Purpose comes from design, not desire—where your gifts, skills, and context align.

Your job isn’t your identity; it only expresses your deeper pattern.

Stress reveals your design. How you act under pressure shows your true strengths.

Design evolves—your gifts grow through practice, reflection, and service.

4 Ways to Discover What You’re Designed to Do

Study your defaults under pressure.

Look beyond your job title.

Experiment, don’t declare.

Refine through service.

When stress rises, notice what you instinctively do. That pattern—your natural mode of problem-solving or connecting—is a clue to your design.

As Viktor Frankl (1959) observed, purpose is not found in what we get from life but in what life expects from us. Your profession may be a vehicle, but your design is the engine.

Treat your design as a prototype. Try new contexts, collaborators, and challenges. Growth, as Dweck (2006) reminds us, is iterative.

The surest test of a gift is its value to others. When your work creates coherence, insight, or uplift in others, you’ve likely found alignment between your design and your purpose.

To ask What am I designed to do? is not to surrender freedom—it is to locate it. It means working with the grain of your nature rather than against it, shaping your life as a craftsman shapes wood: respecting the knots, the curves, the tensile strength that make it beautiful.

The poet Rainer Maria Rilke (1934) once wrote, “Go into yourself and see how deep the place is from which your life flows.” That place—the confluence of gift, growth, and grace—is where design becomes destiny.

