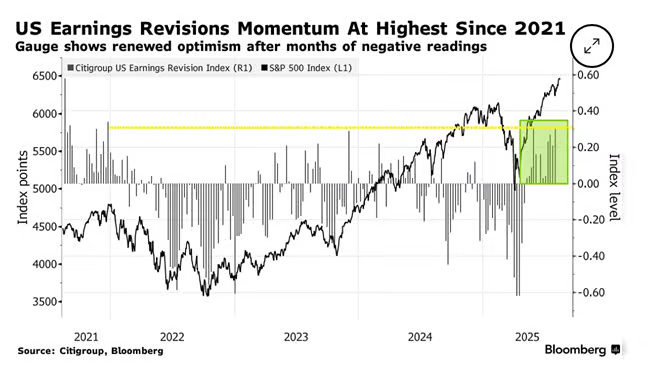

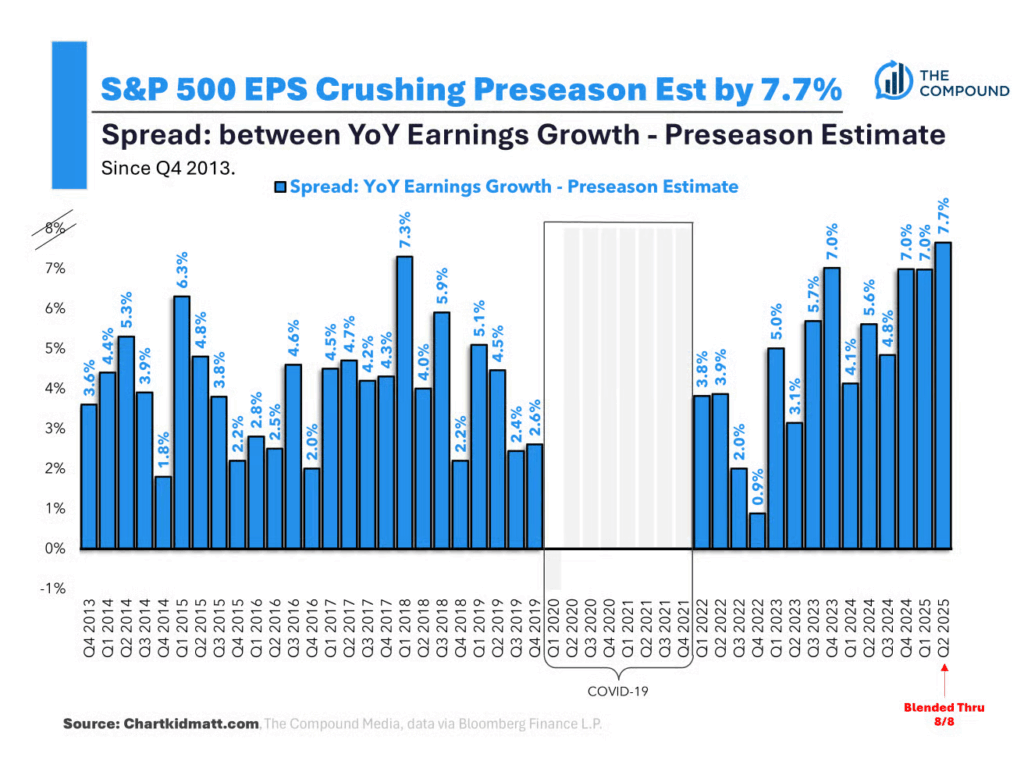

1. It’s All About Earnings—Revision Momentum Highest Since 2011

Bloomberg

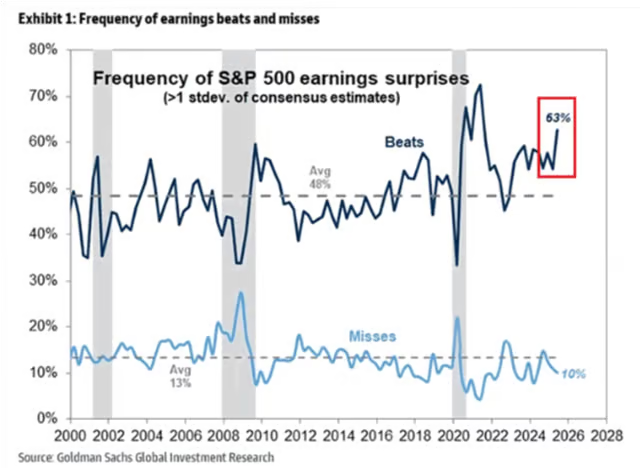

2. It’s All About Earnings—Beats Going Up and Misses Going Down

Irrelevant Investor

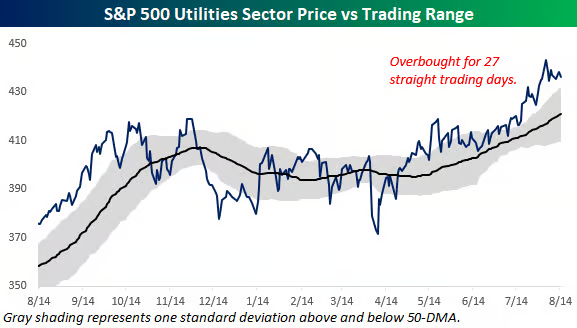

3. AI and Crypto = Energy Usage

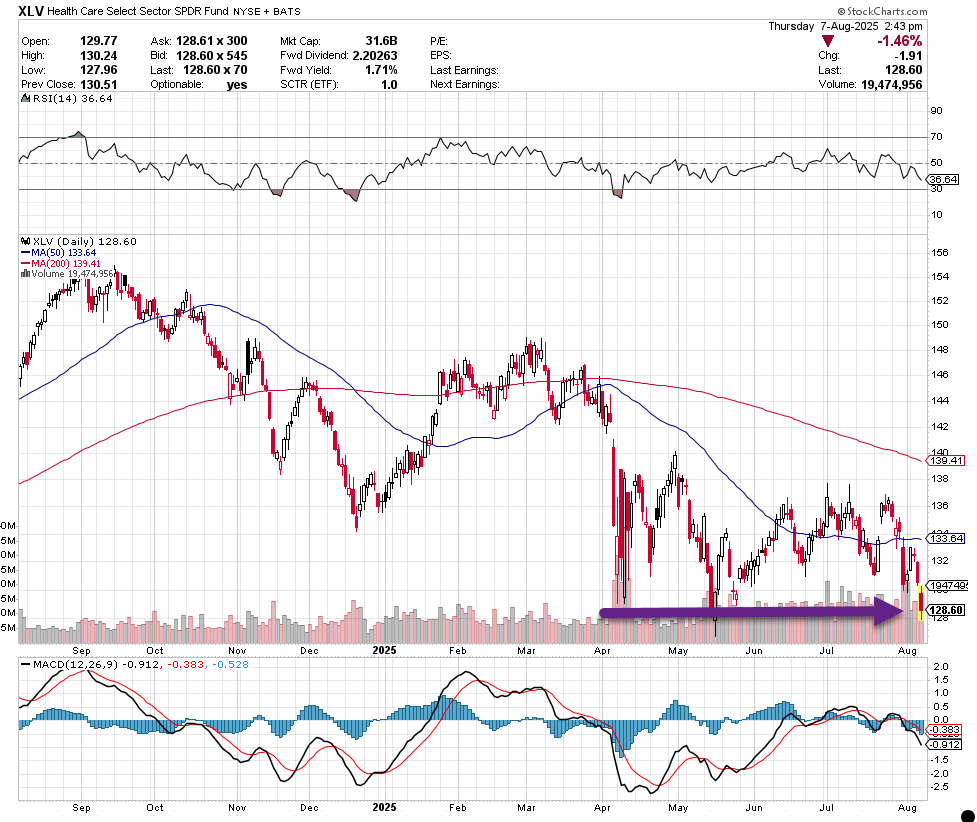

