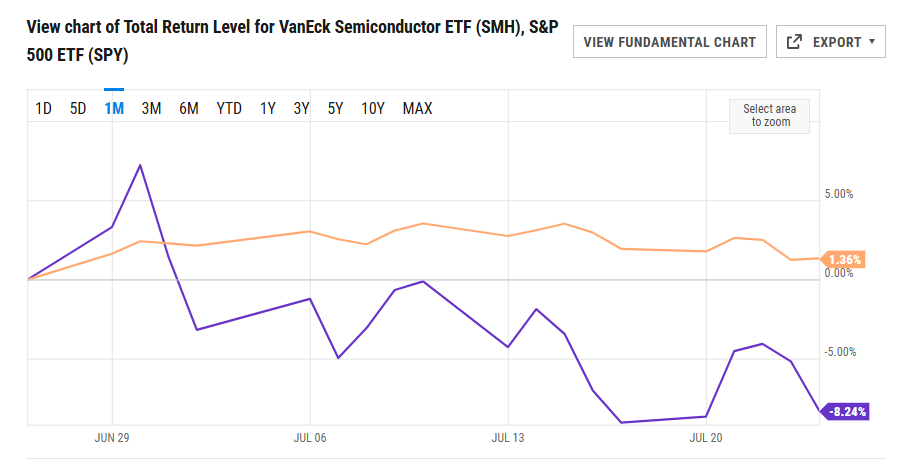

2. One Month Semiconductors Underperform S&P by -10%….S&P +1.26% vs. SMH -8%

YCharts

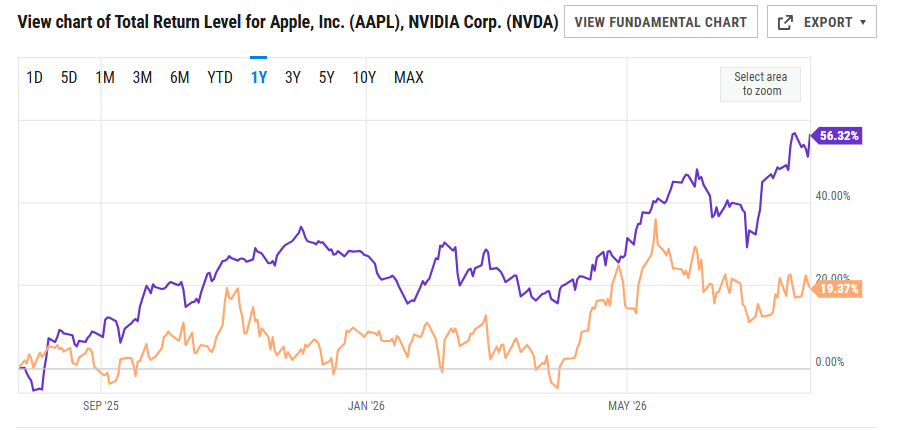

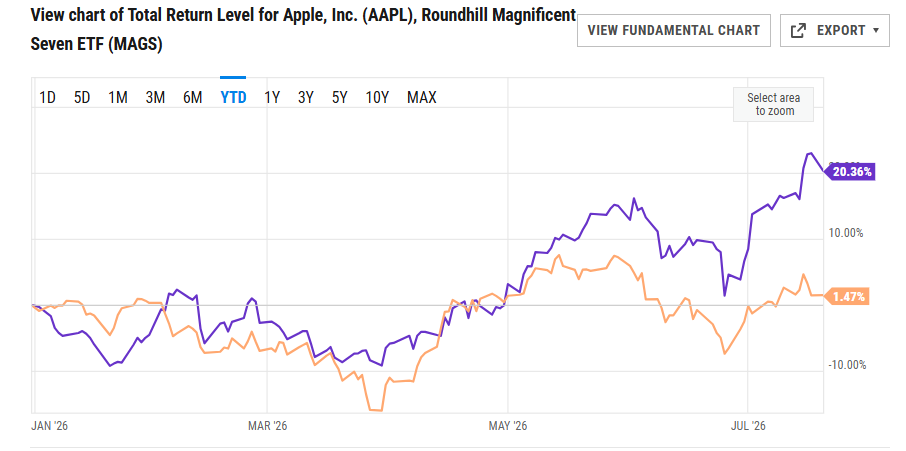

3. One-Year Chart AAPL +56% vs. NVDA +19%

YCharts

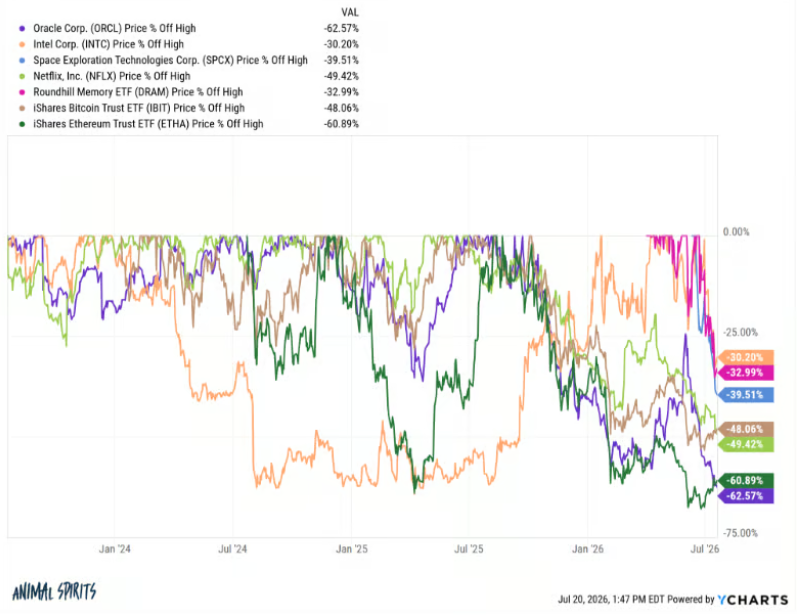

4. Drawdowns on Some Favorite Retail Investor Names-Irrelevant Investor

The Irrelevant Investor

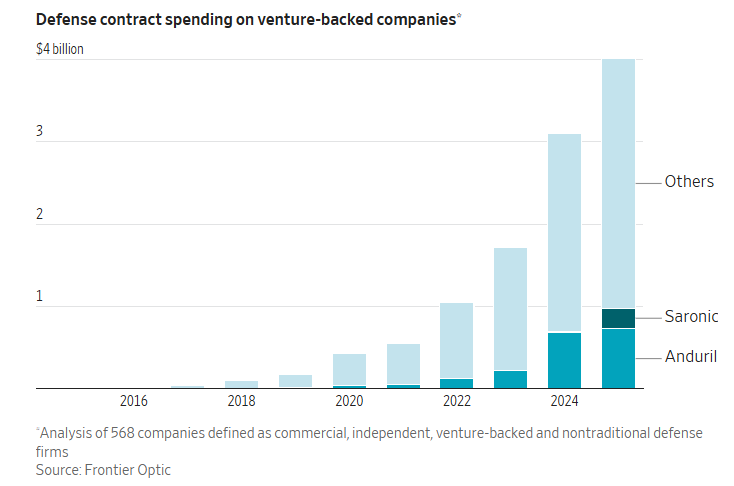

5. Defense Contractors Spend on Venture Back Military Start Ups

WSJ

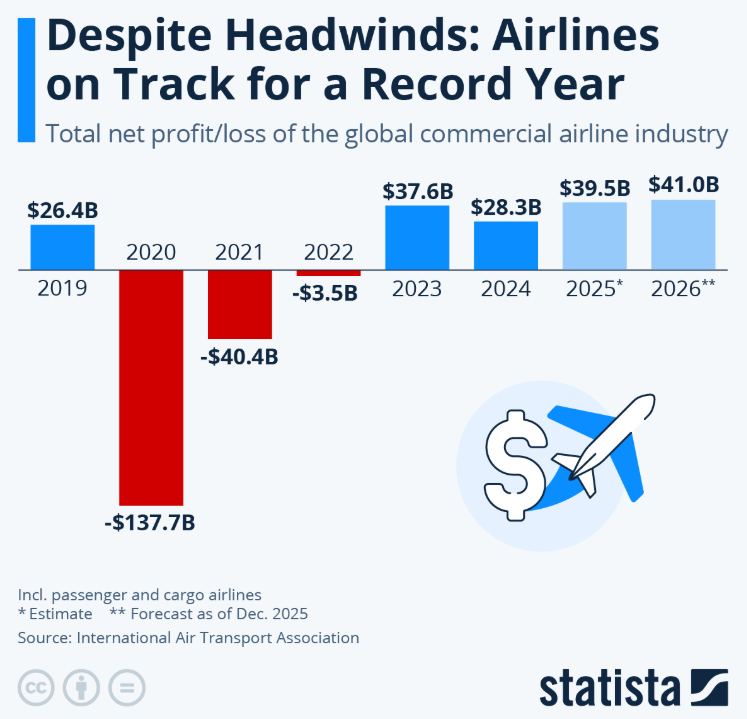

6. Airline Margins Around 3-6%….Airline Margins on CC Points 50-60

Statistics

7. Big Banks Are Wading Back Into Commercial Real-Estate Lending-WSJ

Lenders were shunning the category just a few years ago, with investors and analysts warning of a wave of defaults By Ben Glickman

Big banks are on the hunt to grow their loan books and are turning back to an area they had shunned not that long ago.

Just a few years ago, banks couldn’t get away from commercial real-estate loans fast enough, fearing potential losses as office vacancy rates remained elevated after the pandemic.

Now, they are wading back in with a focus on big growth areas like multifamily housing and industrial real estate, which is being fueled by a boom in big data-center projects. They are doing so with tighter lending standards, they say, while still working through some troubled loans stemming from continued distress in some office markets.

Overall, commercial real-estate mortgage loan originations in the first quarter were up more than 50% from a year earlier, according to a survey by the Mortgage Bankers Association, driven in part by an 80% increase in loans from deposit-taking institutions.

“There’s kind of an awakening that it’s probably safe to go back into the water,” said Citizens Financial Group Chief Executive Bruce Van Saun. “We need earning assets, and we can find some attractive earning assets.”