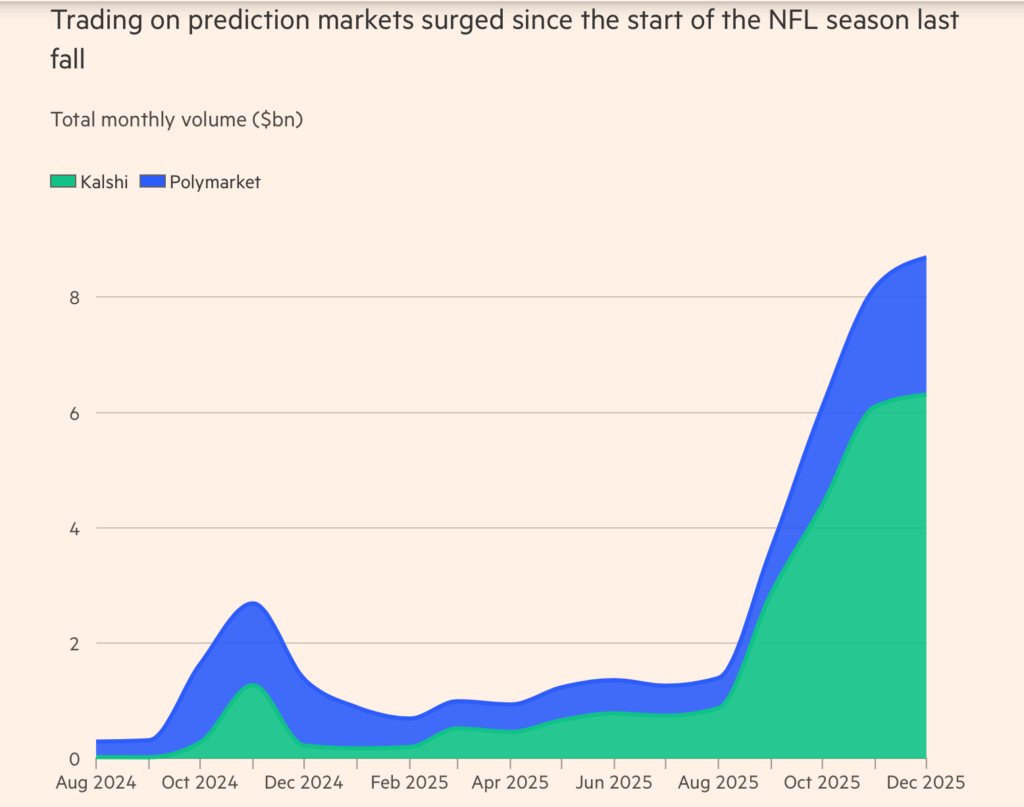

Trading on prediction markets surged since the start of the NFL season last fall

Financial Times

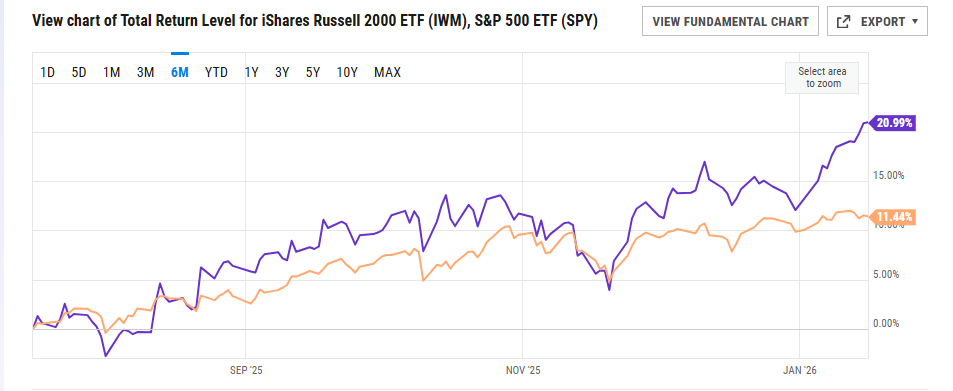

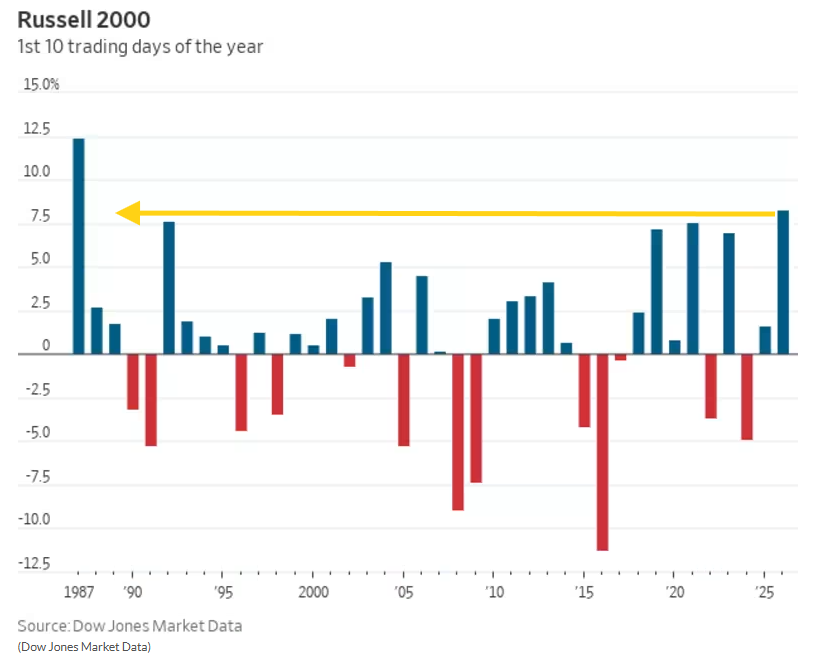

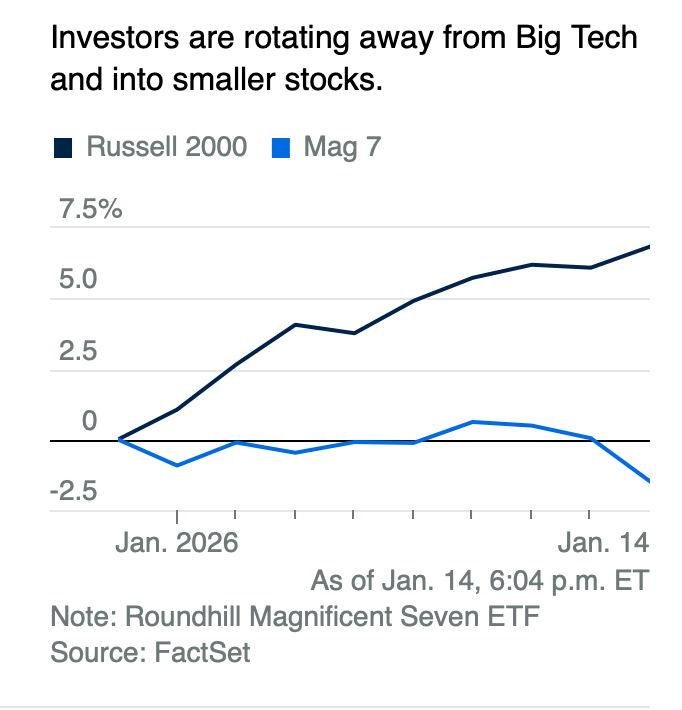

2. Small Cap Stocks on Best 10 Day Start Since 1987

Zach Goldberg Jefferies …The Russell 2000 is up roughly 8.3% so far in January. This puts it on track for its best 10-day start to any year since 1987, according to Dow Jones Market Data. The index has gained 2.4% in this week alone and has outpaced the S&P 500 over the past three months.

