Category Archives: Daily Top Ten

Topley’s Top 10 – November 10, 2021

1.85% of U.S. High Yield Market has a Yield Below the Current Rate of CPI Headline Inflation vs. Historical Less Than 10%

Topley’s Top 10 – November 9, 2021

1.Get Rich Overnight FOMO

Topley’s Top 10 – October 20, 2021

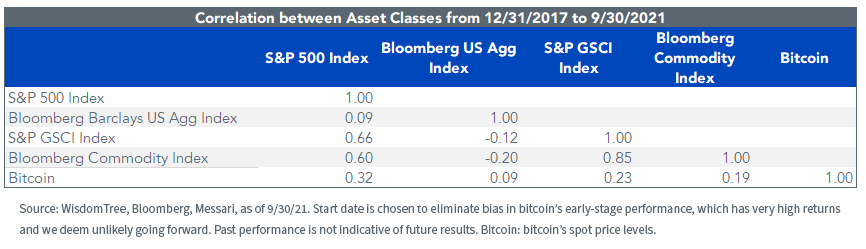

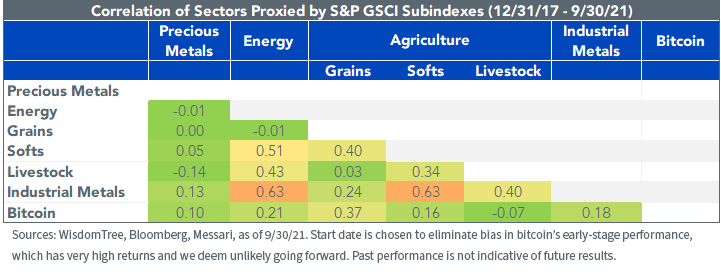

1.Bitcoin Correlation to other Asset Classes

WisdomTree

For definitions of terms in the chart, please visit the glossary.

We believe it could also further enhance portfolio diversification among commodity sectors.

The Story Behind Bitcoin Futures in an ETF–Jianing Wu https://www.wisdomtree.com/blog/2021-10-18/the-story-behind-bitcoin-futures-in-an-etf

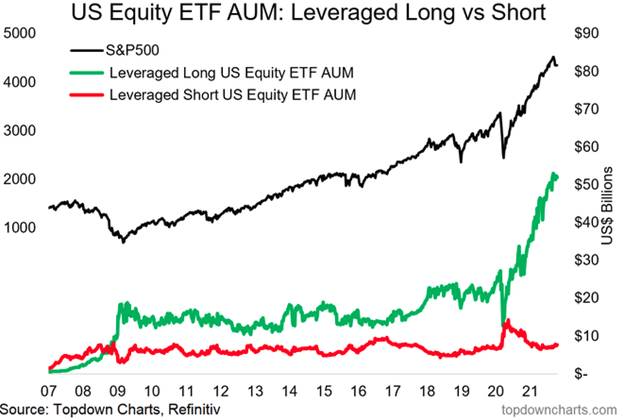

2.Leveraged Long Equity ETF Strategies at All-Time Highs…Risk On in Place.

