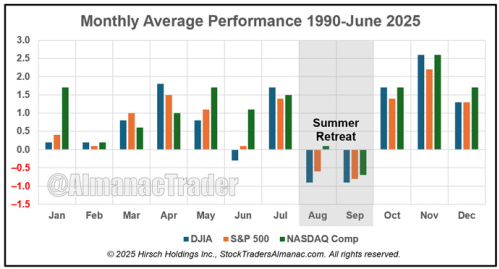

Dave Lutz Jones Trading Over the last 35 years, August and September are the worst performing months of the year. Average performance has been mixed in August with DJIA and S&P 500 recording losses of 0.9% and 0.6% respectively while NASDAQ has eked out a meager 0.1% gain. September has been red across the board for DJIA, S&P 500, and NASDAQ – “Our July seasonal pattern chart shows this August-September market retreat actually tends to begin around mid-July” noted AlmanacTrader

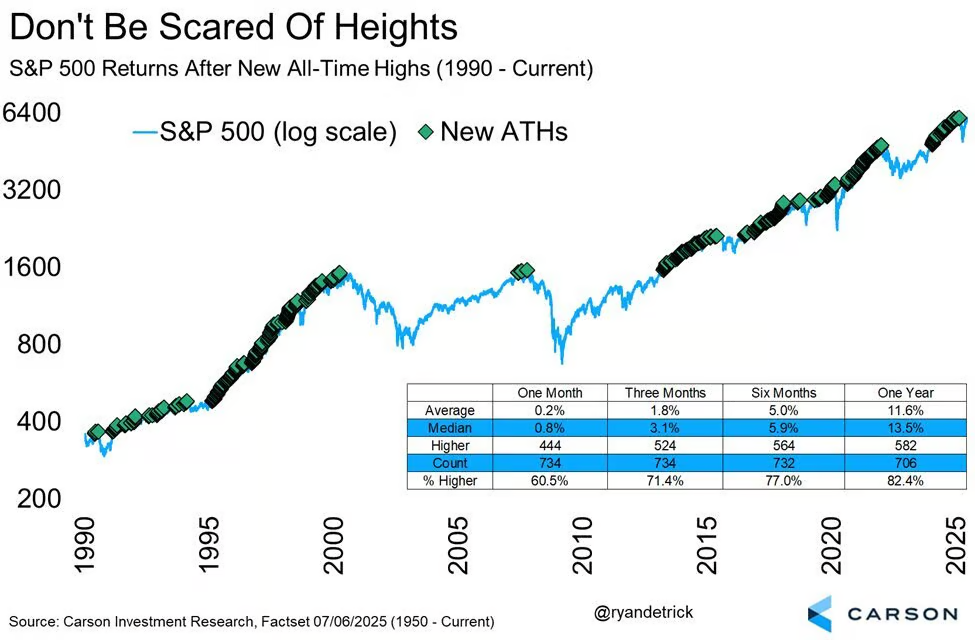

2. All-Time Highs Not Bearish

SPX vs. ATHs. “Since 1990, the S&P 500 was higher a year after an all-time high 82.4% of the time and up a median return of a very impressive 13.5%.”