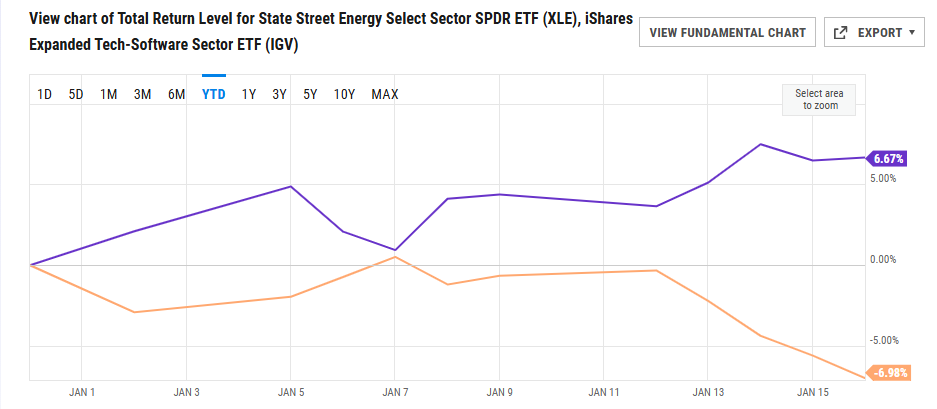

3. Broadening of Market Leadership

Reuters

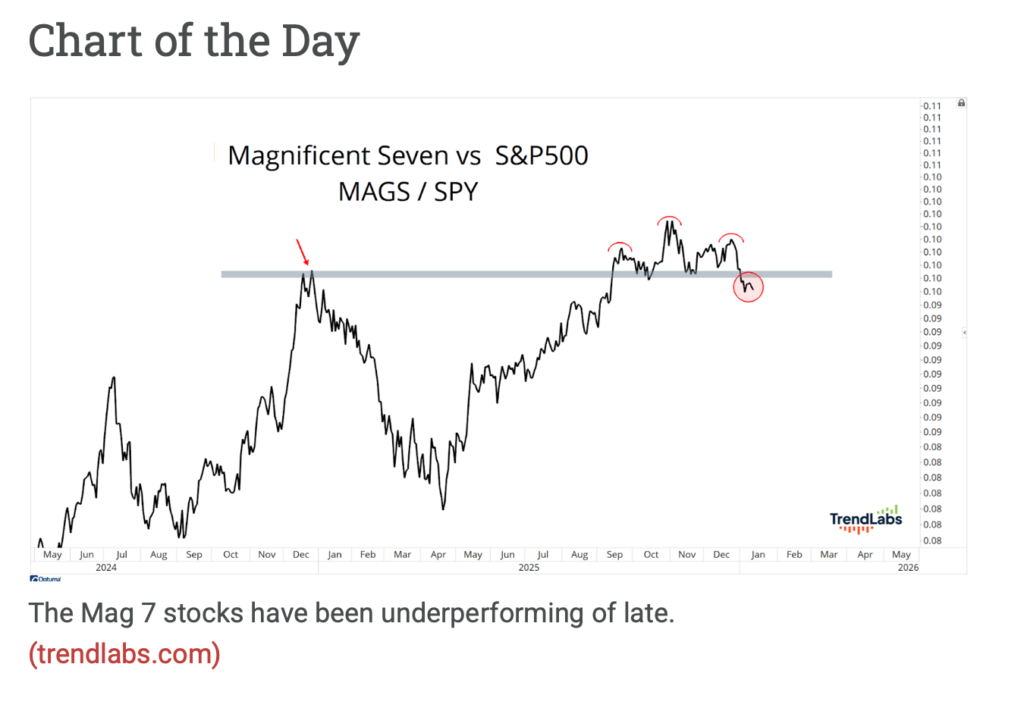

4. Mag 7 Lagging

Abnormal Returns

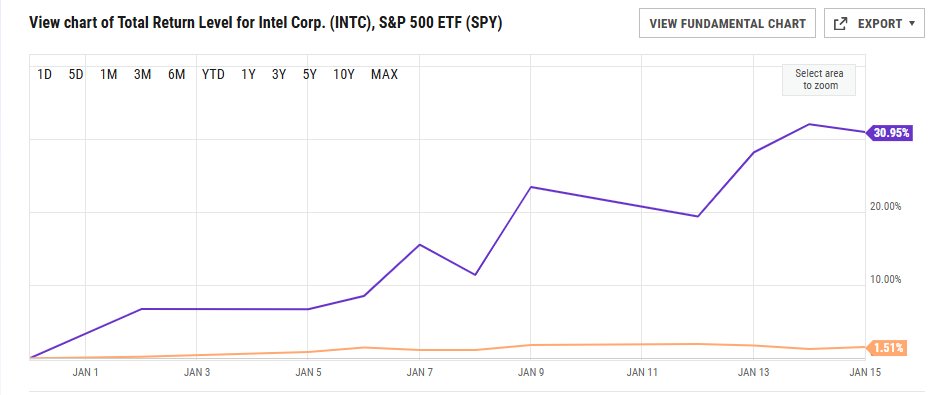

5. Large Money Center Banks

Bespoke Investment Group While large brokerage/investment banking-centric firms like Goldman Sachs (GS) and Morgan Stanley (MS) are seeing modest reactions to earnings, the same can’t be said for the largest money center banks, which reported this week. Bank of America (BAC), Citigroup (C), JPMorgan Chase (JPM), and Wells Fargo (WFC) all traded down at least 3% on their reaction days this week. For most, it was their worst earnings reaction day performance in over a year, and for BAC, it was the worst since October 2020!

