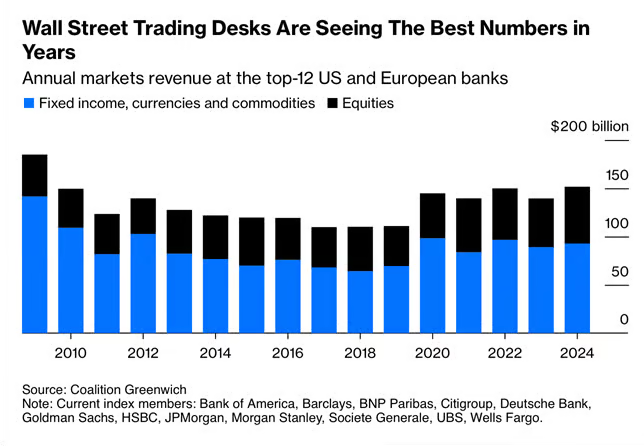

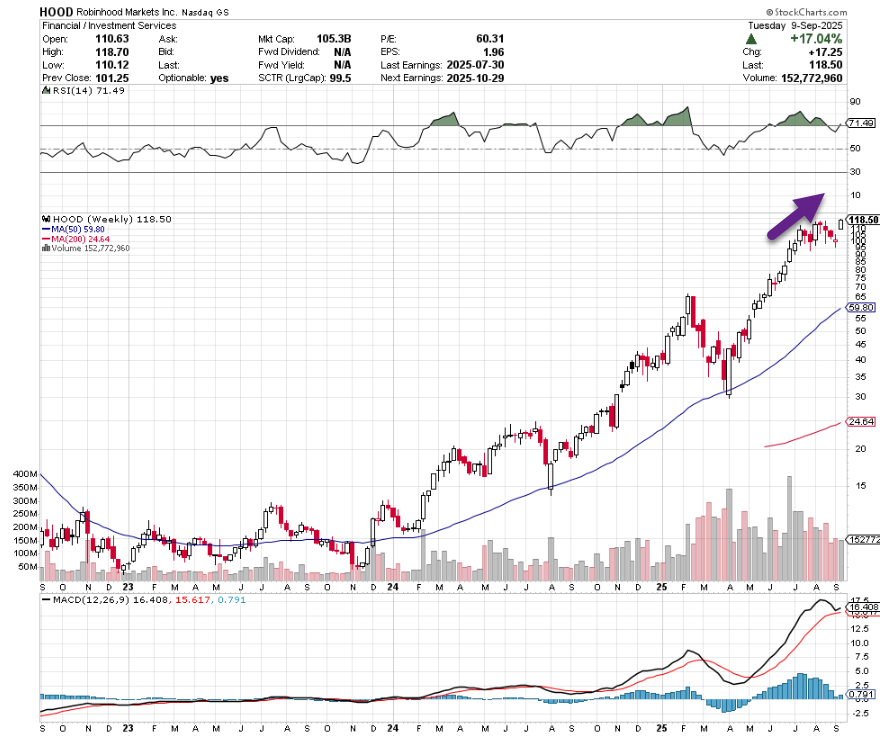

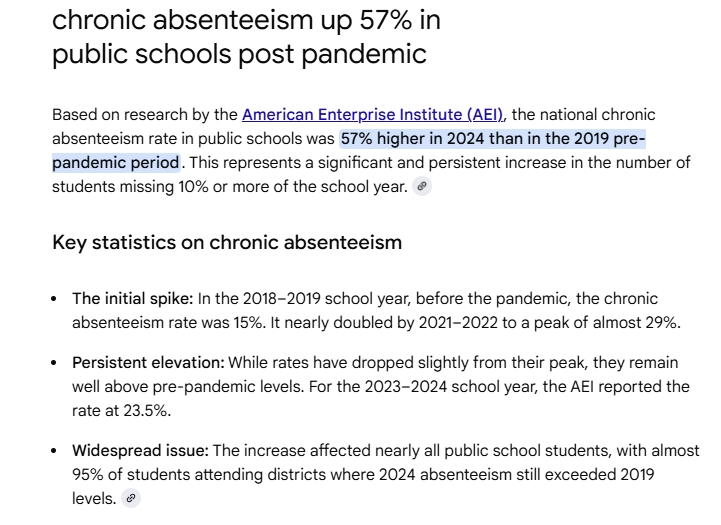

1. Quarterly S&P Earnings Being Market Up

SPX earnings. “Positive S&P 500 earnings revisions are very uncommon unless the US economy is coming out of a recession, so the Street’s recent bullishness on future index earnings is nothing short of remarkable.”