Dave Lutz at Jones Trading

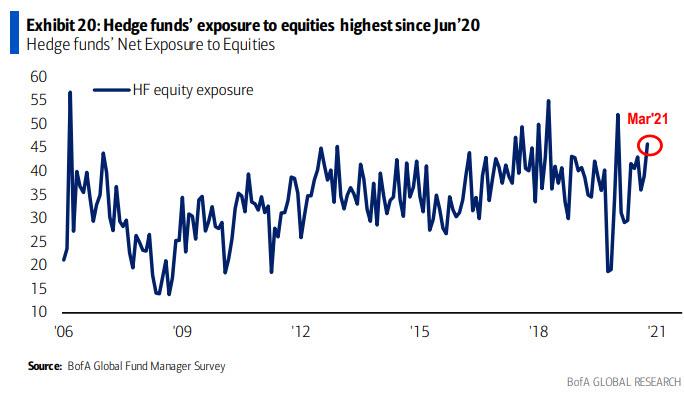

3.Hedge Funds Exposure to Equities Highest Since June 20

BY TYLER DURDEN

https://www.zerohedge.com/markets/historic-divergence-emerges-wall-street

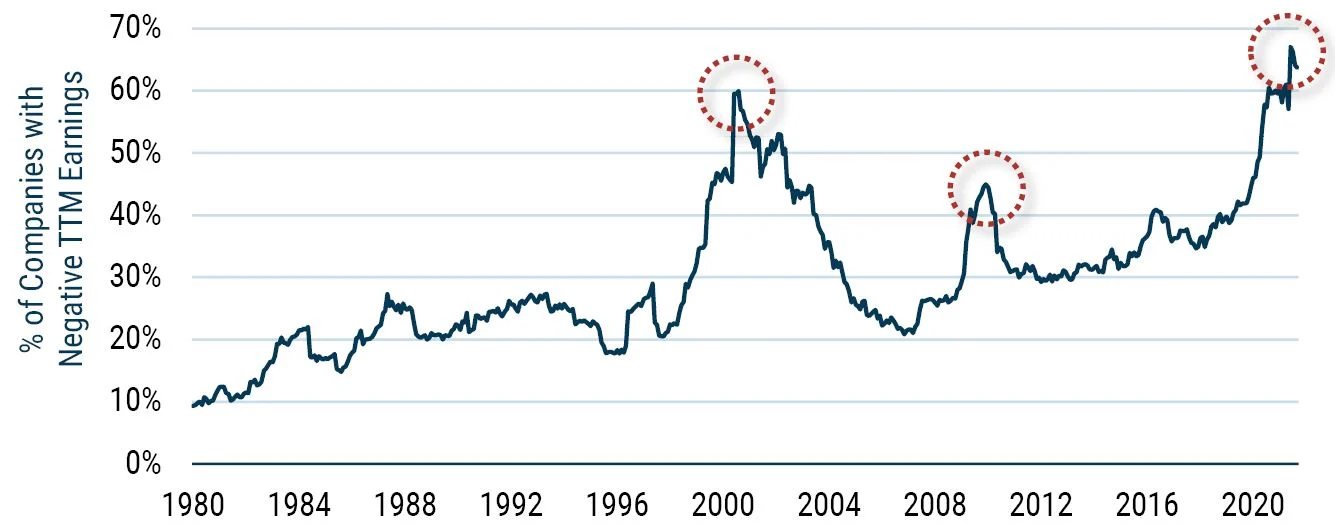

4.More Than Half of U.S. Growth Stocks Have Negative Earnings

More than half of U.S. Growth stocks* have negative earnings, yet Growth stocks have dramatically outperformed in the past few years

Growth Bubble: Making Money On Companies That Make No Money

Today, 60% of the Growth stocks in the Russell 3000 Index make no money, and this was true even before the COVID-induced recession. Yet these very companies have been generating huge returns in price movement over the past few years, dramatically outperforming their Value counterparts. The Russell 3000 Growth Index was up 84% cumulatively over the last two years through August (more than double the return of its Value counterpart). So investors are making money on companies that make no money – never a good sign when it is done this pervasively and at these valuations. And while not common, it is also not unique. We all witnessed the same speculative behavior in the late 1990s and in the 2008 speculative bubble.

Source: GMO

Found at Barry Ritholtz The Big Picture https://ritholtz.com/2021/10/10-tuesday-am-reads-353/

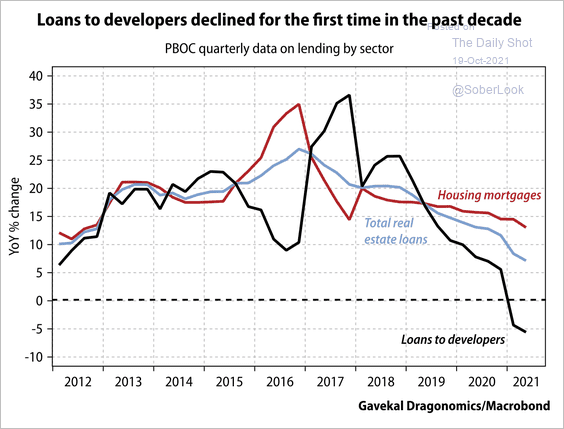

5.Loans to Developers in China dropped for the First Time in a Decade.