Bespoke

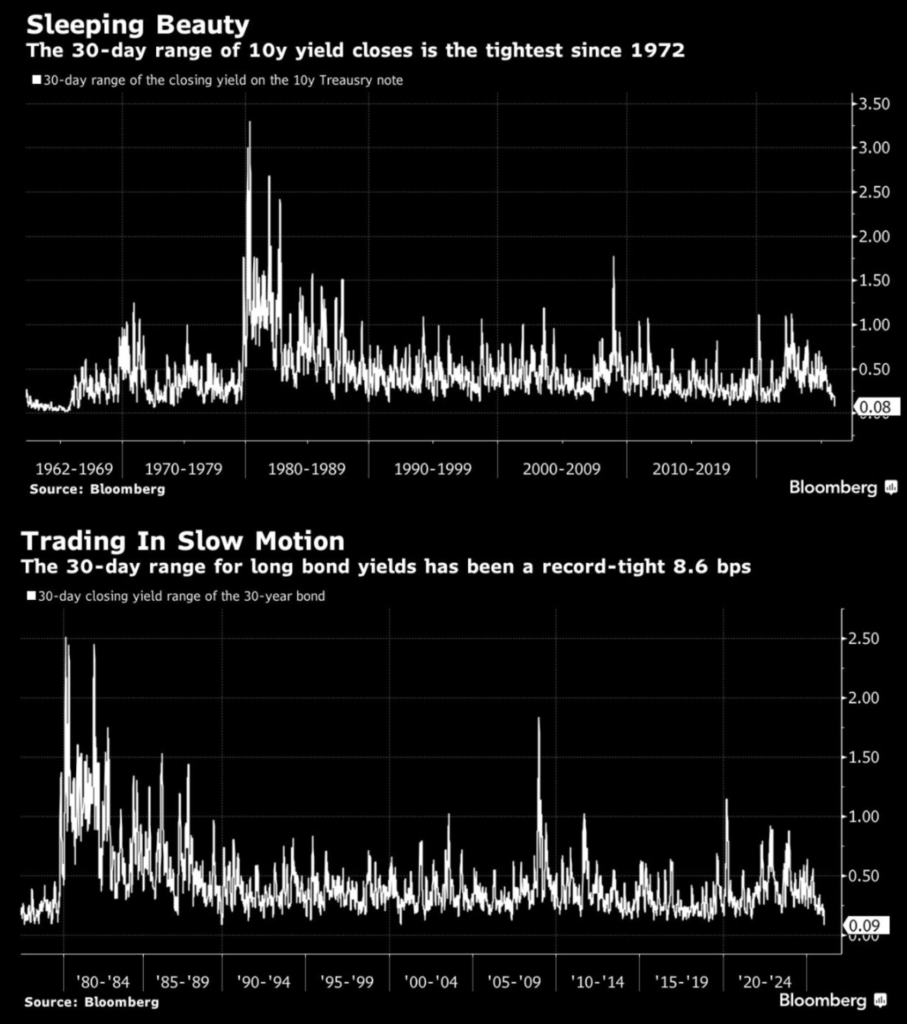

6. Bond Market Calmest Ever

Bond market calm. “The bond market has never been so quiet … the 30-day trading range for the benchmark 10-year US Treasury, which is now the tightest it’s been since the 1970s. Meanwhile, the trading range for the 30-year has reached a record low.”

Bloomberg

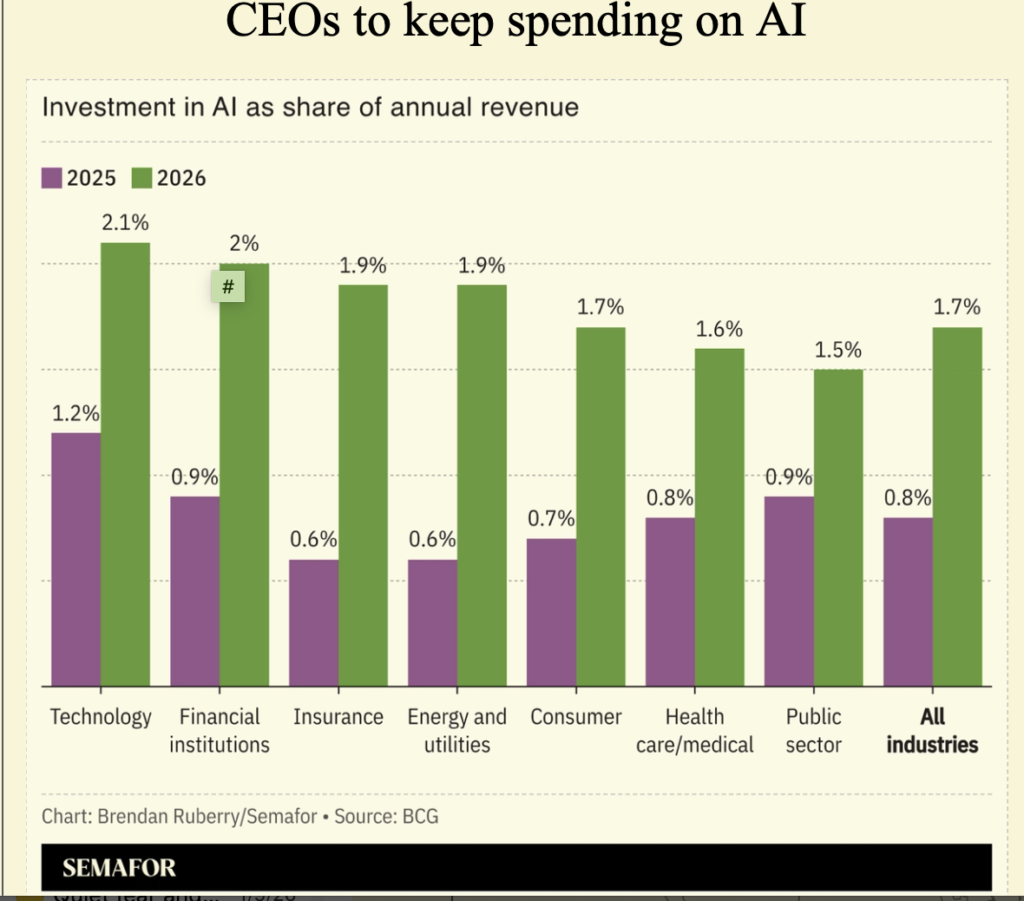

7. CEO’s Keep Spending on AI

Semafor

8. Half of GLP-1 users ditch their injections — and some are turning to other weight-loss methods instead

New research has found that 50% of patients regain the weight they lost if they stop taking Wegovy and Zepbound By

Approximately half of individuals discontinuing GLP-1 medications regain all lost weight within two years, often experiencing the return of associated medical problems.

A study of 77,310 adults in Denmark revealed that 52% of Wegovy users stopped treatment within a year due to cost or gastrointestinal side effects.

New oral GLP-1 options are emerging as potential maintenance treatments.

Millions of Americans have tried GLP-1s, but some people find that the weight-loss drugs have too many side effects, are expensive or just don’t work for them.