@

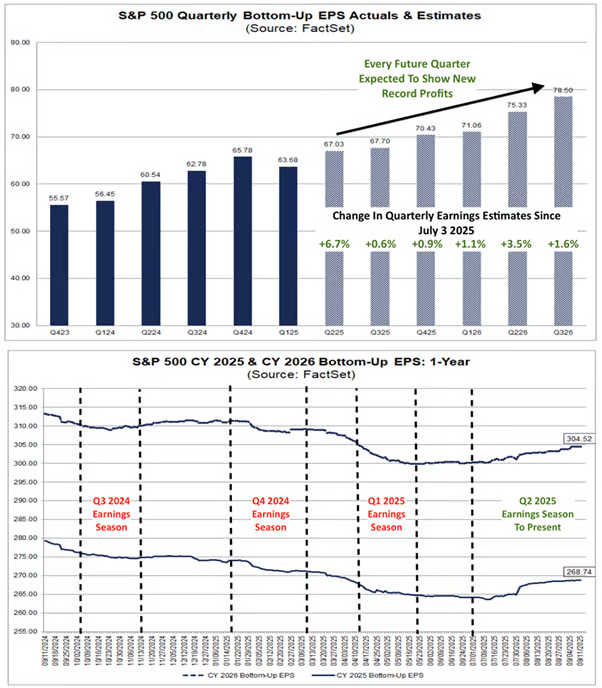

2. Nasdaq Win Streak Tied for Longest in 4 Years

This is now the longest winning streak for the Nasdaq 100 in nearly two years (November 2023) and tied for the longest since November 2021, or nearly four years! The longest daily winning streak in the index’s history was 19 back in May 1990, just two months before a July peak that led to a 33% decline in the subsequent weeks. We also found it notable that while extended winning streaks were relatively uncommon before 2009, they have become far more frequent in the last 15 years. For example, in the 23+ years from 1985 through 2008, there were just nine winning streaks of nine or more days, but in the last 16 years, there have been 13.