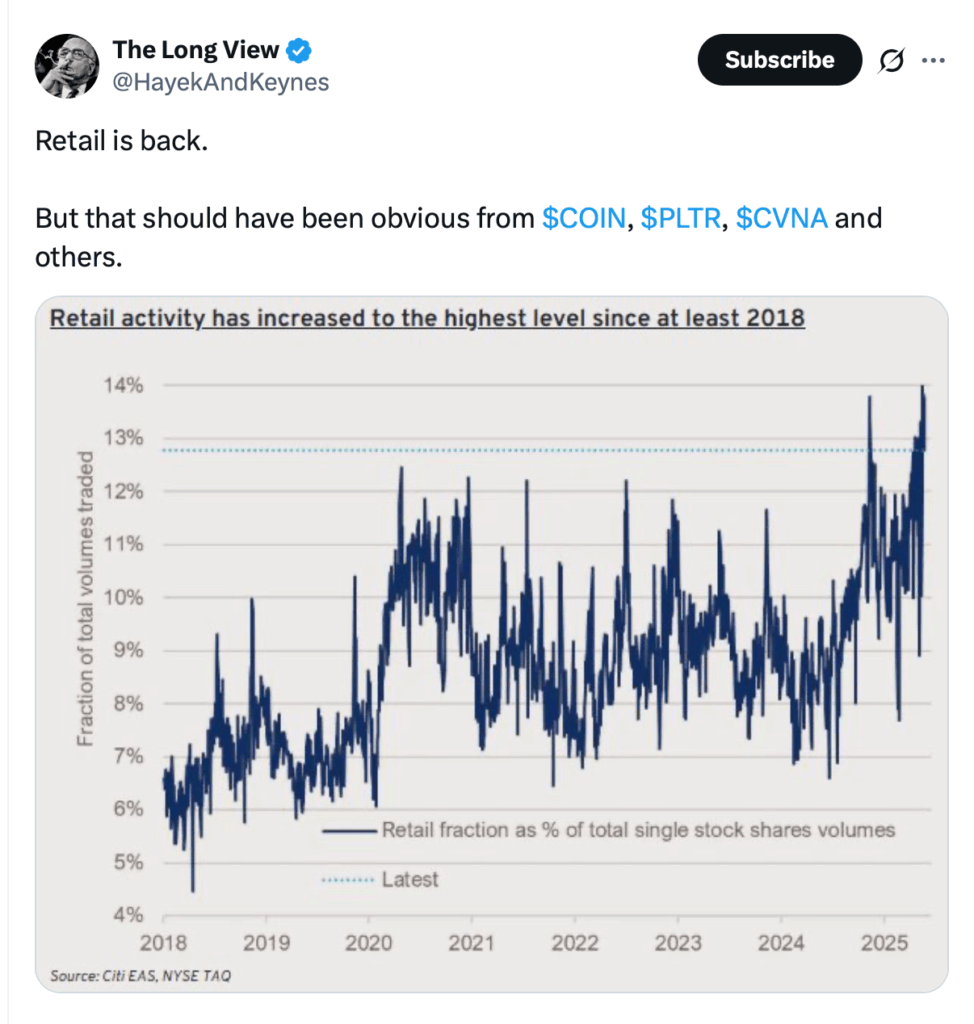

BofA noted, The cumulative gap between institutional selling and retail buying in the YTD is the largest of any comparable YTD period in our data history since ‘08 and the 2nd largest (after 2017) when normalized by market cap

For these lucky people, the experience of the Vanderbilts and their contemporaries offers a cautionary tale. At the turn of the 20th century, America’s census recorded about 4,000 millionaires, note Victor Haghani and James White, two wealth managers, in their book, The Missing Billionaires. Suppose a quarter of them had at least $5m (the richest had hundreds) and had invested it in America’s stockmarket. Had they then procreated at the average rate, paid their taxes and spent 2% of their capital each year, their descendants today would include nearly 16,000 old-money billionaires. In reality, it is a struggle to find a single one who traces their fortune back to the first Gilded Age.