Patients also have to deal with changes to their health insurance at the start of a new year, and more employers have withdrawn coverage of the pricey medications. About half of the people who stop taking GLP-1s, like Eli Lilly’s

Wegovy, discover that they gain back all the weight they lost within two years.

“The only way that they work is if you keep taking them,” said Scott Isaacs, an endocrinologist at the Grady Health System in Atlanta. “And when people stop taking them, they have a lot of weight regain, and the medical problems that went away tend to come back.”

Modern life is optimized for comfort, especially while sitting, but not for longevity. We relax on soft couches, work in rigid desk chairs, and spend hours driving or scrolling on our phones. Over time, these habits pull the head forward, round the spine and tighten the hips.

Those patterns quietly erode posture, mobility and the ability to rest with ease, which are all important for aging well. But I always tell my clients that a short, intentional daily stretching routine can help counteract the physical strain of modern life.

Just a few minutes a day can improve posture, calm the nervous system and keep the body resilient for years to come. Here are five stretches I do every day to help with just that.

1. Seated spinal twist

Why it’s important:Spinal rotation helps maintain mobility, improves posture, decompresses the spine and reduces stiffness caused by prolonged sitting.

How to do it:Sit cross-legged on the floor or upright in a chair. Inhale to lift the arms, then exhale as you twist to the right, rotating from the belly through the ribs, chest, shoulders, head and neck. Hold for five slow breaths, then repeat on the other side.

2. Lunge

Why it’s important:Sitting with bent hips, whether at a desk or in a car, shortens the hip flexors and pulls the torso forward. Lunges lengthen these muscles, supporting better posture and helping prevent low back pain.

How to do it:Step one foot forward and lower the back knee. Reach the arms overhead, gently firm the glutes and engage the abdomen to protect the lower back. Hook the thumbs if comfortable to lengthen the torso and lift the chest. Hold for five to eight breaths, then switch sides.

3. Supported fish pose

Why it’s important:This pose counteracts “tech neck” and upper-back rounding by opening the chest, throat and thoracic spine.

How to do it:Lie back over a rolled blanket, foam roller or yoga block placed beneath the shoulder blades. Use a blanket if you need additional support for your head. Keep the knees bent so the focus stays on the upper back. Let the arms fall open with palms facing up and allow gravity to do the work. Stay for one to two minutes.

4. Bridge pose

Why it’s important:Bridge pose strengthens the back body — glutes, hamstrings and spinal muscles — while opening the front of the hips, supporting both posture and spinal health.

How to do it:Lie on your back with knees bent and feet hip-width apart. Press into the heels to lift the hips. Keep the chest broad by tucking the arms underneath and pressing them down. Hold for five breaths, then lower. Repeat three times.

5. Legs up the wall

Why it’s important: This simple and gentle inversion helps reset the nervous system, improves circulation and relieves swelling in the legs after long periods of sitting, standing or travel.

How to do it:Sit sideways next to a wall and swing the legs up as you lie back. Open the arms with palms facing up. If a wall isn’t available, rest the legs over a couch or chair. Close the eyes, slow the breath and stay for at least five to seven minutes.

You don’t need long workouts to boost longevity. These five stretches work together to undo some of the physical strain of modern life. They will help you you stand taller, move more freely and rest more deeply.

Patrick Francois a yoga instructor and co-director at YogaRenew Teacher Training Online. He leads in-person and online teacher trainings all over the world, and focuses primarily on yoga sequencing and the business of yoga, infusing his own enthusiasm and grounded approach to spirituality into every class he teaches.

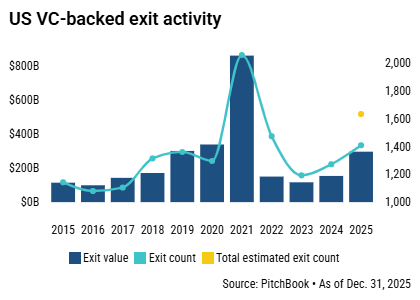

2025 IPO boom wasn’t enough to solve VCs’ problems

By Kyle Stanford, Director of US Venture Research

US VC-backed exits totaled nearly $300 billion in value during 2025, nearly double 2024’s total—but making it only the fourth-highest value in the past decade, according to our latest PitchBook-NVCA Venture Monitor.

VCs expected 2025 to finally bring back significant liquidity, which it delivered to a point. While total value did increase, the uncertainty created by the new US tariffs and the government shutdown in early Q4 put a damper on the year’s IPO count.

The number of completed listings barely surpassed the prior couple of years. And by year’s end, only a small pipeline of companies had begun the registration process, not the long line of candidates the industry would hope for.

The aggregate value of unicorns has jumped to $4.3 trillion, further straining the problem. The ongoing lack of liquidity comes after years of robust fundraising by VCs, fueled by growing private market valuations.

But with returns remaining unrealized, LPs are left waiting and wishing. The impact of the overall lack of liquidity is obvious: 2025 recorded the lowest VC fundraising total since 2018.