Utilities has been doing anything but lagging the broader market these days. As noted in last night’s Sector Snapshots report, the sector closed at overbought levels for the 27th day in a row yesterday.

Bespoke Investments

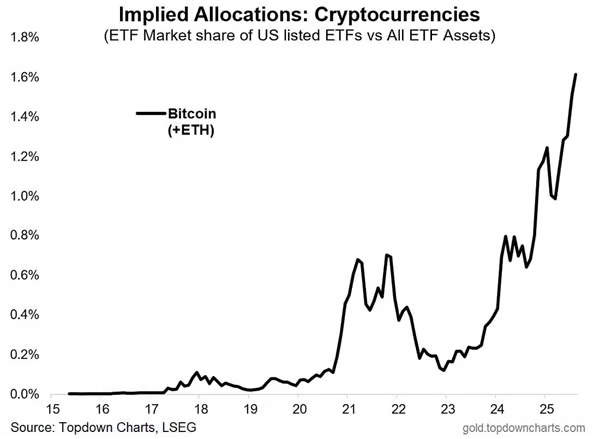

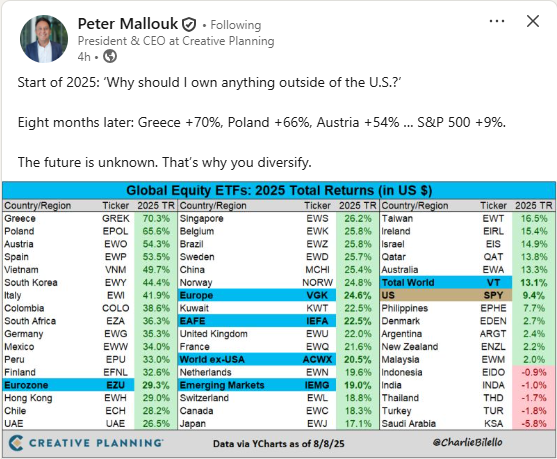

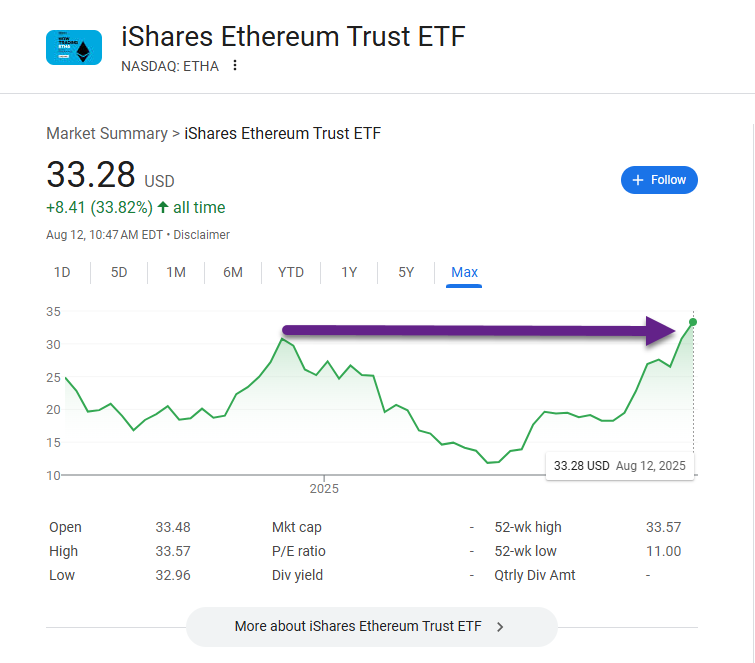

4. Allocation to Cryptocurrencies

Implied crypto allocations. “A mass adoption/speculation phase appears to be taking place as more and more investors make allocations into Bitcoin/crypto.”