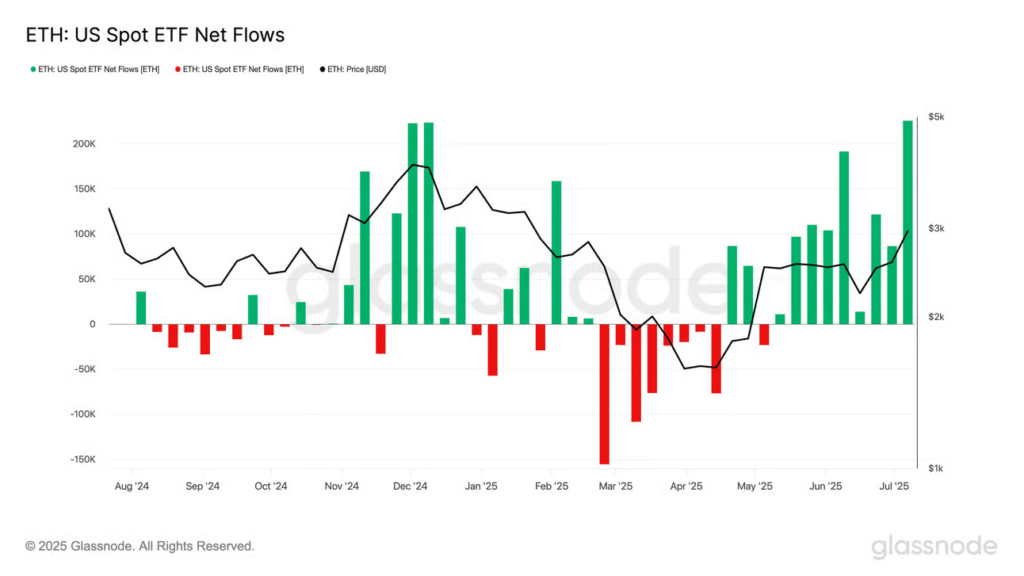

ETH ETF flows. “US spot Ethereum ETFs recorded their largest weekly net inflows since launch – 225,857 ETH – extending a multi-week trend of growing institutional demand.”

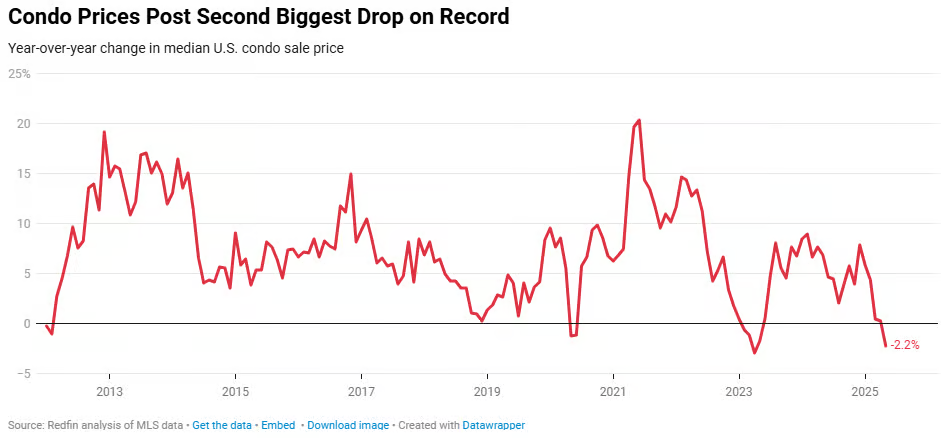

Condo prices just posted their 2nd‑biggest YoY drop on record: –2.2% in May.

Why the slump?

80% more condo sellers than buyers

Surging HOA fees, insurance costs & special assessments

Financing hurdles

10. On Track for Lowest Murder Rate in History.

The US is on course for the lowest murder rate in its history this year. After years of decline, crime spiked in 2020 and 2021, with murders reaching their highest since the mid-1990s. But they have since dropped precipitously, and continue to do so: The Real-Time Crime Index recorded 2,095 homicides in January to April, the most recent data available, down 20% from the same period last year. The data analyst Jeff Asher wrote in May that the figures were set to be lower than 2014’s murder rate record of 4.45 per 100,000, and that increased investment in local communities was likely a factor. Violent and property crime are both also close to record low levels, Asher wrote.

Vanguard owns more than 20 million shares, nearly 8%, of all of Strategy’s (MSTR) outstanding Class A common stock, and likely surpassed Capital Group Cos. for the no. 1 spot sometime in the fourth quarter, according to data compiled by Bloomberg based on regulatory filings. The dozens of Vanguard mutual funds and ETFs that hold the stakes track everything from small- and mid-cap benchmarks to momentum, value and growth gauges, among o “God has a sense of humor,” said Eric Balchunas, senior ETF analyst at Bloomberg Intelligence and author of The Bogle Effect. “Vanguard chose this life. When you have an index fund, you have to own all the stocks, for better or worse, and that includes stocks that you may not like or approve of personally.”thers.

