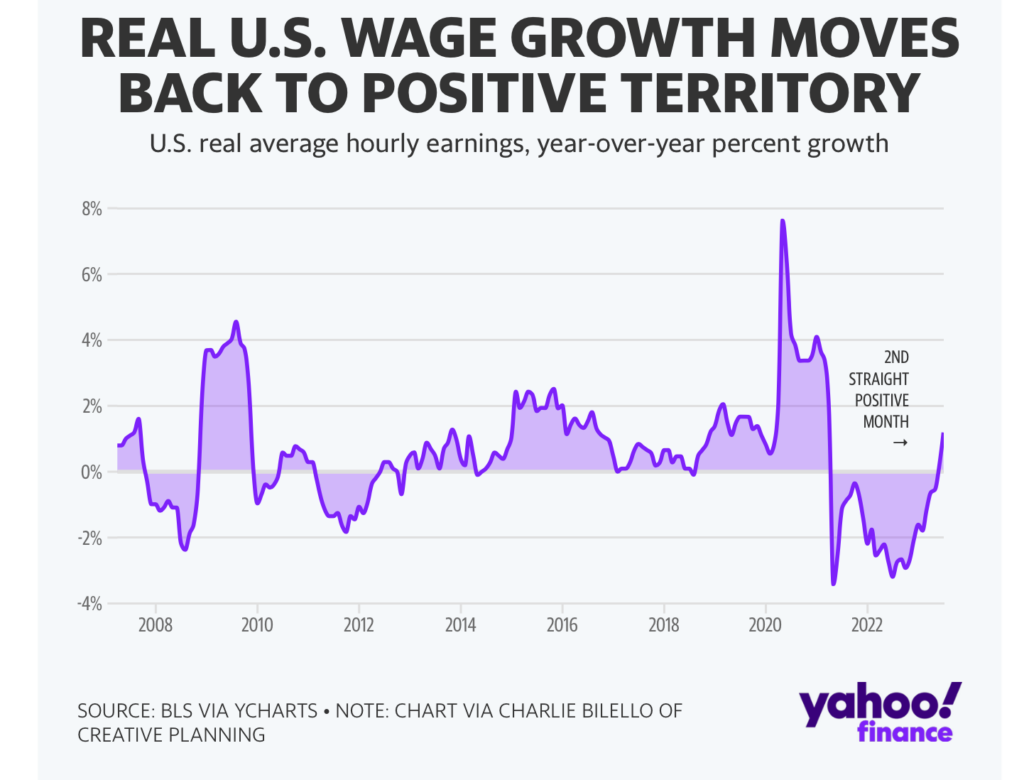

6. Real U.S. Wages Moved Back to Positive Territory

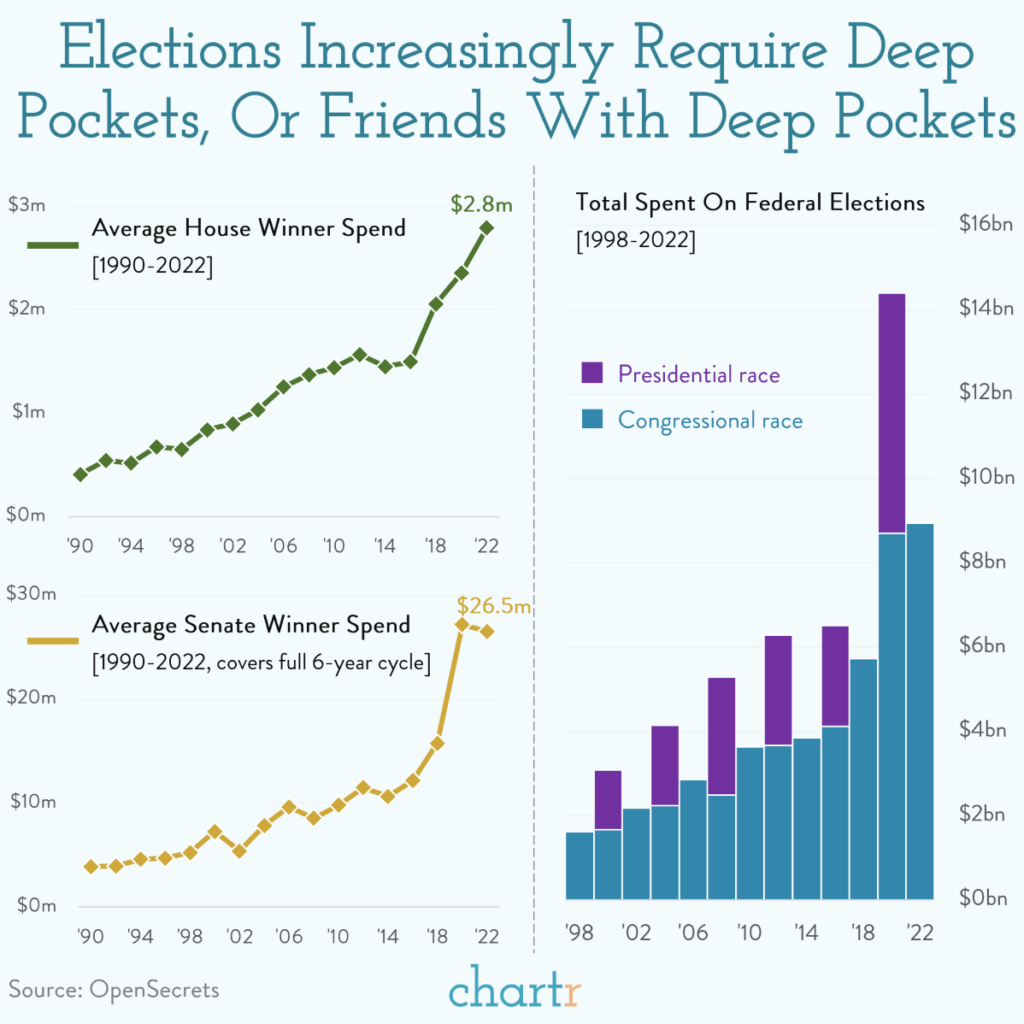

9. Get Ready for $20B in Spending on Presidential Election

Chartr Blog Indeed, data from OpenSecrets reveals that the most recent presidential election set a new record as the most expensive cycle in history — and by some way, with political spending for the 2020 showdown tallying an eye-watering $14.4bn, or a staggering $16bn if adjusted for inflation.

5. 20% of Private Valuation Unicorns Fall in AI Sub-Sector

MorningstarJohn Rekenthaler Most unicorns sell technology. One fifth of unicorn assets are in companies devoted to artificial intelligence, with another 15% in financial technology and 12% in e-commerce businesses. Software services, telecommunications, and biotechnology are also well-represented.

6. Regional Bank ETF Bounce did not get Close to 200 Week Moving Average

Unfortunately, many of the business professionals I meet these days in my mentoring and consulting activities feel perennially stressed and out of control, versus calm and satisfied with their position. They realize that their productivity is suffering, as well as their health, but they don’t know what to do about it. In my experience, it’s all about work-life balance and enjoying the role.

Over my years in business, I have accumulated a list of recommended strategies for keeping cool and calm in the face of increasing demands at work. On the top of my list is a focus on minimizing multitasking, a result of continuous smartphone and email alerts, as well as an instant gratification mentality. Trying to do too many things at the same time, in my view, results in nothing done well.

Here is my prioritized list of work management strategies I recommend to all business professionals and entrepreneurs:

1. Avoid reliance on multitasking to keep up with requests.

Take the time to fully focus on each task you are faced with, and your decisions and productivity will improve. Make every effort to have your mind be totally present for each challenge from a team member or customer. You will also find this reduces stress and allows you to stay cool and calm.

Some recent studies by scientists assert that multitasking not only reduces your output, but it also reduces your IQ. Some say that when people do two cognitive tasks at once, their cognitive capacity can drop from that of a Harvard MBA to that of an 8-year-old.

2. Schedule uncomfortable tasks when you are fresh and alert.

Practice scheduling your most onerous tasks, such as counseling team members or meeting unhappy customers, when you are most calm and collected at the beginning of a day, or when you are least likely to be distracted. Balance your time on strategy and operational issues.

In simple terms, this means managing your own schedule, rather than allowing events and distractions to manage you. Some successful people do this by establishing a routine and sticking to it, or by writing down and managing their own list of open work items.

3. Practice patience to listen before reacting out of emotion.

Always start by taking a few deep breaths to reset your mind and body when approached with a new issue. Then actively listen to input, asking questions to get to the root cause before jumping to conclusions that may be clouded by ego, biases, and previous similar experiences.

4. Look at each challenge with a fresh and clean perspective.

Avoid the tendency to jump to a conclusion based on past situations. Challenge yourself to avoid emotional reactions and look for fresh new information rather than stereotypes. Express your logic out loud and ask trusted associates to critique your perspective for credibility.