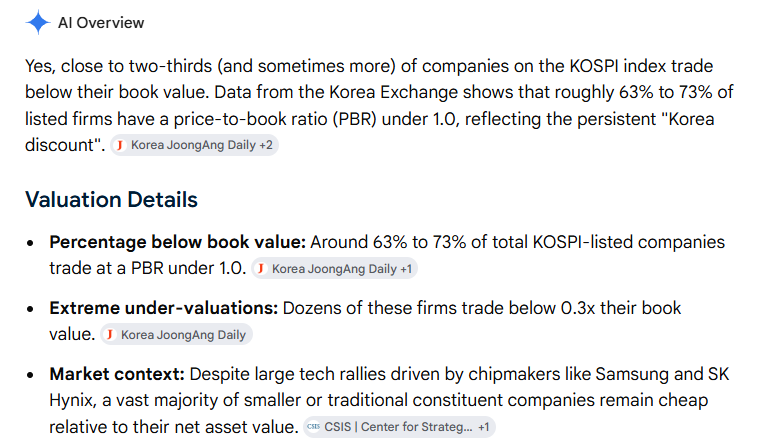

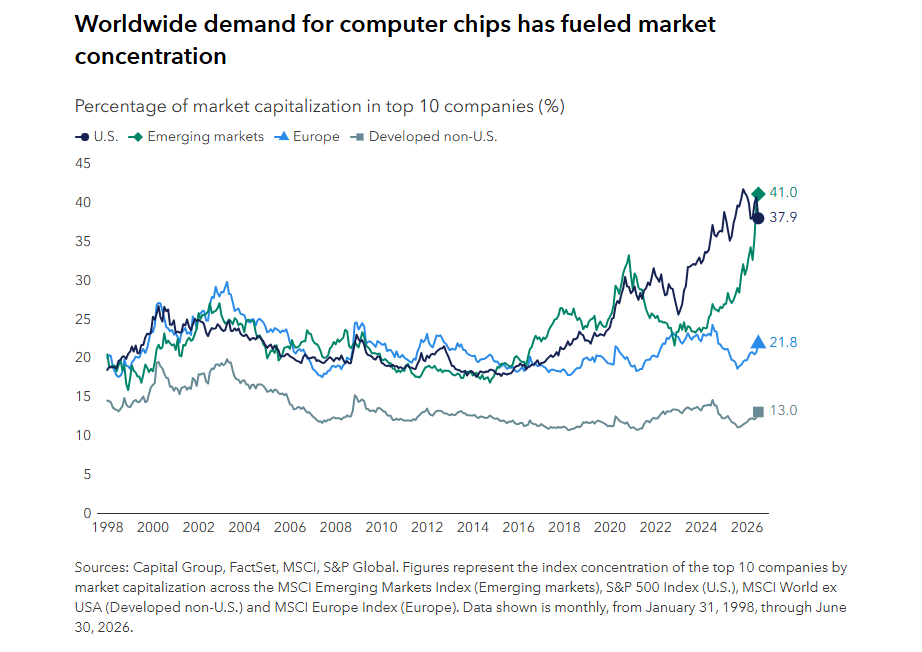

3. Concentration of Returns is Global Stock Market Issue…Emerging Market Concentration Now Higher than U.S.

Capital Group

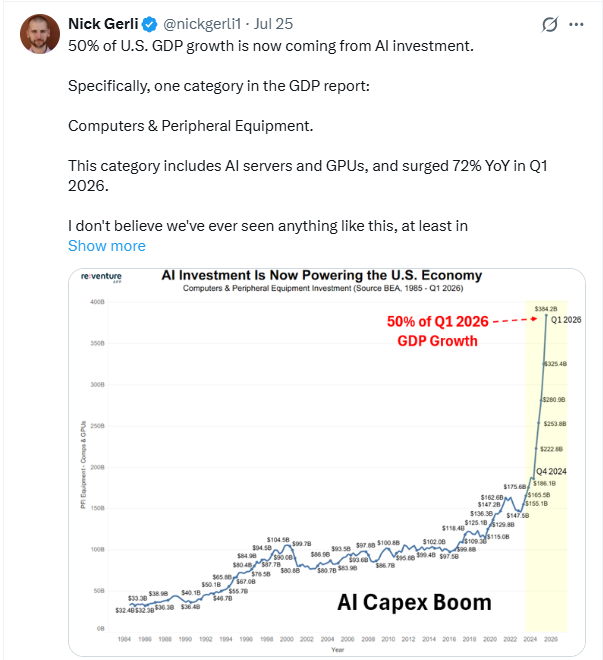

4. 50% of U.S. GDP is Now Coming From AI

Nick Gerli

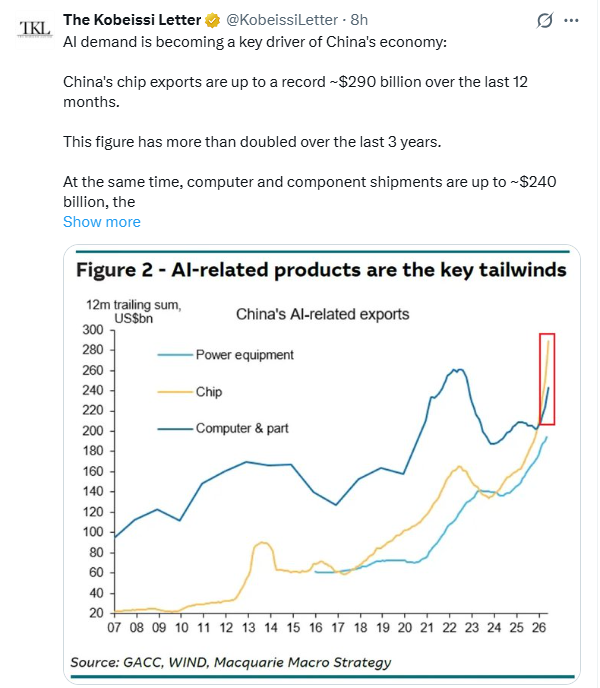

5. China Now Dependent on AI Demand

The Kobeissi Letter

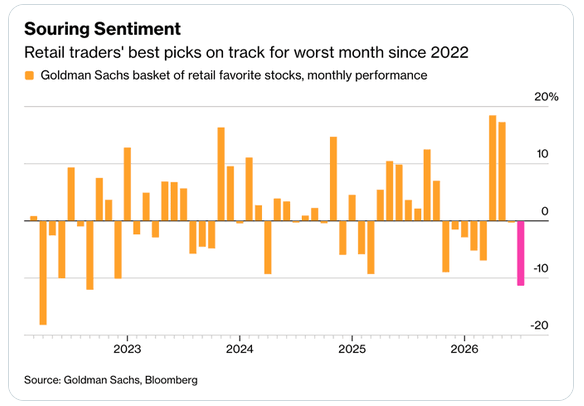

6. Retail Traders Picks Having Bad Month

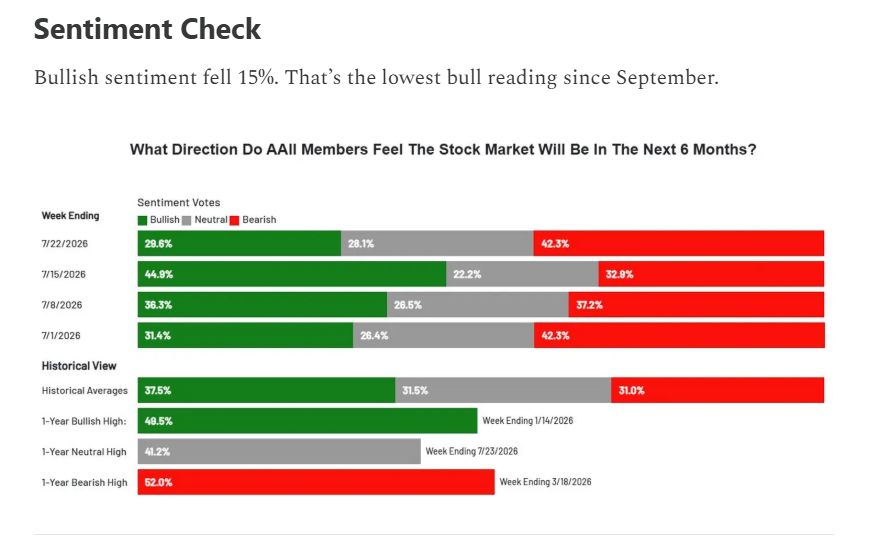

7. Investor Sentiment Falls to Low Bull Reading

Spilled Coffee

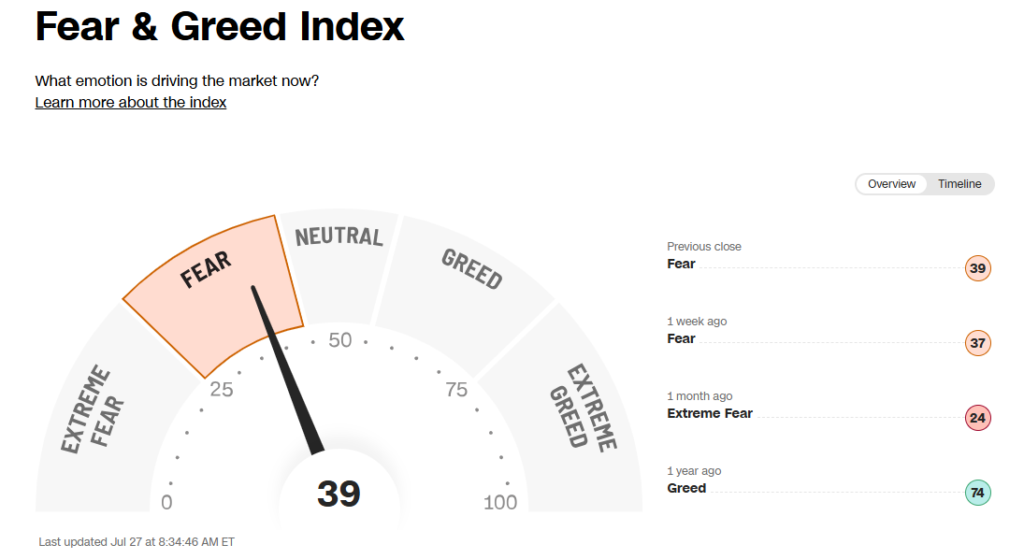

8. CNN Fear and Greed Index

CNN

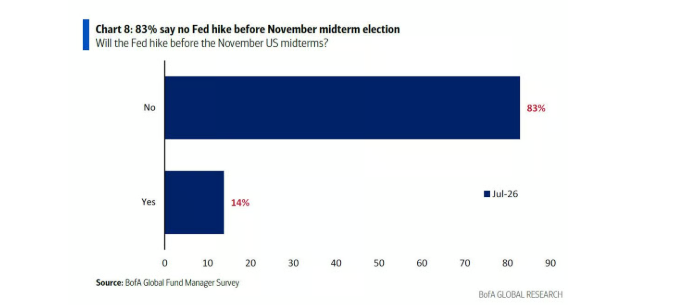

9. Professional Investors in B of A Poll….83% Say No Hikes Before Mid-Terms

10. Perseverance in Life

Personal Perspective: Moving forward in the face of crushing obstacles-Psychology Today Greg O’Brien

Key points

Perseverance often means steady faithfulness, not dramatic acts of courage.

Forward motion—no matter how slow—is vital when facing crushing obstacles.

Studies show perseverance and optimism can help reduce anxiety, depression, and panic.

“If you can’t fly then run, if you can’t run then walk, if you can’t walk then crawl, but whatever you do, you have to keep moving forward.” — Martin Luther King, 1960

I’ve been crawling a lot of late.

I’m not alone in this. Life, at times, offers all of us a haversack of trials—crushing burdens in the moment and beyond.

And we think of giving up.

I’m not saying my challenges are any tougher than others, but just sayin’: in my case, fighting off advancing and bruising Alzheimer’s, cancer, black hole depression, and the death of a son in 2022. No parent should ever have to bury a child.

Some days, the urge just to give up is overwhelming, as the body feels frozen in the moment and the demons are snapping. But I’m trying not to take the bait, and think often of others struggling.