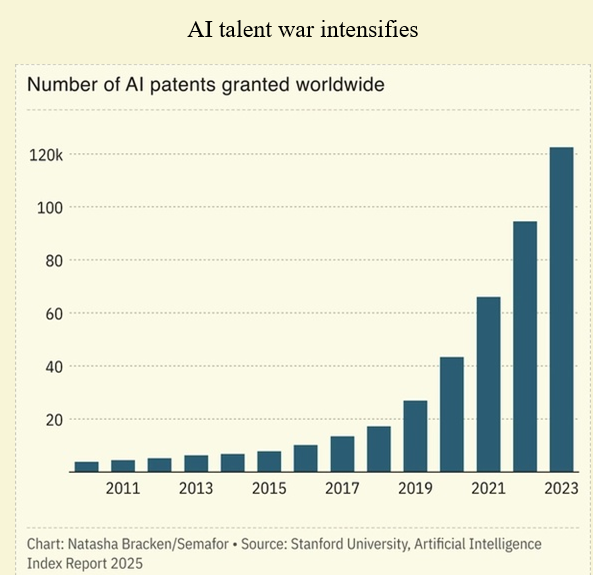

Google spent $2.4 billion to hire the leaders of an artificial intelligence programming company, the latest big-ticket move in an intensifying AI talent war. Windsurf’s CEO and co-founder will join Google DeepMind along with several top employees. Tech giants buying stakes in rivals attracts the attention of antitrust regulators, but hiring decisions do not, The New York Times reported; Google’s huge outlay is comparable to a soccer team paying a transfer fee to acquire a top player’s contract. Meta, too, has been on a hiring spree recently, sometimes offering compensation packages of up to $100 million for top talent, as it tries to make up ground in the AI race.

$TRUMP was listed in an average of 4 days by exchanges, vs 129 days for other big coins

Three crypto exchanges say they moved to list $TRUMP fast because of customer demand

Exchanges say no corners were cut in vetting the coin for listing

White House says Trump coin poses ‘no conflicts of interest’

NEW YORK, July 14 (Reuters) – Crypto exchange Coinbase assures users on its website that it puts any new digital coin through “rigorous” vetting before allowing it to trade. It’s an at-times lengthy process meant to protect customers by examining the people connected to the project and the risk of market manipulation or other scams.

With President Donald Trump’s crypto token, $TRUMP, Coinbase made up its mind in just one day.

Make sense of the latest ESG trends affecting companies and governments with the Reuters Sustainable Switch newsletter. Sign up here.

The $TRUMP token, which launched three days before his inauguration in January, is a meme coin. Based on cultural fads or celebrities, these coins have no intrinsic value and – past experience has shown – are prone to large price swings that can leave investors with losses.

A Reuters analysis of crypto market data and industry announcements found that, compared to other recent large meme coins, the biggest crypto exchanges took Trump’s to market with unusual speed, despite stating they vet risky coins thoroughly to protect small investors.

Some also approved the listing in spite of the high share of coins concentrated in the hands of Trump and his partners, which would normally represent a red flag because of the risk that dumping of tokens by insiders could collapse the price and hurt other investors, some executives said.

After reaching an all-time high of $75.35 on April 19, just two days after its launch, $TRUMP crashed to the $7 range by early April, leaving many holders nursing losses. It was trading around $9.55 Thursday.

Afriend passed along a recent blog post from Drive by DraftKings, a venture capital firm whose founding partners include (wait for it) DraftKingsDKNG $43.85 (1.91%), titled, “The Gen Z Effect: The Behavioral Shift Shaping Gaming, Fandom, and Human Performance.”

Here’s a passage that piqued my interest (emphasis added)

“Gen Z’s approach to gaming is clear. They gravitate toward formats that are fast, emotionally charged, and offer the chance at a meaningful payoff. Traditional, slow-paced gameplay is losing ground to experiences that deliver instant feedback and the possibility of an outsized win.

This is why crash games, meme stocks, and parlay bets have gained so much traction with this generation. These formats share a common formula: low-cost entry, high potential upside, and just enough unpredictability to keep things exciting. A recent Morgan Stanley survey found that 60% of bettors aged 21 to 34 have placed parlays, a rate nearly 30% higher than the overall population. Similarly, around 30% of US stock investors aged 18 to 24 have invested in meme stocks compared to 12% of investors ages 45-54.