Callum Thomas – Top Down Charts

5. JNJ Breaks Out of 5-Year Sideways Channel

Macrotrends

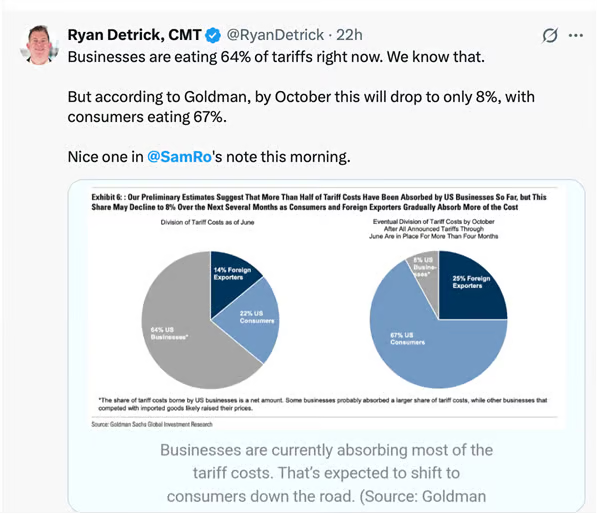

6. Will Business Eating Tariffs Change to Consumers?

Ryan Detrick

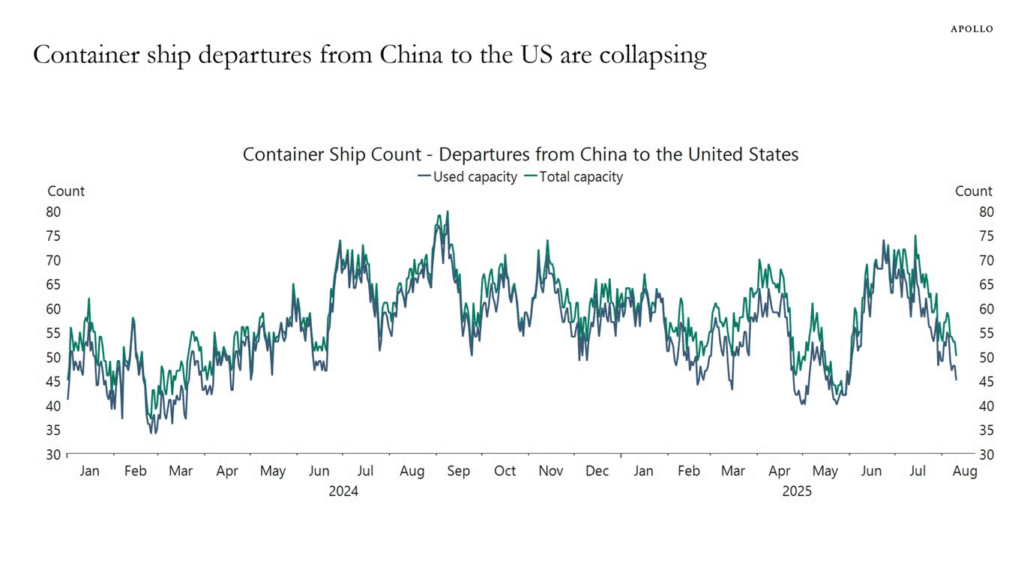

7. Container Ship Departures from China to U.S. are Collapsing

Container ship departures from China to the US are collapsing, see the first chart.

When consumers cannot get the products that they want from abroad, and the products that are imported are more expensive because of tariffs, the outcome is a slowdown in US consumer spending, see the second chart.

The bottom line is that US consumer spending is facing headwinds from tariffs, relatively high interest rates, student loan payments restarting and deportations lowering the number of consumers.