I’m encouraged by Albert Einstein, who said: “You never fail until you stop trying.”

As an aging jock, 76 now, I don’t want to stop trying. So, I’m fighting forward, but can’t say it’s easy in any way.

We all find discernment in many ways. I was raised Irish Catholic, both mother and father with deep Irish roots (47 of 48 branches of our family tree from Erie). I’m now a bit more evangelical, though I haven’t forgotten my roots.

I’m not preaching, just trying to connect; we all come from different places.

I so respect that…

I recently saw the blockbuster summer movie The Odyssey—Director Chris Nolan’s account of the ancient epic about the hero Odysseus trying to return home to his wife and son after serving in the Trojan War and the interminable string of hurdles in his path. Bloodied but unbowed, as William Henley writes in his epic poem “Invictus,” Odysseus never gave up, and through remarkable perseverance, he finally makes it home.

Doug Scalise, my pastor on Outer Cape Cod, emphasized the drive of Odysseus in his Sunday sermon to underscore the faith needed to persevere in life. “There’s something deeply admirable about refusing to quit,” Scalise said. “Sometimes we imagine perseverance as dramatic acts of courage. Occasionally it is. More often it looks like quiet faithfulness over a lifetime.”

Added Scalise, “Have you ever had a week where every day brings another problem, another disappointment, another phone call telling you something you didn’t want to hear?” In a reference to the New Testament Book of Hebrews, he says: “Faith in everything requires perseverance.”

As a wholly imperfect person, I’m trying to find my way out of a valley of depression without wavering. Scalise once reinforced to me that one can’t helicopter out of such a serpentine valley; you have to walk it out.