It’s not just the payout that attracts Gen Z. It’s the emotional volatility, the rush of possibility, and the shareable nature of “just-missed” or jackpot moments. The appeal is simple: put down a small amount, take a swing, and hope to hit it big. Most of these bets won’t pay off, but the ones that do tend to go viral. Social media elevates these wins, creating a sense of FOMO that draws others in. It becomes a feedback loop of visibility, aspiration, and repeat behavior, which keeps Gen Z highly engaged and emotionally invested in the experience.”

To riff on this conception of a “common formula” between parlays and meme stock punts, which often take place through the options market to access embedded leverage:

Both parlays and short-term options punts are examples of things where you need multiple things to go right to win. In parlays, it’s discrete (usually sports-related) outcomes; in options, you need to get the direction and magnitude right by a certain point in time.

This is why I love the use of options as a storytelling device: they are always and everywhere a greed, fear, or complacency play built around a specific date by which something needs to either happen or not happen. There’s a subject, verb, and time.

“I think one thing that’s very clear about Gen Z is that they’ve repeatedly been told nobody is coming to save you,” Emily Sundberg, author of the Feed Me Substack, said at a live taping of Bloomberg’s Odd Lots podcast. “You hear this sense of ‘get the bag while the world is still here for you to make some money out of it.’”

Kind of ironic that the generation that thinks nothing in the world is going right for them seeks out betting and trading structures that require multiple things to go right to profit.

Is this really a Gen Z thing, though?

One can quibble about some of this line of thought. And I will. The 2021 meme stock boom was occurring when the average member of Gen Z was just in their early high school years. I doubt many of them were part of the Apes Together Strong crew.

The “YOLO” catchphrase that serves as a shorthand for the kind of “eff it, we ball” approach to life was popularized by a somewhat seasoned millennial.

And to dodge any accusations of millennial-boosting, manias have existed well before we were a twinkle in our boomer parents’ eyes and will continue to persist long after we’re ashes. To this author, a person’s willingness to dive headfirst into booms is much more defined by their stage of life rather than the generation they belong to. Oh, to be young…

Gen Z likes structures with huge payoffs that often end in busts? How convenient for the VC firm, which concludes that the shifts in Gen Z behavior “reinforce why we focus where we do — on the edge of behavioral change, where category defining companies are born,” highlighting portfolio companies Triumph and Picklebet as great examples of firms whose products have been built for this generation.