Torken Slok Appolo

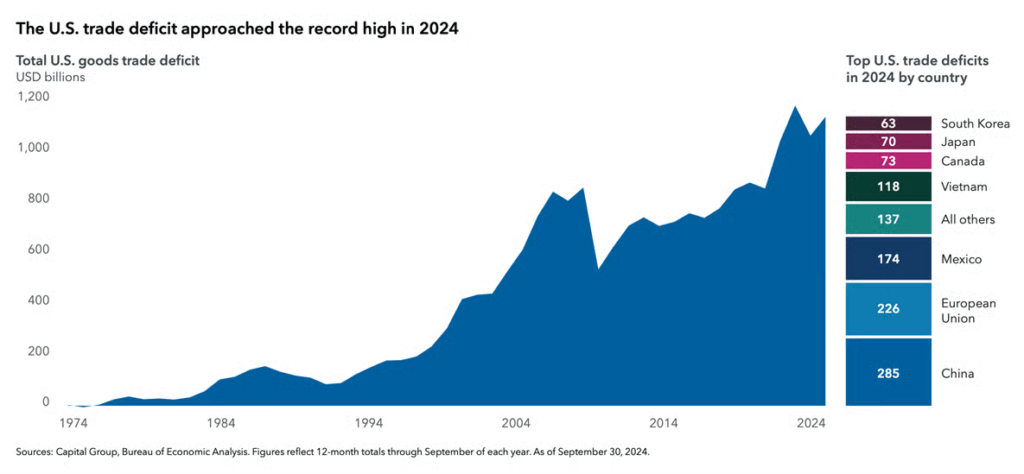

8. U.S. Trade Deficit by Country

Capital Group

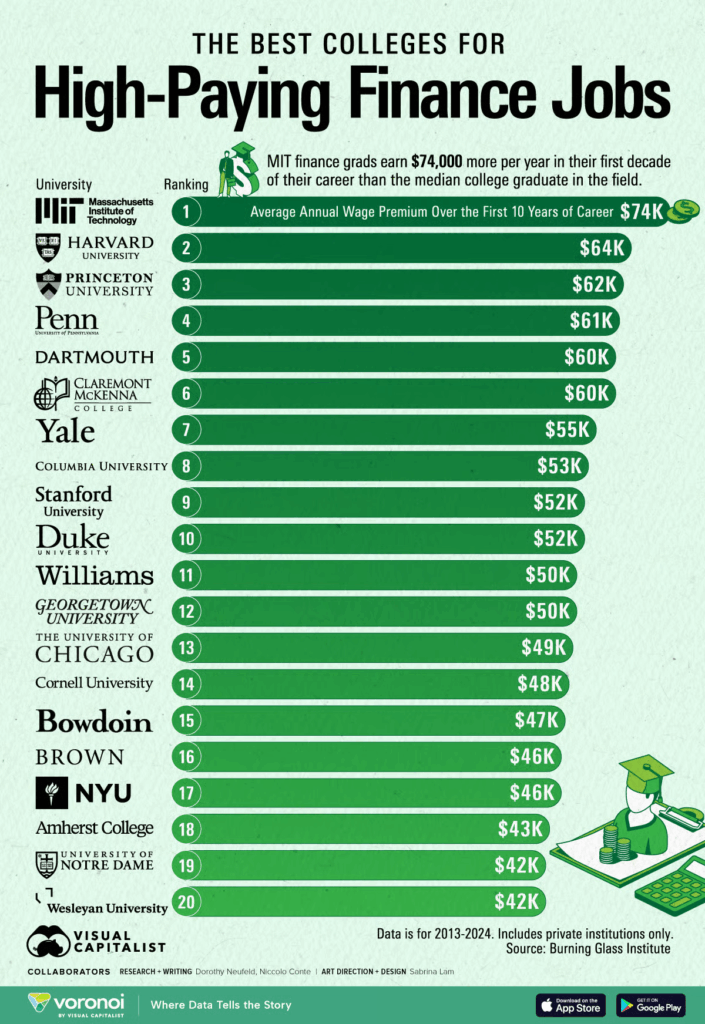

9. The Best Colleges for High Paying Finance Jobs

Visual Capitalist

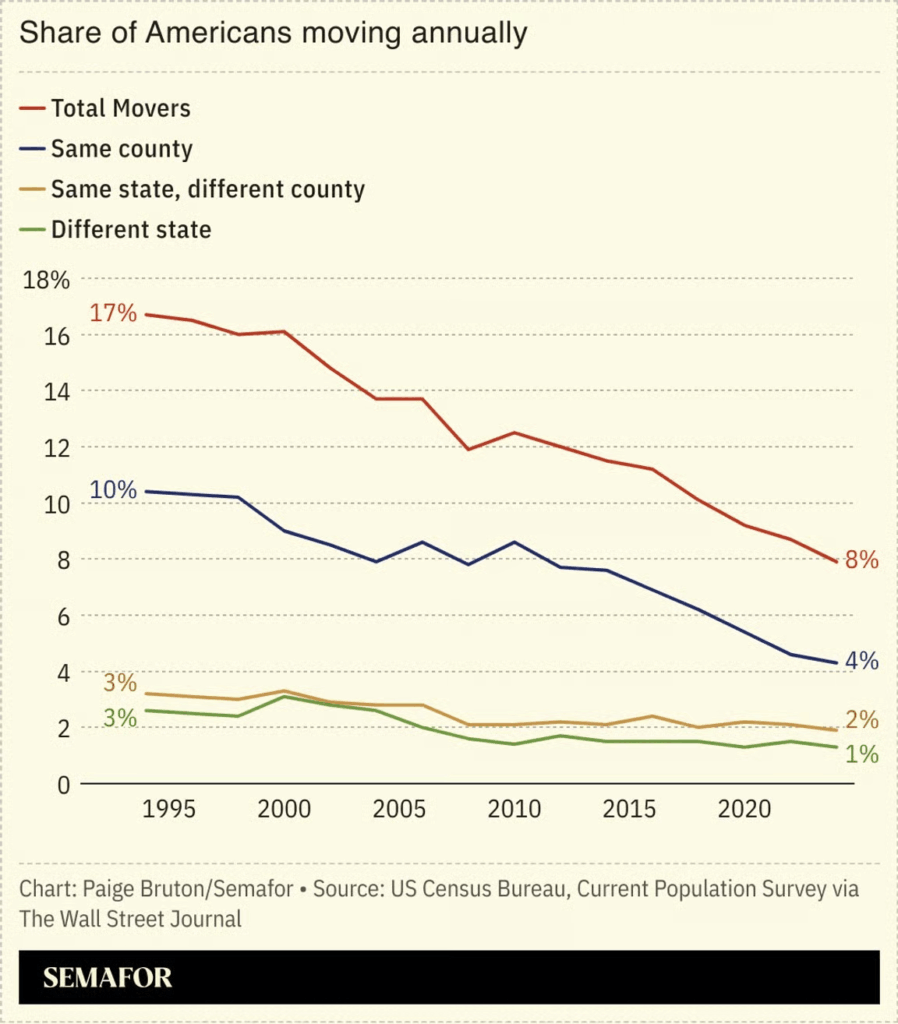

10. Americans Moving Less

Semafor

Americans are moving between cities at historically low rates, with drastic consequences for the country’s economy and politics. Experts worry the lack of internal migration may put the country’s historic dynamism at risk: More people are keeping their homes, and their jobs, resulting in fewer opportunities for younger ones. Some smaller cities are trying to address the issue by offering bonuses to lure remote workers, hoping to help reverse a longrunning brain drain. The US was characterized by moves toward opportunity, but a recent book by the historian Yoni Appelbaum argues that “a country that once made it possible for its people to move freely and chase a better life has steadily strangled that mobility over time.”

A new Gallup report reveals that only 54% of American adults reporting drinking alcohol in 2025.

The percentage of Americans who report drinking alcohol has hit a nearly 90-year low, according to a recent Gallup poll.