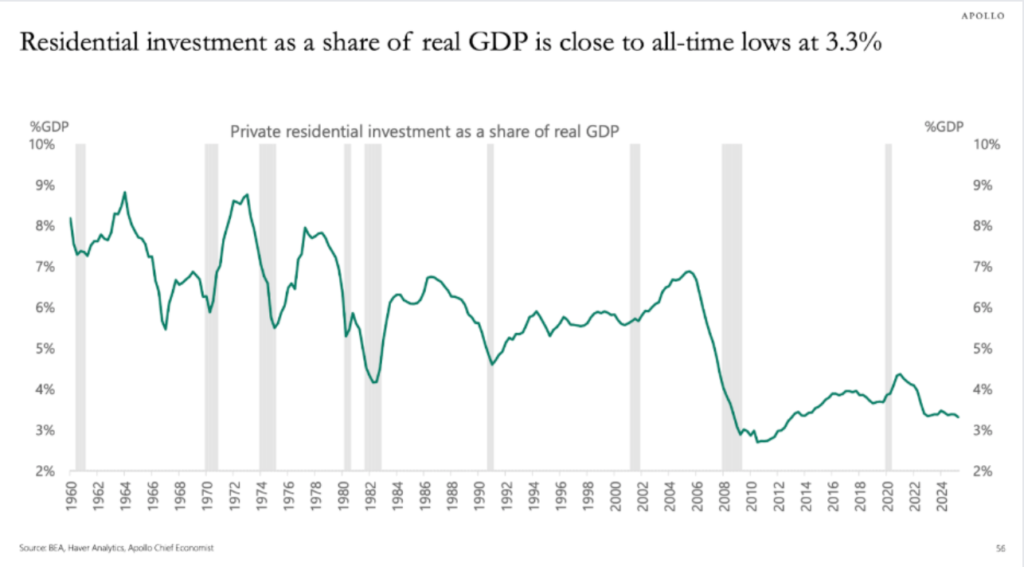

4. Residential Investment as a Share of Real GDP is Close to All-Time Low

The irrelevant investor

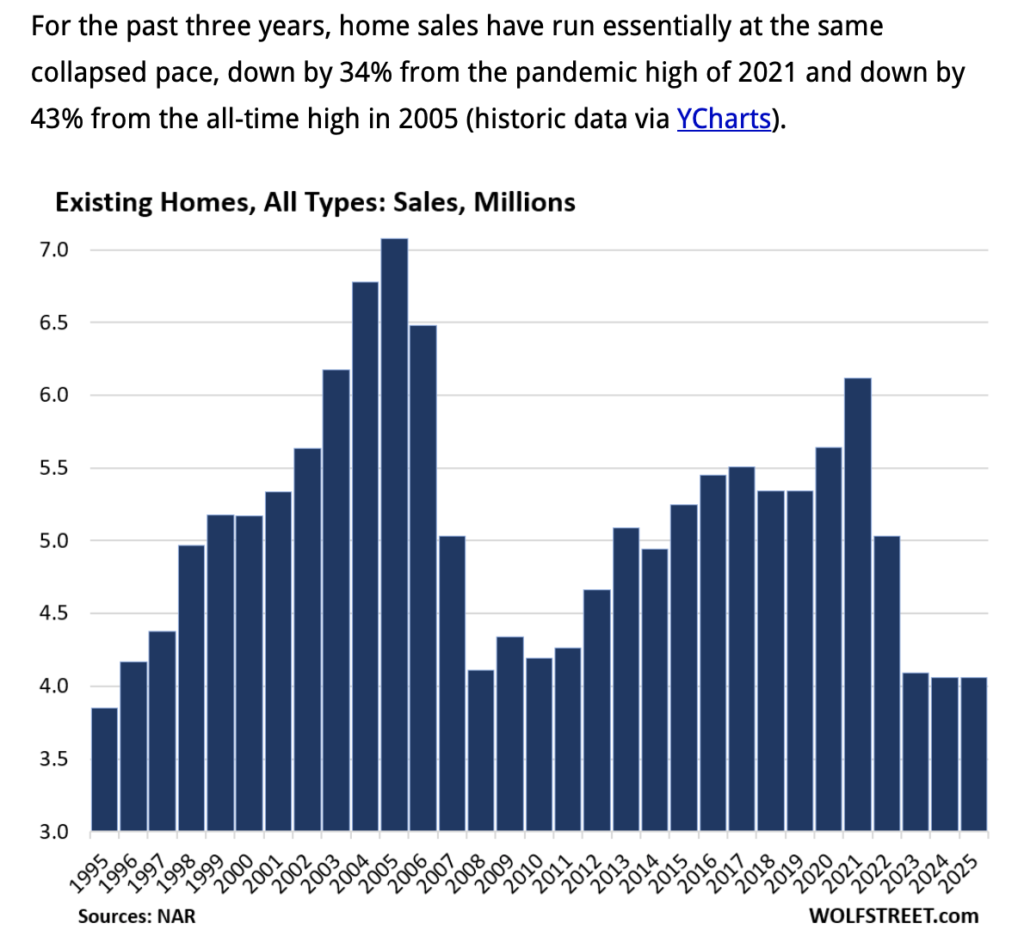

5. Home Sellers Pull Listings Off Market Until Spring

Sales of Existing Homes in 2025 Drop to Lowest since 1995, Sellers Massively Yank Listings off the Market, Waiting for Spring-by Wolf Richter