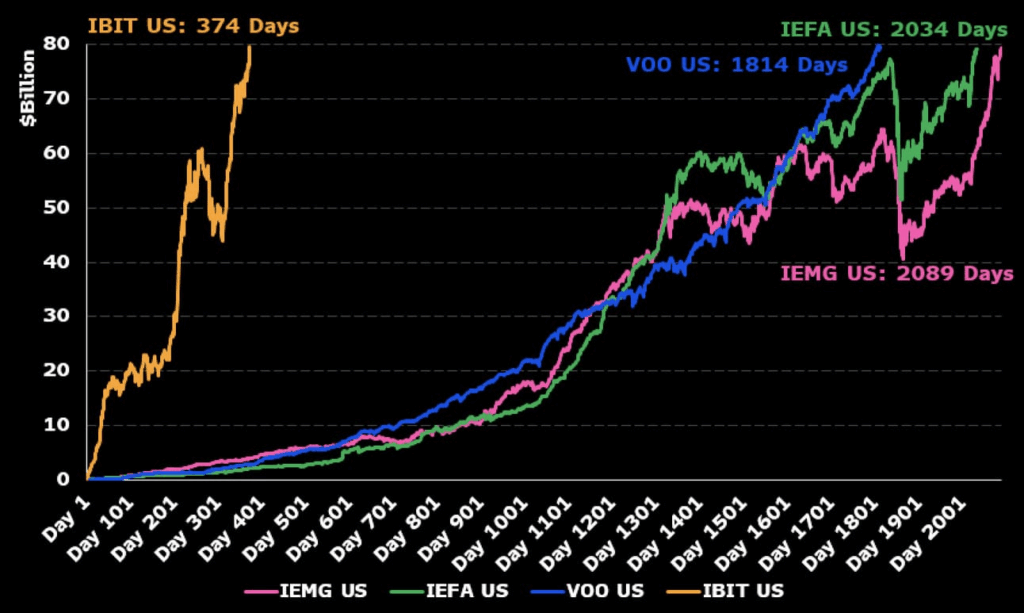

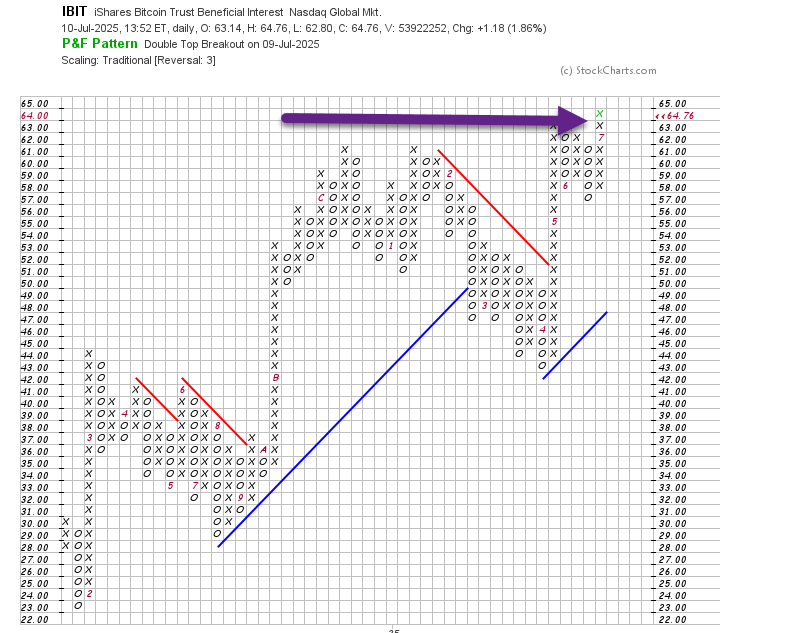

Bitcoin ETF flows. “$IBIT blew through the $80b mark last night, fastest ETF to get there in 374 days, about 5x faster than the previous record, held by $VOO, which did it in 1,814 days. Also at $83b it’s now 21st biggest ETF overall.”

5. SPACS, Reverse Mergers and Digital Assets Joining Up

Bloomberg-For dealmakers who cultivated crypto relationships through the industry’s troubled years — not to mention who hung in during the post-pandemic collapse of the SPAC boom — now is the time to cash in. The appeal of blank-checks is in their relative speed. Unlike IPOs that can take more than six months, a reverse takeover or SPAC deal can be agreed in weeks, according to Paul McCaffery, KBW’s co-head of digital assets.

A rebound in token prices and a more permissive US regulatory environment have emboldened crypto firms, leading to more deals, particularly among SPACs and reverse mergers.

8. US government to invest in rare earths production

Jonathan Josephs–Business reporter, BBC News•jonathanjosephs

Bloomberg/Getty

The US government is to become the biggest shareholder in the country’s only operational rare earths mine.

It is also going to take a series of other steps to underpin the future of the operation in Mountain Pass, California.

Rare earths are essential to huge amounts of modern technology, such as electric cars and wind turbines.

Access to these metals has been at the heart of a US-China trade war, with Beijing controlling about 90% of global processing capacity.

Advertisement

MP Materials, which owns the mine, has entered into an agreement with the US Department of Defense that is designed to reduce America’s dependency on imports of rare earths.

The deal means that for the next 10 years the US government will commit to MP Materials receiving a minimum price of $110 per kg for its neodymium and praseodymium output.

These are two of the most in-demand of the 17 different rare earths for the global economy. They are crucial for making permanent magnets, which are found in everything from smartphones to MRI scanners and electric motors.

The move follows concerns that China has used its near total control of the industry to push prices down and force companies in other countries out of business.

Macro conditions. “The overall equity movement is perceived as occurring in one of the most favorable macro environments, characterized by a depreciating dollar, narrowing credit spreads, subdued inflation, and interest rates remaining below 4.5%.”