The results of Gallup’s annual Consumption Habits survey, released Wednesday, revealed that only 54% of U.S. adults reported drinking alcohol in 2025. This figure represents a three-year decline from 67% in 2022, and falls below the previous record low of 55% in 1958.

Another record low from the 2025 poll: Only 24% of drinkers said they had a drink in the past 24 hours, down from 32% two years ago.

Gallup’s survey of roughly 1,000 U.S. residents, which the company has conducted since 1939, was consistent with other reports on declining alcohol consumption and sales. While there are many contributing factors to the slump — cause for deep concern within California’s $55 billion wine industry — Gallup’s data largely points to the shift in how Americans view alcohol’s effects on health. For the first time since 2001, a majority of Americans surveyed — 53%, up from 45% in 2024 — said they believe drinking in moderation, defined as one or two drinks a day, is bad for their health. In 2018, just 28% of Americans surveyed believed alcohol had negative health impacts.

Perception has changed drastically since the 1990s, when a “60 Minutes” episode about the French Paradox — the belief that a stereotypical French diet heavy on butter, cheese and wine lowers the risk of heart disease — launched a decades-long wine boom. Gallup added questions about beliefs on alcohol’s impact on health in 2001: Through 2011, the percentage of people who believed alcohol was bad for them “hovered near 25%,” states the Gallup report, “roughly equal to those who considered drinking beneficial.”

Yet since then, “the medical research has turned,” said Gallup expert Lydia Saad, who authored the report. Today, only 6% of respondents said they believe alcohol is good for one’s health, another survey low. The shift has occurred as new studies have called the French Paradox hypothesis into question, offering evidence that alcohol has negative impacts on health and can even increase the risk of several types of cancer. In 2023, the World Health Organization declared that no level of alcohol consumption is safe for our health, and earlier this year, the U.S. surgeon generalissued an advisory that stated alcohol is the third leading preventable cause of cancer in America. The U.S. Dietary Guidelines could follow suit this year with a potential change to its recommendation on alcohol consumption. The Gallup report likens alcohol’s decline to tobacco’s in the 1960s after the U.S. surgeon general’s warnings, which “marked the start of a long-term decline in smoking.”

“We’re seeing how quickly Americans have absorbed the information that drinking is likely bad for your health,” said Saad. “The more these findings are reinforced by health authorities, doctors, the federal government, the more likely it is that people who have resisted thus far in believing alcohol is bad for their health may change their minds.”

Moreover, Saad said that while “people who say drinking is bad for your health are still drinking,” the data reveals that many are cutting back. The average number of drinks consumed over the past seven days is 2.8, down from 3.8 drinks a year ago and the lowest figure since 1996. Forty percent of drinkers said it had been a week since they last consumed alcohol — a 25-year high. Those concerned about alcohol’s health effects are having fewer drinks on average than those who aren’t, the data shows.

Read on for other key takeaways from Gallup’s report on alcohol consumption.

It’s so easy to idealize the past. As if people haven’t always been deranged. As if things haven’t always been falling apart. As if fate hasn’t always been indifferent to everyone and everything.

Socrates lived through a 27-year long war—a great power conflict between Athens and Sparta…and then in a country ruled by what was known as the 30 Tyrants. Zeno lived in a world torn apart by the wars of Alexander the Great’s successors (and his own personal shipwreck). Cato saw the Republic fall. Seneca lived through Nero and watched Rome literally burn. So unstable were things that, shortly after his death, people enjoyed the spectacle of the “year of the four emperors” Epictetus spent three decades in slavery. Marcus Aurelius, as we’ve detailed, saw flood and famines and wars. Indeed, this whole period is known as the beginning of the decline and fall.

One could go on and on and on. The point is: It’s always been rough. The point is: It always will be rough. The Stoics were tough—they had to be, to get through what they lived through. You will need to be tough if you’re going to make it through what the present and the future holds.

None of us control when we were born, only how we live. None of us control what our leaders do—not really anyway—only how we live, how we act, how we lead in our own lives. We don’t control what happens, we control how we respond to what happens. We don’t control the awfulness of our times, only whether we rise above them, only whether we do good for and inside them. https://dailystoic.com/

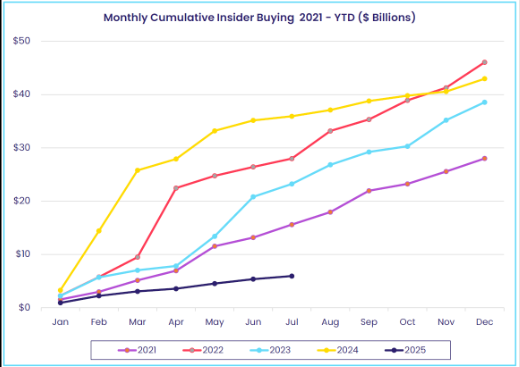

Dave Lutz Jones Trading But Insider buying has plunged this year, with corporate executives showing more caution than the broader investor pool who have driven markets to record highs, Bloomberg reports. Insider purchases totaled just $6 billion in 2025 through July, the slowest pace in eight years, according to data from EPFR Global.