5. Seek to provide thoughtful and sincere responses to input.

This effort will force your mind to organize thoughts and structure your understanding of the issues at hand. Focus on a calm and sensitive delivery to gain the trust and credibility you need for maximum impact and following from constituents. The results will be more satisfying for you as well.

6. Find an activity to clear your head and refocus on the positives.

For some of us, that may mean taking a coffee break or a walk around the park. Let go of the hard negatives and focus on the rewards for yourself and other team members. Another alternative is to switch often to less demanding tasks, such as email or managing by walking around.

7. Avoid extended internal battles with tough problems.

Make a reasonable mental effort to understand and resolve every challenge, but don’t rehash every issue incessantly to the point of mental exhaustion and frustration. There will always be some problems that aren’t easily solved, and more pain will only make you less effective.

8. Intentionally schedule at least one enjoyable activity every day.

Try to balance the difficult tasks on your schedule, such as counseling employees, with ones you look forward to. For some of us, that may mean quiet time to contemplate strategy, or coffee time to chat with team members and customers. Celebrate even small successes.

In today’s business environment of information overload and a thousand ways to get interrupted, we all face the same pressure to move fast, and deal with the many distractions. I challenge each of you to spend more time managing your time and focus, rather than simply trying to react real-time to all the competing demands coming your way. Your career and your health depend on it.

AUG 22, 2023

The opinions expressed here by Inc.com columnists are their own, not those of Inc.com.

A refreshed look at leadership from the desk of CEO and chief content officer Stephanie Mehta

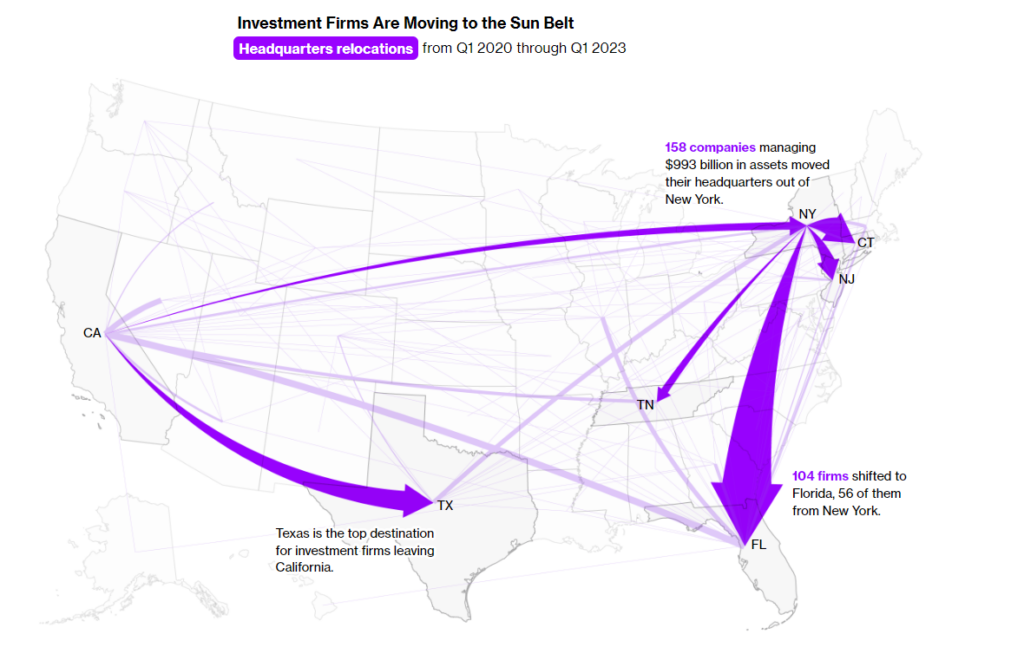

The drip, drip, drip of the finance industry’s exit from New York and California has been measured anecdotally, one at a time, these past few years. Elliott Management decamped to West Palm Beach. AllianceBernstein to Nashville. Charles Schwab moved to suburban Dallas.

Now, for the first time, there are hard numbers quantifying the exact scope of the exodus. Both states have in the past three years lost firms that managed close to $1 trillion of assets, Bloomberg News calculated after going through corporate filings from more than 17,000 firms since the end of 2019.

The exodus from the Northeast and West Coast has meant the loss of thousands of high-paying jobs, straining city and state finances by sapping tax revenue. Commercial property markets have also lost valuable tenants at the same time they’ve been struggling with the new realities of hybrid work.