We often find perseverance in different ways, though forward motion is forward motion.

Experts say perseverance is the confluence of passion and lasting stamina and is more critical in life than talent or intelligence.

The American Psychological Association notes: “People who don’t give up on their goals (or who get better over time at not giving up on their goals) and who have a positive outlook appear to have less anxiety and depression and fewer panic attacks, according to a study of thousands of Americans over the course of 18 years.”

The study, published by the American Psychological Association in the Journal of Abnormal Psychology, says: “Perseverance cultivates a sense of purposefulness that can create resilience against, or decrease, current levels of major depressive disorder, generalized anxiety disorder and panic disorder.”

Lead author of the study, Nur Hani Zainal, M.S., from Pennsylvania State University, notes: “Looking on the bright side of unfortunate events has the same effect because people feel that life is meaningful, understandable and manageable…Our findings suggest that people can improve their mental health by raising or maintaining high levels of tenacity, resilience and optimism.”

No one said it would be easy…Something to be said for baby steps.

As Rev. King once observed, “You don’t have to see the whole staircase, just take the first step.”

Had Odysseus not persevered, had he given up, symbolically he’d still be in the Trojan Horse.

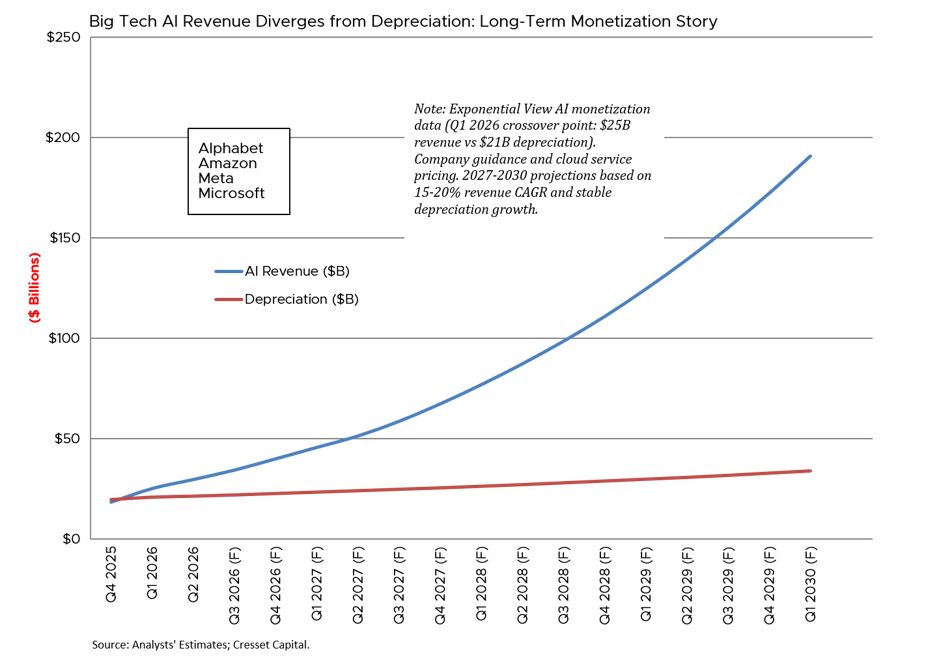

Jack Ablin Cresset-There are, however, early signs that the economics may be turning in the industry’s favor. Data from research firms tracking AI adoption found that global AI sales from hyperscalers and neo-cloud providers reached approximately $25 billion in the first quarter of 2026, surpassing the $21 billion in estimated depreciation tied to their data center investments. That crossover point, where new AI revenue exceeds the depreciation burden of the assets built to generate it, represents a meaningful inflection. It does not mean the return on the entire invested capital base is positive, nor does it resolve questions about competitive saturation or technology obsolescence. But it does suggest that the spending cycle may be approaching economic sustainability.

Cresset

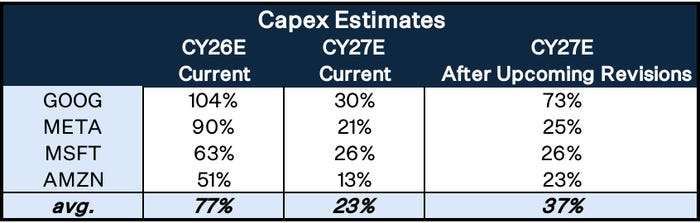

2. A veteran investor says this is the most important AI capex number that markets should watch-BI

Big Tech earnings are here, and the AI capex discussion is set to be the main event for investors. Rather than focusing on what the current quarter—or even the rest of 2026—may hold, tech veteran Gene Munster says investors should be looking further out.

With the AI trade looking “tired,” the investor says that Q2 earnings are the only thing that can generate fresh momentum. Munster, a longtime tech analyst and now managing partner at Deepwater Asset Management, says he’ll be focused most on what hyperscalers are planning for 2027.

“Within the hyperscaler capex conversation, the key metric is next year’s growth,” Munster wrote. “As it stands, the Street is looking for 23% growth in CY27. That said, whisper expectations have moved higher following Google’s $85B and Amazon’s $25B capital raises, which will be spent predominantly late this year and into next year.”

Munster charted the four major hyperscalers’ projected capex estimates for the coming year, and predicts that spending likely won’t cool as much as Wall Street anticipates, leaving a large part of the bull thesis intact.

An earnings chart provided by Munster in his analysis on his web page. GeneMunster.com

Munster noted that much of his analysis centers on the themes of AI capex spending and cloud computing in Q2 tech earnings, which he described as equally important for investors. But while he made it clear that he sees Microsoft as the weakest link in the hyperscaler chain, even its 20% year-to-date decline isn’t enough to derail the AI infrastructure boom.

“The biggest narrative risk in the capex conversation is Microsoft, where I believe management will guide investors to an unchanged 26% growth rate for next year,” Munster noted. “If three of the four hyperscalers raise their outlook, I believe the AI infrastructure narrative will remain intact.”