https://dailyshotbrief.com/the-daily-shot-brief-october-19th-2021/

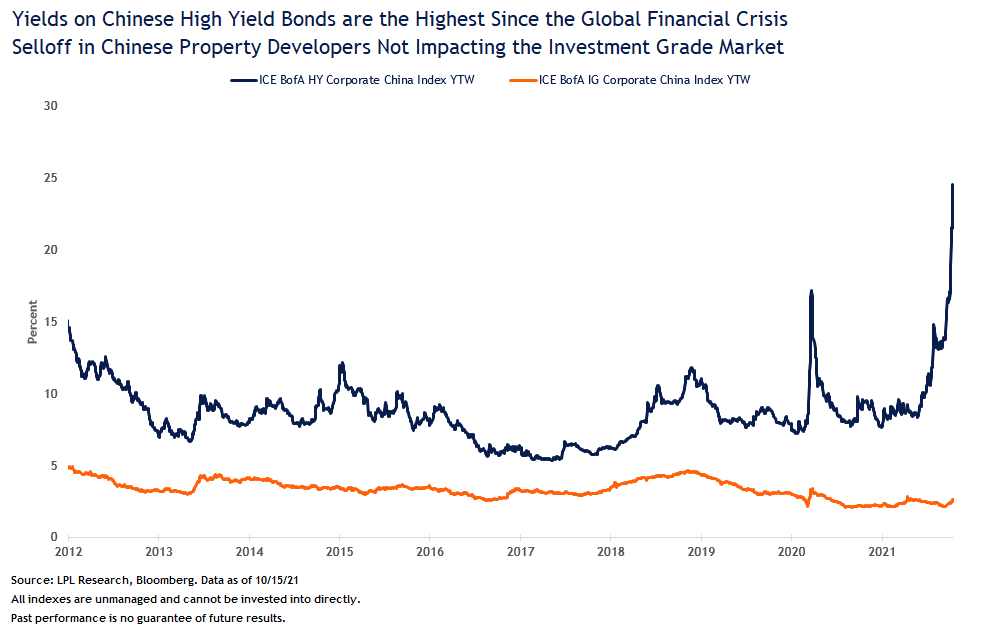

6.Yields on Chinese Junk Bonds Hit 25%

Taking Another Look at the Chinese Real Estate Market

Market Blog

Tuesday, October 19, 2021

China’s debt levels have surged since the global financial crisis and now sit at over 300% of gross domestic product (GDP), as of December 2020. The majority of that new debt has come from households and non-financial companies, which is why the Chinese government has made deleveraging a priority. Moreover, to help rein in the very high debt levels in the US$60 trillion China real estate market—which is likely the largest asset class in the world—more than 400 new regulations have been announced this year. As such, these regulations have caused Chinese junk-rated property developer bonds to underperform this year—and in the case of Evergrande, stoke concerns about broader economic spillovers.

“Default risk has clearly risen within the Chinese real estate market,” noted LPL Financial Fixed Income Strategist Lawrence Gillum. “However, we still think policy makers in China will prevent broader systemic risks to spread due to the deleveraging efforts currently taking place.”

As seen in the LPL Research Chart of the Day, yields on Chinese junk-rated bonds nearly touched 25% before falling recently. So far, this month has been one of the worst months in decades for the Chinese high yield market as the selloff in the property developer markets continued—the real estate sector makes up 66% of the high yield index. Additionally, of the $142 billion of U.S. dollar-denominated bonds trading at distressed prices (generally defined as debt with yields over 10%), 48% were issued by Chinese real estate companies, according to data compiled by Bloomberg. However, that the China investment-grade corporate index hasn’t responded in-kind provides us comfort that the spillover effects are, at this time, limited to the junk-rated property developer issuers. Property developers make up over 11% of the investment-grade index and while these companies have seen their yields increase, they haven’t increased nearly has much as their junk-rated counterparts. In aggregate, yields on the investment-grade property developers are still less than 5%.

Interestingly, the most recent move higher in junk-rated yields wasn’t related to Evergrande, which has likely already been priced into markets. Rather, a much smaller property developer, Fantasia, told investors that it wasn’t going to make a bond payment when it was due despite having the necessary cash on hand to make the payment. Bond investors are generally concerned about an entity’s ability to pay its debts but also its willingness to pay its debt. That Fantasia decided not to pay its obligations caused investors to question the commitment of the property developer market broadly in servicing its financial obligations. That breach of financial responsibility caused the People’s Bank of China (PBOC) to finally break its silence on the ongoing selloff in the property developer market by urging real estate developers to pay its bills on time.

Additionally, the PBOC finally commented specifically on the potential spillover crisis at Evergrande and said the risk was “controllable”, which likely means there won’t be a bailout per se but we do expect the PBOC to ring-fence the risks and prevent them from spilling over into the broader financial system and the economy. Time is running out on Evergrande, though, as the company could officially be in default on October 23 after the payment grace period runs out.

Taking Another Look at the Chinese Real Estate Market | LPL Financial Research (lplresearch.com)

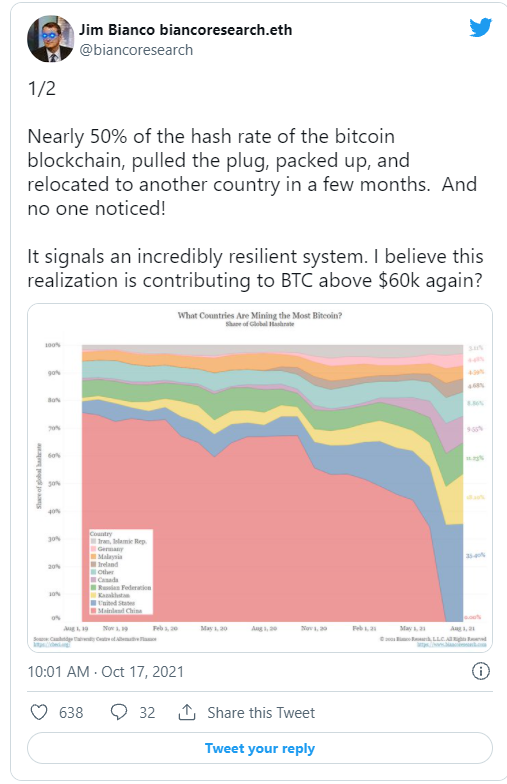

7.China Handed Bitcoin Mining Over to U.S. and Canada.

Marketwatch “Nearly 50% of the computing power (called hash rate) of the bitcoin blockchain, pulled the plug, packed up, and relocated to another country in a few months. And no one noticed! It signals an incredibly resilient system. I believe this realization is contributing to BTC above $60k again?” he said.

Bianco was referring to China, as this chart shows:

He credited the China pullout to a “catastrophic mistake,” saying that “when cryptos take hold as a legitimate medium of exchange, they will be left behind.” China last month declared all crypto-related transactions illegal.