Bespoke

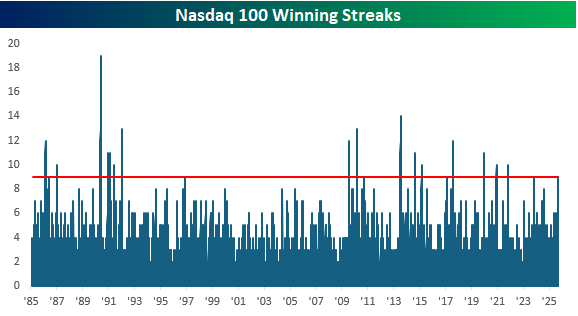

3. Institutional Investors 3rd Weekly Purchase of Tech Stocks in 5 Years

@KobeissiLetter

4. GOOGLE is Best Performing Mag 7 Stock 2025 …At Lowest Point this Year -24% on Fear of Losing Search to AI

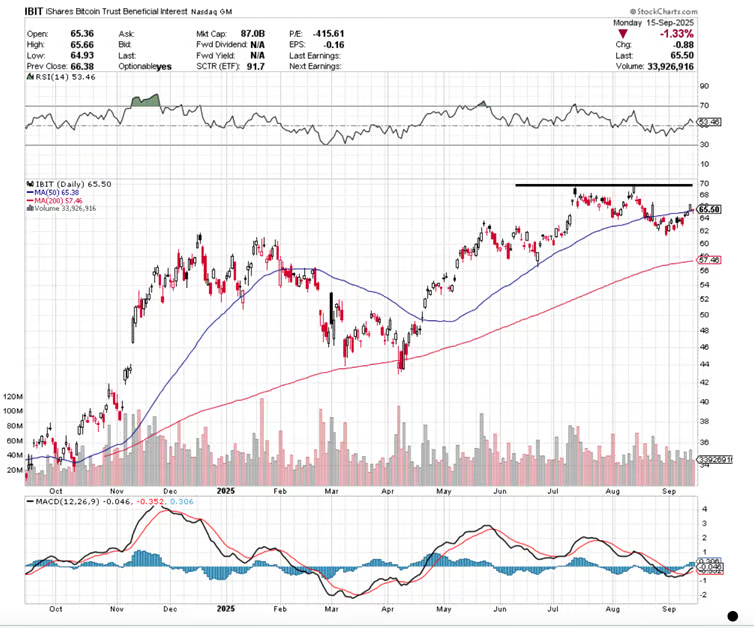

StockCharts

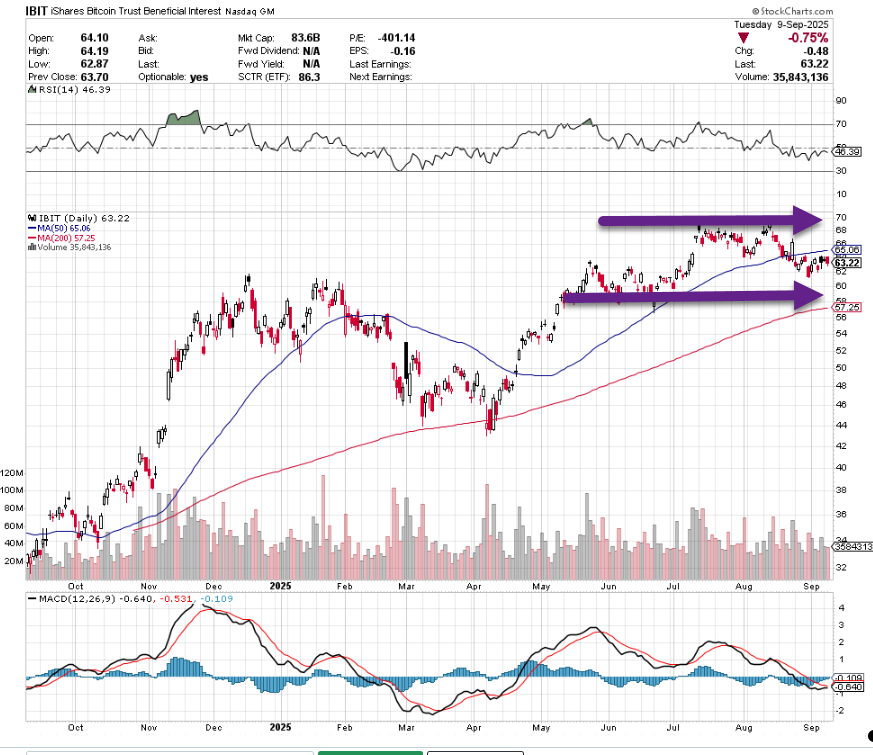

5. Bitcoin Did Not Make New Highs with QQQ

StockCharts

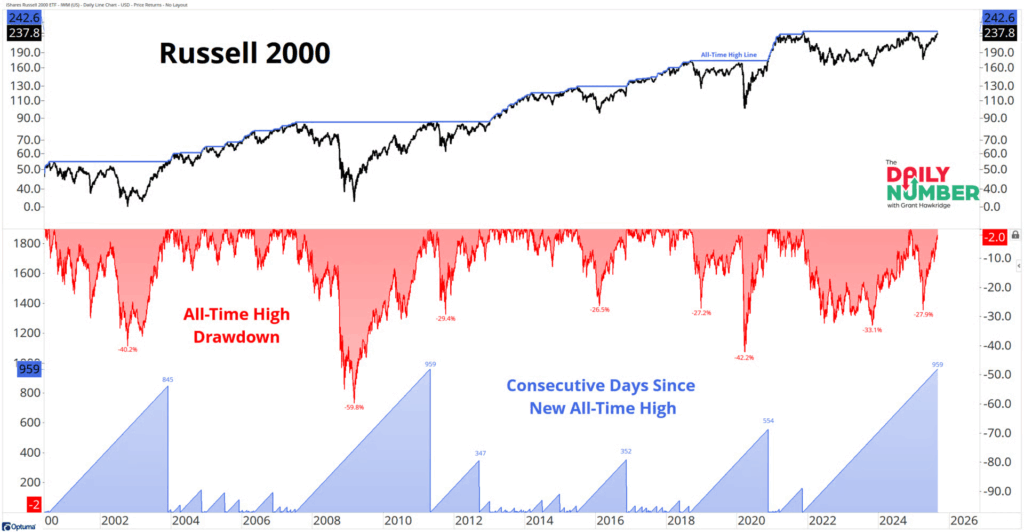

6. Small Cap One Tick from New Highs

StockCharts

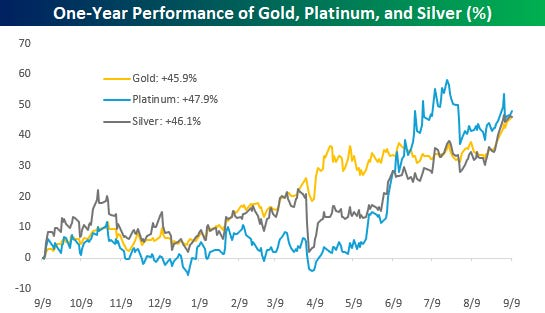

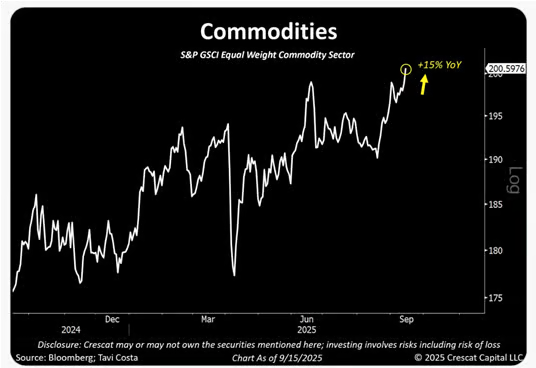

7. Commodities Equal Weight New Highs

Crescat Capital

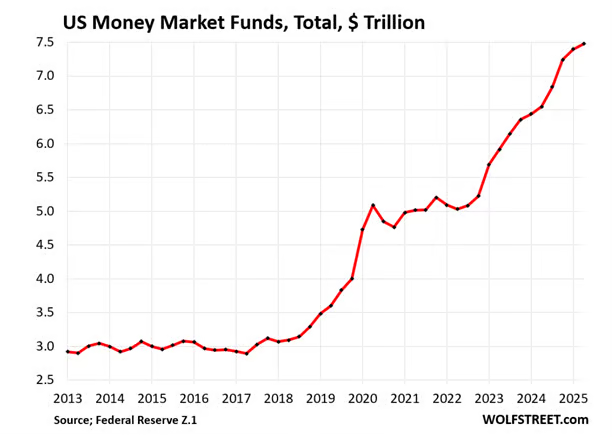

8. Money Markets Hit $7.5 Trillion Before Fed Cut Coming

Total MMFs (those held by households and institutions) rose by $83 billion in Q2 from Q1, and by $933 billion year-over-year, to $7.48 trillion. Since Q1 2022, balances have ballooned by $2.39 trillion.

WolfStreet

9. Bessent says US won’t hit China with tariffs over Russian oil unless Europe goes first

By David Lawder

- Europe needs to ‘do their share’ to cut off Russian oil revenues, Bessent says

- Bessent criticizes European countries for buying Russian oil, Indian refined products

- US to consider new Russian sanctions, uses for Russian assets, Bessent says

MADRID, Sept 15 (Reuters) – U.S. Treasury Secretary Scott Bessent said on Monday the Trump administration would not impose additional tariffs on Chinese goods to halt China’s purchases of Russian oil unless European countries hit China and India with steep duties of their own.

Bessent told Reuters and Bloomberg in a joint interview that European countries needed to play a stronger role in cutting off Russian oil revenues and bringing its war in Ukraine to an end.

10. 5 Tips to Make Fast Progress on Any Goal

Some strengths are only visible when you’re in action mode.-Psychology Today

We all have goals that languish on our mental should-do list. Goals we’re either taking no action or painfully slow action on.

Common examples:

- Home projects or de-cluttering

- Health-related goals, like incorporating more strength-training

- Systems-related goals, like becoming more organized at home or work

- Learning a new tool or technology, like AI

Here are 5 tips to make quick progress on any should-do. As a bonus, they’ll help you discover how taking action itself changes what seems possible and reveals strengths you already possess but only see when you’re in action-mode, not thinking-mode.

Jumpstarts That Work

Choose the one or two strategies that best suit your goal and your flavor of stuckness.