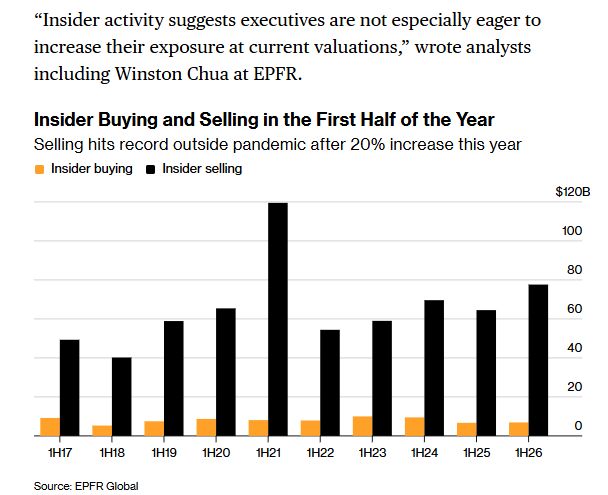

US Corporate Insiders Are Selling Stocks at a Near Record Pace By Michael Msika US executives are selling shares at the second-fastest pace in more than 20 years, a classic red flag to some investors because it suggests people with the most corporate knowledge are wary about markets.

Most of what people believe about aging was formed decades ago, when the science was thinner and the assumptions were darker. The working model—that physical and cognitive decline are inevitable, that the goal is simply to slow the slide—is being replaced by something more accurate and more demanding.

This year’s research is specific in a way that earlier longevity science wasn’t. Not “exercise more” but exactly how many minutes. Not “stay social” but a precise mortality comparison that changes how seriously you should take it. Not “eat enough protein” but the number that’s almost certainly higher than what you’re currently targeting. Five findings from 2026 that are worth updating your operating assumptions around.

1. Decline Is Not the Default—But Your Mindset Makes It One

The starting premise most people bring to aging is wrong. A Yale School of Public Health studypublished in 2026 tracked nearly 4,000 adults ages 19 to 94 over three years and found that 45% of adults 65 and older improved in at least one area—roughly 32% improved cognitively and 28% improved physically. Led by researcher Becca R. Levy and published in the peer-reviewed journal Geriatrics, the study found something more actionable: People who held more positive attitudes about their own aging were significantly more likely to show these gains.

That’s not a motivational footnote. It’s a mechanism. The way you think about what’s coming shapes the biological and behavioral choices that determine whether it arrives. If you’ve already written off your 70s as a period of managed decline, you are actively contributing to that outcome. The practical move here is to audit the assumptions you’re carrying about your own future health because the data increasingly suggests they are the most important variable you can control.

2. The Exact Amount of Strength Training That Pays Off

For years, the advice has been vague: lift weights, build muscle, do resistance training. A June 2026 study in the British Journal of Sports Medicine finally puts a number on it. Researchers tracked 147,374 people over 30 years and found that 90 to 120 minutes of strength training per week was the longevity sweet spot, linked to a 13% lower risk of death from any cause, a 19% lower risk of death from cardiovascular disease and a 27% lower risk of death from neurological disease. Critically, they found no additional mortality benefit above 120 minutes per week.

That’s three sets of data points that change the conversation. First, the specific window (90-120 minutes) gives you an actual target instead of a vague directive. Second, the neurological protection finding—27% lower risk—is striking and underreported; most discussions of strength training focus on cardiovascular and metabolic benefits. Third, the ceiling matters: Doing more doesn’t help. Two focused sessions of 45 to 60 minutes weekly is not a beginner’s approach. It’s the evidence-backed optimum. If you’re already doing more, you may be spending time that could go elsewhere.

3. Cardio & Strength Together Are a Different Category

The same 30-year study found that combining strength training with aerobic exercise produces benefits that neither generates alone. Participants who accumulated high levels of both—30 to 44 MET hours of aerobic activity weekly alongside 60 to 119 minutes of strength training—saw a45% lower risk of death compared with those doing minimal amounts of either. At the highest aerobic volumes, mortality risk dropped 53% to 58% regardless of the amount of strength training.

The practical interpretation isn’t “do more.” It’s that aerobic and strength training operate on different biological pathways and stacking them produces compounding protection rather than redundant protection. If you’ve been treating your weekly workout as a choice between cardio and strength, the data argues for both—not as a performance goal, but as a longevity strategy. A structured week that includes three cardio sessions and two strength sessions, each around 45 minutes, clears both thresholds.

4. Social Isolation Has a Mortality Number, & It’s Alarming

Stanford Medicine’s longevity research for people in their 40s and 50s cites a finding that deserves more attention than it typically gets. A study analyzing data from 2.3 million adults,published in Nature, found that social isolation increases the risk of premature death by about 30%, a mortality risk comparable to smoking 15 cigarettes per day.

Most high-achievers in their 40s and 50s treat social connection as a discretionary item that gets trimmed when schedules are full. The data says this is a serious miscalculation. Stanford’s Abby King, Ph.D., who has spent decades researching health behaviors across the lifespan, frames this explicitly: “Social connection is really important for healthy aging—for your brain and for your emotional health. Finding ways to stay engaged with others, whether through community groups, volunteer work or simply maintaining close friendships, is one of the most protective things you can do for your long-term health.”

The midlife years—when careers and family demands peak—are precisely when social connection tends to contract. Building structural habits around it now (a standing dinner, a recurring commitment, a consistent community) isn’t a lifestyle choice. Based on the mortality data, it’s closer to a health intervention.

5. Your Protein Target Is Probably Too Low

The standard dietary recommendation for protein is 0.8 grams per kilogram of body weight per day. Stanford Medicine’s experts say that number is wrong for adults over 40, and the gap matters. Starting around age 40, you lose approximately 1% of muscle mass per year; the rate accelerates through your 50s. To counter that loss, Stanford’s research puts the effective target for adults over 40 at 1.0 to 1.2 grams of protein per kilogram of body weight daily, 25% to 50% higher than the standard recommendation.