“Combined with China’s regulatory crackdown in other industries, and why do we have a hard time believing that China is regressing? It seems to be the most plausible explanation,” said the strategist, who noted North America is dominating those hash rates.

“The Chinese handed an incredible opportunity to the U.S. and Canada to now dominate the digital currencies. Let’s not blow it,” added Bianco.

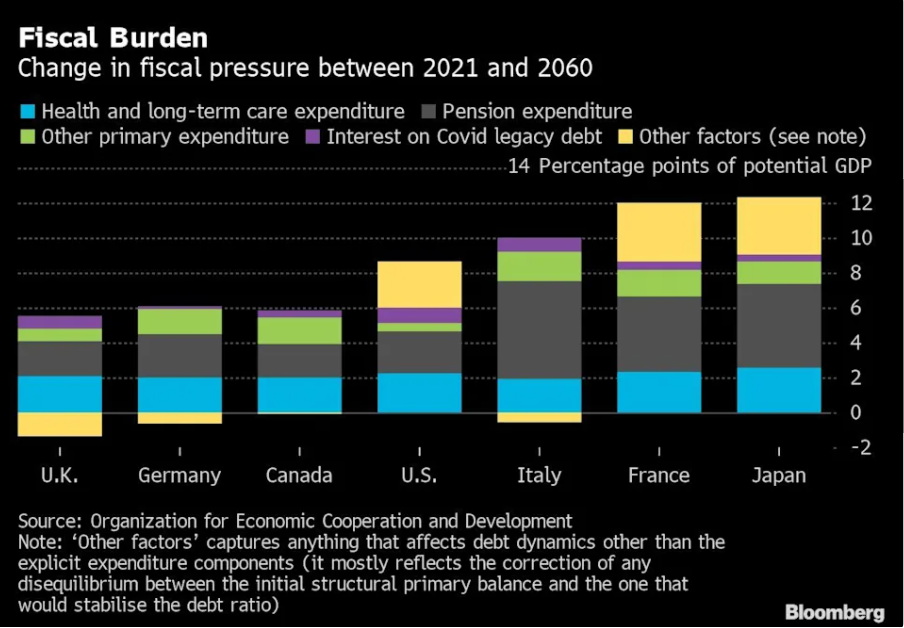

8.Covid Related Increases in Global Fiscal Burdens.

William Horobin(Bloomberg) —

The Covid-19 pandemic may have bloated public debt to levels already pushing some governments to consider consolidation, but that’s nothing compared to the fiscal difficulties brewing in the coming decades, the OECD said.

According to its long-term scenario, a deceleration in large emerging economies, demographic change and slowing productivity gains will drag trend economic growth among the OECD’s 38 members and the Group-of-20 nations to 1.5% in 2060 from around 3% currently. At the same time, states will face rising costs, particular from pensions and health care.

To maintain public services and benefits while stabilizing debt in that environment, governments would have to raise revenues by nearly 8% of gross domestic product, the OECD said. In some countries, including France and Japan, the size of the challenge would amount to more than 10% of output, and the economists didn’t even account for new expenditures such as climate change adaptation.

“Secular trends such as population aging and the rising relative price of services will keep adding pressure on government budgets,” the OECD said in the policy paper prepared by Yvan Guillemette and David Turner. “Fiscal pressure from these long-run trends dwarf that associated with servicing Covid-legacy public debt.”

Countries need not necessarily raise taxes to meet these challenges, the OECD said. Instead, it called for reforms to boost employment rates and raise retirement ages.

A combination of action in those two areas — including ensuring effective retirement ages rise by two thirds of future gains in life expectancy — could halve the projected increase in fiscal pressure by 2060 in the median country, according to the organization.

https://www.yahoo.com/finance/news/world-faces-fiscal-problems-much-090000541.html

9.These 7 habits will keep your mind sharp no matter how long you work

But you can turn these odds in your favor by practicing certain healthy habits, says William R. Klemm Ph.D., a senior professor of neuroscience at Texas A&M University. He offers these tips:

- Get better organized. Keep your keys, for example, in one place all the time. “Life is simpler when you have a place for everything,” Klemm says. Habit relieves the memory.”

- Challenge yourself mentally. “Seek out new experiences, stay active socially, make mental demands on yourself, such as learning a new language, playing chess, or getting an advanced college degree,” Klemm says.

- Reduce stress. “Chronic stress(emotional pressure suffered for a prolonged period of time in which an individual perceives they have little or no control) clearly disrupts memory formation and recall,” he writes.

- Eat foods with vitamins and antioxidants. Focus on vitamins C, D, and E. Like many experts on aging, he says you should eat blueberries, “especially on an empty stomach.” What about vitamin supplements? They won’t help, Klemm says, unless you have a nutritional deficiency. Focus on food.

- Avoid obesity. Weight increases stress on the heart and arteries, which pump oxygenated blood to your brain, which helps you retain mental sharpness.

- Exercise. Enough said. Keeps the blood flowing, and the pounds off. Talk to your doctor first.

- Get plenty of sleep. “Many studies show the brain is processing the day’s events while you sleep and consolidating them in memory,” Klemm says. “Naps help too!” He adds.