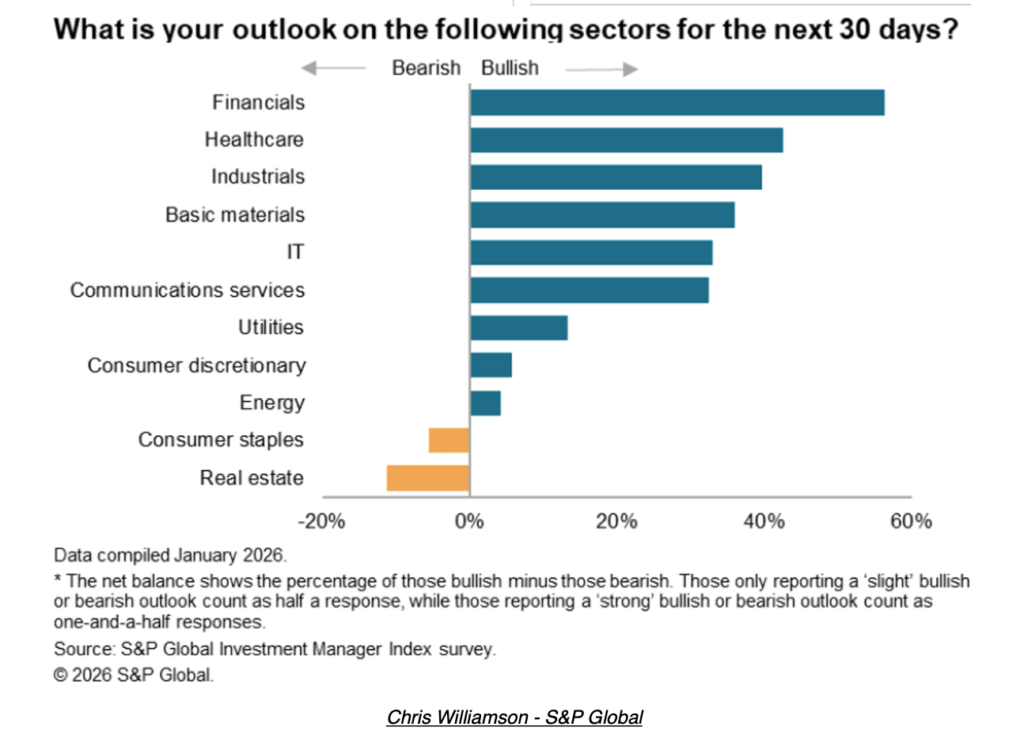

6. Institutional Investors Most Bullish on Financials and Healthcare

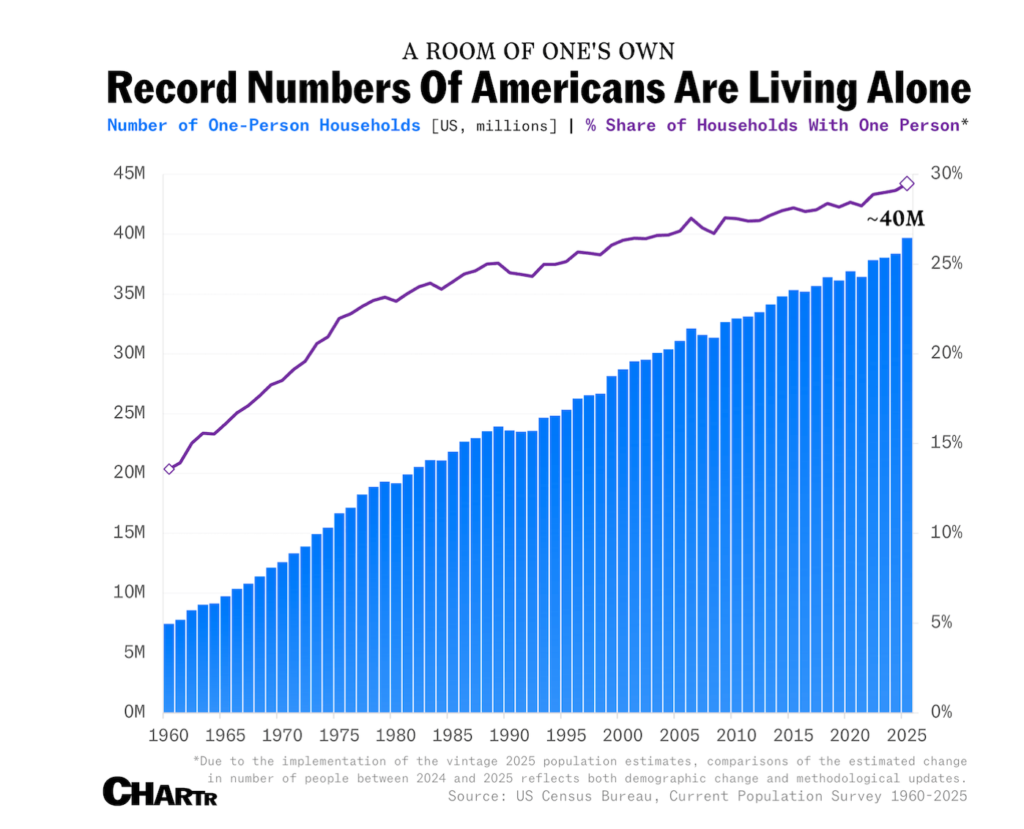

7. Record Number of Americans Live Alone

chartr

8. 25k Russian Soldiers Being Killed Per Month in Ukraine.

Russia’s ‘massive’ losses in Ukraine have it heading toward a breaking point, NATO’s top official says

NATO’s secretary general said up to 25,000 Russian soldiers are being killed in Ukraine each month. By Jake Epstein

Mark Rutte described the carnage as “unsustainable” for Moscow.

That suggests that a breaking point is coming, though it remains unclear when.

Russia’s military is suffering heavy losses fighting in Ukraine, with up to 25,000 soldiers killed a month, NATO’s top civilian official said this week, calling the carnage “unsustainable” for Moscow.