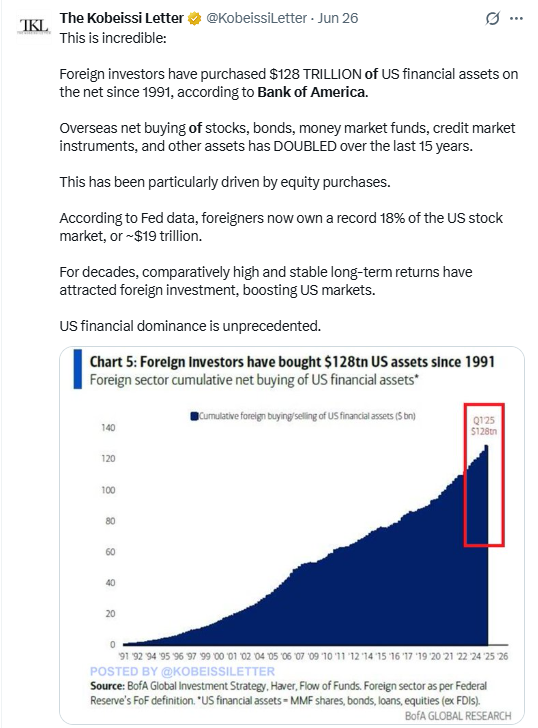

7. Overseas Buying of U.S. Assets Has Doubled in Last 15 Years.

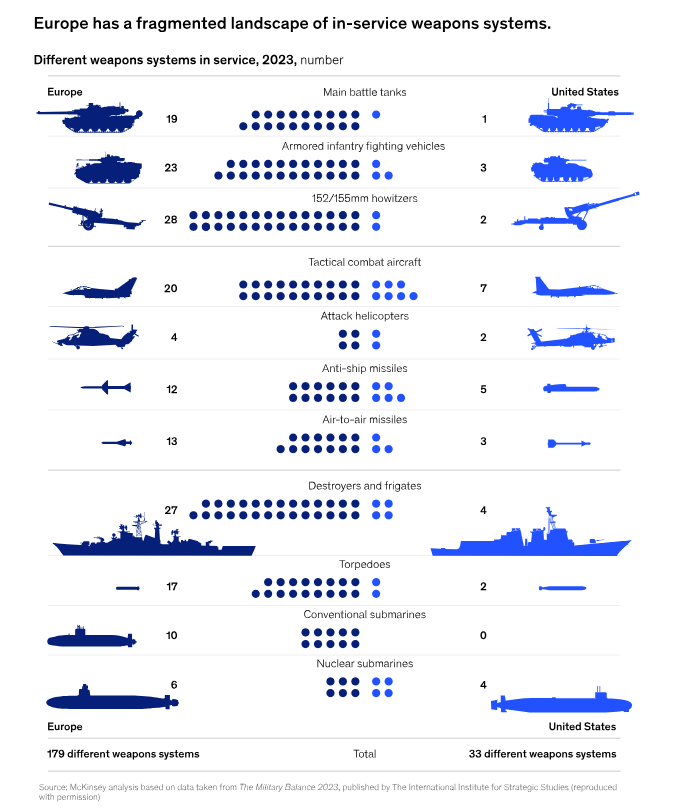

8. 179 Weapons Systems Supplying Europe Military vs. 33 for U.S.

Barrons The result is a hodgepodge of 179 weapons systems supplying European militaries, compared with 33 in the U.S., where the top four contractors soak up more than half of Pentagon procurement, according to Morningstar research. “Joint procurement will be the key to expanding Europe’s defense base,” Muharremi says. https://www.barrons.com/articles/europes-defense-stocks-cool-2-buck-trend-1dc8e6c2?mod=past_editions

Looking for the best finance blogs to follow in 2025? Whether you’re a retail investor, finance professional, or just curious about markets, this curated list of 60 top finance and investing blogs offers deep insights across macro, stocks, tech, and more. These blogs are carefully selected for their originality, consistency, and thought leadership — from hedge fund managers to fintech insiders. Updated regularly by Snippet Finance.

You can find the whole list in the Content Hub where it is regularly updated. There, the blogs are categorized, you can rate them, and add any you think we missed.

Want bite-sized insights from these blogs? Subscribe to Snippet Finance and get curated highlights twice a week.

To discover the 60 best finance and investing blogs, keep reading. Note these are not in order of best to worst but simply the 60 best.

1. Net Interest Category: Financials Smooth, insightful, and effortless writing on everything and anything related to the financial sector.