Naps? Count me in.

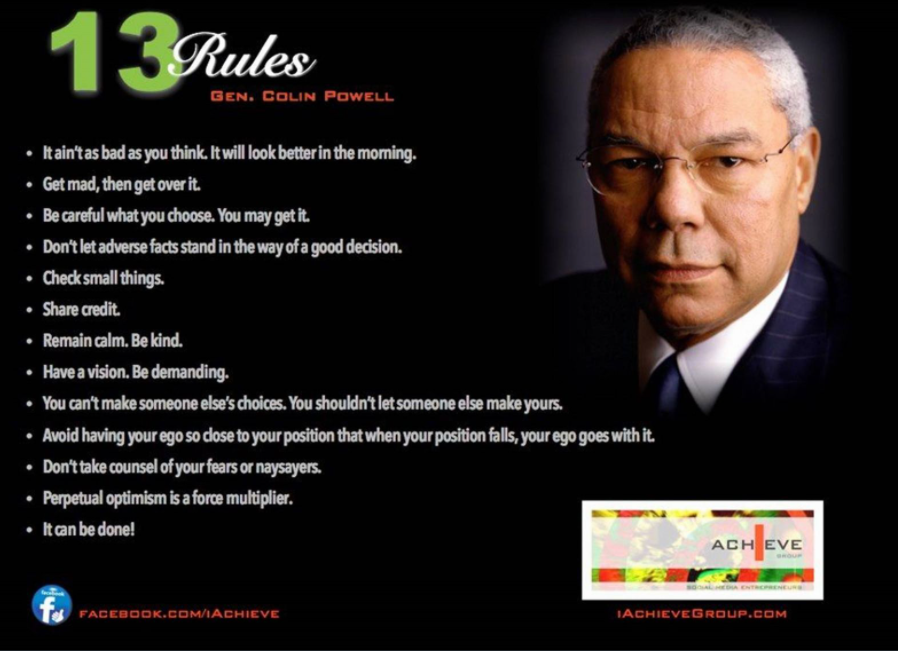

10.Colin Powell’s 10 Simple Rules.

Topley’s Top 10 – October 19, 2021

1. Energy having a Big Run but Interesting to Run the 10 Year Charts.

XLE Energy ETF 10 Year

VDE Vanguard Energy ETF 10 Year

PSCE Invesco Small Cap Energy ETF 10 Year

https://www.google.com/finance/quote/PSCE:NASDAQ?sa=X&ved=2ahUKEwj5k9CgxdTzAhU2oXIEHWwuDVEQ3ecFegQIDBAS

2. Shanghai to LA Container Prices Topping Out??

From Morning Brew

In 2013, the Winklevoss twins filed the first application for a bitcoin exchange-traded fund (ETF). Eight years and countless rejections later, the first bitcoin-based ETF could begin trading as soon as today.

The ETF, launched by the fund manager ProShares, will give virtually any investor with a brokerage account the ability to gain exposure to the world’s largest crypto.

- We didn’t say “buy the crypto,” because that’s not what’s happening. The bitcoin ETF is based on futures contracts, which allow investors to bet on the price swings of an underlying asset without owning it outright.

The SEC, Wall Street’s top sheriff, is much more comfortable allowing a futures-based bitcoin ETF to proceed than one that directly buys the tokens. Bitcoin futures have been trading on the regulated Chicago Mercantile Exchange since 2017. Bitcoin itself, meanwhile, is bought and sold on many different exchanges that are outside the gaze of the SEC.

It’s unclear whether the ETF will be a hit

The first mutual fund based on bitcoin futures, which launched in July, had only $15 million in assets under management two months later—basically negligible when put in the context of the $21.3 trillion US mutual fund industry.

And the ETF news was received by some crypto professionals with a big “meh.” A bitcoin futures ETF may not reliably track bitcoin prices, while many investors are comfortable with the current options available for buying bitcoin. When asked by CNBC whether he would be investing in the ETF, bitcoin bull Mark Cuban said, “No. I can buy BTC directly.”

Looking ahead…bitcoin’s price could be volatile in the next few weeks as four different bitcoin futures ETFs may begin trading this month.