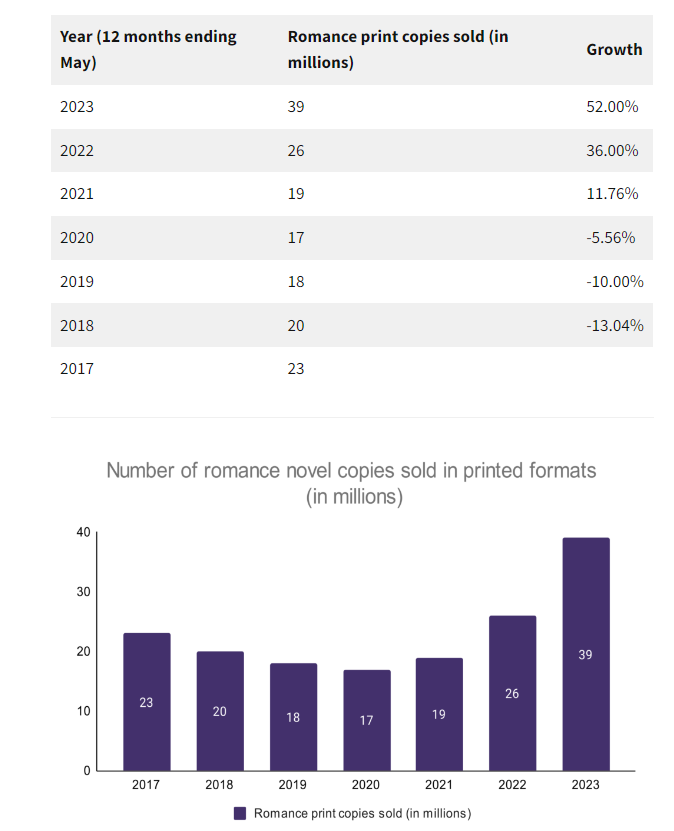

· Romance reached over 39 million printed units sold over the last 12 months as of May 2023.

· Romance sales grew by 52% compared to the 12 months ending May 2022, and this has been the third consecutive year with positive growth in romance novel sales in printed format.

· Sales of romance novels more than doubled compared to 2021 figures (12 months ending May 2021).

· Over 33% of books sold in mass-market paperback format were romance novels.

10. This Is How To Succeed Under Pressure: 4 Secrets From Astronauts

Eric Barker

This is how to succeed under pressure:

“Okay, what’s the next thing that will kill me?”: Negative thinking can be a positive during a crisis. When you’re facing a perverse all-you-can-eat buffet of misery, anticipating problems and finding solutions is a superpower, while “thinking it will all work out” leads to a passive demise.

“Sweat the small stuff”: Prepare. And then prepare some more. You may think you’re busy now but you will always have more time before a problem strikes than when you’re in the middle of it.

“Working the problem”: Find a way to safely experience the challenge before it ever hits. May sound like the emotional equivalent of chewing aluminum foil but nothing beats the understanding and experience from having dealt with a problem previously.

“How can I help us get where we need to go?”: Yes, it seems like some people are only here to give you a head start on a midlife crisis. The first thing is don’t make things worse. Don’t be afraid to be a big steaming pile of mediocrity at first. Be competent and trustworthy and then find the best way to be a “plus one.”

1. Stock Bond Ratio Breaks Way Above 25 Year Range

Callum Thomas Chart Storm Stocks vs Bonds: As a continuation or different angle on the previous chart, this one shows just how sharp and stark the disconnect between stocks and bonds has become — thanks to the most catastrophic run of performance for treasuries in recent history, stocks have absolutely smashed bonds on a relative performance basis. But to pause and reflect, this chart does NOT look sustainable. https://www.chartstorm.info/

2. Huge Spread Between Nasdaq and Russell 2000 Small Cap 2023

From Dave Lutz at Jones Trading

3. Analysts Raise Forward Earnings Estimates

4. China High Yield Real Estate Chart

Callum Thomas @Callum Thomas (Weekly S&P500 #ChartStorm) Next Shoe to Drop: Aside from the tech/rates aspect, also lurking in the background is increasingly bad macro in China. Now eventually this may become a case of “bad news is good news” when/if China opts for large scale stimulus to avert a deflationary spiral, but I would say until then it’s probably going to be a case of bad news is bad news (at least for those actually paying attention).