2. Bits about Money Category: Financials Go deep on the most important financial topics.

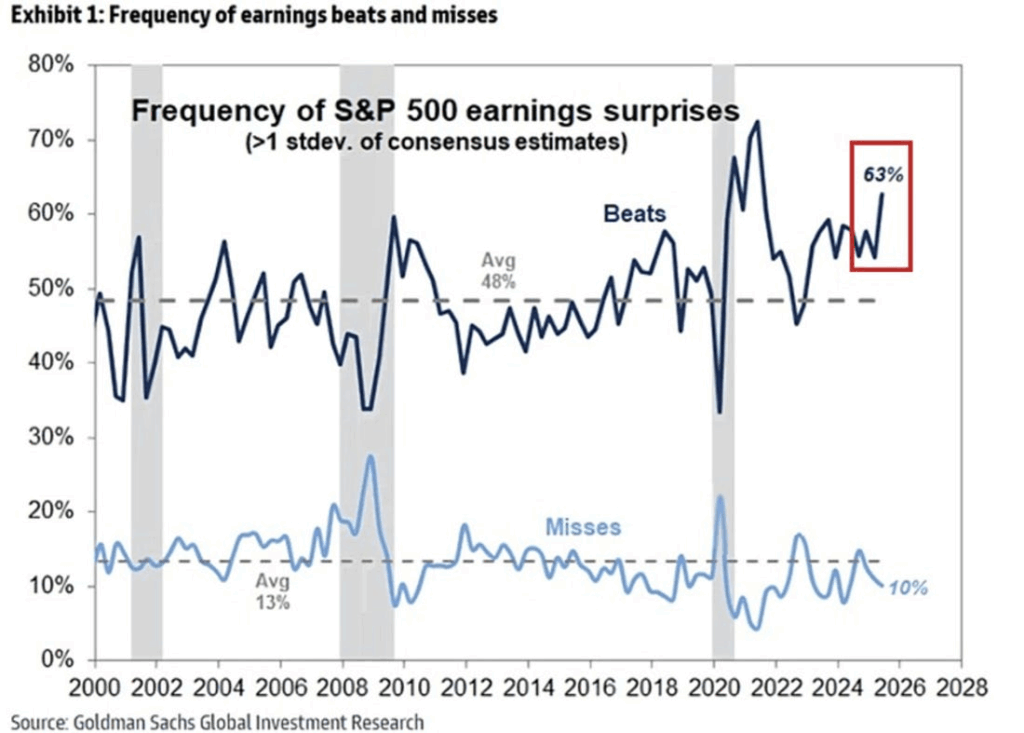

Earnings Surprise! And if you want something to support that, here’s one interesting stat; 63% of the S&P 500 beat their consensus earnings estimate by at least 1 standard deviation. Now to be fair there is a bit of gaming around earnings estimates (companies talk down prospects to analysts to try lower the bar for outperformance — you can see this potentially becoming more endemic over time with big beats trending up and misses trending lower to sideways). But even still, this is a notable datapoint.

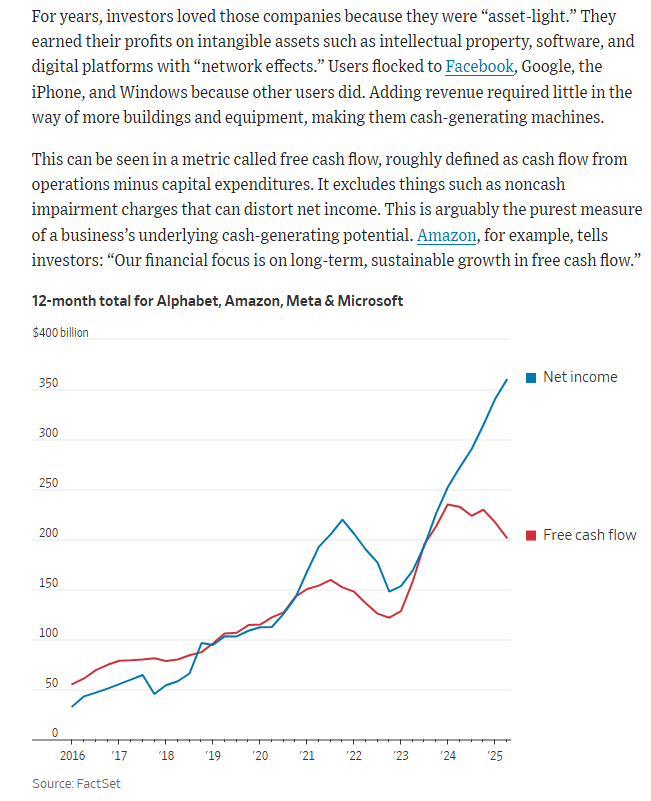

4. Free Cash Flow Slowing Down Due to Huge Capex Spends.

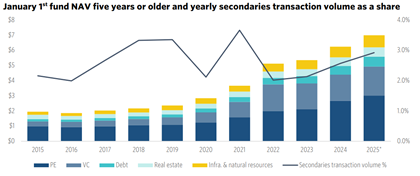

8. Secondaries are becoming second nature-Pitchbook

According to Evercore’s latest Secondaries Market Report, global secondaries transaction volume reached a record $102 billion in the first half of the year.

Once a niche strategy, secondaries have become a core part of the private capital toolkit, offering GPs and LPs alike a flexible, scaled solution for liquidity and portfolio management. LP-led deals made up 53% of total volume, reflecting steady demand from institutional sellers like endowments, foundations, and family offices.

Headline transactions such as Yale’s $2.5 billion sale and the New York City pension system’s $5 billion portfolio sale to Blackstone show how dramatically the market has evolved. What was once a quiet corner of alternatives is now handling transactions at the scale and complexity of large buyouts.

Meanwhile, GP-led deals totaled $48 billion, with multi-asset continuation vehicles gaining traction and syndication options expanding. These structures continue to adapt, balancing alignment with investor optionality and unlocking value from aging assets.

Still, the market is far from saturated. Our estimates suggest that secondaries activity represents only about 3% of total NAV held in funds older than five years, which is where most transaction volume is concentrated. That leaves trillions in legacy fund value as potential future deal flow.

Dry powder has kept pace, growing to an estimated $255 billion, up from less than $180 billion five years ago, based on our estimates. The pools of capital have also grown more specialized, with new strategies targeting credit, real estate, venture, and bespoke GP-led transactions.

In a slower exit environment, secondaries have increasingly become second nature and a central part of the private market landscape.

For related research, our colleagues in Europe have sized the institutional direct VC secondaries market at nearly $15 billion last year in a recent analyst note. Access prior editions of the PitchBook Weekly Commentary in our dedicated workspace.

Psychology Today Why Einstein’s brilliance owed more to method, curiosity, and work than IQ. T. Alexander Puutio Ph.D.

Key points

Raw intelligence is common; genius emerges when it’s systematically developed.

We overrate talent because it’s visible and underrate the hidden work behind it.

Genius can be cultivated through productive skepticism and deliberate practice, even if its a slow process.

Émile Zola, the French novelist, once quipped: “The artist is nothing without the gift, but the gift is nothing without work.”

The very same can be said about geniuses, and, in fact, it should be said much more often than it is.

Our fixation on thinking about intelligence as a feature induces a harmful kind of myopia that does nothing to help us run our engines better. When we look at geniuses like Einstein, what they had going on inside their craniums was only the beginning.

Think of it this way. If genius were a cake, Einstein would have had a bigger kitchen. What he still needed was the right ingredients, the right process, and the willingness to bake. And not just bake, but to make something exquisite.

The work, it turns out, matters much more than the raw brainpower. Without it, we would never have heard of Einstein at all.

Why intelligence doesn’t always germinate into performance

Intelligence is not as rare a commodity as we tend to think.