https://www.morningbrew.com/daily

Current Bitcoin ETF Filings Etf.com

|

Fund |

Issuer |

Filing Date |

SEC Filing |

|

Bitwise Bitcoin Strategy ETF |

Bitwise |

9/14/21 |

|

|

AdvisorShares Managed Bitcoin ETF |

AdvisorShares |

8/20/21 |

|

|

Galaxy Bitcoin Strategy ETF |

Galaxy Digital |

8/18/2021 |

|

|

Valkyrie Bitcoin Strategy ETF |

Valkyrie Funds |

8/11/2021 |

|

|

Bitcoin Strategy ETF |

VanEck |

8/9/2021 |

|

|

ProShares Bitcoin Strategy ETF |

ProShares Advisors |

8/4/2021 |

|

|

Invesco Bitcoin Strategy ETF |

Invesco Capital Management |

8/4/2021 |

|

|

Global X Bitcoin Trust |

Global X Digital Assets |

7/21/2021 |

|

|

ARK 21Shares Bitcoin ETF |

21Shares |

6/28/2021 |

|

|

One River Carbon Neutral Bitcoin Trust |

One River Digital Asset Management |

5/24/2021 |

|

|

Teucrium Bitcoin Futures Fund |

Teucrium Trading |

5/20/2021 |

|

|

Galaxy Bitcoin ETF |

Galaxy Digital Capital Management |

4/12/2021 |

|

|

Kryptoin Bitcoin ETF Trust |

Kryptoin Investment Advisors |

4/9/2021 |

|

|

Wise Origin Bitcoin Trust |

FD Funds Management |

3/24/2021 |

|

|

First Trust SkyBridge Bitcoin ETF Trust |

First Trust Advisors |

3/19/2021 |

|

|

WisdomTree Bitcoin Trust |

WisdomTree Digital Commodity Services |

3/11/2021 |

|

|

NYDIG Bitcoin ETF |

NYDIG Asset Management |

2/16/2021 |

|

|

Valkyrie Bitcoin Fund |

Valkyrie Digital Assets |

1/22/2021 |

|

|

VanEck Bitcoin Trust |

VanEck Digital Assets |

12/30/2020 |

https://www.etf.com/sections/blog/etfcom-live-blog-bitcoin-etf-launch-watch

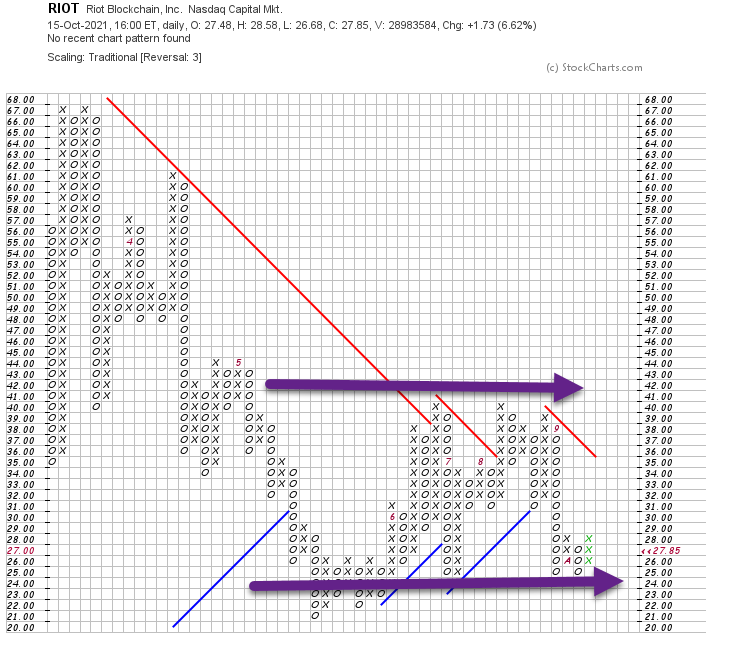

3. Crypto Stock Charts not Following Bitcoin Rally.

RIOT Sideways -50%+ from highs

COIN -50% Correction…Sideways pattern for months.

MARA different story…..Breaking out to new highs.