For a 165-pound person, that means roughly 75 to 90 grams of protein per day, distributed across three meals of 20 to 30 grams each plus a 15- to 20-gram snack. Most people eating a standard Western diet fall significantly short of this, particularly at breakfast. The practical adjustment isn’t complicated—it’s adding a structured protein source to every meal rather than treating protein as incidental—but it requires knowing the actual target, which most people don’t.

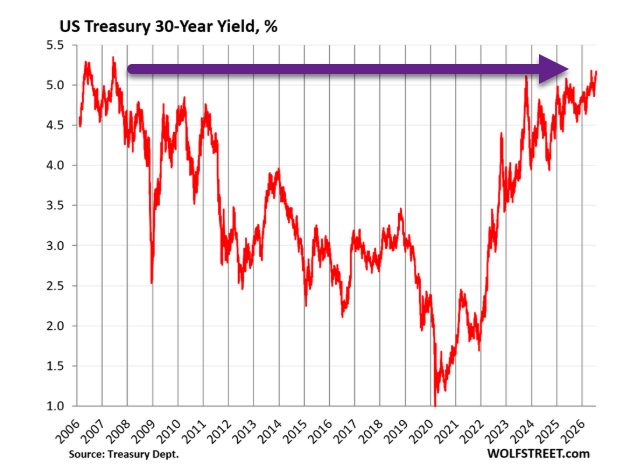

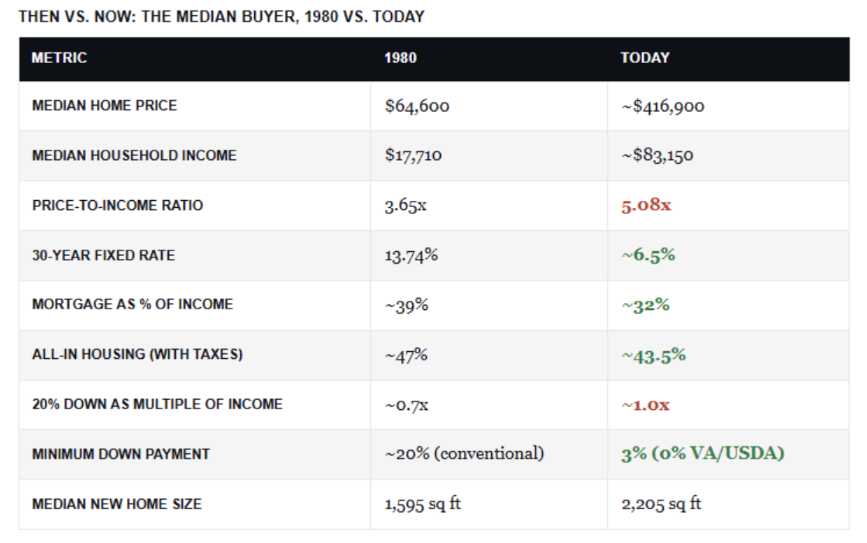

Here’s the part the narrative skips. The Boomer who bought in 1980 financed at a 30-year fixed rate of 13.74%, watched it climb past 18% by October 1981, and had no way to know rates would ever come back down, which made every payment feel like a life sentence.5 Think about that. For a median home price of $64,600 with 20% down, that household sent roughly 39% of its income to the mortgage before property taxes.6 Add the taxes, and the typical 1980 family spent close to 47% of their income on housing.

Today’s buyer, financing about $417,000 near 6.5%, spends closer to 32% on the mortgage and about 43% all in.6,14 Two independent analyses ran this exact math and landed in the same place. On the payment that matters, 1980 was as hard as, or harder than, 2026. So home affordability today is mostly a payment story, and the payment math favors the present. Notice what the work did. It isn’t the price of the home, it’s the rate.

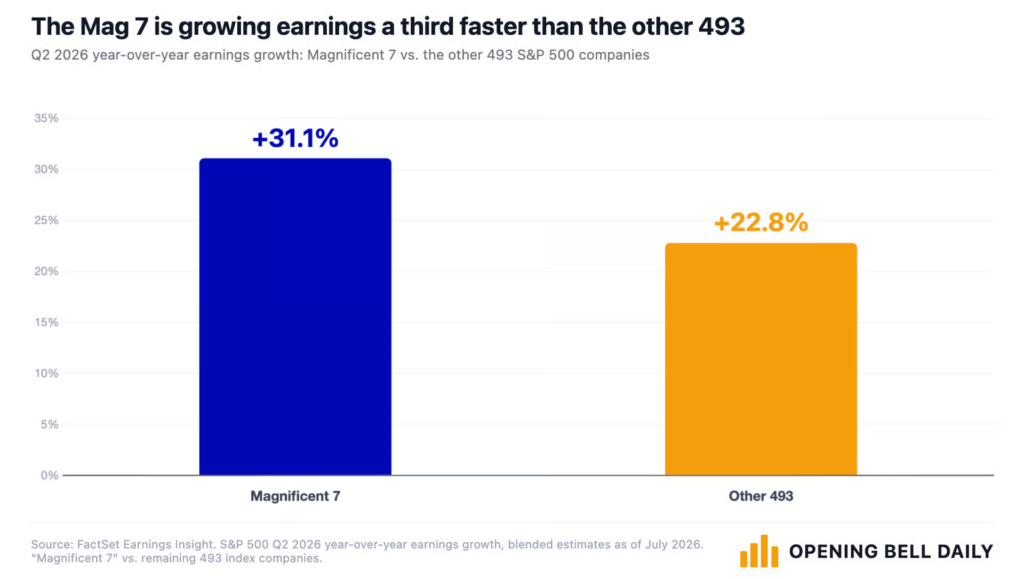

According to FactSet estimates, the S&P 493 is expected to grow earnings at 22.8% compared to a year ago.

That in itself would mark the strongest rate since the end of 2021, but even that won’t be enough to keep up with the household mega-cap technology names.