Statistically speaking, there are likely hundreds of Einstein-level minds walking among us today. There were likely just as many when our earliest ancestors roamed the plains, when their collective intelligence amounted to little more than sharper bits of obsidian and an improved way of roasting meat.

When thinking about geniuses of yore, we often fall for a post-hoc fallacy: We see extraordinary people and their accomplishments, and we attribute those accomplishments entirely to the intelligence they harbor. What we don’t see is the grind behind the scenes and the years of reading, tinkering, failing, and recalibrating, and the failures they’ve left behind. We underweight the work, and in doing so, we miss the true lesson that the rare glimpses of true genius we see could teach us.

Psychologist Françoys Gagné offers a useful lens for why we don’t generate more Einsteins and da Vincis than we do. He divides human abilities into two broad categories: natural abilities and systematically developed ones. We tend to notice the first, the obvious talent, but the second is invisible to us. That invisibility creates the double bind where we overemphasize natural talent because it’s salient, and we underemphasize systematic development because it’s hidden. As a result, we copy the wrong things.

Worse still, those who do find their way to systematic development often struggle to explain it to others. In fact, we often keep them as far away from teaching their methods as we can, and only want to hear of the outcomes instead. Einstein and da Vinci are perfect examples.

What Einstein and da Vinci actually did differently

Einstein, though widely revered today, was no star student in the conventional sense. He disliked rote memorization and distrusted the authoritarian style of teaching that had been passed down since Comenius coined the term didactics in the 17th century.

Instead, he gravitated toward teachers and peers who matched his yearning for independent thought. One such influence was his “Olympia Academy,” a self-made discussion group with fellows Maurice Solovine, a philosophy student, and Conrad Habicht, who was a mathematician and Einstein’s neighbor. Together, they read voraciously across fields, debating philosophy, science, and literature. They weaponized curiosity for no other reason than the joy of it, and that’s how Einstein first encountered Ernst Mach’s The Science of Mechanics, along with other concepts without which we would not be talking of his genius today.

For da Vinci, the formative influence wasn’t in books but in pure, unstructured experimentation. In Andrea del Verrocchio’s workshop, he learned a restless, cross-disciplinary way of working where switching from sculpture to painting to hydraulics without warning; leaving projects half-finished when a new obsession seized him was the norm. Pope Leo reportedly sighed, “Alas, this man will never finish a thing,” while Michelangelo openly mocked him for his unorthodox approach to work and learning. But that habit of wandering into new domains was precisely what fueled da Vinci’s breakthroughs.

In both men, you see the same threads: non-orthodoxy, early exposure to experimentation, and an almost aggressive curiosity. The same pattern runs through Richard Feynman’s safe-cracking physics, Alan Turing’s chess-playing machines, and countless others.

And yet, when we try to “recreate” genius today, we do the opposite. We hand out standardized textbooks, map out linear career paths, and treat curiosity as a distraction rather than the primary fuel for what we hope to come out at the end. Good luck to all involved.

Could you become a genius too?

The question isn’t as naive as it sounds.

We dismiss the thought because we’ve bought the myth that genius is a feature, an inborn gift, rather than a result. Many will even tell you that geniuses are born, not made. But the truth is that genius is cultivated, and, better yet, the cultivation process is accessible to almost everyone.

Adopting productive skepticism and weaponizing your curiosity will build a mind capable of surprising things. Even if your engine runs slower than Einstein’s, remember: This is not a race. Einstein himself took decades to reach his greatest insights, and in some cases, he was wrong.

A good place to start is the work ethic. You can borrow the tools, try your own thought experiments like Einstein, and explore fields you know nothing about like da Vinci. You could even chase ideas you have no immediate use for, just to create space for lateral thinking in the future.

I can’t promise you’ll solve quantum dynamics any better than Einstein did, but I can promise this. If you commit to the same kind of practice, you’ll end up in the rarest labor pool of all, the fellowship of people who are doing the work that creates genius. And that, more than IQ points, is what changes the world.

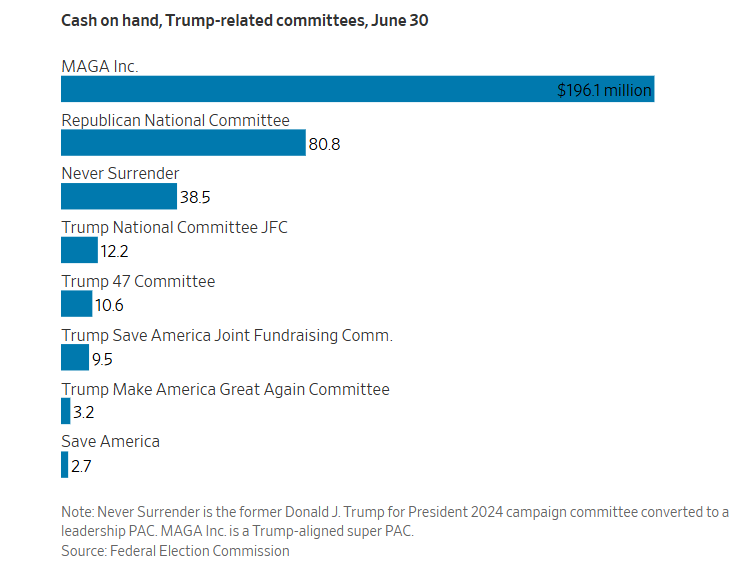

Trump’s political operation has amassed commitments for $1.4 billion, according to a person familiar with the matter—roughly the same amount as contributions in 2024 to Trump’s committees, super PAC and the Republican Party.

Regression to the mean explains that in statistics, outlying events tend to be overcome by average ones. But in society, the opposite is often true. A small headstart becomes a bigger one, or a small stumble can turn into something that is hard to overcome.

Individuals can work to amplify their good luck.

And society is obligated to create the conditions for bad luck to fade into the background.