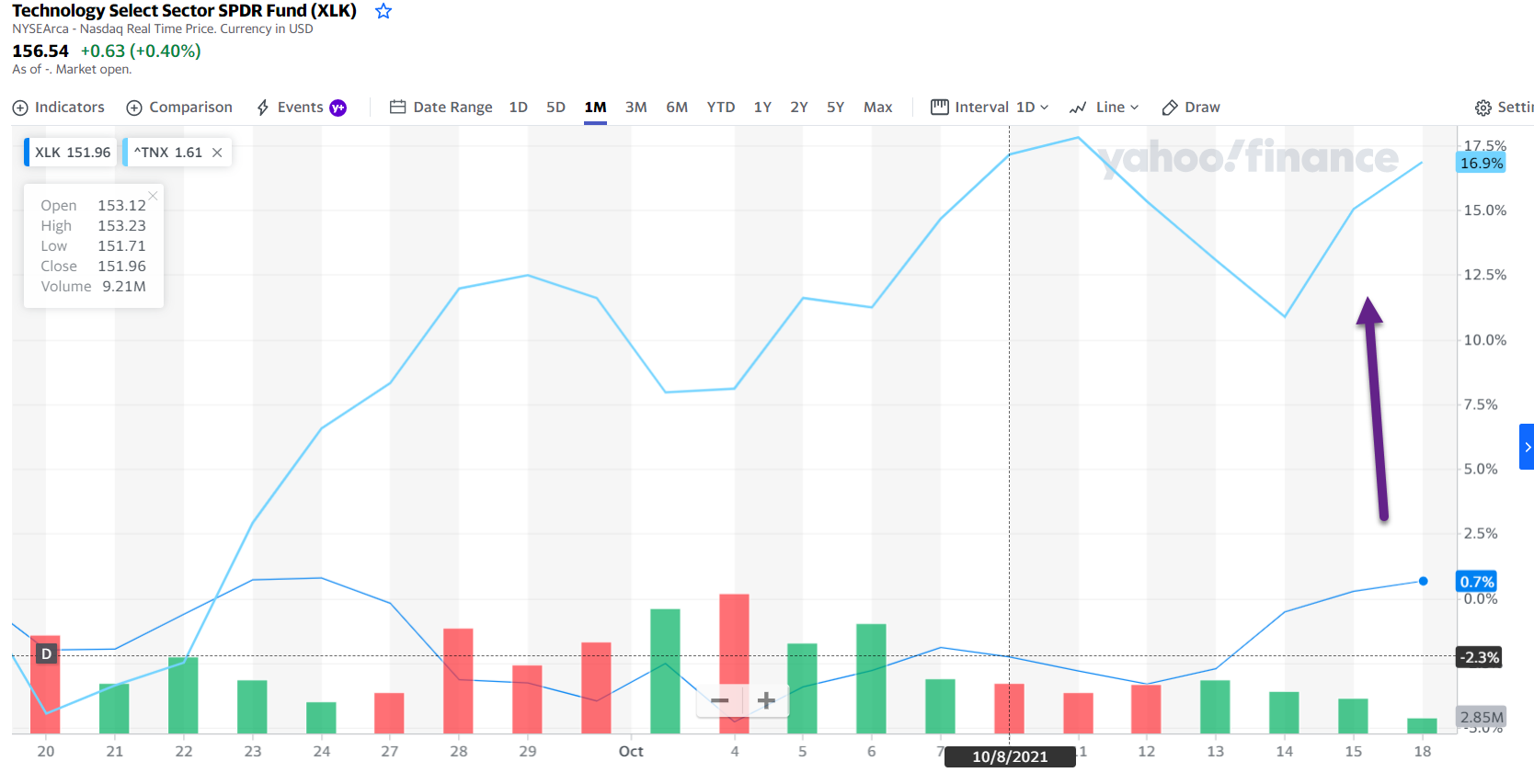

4. Correlation Between S&P Tech Stocks and 10 Year Treasury Yield is -.69 This Year.

Barrons–The connection between yields and tech shares is no illusion. The correlation between the S&P 500 Technology Sector index’s performance, relative to that of the S&P 500, on the one hand, and the 10-year yield on the other has averaged -0.69 this year, and hit -0.78 for the 126 days ended Sept. 30. (A correlation of -1 means that two variables move in perfect opposition.)

https://www.barrons.com/

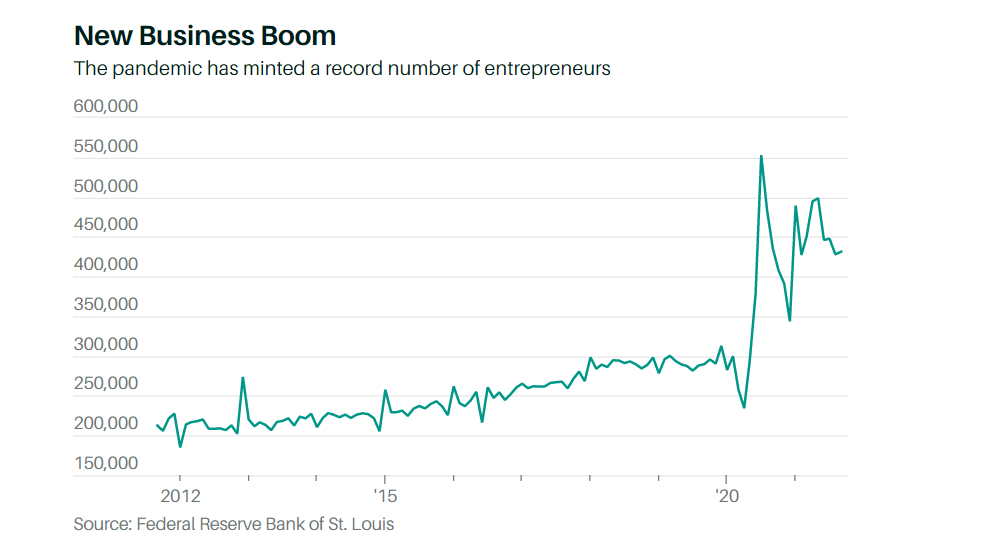

5. Positive for America….Entrepreneurs are Booming

Barrons-The peak was in July 2020, when close to 600,000 new business applications were filed, up 100% from the year prior. Monthly applications have since fallen but remain about 50% higher than before the virus took hold

The Workers Won’t Be Coming Back, Covid or Not. Here Are Theories on Where They Went.By Lisa Beilfuss

6. Up to Date Hedge Fund Returns Since 2013

The digital economy accounts for about 10% of India’s gross domestic product, compared with 40% in today’s China. One in 10 Indians shopped online prepandemic; nearly half of all Chinese do. By Craig Mellow https://www.barrons.com/

7. Number of +/- 1% Days Normalizing Vs. Historical for 2021

8. Stock Market Leader Domino’s Pizza …-15% Correction from highs

DPZ pulls back to June levels.