Opening Bell Daily

2. But Off Balance Sheet AI Debt Hits $1.65 Trillion

Semafor

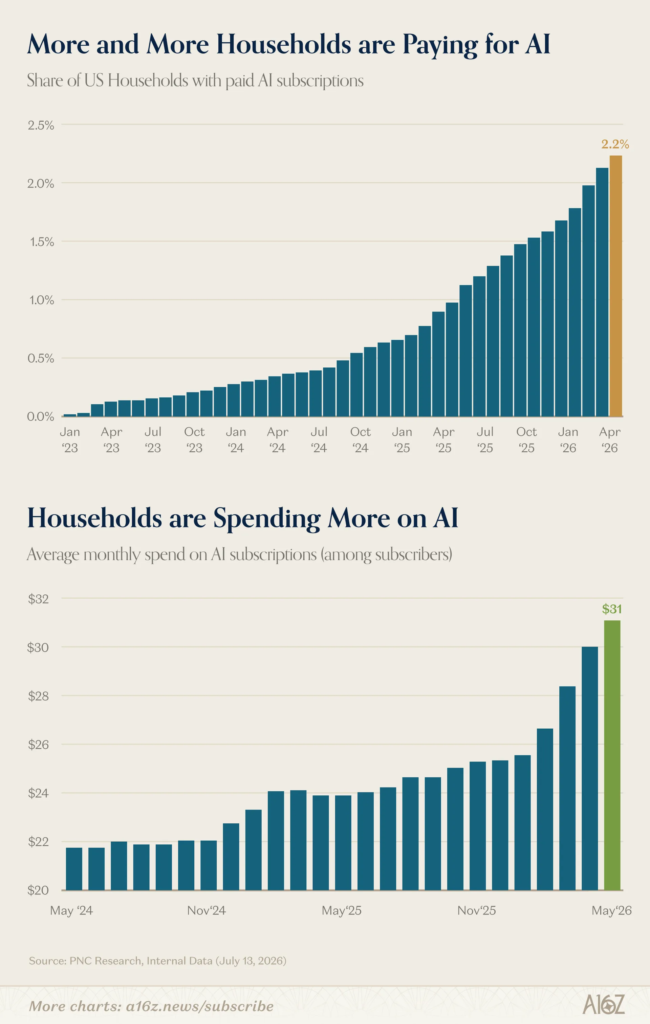

3. Updated Household Spending on AI

Household AI spending. “Both the share of households paying for AI, and their average monthly spend, continue to climb-monthly spend has increased even more steeply, rising ~25% since the beginning of the year.”

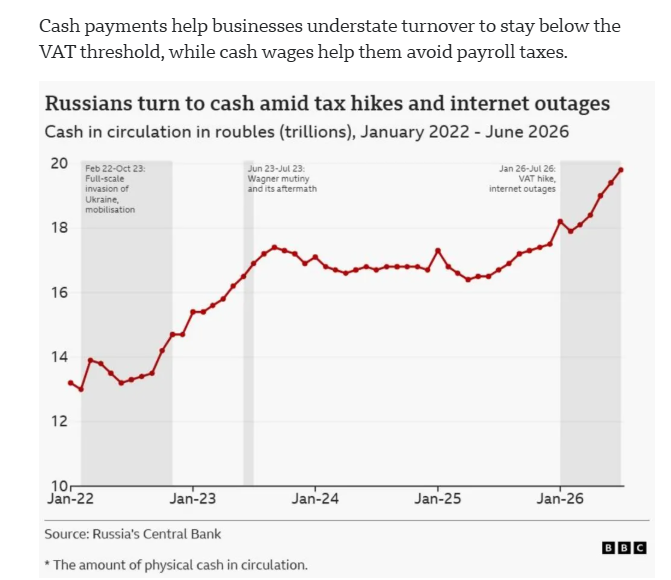

8. Russians Increasing Cash Usage that Drains Tax Money Going to War

BBC

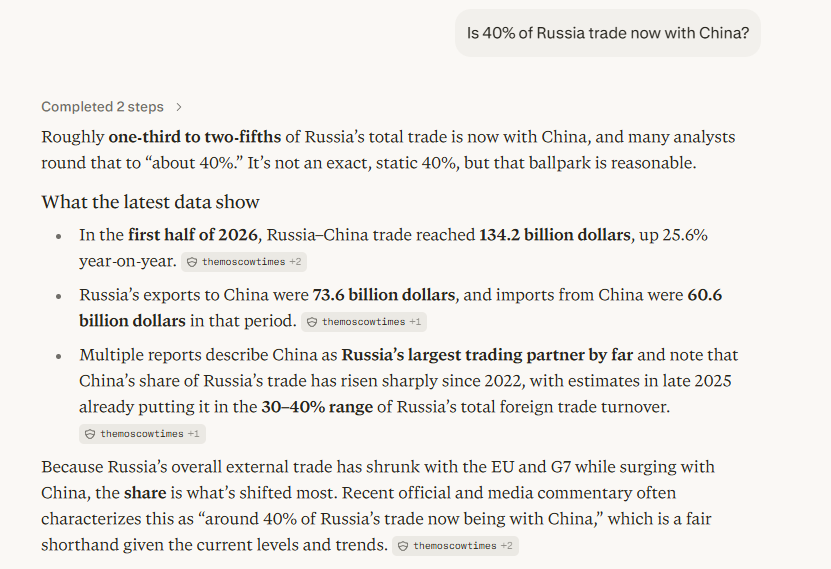

9. 40% of Russian Trade Now with China

Perplexity

10. This Is How To Live A Good Life: 5 Secrets From Ancient Wisdom

Here’s how to live a good life…

You Are What You Repeatedly Do: Character is a practice, not a personality trait. Every action is a rep.

If You’re Still Fighting Temptation, You Haven’t Arrived: You can’t build a good life out of stop signs. Instead of resisting temptation, learn to love better things.

Happiness Is an Activity, Not a Mood: Ask, “Am I making proper use of myself?”

Study Manipulation Even If You Hate Manipulators: Nobody thinks oncologists are evil because they study cancer. And they wouldn’t be able to fight cancer if they didn’t understand it.

Humans Cannot Flourish Alone: Modern culture asks, “What can this relationship do for me?” An Aristotelian asks, “What kind of person does this relationship help me become?”