1. Try an Idea You’ve Been Thinking About

Most of us have more good ideas we don’t try than bad ideas we do try. Even finding out an idea didn’t work moves you forward because it takes that idea off your mind.

Try the best (or just quickest to implement) idea you’ve got now, rather than waiting for a better one.

2. Dedicate a Consistent, Weekly Slot for Several Weeks in a Row

I recently dealt with a health concern that felt very emotionally weighty. It was hard to find a balance between ignoring it completely or letting worry about it take over my life.

How did I handle it? For four Mondays in a row, I did something toward addressing it.

To give a real-world example: In week one, I ordered at-home testing supplies. In week two, I started using them. In week three, I got a blood test and emailed some leading researchers. In week four, I did a urine test (after picking up the cup at the blood draw) and read a 14-page document one of the researchers sent.

By the end, I had an annual plan to follow.

A key to this strategy is that your weekly slot should be for executing an action, not deciding what it will be, so plan accordingly.

When you start working, you’re no longer waiting. You’re influencing your outcomes, even when the problem feels scary.

3. Message Someone the Progress You’ve Made on the Goal, Each Monday, for the Next Four Mondays

I’ve been specific with the instructions for this tip to relieve you of some decision-making. Pick a well-regulated friend, therapist, work supervisor, or anyone you think might be a good person for this role.

Let them know what you’re working on, and quietly message them each week to tell them the progress you’ve made in the previous week. You don’t necessarily need to let the person know this is what you’re doing if you’d organically be having ongoing discussions anyway.

4. Give Up Looking for a Solution You’re Sure Will Work

We often hesitate until we’ve thought of an action we’re sure will work.

When I emailed researchers, I had no idea if any would reply, but one did and was extraordinarily helpful.

Here’s another example. My spouse is currently fixing something that’s broken at our house. She’s not sure if she needs to replace the entire unit that’s causing the problem or one part of it.

In these scenarios, back-of-the-napkin math can help you choose an action. Say the whole unit costs $150, and the part costs $20. She estimates there is a 50% chance that swapping the part will be enough.

That seems like a good trade-off.

Rather than trying to know for sure what needs replacing, she can experiment.

Solutions that work often weren’t guaranteed to work. If your anxiety is only managed by knowing a solution will work before trying it, you’ll miss out on solutions you only discover work after trying them.

5. Progress Through Showing Up, Not Planning

This is a completely different strategy that’s well-suited to some goals.

Let’s say you want to learn to use AI, but the possible routes to doing so feel overwhelming. Rather than focusing on a specific goal, spend around 10 hours exploring the tools and possibilities. See where that takes you.

You could take a similar approach to strength training. Commit to spending, say, ten 1-hour slots in the weight room at a gym. Explore. Try out different equipment rather than attempting to have efficient workouts.

Don’t have a gym membership? Get a one-week trial at one gym chain, then try another. Or get a cheap weekly or monthly pass at a community center gym that doesn’t require contracts.

Leverage putting yourself in a setting where action and progress will occur. Focus on exploration and time spent, not a specific outcome.

Develop Meta-Awareness of How Action Itself Transforms Your Thinking and Emotions

By applying any of these strategies, you’ll see actions reveal options, strengths, and solutions you hadn’t imagined.

Taking physical action toward a goal tends to revolutionize our relationship with that goal vs. when we’re just mentally marinating on it. If thinking is a more comfortable state for you than doing, you can marry the two by better appreciating the processes through which action is clarifying.

When we act, we recognize levers we can pull and variables we can influence that we hadn’t considered. Scary tasks, like my medical example, become less scary when we actually start taking effective action. We might realize a goal is harder or easier than we expected, and can adjust accordingly.

Taking action helps us realize the creativity, flexibility, and strength within us that mostly sit unused when we’re not making active progress. There can be fun in seeing what works that we didn’t expect. Our ideas become better after we’ve acted, not before. The problem-solving skills that strong thinkers possess aren’t fully evident until the results of your experiments require them.

When you understand how fast progress can influence your ideas and your self-perceptions, and you have some specific strategies to jumpstart you, this combination can help you make progress on pesky or scary should-dos that have weighed you down.

https://www.psychologytoday.com/ie/blog/in-practice/202509/5-tips-to-make-fast-progress-on-any-goal