9. Surge in Conversions of Office, Factories, Retail into Apartments……..Philadelphia Leads the Pack.

‘Living at the Office’ Takes On a New Meaning During the Pandemic-The sudden increase in vacant commercial spaces has fueled a surge in conversions to rental homes, according to a new study.

NY Times By Michael Kolomatsky Creating rental apartments in former offices, factories and other nonresidential buildings is nothing new, but a recent increase in vacant commercial spaces as a result of the pandemic has fueled a surge in conversions, according to a new study by RentCafé.

https://www.nytimes.com/2021/10/14realestate/offices-hotrls-converted-to-rental-apartments.html

10. Steven Pinker on Rationality

Commentary: Pinker asks, “What’s wrong with people?” but his answer is narrow.

KEY POINTS

- In a new book, Pinker provides clear and useful explanations of logic, probability, and other tools for critical thinking.

- But his explanation of irrationality focuses on motivated reasoning and myside bias.

- Overcoming irrationality could gain from motivational interviewing and political action, not just critical thinking.

The world seems awash with irrationality, evident in anti-vaxxers, climate change deniers, and political conspirators. What is to be done? Steven Pinker’s spirited, amusing, and lucid new book argues that the solution comes from increasing the amount of rationality in the world, accomplished by expanding people’s understanding of logic, probability, rational choice, and causal reasoning. But helping people to be more rational in their thoughts and actions needs improvements in empathy and politics as well as critical thinking.

Pinker provides clear and useful expositions of topics like the contribution of probability theory to producing better beliefs and actions, and the difference between correlation and causation. He then moves on to consideration of why humanity appears to be losing its mind, as shown in the “carnival of cockamamie conspiracy theories” about COVID-19, such as that vaccines implant microchips in people’s bodies.

Pinker discounts three popular explanations for why people succumb to such nonsense.

The first is that people fall prey to the systematic thinking errors that philosophers call fallacies and psychologists call biases. The second is that the “pandemic of poppycock” results from the prevalence of social media. The third is that people embrace false beliefs that give them comfort or help them make sense of the world. Instead, he thinks that irrationality arises largely from motivated reasoning and what he calls “myside bias.”

Motivated reasoning is the tendency to base conclusions on personal goals and emotions rather than on objective evidence (Kunda, 1990). We all want to believe that we are going to be happy, healthy, successful, and loved, so we distort evidence to help us think that these goals are being accomplished. I agree with Pinker that motivated reasoning is a major cause of false beliefs about COVID-19 (e.g., I’m not going to get sick, so I don’t need to be vaccinated), climate change (e.g., the weather just fluctuates, so I don’t need to change my energy habits), and politics (e.g., my wonderful leader will solve my economic problems).

Pinker’s second major source of irrationality is myside bias, which Pinker interprets as the tendency of people to reason to conclusions that enhance the correctness of their political, religious, ethnic, or cultural tribe. For example, conservatives want to support the beliefs of other conservatives, and liberals want to support the beliefs of other liberals. Pinker’s myside bias is narrower than the usual interpretation of myside bias that “occurs when we evaluate evidence, generate evidence, and test hypotheses in a manner favorable toward our prior opinions and attitudes” (Stanovich, 2021).

Here myside bias is equivalent to motivated reasoning, whereas Pinker applies it to cases where people reason to support their tribe’s interests even when they go against personal motivations. Usually, however, people’s need to belong to and identify with social groups provides a strong motivation to support their beliefs. So I think that Pinker’s narrow idea of myside bias is just a special case of motivated reasoning.

article continues after advertisement

Pinker does not address the question of why people are so prone to making motivated inferences that turn out to be false. In a recent article, “How Rationality is Bounded by the Brain,” I explain the tendency of people to succumb to motivated reasoning as the result of the tight integration of cognition and emotion in the brain. In general, this integration is beneficial because it keeps people’s thinking focused on what emotions indicate are important to their well-being. But integration causes problems when people’s motivations swamp their ability to draw conclusions based on good evidence. Other limitations of the brain that hinder rationality are its slowness and restricted size, along with imperfections in attention and consciousness.

Taking action against irrationality

These limitations raise the question of whether critical thinking is always the best way to overcome irrationality. Most of Pinker’s book concerns using good reasoning strategies such as logic and probability to overcome people’s tendencies to fall into inferential illusions. But another way to help people to overcome errors in thought and action is more like psychotherapy than logic. My blog post on motivational interviewing conjectures that a technique based on questioning and empathy might be better at overcoming motivated inference than more conventional applications of critical thinking. Experiments are needed to compare the two approaches.

Another strategy for overcoming the spread of irrationality is political action to limit the effects of irresponsible social media. Pinker dismisses social media as the main cause of the current prevalence of so many false beliefs but ignores the fact that most people today with false beliefs about COVID-19, climate change, and political conspiracies get them from social media such as Facebook, YouTube, Twitter, and Whatsapp. Explanation of rampant misinformation

I agree with Pinker that the world desperately needs more rationality, but critical thinking needs to combine with empathy and political action to combat the rampant spread of misinformation.

https://www.psychologytoday.