“The Russians, at the moment, are losing massive amounts of their soldiers thanks to the Ukrainian defense,” NATO Secretary General Mark Rutte told European lawmakers at a forum in Brussels on Tuesday. He said that 20,000 to 25,000 troops are dying each month as the war drags on.

“I’m not talking seriously wounded. Killed.” Rutte clarified. He compared the incredibly high losses to the Soviet Union’s invasion of Afghanistan in 1979, where an estimated 15,000 of its soldiers were killed over a period of more than nine years.

“Now they lose this amount or more in one month,” he said of the number of Russian soldiers killed every month. “So that’s also unsustainable on their side.”

Russia has not disclosed official casualty figures, but Ukrainian and Western estimates paint a grim picture for Moscow.

Caring What Others Thought: This was my biggest waste of energy. I used to worry about how my choices looked to people who weren’t even living the life I wanted. The truth? Nobody cares as much as you think they do. Do what’s right for you.

The Cost of Waiting is Real: Whether it’s traveling, building a home, or starting a renovation, waiting will almost always cost you more money. Materials go up, labor goes up, and time disappears. If you have the means, do it now.

Helping Others: I did not help others soon enough. Sharing what you know can change someone’s life. Business, investing, or otherwise. It’s why I started to gift my book as much as I have. Make sure you give back.

Life is a Series of Routines: We are what we do every day. If your routine is nothing but stress and spreadsheets, that’s what your life will be. So build good ones.

Work to Live, Don’t Live to Work: We all have to grind sometimes, but don’t let the grind become your identity. Work is the engine that funds the life you want to lead, not the other way around.

The U-Haul Principle: You’ve heard it before, there’s no U-Haul behind a hearse. You don’t want to be the richest man in the graveyard. Use your investments to fund a life you actually enjoy today, not just a number for a future you might not see.

Spreadsheets Don’t Capture Everything: You have to do what you want to do, not just what looks mathematically optimal on a spreadsheet. Sometimes the “right” move for your life doesn’t fit into a cell in Excel. Not everything fits on a spreadsheet. You do what works for you, not what looks right to others. Who cares.

“Toxic masculinity” is often mentioned online but there is not much psychological research on it.

A new study in more than 15,000 mean investigated eight markers of toxic masculinity.

Only 10.8 percent of men included in the study showed clear signs of toxic masculinity.

Hostile and benevolent toxic masculinity need to be differentiated.

“Toxic Masculinity” is a buzzword widely used online that broadly captures troubling attitudes about masculinity that may be harmful to others. However, little actual psychological research has been conducted on it. This is a problem, since it leaves unclear what defines toxic masculinity and how common it is.

A new psychological study on toxic masculinity

A new study entitled “Are Men Toxic? A Person-Centered Investigation Into the Prevalence of Different Types of Masculinity in a Large Sample of New Zealand Men,” published in “Psychology of Men & Masculinities,” a scientific journal by the American Psychological Association APA, focused on toxic masculinity (Hill Cone and co-workers, 2026). In the study, the research team, led by scientist Deborah Hill Cone from the School of Psychology at the University of Auckland in New Zealand, analyzed data from the New Zealand Attitudes and Values Study. Overall, data from more than 15,000 male heterosexual volunteers aged between 18 and 99 years were included in the study. The volunteers included in the study had filled out various questionnaires, and the scientists concentrated on analyzing eight factors that could indicate problematic or toxic masculinity:

Gender identity centrality: This psychological construct measures how important it is for someone’s sense of self to be a man.

Disagreeableness: A personality trait that includes being unpleasant and offensive to other people.

Narcissism: A personality trait that includes an increased sense of self-worth, often at the cost of other people.

Hostile sexism: Overtly negative attitudes towards women.

Benevolent sexism: Attitudes towards women that are not overtly hostile but still view them in a stereotypical way.

Opposition to domestic violence prevention initiatives: Being opposed to initiatives helping prevent violence towards women in relationships

Social dominance orientation: A preference against equality in social groups and for having a dominance hierarchy within groups.

Results of the study: Only about 11 percent of men show toxic masculinity

The scientists used advanced statistical modelling to identify subgroups of men characterized by distinct profiles across the eight toxic masculinity markers included in the study. These “latent profile analyses” revealed five distinct groups of men regarding toxic masculinity. The good news is that most men did not show toxic masculinity.

The largest group was called “Atoxics” (35.4 percent). These men showed low values across all eight indicators of toxic masculinity.

The second and third largest groups (27.2 percent and 26.6 percent of volunteers) both showed low to moderate values across the eight indicators of toxic masculinity.

Only the two smallest groups showed high levels of toxic masculinity. These included the “Benevolent Toxic” group (7.6 percent) that showed high values on benevolent sexism and sexual prejudice and moderate-to-high values on the other markers of toxic masculinity. The smallest group was the “Hostile Toxic” group (3.2 percent) that showed the highest values on hostile sexism, opposition to domestic violence prevention, disagreeableness, narcissism, and social dominance orientation.

Takeaway

Taken together, only 10.8 percent of the volunteers in this large study showed clear signs of toxic masculinity, while 89.2 percent did not. This finding indicates that the vast majority of men are not “toxic” and do not believe in destructive male attitudes. The study also showed that there seem to be two forms of toxic masculinity: the hostile and the benevolent. The scientists suggested that this finding should be kept in mind when developing measures to protect against toxic masculinity.